二手车价预测分析

数据分析:二手车价格预测分析

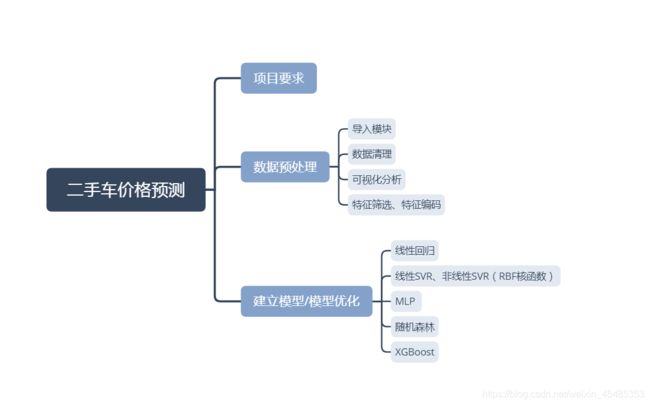

目录

一、项目要求

1,背景

二手车报价在二手车交易中对消费者有着至关重要的意义,为了大致了解二手车评估价格,消费者直接利用网上评估也是比较常见的方法,可以避免被‘坑’。

汽车网站提供的在线评估系统可以为消费者了解市场、了解价格提供了重要的依据。

2,目标

借助二手车交易数据,建立准确的二手车价格预估回归模型,可以为网站在线评估系统汽车定价提供依据。

3,内容

根据二手车市场交易相关数据,分析不同特征与价格之间的关系,使用多类算法(线性回归、支持向量机、多层感知机、随机森林、XGBoost)创建回归模型,预测二手车交易价格。

二、数据预处理

导入模块

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

from scipy.stats import norm

from sklearn.preprocessing import StandardScaler

from sklearn.model_selection import train_test_split

from sklearn.model_selection import GridSearchCV

from sklearn.linear_model import LinearRegression

from sklearn.svm import LinearSVR

from sklearn.svm import SVR

from sklearn.neural_network import MLPRegressor

from sklearn.ensemble import RandomForestRegressor

from xgboost import XGBRegressor

from sklearn.metrics import r2_score

from sklearn.model_selection import cross_val_score

#可视化的中文处理

plt.rcParams['font.sans-serif'] = 'Microsoft YaHei'

plt.rcParams['axes.unicode_minus'] = False

plt.style.use('ggplot')

导入数据

#导入数据

car=pd.read_csv(r'second_cars_info.csv',encoding='gbk')

#数据无缺失值。

car.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 11281 entries, 0 to 11280

Data columns (total 7 columns):

Brand 11281 non-null object

Name 11281 non-null object

Boarding_time 11281 non-null object

Km 11281 non-null object

Discharge 11281 non-null object

Sec_price 11281 non-null float64

New_price 11281 non-null object

dtypes: float64(1), object(6)

#查看数据大致信息内容,变量包括汽车品牌Brand、汽车款式Name、上牌时间Boarding_time、行驶里程数Km、排放标准Discharge、二手价格Sec_price和新车价格New_price,其中只有二手价格Sec_price是数值变量。

car.head()

Brand Name Boarding_time Km Discharge

0 奥迪 奥迪A6L 2006款 2.4 CVT 舒适型 2006年8月 9.00万公里 国3

1 奥迪 奥迪A6L 2007款 2.4 CVT 舒适型 2007年1月 8.00万公里 国4

2 奥迪 奥迪A6L 2004款 2.4L 技术领先型 2005年5月 15.00万公里 国2

3 奥迪 奥迪A8L 2013款 45 TFSI quattro舒适型 2013年10月 4.80万公里 欧4

4 奥迪 奥迪A6L 2014款 30 FSI 豪华型 2014年9月 0.81万公里 国4,国5

Sec_price New_price

0 6.90 50.89万

1 8.88 50.89万

2 3.82 54.24万

3 44.80 101.06万

4 33.19 54.99万

数据清理

#New_price 中含有较少的‘暂无’内容数据,删掉这些样本,数据转化为float形式

car['new_price'] =car.New_price.str.extract(r'(\d+.\d+)') .astype('float64')

car.dropna(inplace=True)

