7天微课程day7——完整项目:用Python预测法国香槟的月销量

声明:

终于到最后一天了,开不开心,激不激动?来瓶香槟奖励一下自己。

然后今天的任务很艰巨….毕竟最后一天了,笔者也有点小激动,可能行文风格有点飘,哈哈不要见怪。

另外,再安利一波,加入这个机器学习社区跟着大神Jason一起学习吧。

用Python预测法国香槟的月销量

要做好时间序列预测,唯一的方法就是实践。practice, practice, practice.

在本教程中,你将懂得如何用Python预测法国香槟的月销量。再看完本文后,你应该知道:

- 如何查看自己的Python开发环境,如何定义一个时间序列预测的问题(在生产中,定义问题的人往往是leader,提出idea的是骨干,写代码的是o(╥﹏╥)o)。

- 如何划分训练集和测试集,如何建立一个baseline,如何初步分析时间序列。

- 如何构建一个ARIMA模型,保存该模型,在此之后,加载并预测新时刻的值。

Overview

这是一个端到端的项目,从下载数据到定义问题,从训练模型到作出预测,都包含在内。

该项目不追求最精准的预测,目的只是为了教学。本文分为一下几步:

- Environment

- Problem Description

- Trainset and Testset

- Baseline

- Data Analysis

- ARIMA Models

- Model Validation

我们会提供一条时间序列预测的模板,这样你可以将它套用在你自己的时间序列上。

1. Environment

确保你电脑上有这些包:

- Scipy

- Numpy

- Matplotlib

- Pandas

- scikit-learn

- statsmodels

# 下列代码可以帮助你检查你的包的版本

# scipy

import scipy

print('scipy: %s' % scipy.__version__)

# numpy

import numpy

print('numpy: %s' % numpy.__version__)

# matplotlib

import matplotlib

print('matplotlib: %s' % matplotlib.__version__)

# pandas

import pandas

print('pandas: %s' % pandas.__version__)

# scikit-learn

import sklearn

print('sklearn: %s' % sklearn.__version__)

# statsmodels

import statsmodels

print('statsmodels: %s' % statsmodels.__version__)2. Problem Description

数据集下载链接,下完后记得将数据集重命名为champagne.csv,并检查数据文件,去掉乱码和无用的文字。

该数据集是1964-1972年香槟的月销量。very interesting, right?

3. Trainset and Testset

划分数据集,并确定模型评估的策略

划分测试集

from pandas import Series

series = Series.from_csv('champagne.csv', header=0)

split_point = len(series) - 12

dataset, validation = series[0:split_point], series[split_point:]

print('Dataset %d, Validation %d' % (len(dataset), len(validation)))

dataset.to_csv('dataset.csv')

validation.to_csv('validation.csv')

'''output

Dataset 93, Validation 12

'''如果你的输出不是这个,说明代码或者数据文件有问题,check it!

我们现在将数据集划分为两个:

- dataset.csv: 1964.1-1971.9共93个观测值

- validation.csv: 1971.10-1971.9共12个观测值

测试集差不多占了整个数据集的11%。

模型评估

度量准则

Mean Squared Error(MSE)通常作为回归预测的度量准则。在这里,我们为了让error的单位和原始数据的单位一致,选择Root Mean Squared Error(RMSE). 伪代码如下:

from sklearn.metrics import mean_squared_error

from math import sqrt

...

predictions = ...

mse = mean_squared_error(test, predictions)

rmse = sqrt(mse)

print('RMSE: %.3f' % rmse)如何预测

用walk-forward的方式,也就是一步一步的预测,或者成为rolling-forecast. 具体步骤如下:

- 用训练数据训练模型

- 遍历测试集中的每个观测值,一步一步的预测,每一步要做的是,设当前时刻为t:

- 一步预测,预测 t t 时刻的值并保存

- 将

test[t]加入训练集 - 用新的训练集重新训练模型

- 最后得到所有的预测值序列,将其与test中的数据比较,计算RSME

# prepare data

X = series.values

X = X.astype('float32')

train_size = int(len(X) * 0.5)

train, test = X[0:train_size], X[train_size:]# walk-forward validation

history = [x for x in train]

predictions = list()

for i in range(len(test)):

