- DEFINING THE PATH TO SUCCESS

定义成功之路

According to a report from PwC in association with the Open Data Institute, “Open Banking has the potential to create a revenue opportunity of at least GBP 7.2 Bn by 2022 across retail and SME markets.”

普华永道与开放数据研究所联合发布的一份报告称,“开放银行在2022年,有潜力在零售和中小企业市场创造至少72亿英镑收益的机会。”

Payments and account information services are the priority for banks and fintech companies over the short term.

支付和账户信息服务是短期内银行和金融科技公司的优先考虑的业务。

However, neither this forecast of direct revenues from Open Banking offerings, nor the current emphasis on consumer accounts and payments, give a true sense of the substantial impact this open paradigm will have on financial services.

然而,这种对开放银行产品直接收益的预测,以及目前对消费者账户和支付的强调,都没有真正意识到这种开放范式对金融服务的重大影响。

The opportunities and benefits of Open Banking will accrue not only to those with financial means and technology sophistication.

开放银行的机会和利益不仅会增加在具有雄厚财力和尖端技术的参与者身上。

Railsbank’s CEO Nigel Verdon comments: “There are 92 million unbanked adults in Europe, including the UK, today. The solutions that derive from API-based banking functionality will open up new modes of account access, such as by mobile device and online chat, and will eliminate barriers to individuals being eligible for low-cost accounts and robust support.”

Railsbank的首席执行官Nigel Verdon评论道:“今天,包括英国在内的欧洲有9200万无银行账户的成年人。源自基于API的银行功能解决方案将开辟新的帐户访问模式,例如通过移动设备和在线聊天,并且将消除个人获得低成本帐户和强大支持的资格的障碍。”

Success in Open Banking depends on number of factors, including customer adoption, regulatory standards, data sharing policies, and further API development.

开放银行的成功取决于多种因素,包括客户接纳,监管标准,数据共享政策以及进一步的API开发。

Customer adoption is the primary driver of success

客户接纳是成功的主要驱动力

Open Banking facilitates access through a variety of channels, including smartphone apps, chatbot-fronted social media accounts, and voice-activated home controls.

开放银行通过各种渠道促进访问,包括智能手机应用,聊天机器人社交媒体帐户、以及语音激活房屋控制。

Would-be competitors must invest in user experience design skills, or partner with a firm that possesses these.

想要成为竞争者必须用户体验设计能力上投资,或与拥有这些能力的公司合作。

Jamie Campbell of Bud highlights “the barrier to market entry is much lower when all you need is to download an app. For example, buy a new smart phone and access an app to be evaluated for product financing on the spot. Compelling apps will drive user adoption, overcoming hesitancies about sharing personal data.”

Bud的Jamie Campbell强调,“当你需要做的仅仅是下载一个应用时,进入市场的障碍要低得多。例如,购买新的智能手机并访问应用,以便立刻评估产品融资。明星应用将推动用户接纳,克服有关共享个人数据的顾虑。”

Still, regulators will strive to better protect their citizens’ rights with respect to data privacy and sharing with permission.

尽管如此,监管机构仍将努力在数据隐私和许可共享方面更好地保护公民的权利。

“Individuals have become much more sophisticated in understanding how their data is used to target them. As such, consent and transparency are paramount,” according to Amir Nooriala of OakNorth.

OakNorth的Amir Nooriala表示,“个人在理解他们的数据如何被用于定位他们时变得更加微妙。因此,用户同意和透明至关重要”。

In Europe, 2018’s effective date for the Global Data Protection Regulation (GDPR) is a major step toward ameliorating these concerns. Company executives, marketers, lawyers and technologists must focus proactively on understanding data privacy trends in order to respect the rights of customers while effectively marketing and delivering their offerings.

在欧洲,2018年全球数据保护法规(GDPR)的生效日,是改善这些问题的重要一步。公司高管、营销人员、律师和技术人员必须积极关注明白数据隐私趋势,以便在有效营销和提供产品时尊重客户的权利。

Policies or initiatives that will help drive growth of Open Banking

有助于推动开放银行发展的政策或举措

Strong customer authentication and data security policies: Customers need to feel they have complete control over personal or business data that is to be shared with other third-parties.