#KM中含有较少的‘百公里内’内容数据,将其数据变为0.00,数据转化为float形式

car['km'] = car.Km.str.extract(r'(\d+.\d+)').astype('float64')

car.loc[car.km.isnull(),'km']=0.00

#上牌时间Boarding_time,删去较少的显示‘未上牌’的样本,摘取出上牌年月。计算上牌时间到2018.03的间隔(交易时间)

car = car.loc[car.Boarding_time != '未上牌',:]

car['year']=car.Boarding_time.str.extract(r'(\d+)').astype('int')

car['month']=car.Boarding_time.str.extract(r'(\d+月)')

car['month']=car.month.str.extract(r'(\d+)') .astype('int')

car['time'] = (2018-car.year)*12 + (3-car.month) + 1 #时间间隔,以月为单位

#Name中包括的内容复杂,提取其中部分特征可能与品牌,行驶时间具有较强相关性,暂排除这一特征

#Discharge数据异常,存在一辆车具有多个排放标准的情况,无法判断准确数据,暂排除这一特征

#得到处理后的数据

可视化分析、特征筛选

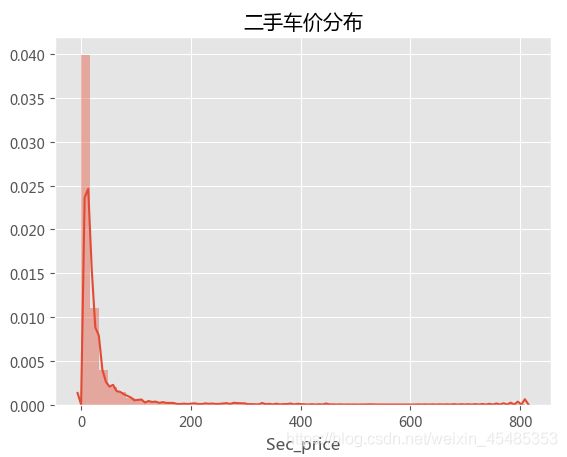

二手车价与折损率

#查看二手价格的分布,二手车价格则增高则二车数量急剧下降,符合偏态分布

sns.distplot(car.Sec_price)

plt.title('二手车价分布')

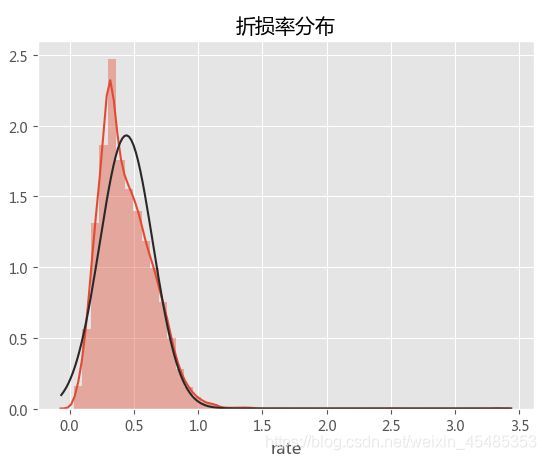

#创造新变量折损率rate(现价/原价)

car['rate']=car.Sec_price.div(car.new_price)

#查看折损率的分布,比较符合正态分布,考虑用折损率来作为作为目标变量

sns.distplot(car.rate,fit=norm)

plt.title('折损率分布')