# predict

yhat = ...

predictions.append(yhat)

# observation

obs = test[i]

history.append(obs)

print('>Predicted=%.3f, Expected=%3f' % (yhat, obs))4. Baseline

还记得在day4中我们这么获得baseline的吗?

from pandas import Series

from sklearn.metrics import mean_squared_error

from math import sqrt

# load data

series = Series.from_csv('dataset.csv')

# prepare data

X = series.values

X = X.astype('float32')

train_size = int(len(X) * 0.50)

train, test = X[0:train_size], X[train_size:]

# walk-forward validation

history = [x for x in train]

predictions = list()

for i in range(len(test)):

# predict

yhat = history[-1]

predictions.append(yhat)

# observation

obs = test[i]

history.append(obs)

print('>Predicted=%.3f, Expected=%3.f' % (yhat, obs))

# report performance

mse = mean_squared_error(test, predictions)

rmse = sqrt(mse)

print('RMSE: %.3f' % rmse)

'''output

...

>Predicted=4676.000, Expected=5010

>Predicted=5010.000, Expected=4874

>Predicted=4874.000, Expected=4633

>Predicted=4633.000, Expected=1659

>Predicted=1659.000, Expected=5951

RMSE: 3186.501

'''5. Data Analysis

这是day3中的内容。

Summary Statistics

from pandas import Series

series = Series.from_csv('dataset.csv')

print(series.describe())

'''output

count 93.000000

mean 4641.118280

std 2486.403841

min 1573.000000

25% 3036.000000

50% 4016.000000

75% 5048.000000

max 13916.000000

'''首先,均值是4641,可以知道我们预测的值应该也在这个附近。

然后,方差较大,分位点的值差异较大,说明香槟销量分布比较分散。

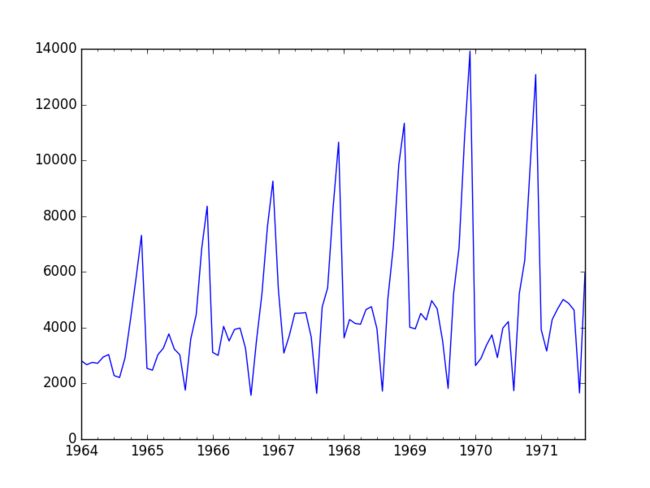

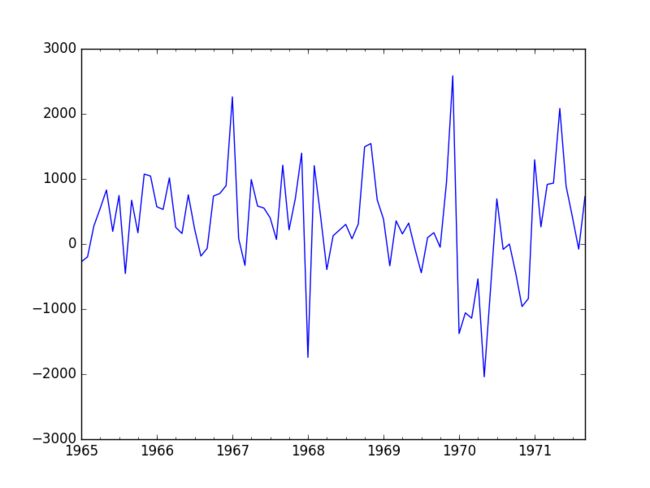

Line Plot

from pandas import Series

from matplotlib import pyplot

series = Series.from_csv('dataset.csv')

series.plot()

pyplot.show()