强客户身份验证和数据安全策略:客户需要感觉到他们可以完全控制个人或业务数据与其他第三方共享。Increased connectivity, customer awareness, and best practices: Banks and fintech players need to collaborate and even share best practices in order to create a trusted ecosystem. Banks and regulatory agencies need to expand customer awareness by explaining the benefits of Open Banking and what value it adds for customers. The connectivity to different platforms and services would be the key for customers to truly enjoy the unified experience.

提高连通性、客户意识和最佳实践:银行和金融科技公司需要协作甚至分享最佳实践,以创建可信赖的生态系统。银行和监管机构需要通过解释开放银行的好处以及它为客户增加的价值来增强客户意识。与不同平台和服务的连接,将是客户真正享受统一体验的关键。-

Governance framework and trust: Commonly-accepted governance policies need to be established in order for customers to select trusted TPPs. For example, a publically available directory of apps approved by the regulator should be maintained.

治理框架和信任:需要建立普遍接受的治理策略,以便客户选择可信的第三方提供商。例如,应维护被监管机构批准为可用应用的公开目录。

image.png

image.png

API and solution areas to prioritize

API和解决方案领域的优先顺序

Nigel Verdon of Railsbank, points out that “the current Open Banking standards define a limited number of functions. In of themselves, API specifications like those in PSD2 will be insufficient to fulfill market demand [for revamped financial services]. We must look to customer-centric innovators – not just technical and regulatory committees – to hone in on the next generation of compelling applications and the APIs needed to support them.” Railsbank的Nigel Verdon指出,“目前的开放银行标准定义了数量有限的功能。就其本身而言,PSD2中的API规范不足以满足[改进的金融服务]市场需求。我们必须寻求以客户为中心的创新者 - 而不仅仅是技术和监管委员会 - 来打磨下一代明星应用以及支持它们所需的API。”

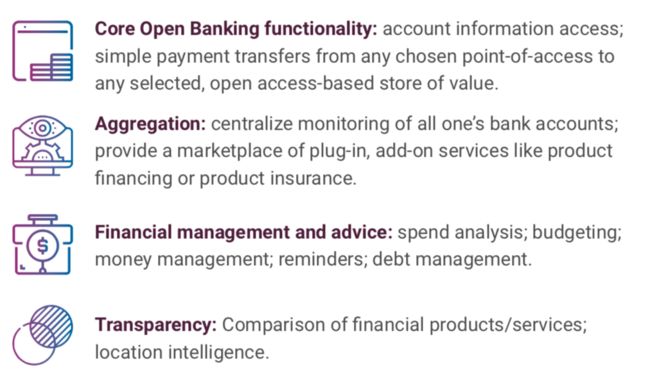

To play a leading role in Open Banking, organizations may choose to focus on one or more of the following areas of current open APIs or APIs that need standardization (in the cases of “Extensions to core functionality” and “Other financial services” below):

要在开放银行中发挥主导作用,组织可以选择关注当前开放API或需标准化API的一个或多个领域(在以下“核心功能扩展”和“其他金融服务”的方面) :

Core Open Banking functionality: account information access; simple payment transfers from any chosen point-of-access to any selected, open access-based store of value.

开放银行核心功能:帐户信息访问;任何选定的接入点间的简单支付,开放基于访问的有价值存储。

Aggregation: centralize monitoring of all one’s bank accounts; provide a marketplace of plug-in, add-on services like product financing or product insurance.

聚合:集中监控某人的所有银行账户;提供插件市场,如产品融资或产品保险等的附加服务。

Financial management and advice: spend analysis; budgeting; money management; reminders; debt management.

金融管理和咨询:支出分析;预算;资金管理;提醒;债务管理。

Transparency: Comparison of financial products/services; location intelligence.

透明性:金融产品/服务的比较;智能定位。

Security & trust: strong authentication & authorization; fraud management/alerts.

安全和信任:强身份验证和授权;欺诈管理/警告。

Connect & control: directory of regulated/ registered third-party providers; connectivity among service providers.

连接和控制:受监管/注册的第三方提供商的目录;服务提供商之间的连接。

Extensions to core Open Banking functionality: multi-destination payments; creation of IBANs / new bank account numbers; issuance of credit/ debit cards; currency conversion.