- 特征筛选,影响二手车价的因素可能有行驶公里km、行驶时间time、品牌Brand、车型款式name等,接下来探索一下各因素与折损率rate之间的关系。

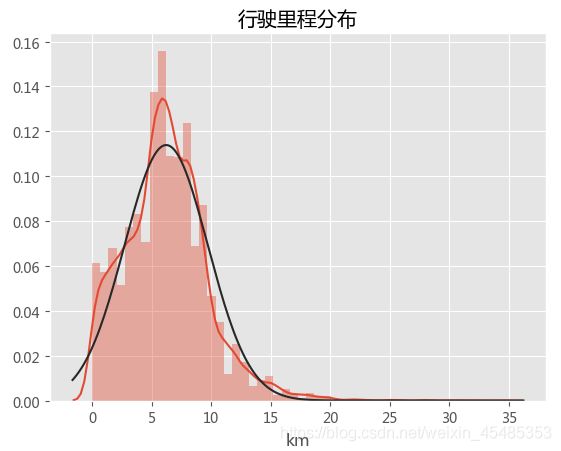

行驶里程km

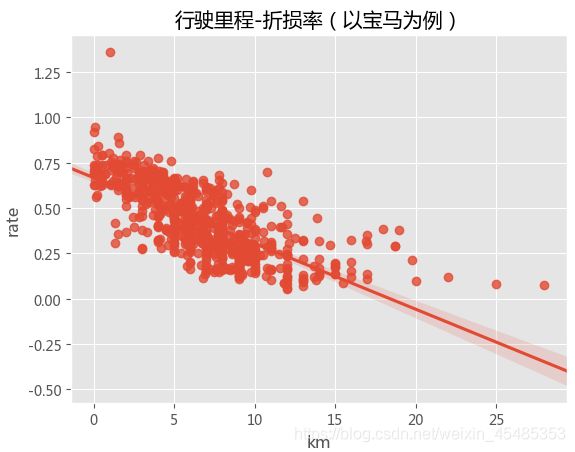

#从分布来看,行驶里程km较符合正态分布,并且与折损率rate间存在明显的负相关(以宝马为例),正常来说,车辆的折损率都是低于1的,(去除rate>1的异常点以及行驶里程超过25km的离散点)

sns.distplot(car.km,fit=norm)

plt.title('行驶里程-折损率')

sns.regplot('km','rate',data=car[car.Brand=='宝马'])

plt.title('行驶里程-折损率(以宝马为例)')

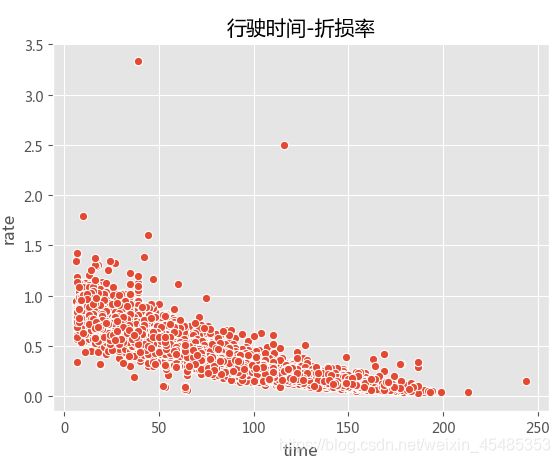

行驶时间time

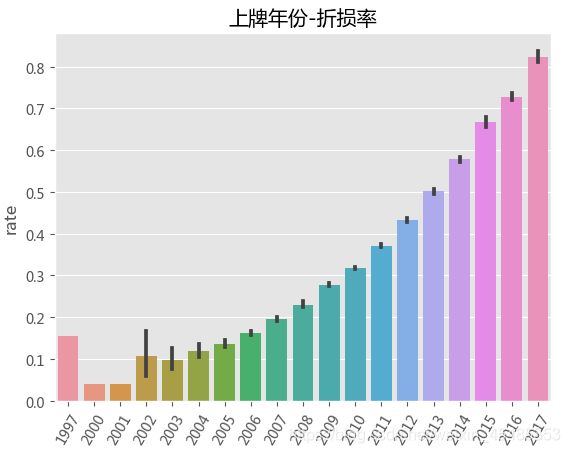

#行驶时间、上牌年份与折损率呈现负相关性。

sns.barplot('year','rate',data=car)

plt.xticks(rotation=60)

plt.title('上牌年份-折损率')