- 有随时间上涨的总体趋势

- 季节特征明显

- 看起来,要对这个时间序列建模比较复杂

- 没有明显的异常值

- 该时间序列明显是不平稳的

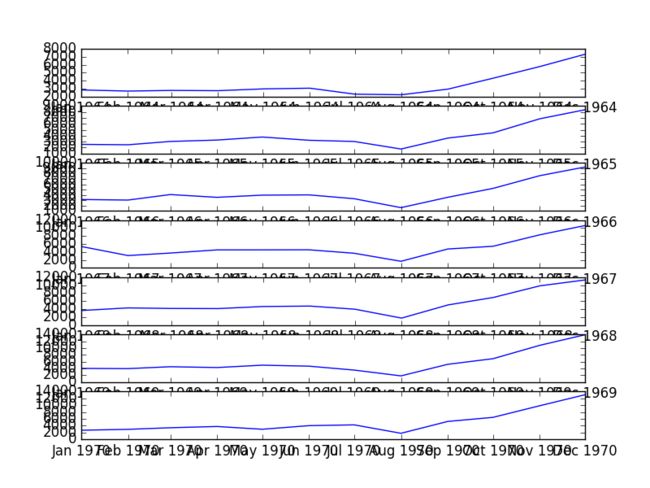

Seasonal Line Plots

# 对1964-1970每一年按月份花了折线图

from pandas import Series

from pandas import DataFrame

from pandas import TimeGrouper

from matplotlib import pyplot

series = Series.from_csv('dataset.csv')

groups = series['1964':'1970'].groupby(TimeGrouper('A'))

years = DataFrame()

pyplot.figure()

i = 1

n_groups = len(groups)

for name, group in groups:

pyplot.subplot((n_groups*100) + 10 + i)

i += 1

pyplot.plot(group)

pyplot.show()

虽然他们的纵坐标不一样,但是大体趋势比较一致,都是在下半年逐渐增高并在年末到达顶峰。

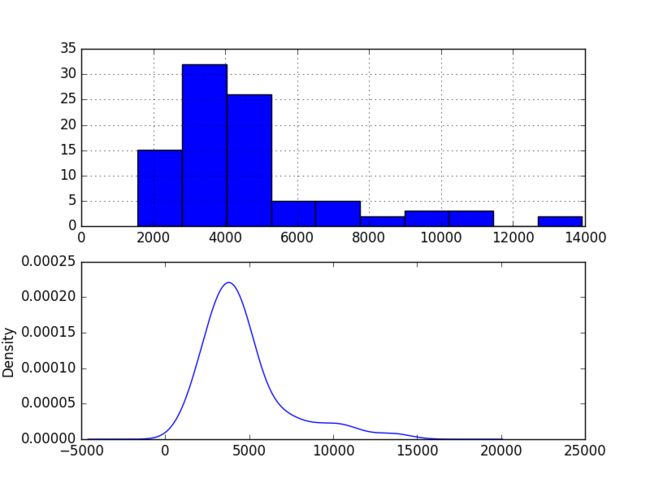

Density Plot

from pandas import Series

from matplotlib import pyplot

series = Series.from_csv('dataset.csv')

pyplot.figure(1)

pyplot.subplot(211)

series.hist()

pyplot.subplot(212)

series.plot(kind='kde')

pyplot.show()