开放银行核心功能的扩展:多目的地支付;创建IBAN /新的银行帐号;发行信用卡/借记卡;货币转换。

(注:IBANs International Bank Account Number 国际银行账号)

Other financial services ripe for open-access standards: invoice presentation and accounts/receivable reconciliation; robo-advising/aggregation of securities-holding accounts.

开放访问标准成熟的其他金融服务:出具付款通知和账户/应收账款对账;证券持有账户的智能顾问/汇总。

A time to revisit business strategy

是时候重新审视业务战略了

Frank Rotman, Partner at QED Investors, offers a compelling analogy about the state of banking. Just as Copernicus revolutionized the world’s view of itself by asserting that the Earth isn’t the center of the universe, the Open Banking wave will revolutionize the financial services industry by asserting the customer (not the bank) as true center of its universe.

QED Investors合伙人Frank Rotman提供了一个关于银行业状况的引人入胜的类比。正如哥白尼通过断言地球不是宇宙的中心而革新了世界对自身的看法,开放银行的浪潮也将通过宣称客户(而非银行)作为其宇宙真正的中心来彻底改变金融服务业。

Practically speaking, banks must carefully evaluate their long-term operational, distribution, and collaboration strategies. More targeted customer segment selection, plus concentration on core in-house expertise, and outsourcing of auxiliary front-end or back-end processes and software will allow them to act more nimbly.

实际上,银行必须仔细评估其长期运营、分销和协作战略。更有针对性地选择客户群,加强内部核心专业能力,以及前端或后端流程和软件的辅助外包,将使他们能够更灵活地采取行动。

Fintechs meanwhile must continually refine their strategies, targeting a value-chain niche and building a defensible moat. Available business models include user experience design, financial information aggregation, analytics & insights, application marketplaces, financial service/price comparison malls, and technology integration gateways.

同时,金融科技公司必须不断完善自己的战略,瞄准价值链利基并建立防御性护城河。可用的商业模式包括用户体验设计,财务信息汇总、分析和见解,应用市场,金融服务/价格比较场以及技术集成网关。

Although 2018 remains early in terms of Open Banking implementation, the future is clearly a dynamic one and the time to prepare is now.

虽然2018年在开放银行实施方面仍然处于早期阶段,但显然是一个充满活力的未来,准备就是现在。

Key characteristics of winners in Open Banking

开放银行成功者的主要特征

Winners are the early adaptors who maintain flexibility in implementing Open Banking APIs and expand their data collaboration capabilities in line with fintech and third-party players.

成功者都是早期的采用者,他们在实施Open Banking API方面保持灵活性,并根据金融科技公司和第三方合作伙伴扩展其数据合作能力。Winners will focus on educating their customers about the value of Open Banking.

成功者专注于向客户宣传开放银行的价值。Winners will not only develop an API marketplace/ecosystem but also collaborate with other technology providers/fintech start-ups to build end to-end solutions. Moreover, banks need to differentiate themselves from fintech competition to ensure total customer satisfaction.

成功者不仅开发API市场/生态系统,还将与其他技术提供商/金融科技初创企业合作,共同构建端到端解决方案。此外,银行需要从金融科技竞争中脱颖而出,以确保整体的客户满意。Winners will embrace new technology, digital tools, modular and nimble IT architectures,and operational capabilities to facilitate transformation within the organization. Winners will offer easy- to-use functionality or usability in the front end.

成功者将采用新技术、数字工具、模块化且灵活的IT架构以及运营能力,以促进组织内的转型。胜利者将在前端提供易用的功能或操作。Winners will focus on automation, strong authentication and risk management process, data governance, and cyber security.

成功者将专注于自动化、强身份验证和风险管理流程、数据治理和网络安全。Winners will have a comprehensive customer data control framework and will share the issues or concerns related to data security or operational issues to regulators.

成功者拥有全面的客户数据控制框架,并向监管机构分享与数据安全或运营问题相关的意见或疑虑。Winners will adopt a customer- centric digital strategy in order to offer better usability and convenience to customers.

成功者采用以客户为中心的数字战略,以便为客户提供更好的可用性和便利性。