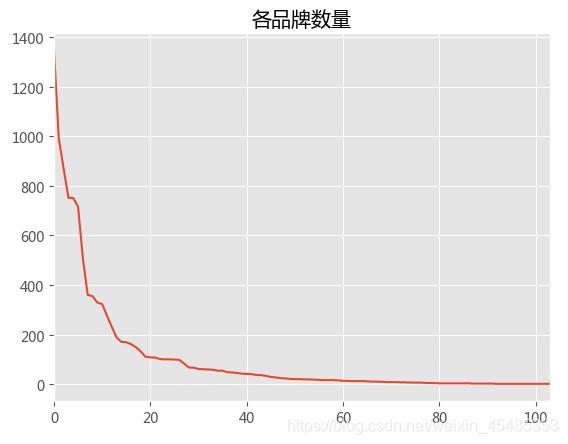

品牌Brand

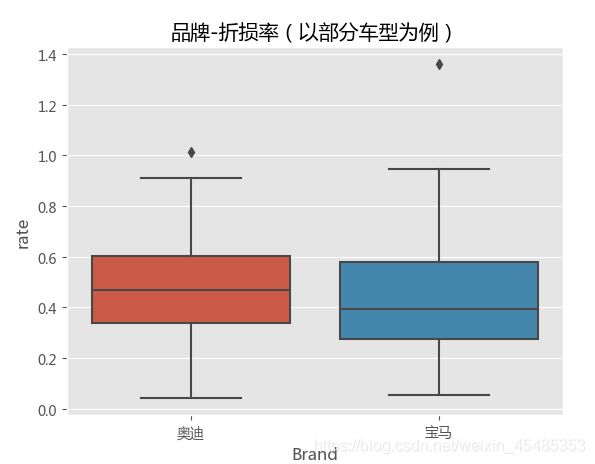

#Brand与折损率相关,以奥迪,宝马,荣威,名爵为例,不同品牌rate的平均值以及分布不一样,存在异常值。

sns.boxplot('Brand','rate',data=car[car.Brand.isin(['奥迪','宝马'])])

plt.title('品牌-折损率(以部分车型为例)')

#品牌数目众多,且数量分布不均,部分品牌数量太少不具有代表性,且不利于模型验证(去除少于10辆的车型)

brand_count=car.Brand.value_counts()

brand_count.index=np.arange(len(brand_count.values))

brand_count.plot()

plt.title('各品牌数量')

去除异常值

#去除异常值,特征筛选

car1=car[(car.rate<1)&(car.km<25)]

car1=car1[~car1.name.isin(['1995','1999','2000','2001','2002'])]

number=dict(zip(car1.groupby('Brand').rate.count().index,car1.groupby('Brand').rate.count().values))

car1['number']=car1.Brand.map(number)

car1=car1.loc[car1.number>=10]

x=car1[['Brand','km','time','name']]

y=car1['rate']

特征编码

#特征Brand和name是类别特征,使用one-hot对变量编码,得到最终数据

x=pd.get_dummies(x)

print(len(x.columns)) #特征维度有71个

71

三、建立模型

划分训练集和测试集

#划分训练集、测试集

xtrain,xtest,ytrain,ytest=train_test_split(x.values,y.values,test_size=.3,random_state=0)

#划分标准化的训练集、测试集

xstd=StandardScaler().fit_transform(x)

xtrainstd,xteststd,ytrain,ytest=train_test_split(xstd,y.values,test_size=.3,random_state=0)

- 线性回归

#建立线性回归模型

lr=LinearRegression()

lr.fit(xtrain,ytrain)

lrpred=lr.predict(xtest)

lrpredtrain=lr.predict(xtrain)