不是高斯分布,在右侧有一个长拖尾

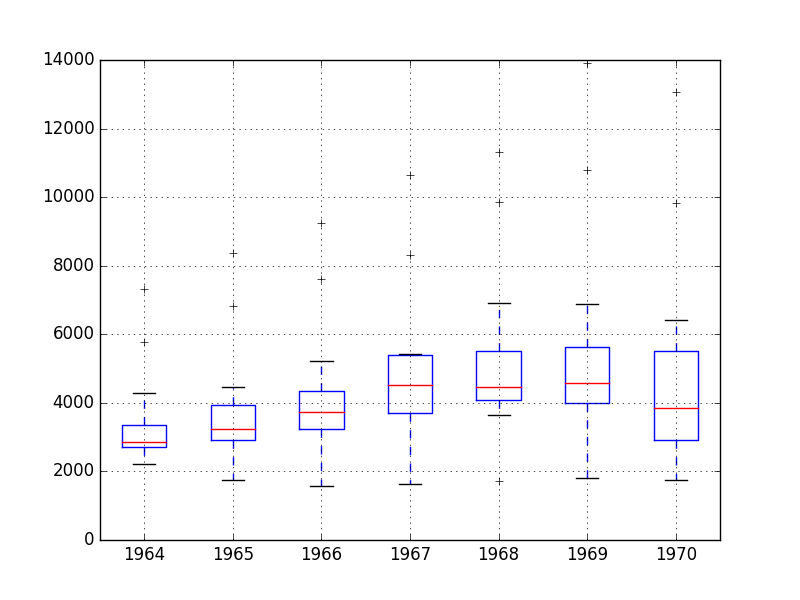

Box and Whisker Plots

from pandas import Series

from pandas import DataFrame

from pandas import TimeGrouper

from matplotlib import pyplot

series = Series.from_csv('dataset.csv')

groups = series['1964':'1970'].groupby(TimeGrouper('A'))

years = DataFrame()

for name, group in groups:

years[name.year] = group.values

years.boxplot()

pyplot.show()

懒得解释了,因为这个数据集的特征很明显,只通过一个直线图就能cover所有点了。但是对于新的数据集,这些可视化手段必不可少,说不定会发现什么对预测有用的信息呢。

6. ARIMA Models

选择ARIMA初始参数

ARIMA模型首先要确定(p, d, q)的值以及其他一些初始化参数。

很明显香槟销量时间序列是非平稳的,我们先差分,再检查序列的平稳性,确保最后处理的是平稳序列。

在前面的可视化分析中,我们发现这个上涨的趋势存在于年-年中,而不是月-月,所以我们用相邻年份相同月份做差分,相当于12步差分。

from pandas import Series

from statsmodels.tsa.stattools import adfuller

from matplotlib import pyplot

# create a differenced series

def difference(dataset, interval=1):

diff = list()

for i in range(interval, len(dataset)):

value = dataset[i] - dataset[i - interval]

diff.append(value)

return Series(diff)

series = Series.from_csv('dataset.csv')

X = series.values

X = X.astype('float32')

# difference data

months_in_year = 12

stationary = difference(X, months_in_year)

stationary.index = series.index[months_in_year:]

# check if stationary

result = adfuller(stationary)

print('ADF Statistic: %f' % result[0])

print('p-value: %f' % result[1])

print('Critical Values:')

for key, value in result[4].items():

print('\t%s: %.3f' % (key, value))

# save

stationary.to_csv('stationary.csv')

# plot

stationary.plot()

pyplot.show()

'''output

ADF Statistic: -7.134898

p-value: 0.000000

Critical Values:

5%: -2.898

1%: -3.515

10%: -2.586

'''ADF Statistic的值比下面5%、1%、10%的值都要下,说明现在序列是平稳的。

接下来我们处理的就是差分后的时间序列,并且可以确定参数d=0。

当然,如果需要的话,这些差分后的时间序列可以在反转成原始序列,该函数为:

# invert differenced value

def inverse_difference(history, yhat, interval=1):

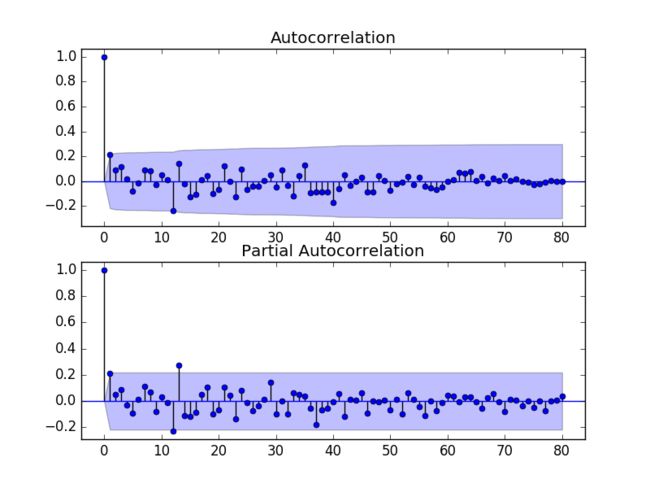

return yhat + history[-interval]下一步是为AR和MA选择参数p和q,这要借助Autocorrelation Function(ACF) 和Partial Autocorrelation Function(PACF)。

Note:我们现在用的是平稳序列stationary.csv

from pandas import Series

from statsmodels.graphics.tsaplots import plot_acf

from statsmodels.graphics.tsaplots import plot_pacf

from matplotlib import pyplot

series = Series.from_csv('stationary.csv')

pyplot.figure()

pyplot.subplot(211)

plot_acf(series, ax=pyplot.gca())

pyplot.subplot(212)

plot_pacf(series, ax=pyplot.gca())

pyplot.show()

ACF的截断点在1处,取

p=1;PACF的截断点有1、11和12,先取q=1。

现在确定ARIMA(1, 0, 1),但是实验显示这种建立在差分序列上的ARIMA(1, 0, 1)模型的表现不如建立在差分序列上的ARIMA(1, 1, 1)模型,所以我们用后者。

from pandas import Series

from sklearn.metrics import mean_squared_error

from statsmodels.tsa.arima_model import ARIMA

from math import sqrt

# create a differenced series

def difference(dataset, interval=1):

diff = list()

for i in range(interval, len(dataset)):

value = dataset[i] - dataset[i - interval]

diff.append(value)

return diff

# invert differenced value

def inverse_difference(history, yhat, interval=1):

return yhat + history[-interval]

# load data

series = Series.from_csv('dataset.csv')

# prepare data

X = series.values

X = X.astype('float32')

train_size = int(len(X) * 0.50)

train, test = X[0:train_size], X[train_size:]

# walk-forward validation

history = [x for x in train]

predictions = list()

for i in range(len(test)):

# difference data

months_in_year = 12

diff = difference(history, months_in_year)

# predict

model = ARIMA(diff, order=(1, 1, 1))

model_fit = model.fit(trend='nc', disp=0) # trend='nc'表示no constant

yhat = model_fit.forecast()[0]

yhat = inverse_difference(history, yhat, months_in_year)

predictions.append(yhat)

# observation

obs = test[i]

history.append(obs)

print('>Predicted=%.3f, Expected=%3.f' % (yhat, obs))

# report performance

mse = mean_squared_error(test, predictions)

rmse = sqrt(mse)

print('RMSE: %.3f' % rmse)

'''output

...

>Predicted=3157.018, Expected=5010

>Predicted=4615.082, Expected=4874

>Predicted=4624.998, Expected=4633

>Predicted=2044.097, Expected=1659

>Predicted=5404.428, Expected=5951

RMSE: 956.942

'''Grid Search ARIMA Hyperparameters

设置搜索区间:

- p: 0-6

- d: 0-2

- q: 0-6

一共有7*3*7=147中组合。记得我们之前可视化PACF时,q的推荐值有11和12,但是实验表明,这些选择不可行。

import warnings

from pandas import Series

from statsmodels.tsa.arima_model import ARIMA

from sklearn.metrics import mean_squared_error

from math import sqrt

import numpy

# create a differenced series

def difference(dataset, interval=1):

diff = list()

for i in range(interval, len(dataset)):

value = dataset[i] - dataset[i - interval]

diff.append(value)

return numpy.array(diff)

# invert differenced value

def inverse_difference(history, yhat, interval=1):

return yhat + history[-interval]

# evaluate an ARIMA model for a given order(p, d, q) and return RMSE

def evaluate_arima_model(X, arima_order):

# prepare training dataset

X = X.astype('float32')

train_size = int(len(X) * 0.50)

train, test = X[0:train_size], X[train_size:]

history = [x for x in train]

# make predictions

predictions = list()

for t in range(len(test)):

# difference data

months_in_year = 12

diff = difference(history, months_in_year)

model = ARIMA(diff, order=arima_order)

model_fit = model.fit(trend='nc', disp=0)

yhat = model_fit.forecast()[0]

yhat = inverse_difference(history, yhat, months_in_year)

predictions.append(yhat)

history.append(test[t])

# calculate out of sample error

mse = mean_squared_error(test, predictions)

rmse = sqrt(mse)

return rmse

# evaluate combinations of p, d and q values for an ARIMA model

def evaluate_models(dataset, p_values, d_values, q_values):

dataset = dataset.astype('float32')

best_score, best_cfg = float("inf"), None

for p in p_values:

for d in d_values:

for q in q_values:

order = (p,d,q)

try:

mse = evaluate_arima_model(dataset, order)

if mse < best_score:

best_score, best_cfg = mse, order

print('ARIMA%s RMSE=%.3f' % (order,mse))

except:

continue

print('Best ARIMA%s RMSE=%.3f' % (best_cfg, best_score))

# load dataset

series = Series.from_csv('dataset.csv')

# evaluate parameters

p_values = range(0, 7)

d_values = range(0, 3)

q_values = range(0, 7)

warnings.filterwarnings("ignore")

evaluate_models(series.values, p_values, d_values, q_values)

'''output

...

ARIMA(5, 1, 2) RMSE=1003.200

ARIMA(5, 2, 1) RMSE=1053.728

ARIMA(6, 0, 0) RMSE=996.466

ARIMA(6, 1, 0) RMSE=1018.211

ARIMA(6, 1, 1) RMSE=1023.762

Best ARIMA(0, 0, 1) RMSE=939.464

'''发现最好的模型参数是ARIMA(0, 0, 1)

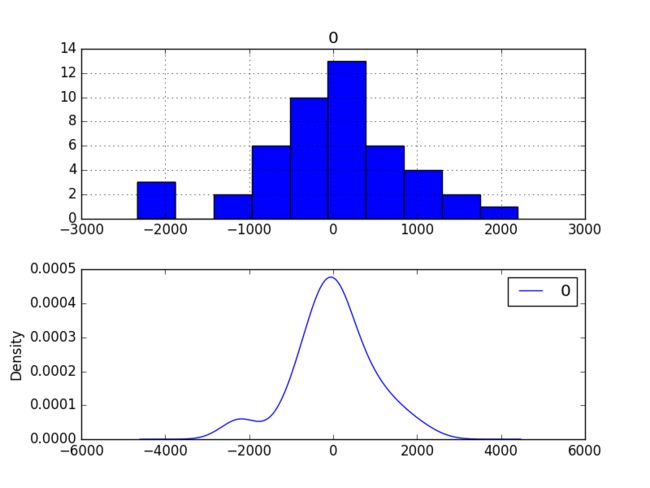

Review Residual Errors

Residual Errors应该是均值为0的高斯分布。

...

# walk-forward validation

history = [x for x in train]

predictions = list()

for i in range(len(test)):

# difference data

months_in_year = 12

diff = difference(history, months_in_year)

# predict

model = ARIMA(diff, order=(0,0,1))

model_fit = model.fit(trend='nc', disp=0)

yhat = model_fit.forecast()[0]

yhat = inverse_difference(history, yhat, months_in_year)

predictions.append(yhat)

# observation

obs = test[i]

history.append(obs)

# errors

residuals = [test[i]-predictions[i] for i in range(len(test))]

residuals = DataFrame(residuals)

print(residuals.describe())

# plot

pyplot.figure()

pyplot.subplot(211)

residuals.hist(ax=pyplot.gca())

pyplot.subplot(212)

residuals.plot(kind='kde', ax=pyplot.gca())

pyplot.show()

'''output

count 47.000000

mean 165.904728

std 934.696199

min -2164.247449

25% -289.651596

50% 191.759548

75% 732.992187

max 2367.304748

'''

我们可以在每个预测值上减去165.904728来中和residual error。

...

# walk-forward validation

history = [x for x in train]

predictions = list()

bias = 165.904728

for i in range(len(test)):

# difference data

months_in_year = 12

diff = difference(history, months_in_year)

# predict

model = ARIMA(diff, order=(0,0,1))

model_fit = model.fit(trend='nc', disp=0)

yhat = model_fit.forecast()[0]

yhat = bias + inverse_difference(history, yhat, months_in_year)

predictions.append(yhat)

# observation

obs = test[i]

history.append(obs)

# report performance

mse = mean_squared_error(test, predictions)

rmse = sqrt(mse)

print('RMSE: %.3f' % rmse)

# errors

residuals = [test[i]-predictions[i] for i in range(len(test))]

residuals = DataFrame(residuals)

print(residuals.describe())

# plot

pyplot.figure()

pyplot.subplot(211)

residuals.hist(ax=pyplot.gca())

pyplot.subplot(212)

residuals.plot(kind='kde', ax=pyplot.gca())

pyplot.show()

'''output

RMSE: 924.699

count 4.700000e+01

mean 4.965016e-07

std 9.346962e+02

min -2.330152e+03

25% -4.555563e+02

50% 2.585482e+01

75% 5.670875e+02

max 2.201400e+03

'''

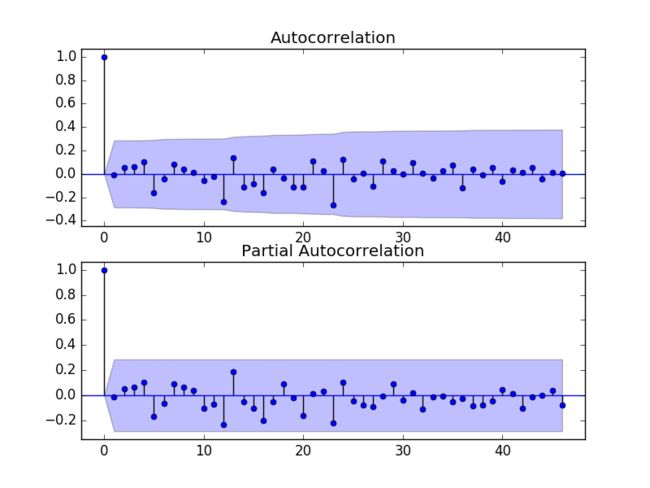

我们还可以检查残差序列的相关性,为残差序列绘制ACF和PACF:

...

# walk-forward validation

history = [x for x in train]

predictions = list()

for i in range(len(test)):

# difference data

months_in_year = 12

diff = difference(history, months_in_year)

# predict

model = ARIMA(diff, order=(0,0,1))

model_fit = model.fit(trend='nc', disp=0)

yhat = model_fit.forecast()[0]

yhat = inverse_difference(history, yhat, months_in_year)

predictions.append(yhat)

# observation

obs = test[i]

history.append(obs)

# errors

residuals = [test[i]-predictions[i] for i in range(len(test))]

residuals = DataFrame(residuals)

print(residuals.describe())

# plot

pyplot.figure()

pyplot.subplot(211)

plot_acf(residuals, ax=pyplot.gca())

pyplot.subplot(212)

plot_pacf(residuals, ax=pyplot.gca())

pyplot.show()

可以看到没有相关性强的点。

7. Model Validation

Finalize Model

应用ARIMA(0, 0, 1)训练并保存模型。

from pandas import Series

from statsmodels.tsa.arima_model import ARIMA

from scipy.stats import boxcox

import numpy

# create a differenced series

def difference(dataset, interval=1):

diff = list()

for i in range(interval, len(dataset)):

value = dataset[i] - dataset[i - interval]

diff.append(value)

return diff

# load data

series = Series.from_csv('dataset.csv')

# prepare data

X = series.values

X = X.astype('float32')

# difference data

months_in_year = 12

diff = difference(X, months_in_year)

# fit model

model = ARIMA(diff, order=(0,0,1))

model_fit = model.fit(trend='nc', disp=0)

# bias constant, could be calculated from in-sample mean residual

bias = 165.904728

# save model

model_fit.save('model.pkl')

numpy.save('model_bias.npy', [bias])上述代码创建两个文件:

- model.pkl: 这里保存的ARIMAResult对象。

- model_bias.npy: 这是当前模型的残差偏执,就是前面我们在每一步预测后都减去的值165.904728。

Make Prediction

from pandas import Series

from statsmodels.tsa.arima_model import ARIMAResults

import numpy

# invert differenced value

def inverse_difference(history, yhat, interval=1):

return yhat + history[-interval]

series = Series.from_csv('dataset.csv')

months_in_year = 12

model_fit = ARIMAResults.load('model.pkl')

bias = numpy.load('model_bias.npy')

yhat = float(model_fit.forecast()[0])

yhat = bias + inverse_difference(series.values, yhat, months_in_year)

print('Predicted: %.3f' % yhat)

'''output

Predicted: 6794.773

'''预测输出为6794.773,其真实值是6981,差不多。

Validate Model

预测test集中的所有值,这时,我们可以一次全部预测这12个值,也可以一步一步预测,在每一步中都加入test集合中的真实值作为输入。

前者的预测只能保证在第一二个时间步准确,后者的预测将会准确预测做够长的序列。我们选用后者的方法,即walk-forward。

from pandas import Series

from matplotlib import pyplot

from statsmodels.tsa.arima_model import ARIMA

from statsmodels.tsa.arima_model import ARIMAResults

from sklearn.metrics import mean_squared_error

from math import sqrt

import numpy

# create a differenced series

def difference(dataset, interval=1):

diff = list()

for i in range(interval, len(dataset)):

value = dataset[i] - dataset[i - interval]

diff.append(value)

return diff

# invert differenced value

def inverse_difference(history, yhat, interval=1):

return yhat + history[-interval]

# load and prepare datasets

dataset = Series.from_csv('dataset.csv')

X = dataset.values.astype('float32')

history = [x for x in X]

months_in_year = 12

validation = Series.from_csv('validation.csv')

y = validation.values.astype('float32')

# load model

model_fit = ARIMAResults.load('model.pkl')

bias = numpy.load('model_bias.npy')

# make first prediction

predictions = list()

yhat = float(model_fit.forecast()[0])

yhat = bias + inverse_difference(history, yhat, months_in_year)

predictions.append(yhat)

history.append(y[0])

print('>Predicted=%.3f, Expected=%3.f' % (yhat, y[0]))

# rolling forecasts

for i in range(1, len(y)):

# difference data

months_in_year = 12

diff = difference(history, months_in_year)

# predict

model = ARIMA(diff, order=(0,0,1))

model_fit = model.fit(trend='nc', disp=0)

yhat = model_fit.forecast()[0]

yhat = bias + inverse_difference(history, yhat, months_in_year)

predictions.append(yhat)

# observation

obs = y[i]

history.append(obs)

print('>Predicted=%.3f, Expected=%3.f' % (yhat, obs))

# report performance

mse = mean_squared_error(y, predictions)

rmse = sqrt(mse)

print('RMSE: %.3f' % rmse)

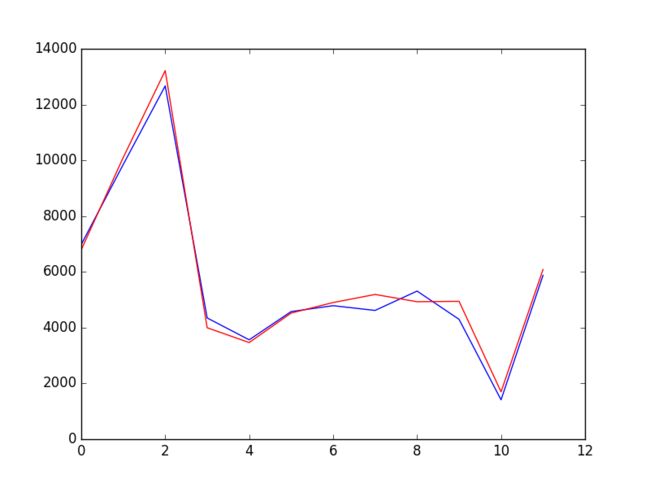

pyplot.plot(y)

pyplot.plot(predictions, color='red')

pyplot.show()

'''output

>Predicted=6794.773, Expected=6981

>Predicted=10101.763, Expected=9851

>Predicted=13219.067, Expected=12670

>Predicted=3996.535, Expected=4348

>Predicted=3465.934, Expected=3564

>Predicted=4522.683, Expected=4577

>Predicted=4901.336, Expected=4788

>Predicted=5190.094, Expected=4618

>Predicted=4930.190, Expected=5312

>Predicted=4944.785, Expected=4298

>Predicted=1699.409, Expected=1413

>Predicted=6085.324, Expected=5877

RMSE: 361.110

'''