#R2评估

print(r2_score (ytest,lrpred)) #测试集R2评分

0.8669428574244431

print(r2_score (ytrain,lrpredtrain))#训练集R2评分

0.8594804025897764

#结合交叉验证评估

print(cross_val_score(lr,xtrain,ytrain,cv=5).mean())

0.8562639774220744

- 调参SVM模型(线性SVR和RBF核函数SVR)

#使用线性SVR模型与非线性SVR模型(RBF核函数)分别进行拟合,SVM模型的输入需要标准化

#线性SVR、调参

svr=LinearSVR()

Cs=[1,10,100,1000,10000]

params={'C':Cs}

gridsvr=GridSearchCV(svr,param_grid=params,cv=5)

gridsvr.fit(xtrainstd,ytrain)

print(gridsvr.best_params_)

{'C': 1}

print(gridsvr.best_score_) #训练集结果

0.8297852276978468

#最优参数模型

svr=LinearSVR(C=1)

svr.fit(xtrainstd,ytrain)

svrpred=svr.predict(xteststd)

print(r2_score (ytest,svrpred)) #测试集R2评分,略低于线性回归

0.8356441749023596

#rbf核非线性SVR、调参

svr_rbf=SVR(kernel='rbf',gamma='auto')

gridsvr_rbf=GridSearchCV(svr_rbf,param_grid=params,cv=5)

gridsvr_rbf.fit(xtrainstd,ytrain)

print(gridsvr_rbf.best_params_)

{'C': 10}

print(gridsvr_rbf.best_score_)#训练集结果

0.8622494426824513

#最优参数模型

svr_rbf=SVR(C=10,kernel='rbf',gamma='auto')

svr_rbf.fit(xtrainstd,ytrain)

svrpred2=svr_rbf.predict(xteststd)

print(r2_score (ytest,svrpred2))

0.8752909049370735 #测试集结果,rbf核SVR模型结果比线性SVR更好,略高于线性回归结果

- MLP

#默认参数的MLP回归模型,效果一般

mlpr=MLPRegressor()

mlpr.fit(xtrain,ytrain)

mlppred=mlpr.predict(xtest)

mlppredtrain=mlpr.predict(xtrain)

print(r2_score (ytrain,mlppredtrain))#训练集R2评分

0.8711448569099354

print(r2_score (ytest,mlppred)) #测试集R2评分

0.8648966919561516

- 随机森林

#使用默认参数的随机森林模型,进行拟合

rfr = RandomForestRegressor()

rfr.fit(xtrain,ytrain)

scores =cross_val_score(rfr, xtrain,ytrain, cv=5) #交叉验证得到R2评分

print(scores.mean())

0.8617835669309049

rpred=rfr.predict(xtest)

print(r2_score (ytest,rpred)) #测试集评分,效果优于其他模型

0.8753017649870939

#简单调参,决策树的个数为400时可获得性能略微提升

ns=[200,400,600,800]

gridrfr=GridSearchCV(rfr,param_grid={'n_estimators':ns},scoring='r2',cv=5)

gridrfr.fit(xtrain,ytrain)

print(gridrfr.best_params_)

{'n_estimators': 800}

print(gridrfr.best_score_) #训练集评分

0.8704172423686983

#最佳参数模型

rfr2 = RandomForestRegressor(n_estimators=800)

rfr2.fit(xtrain,ytrain)

rpred2=rfr2.predict(xtest)

print(r2_score (ytest,rpred2)) #测试集评分

0.8858743975574236

- XGBoost

#默认参数的XGBoost模型,是所有模型中拟合最准确的

xgb=XGBRegressor()

xgb.fit(xtrain,ytrain)

xgbpred=xgb.predict(xtest)

xgbpredtrain=xgb.predict(xtrain)

print(r2_score (ytrain,xgbpredtrain))#训练集R2评分

0.8807846709266941

print(r2_score (ytest,xgbpred)) #测试集R2评分

0.8798086358957151

综上,

1,本数据样本数据量相对特征数较多,模型比较简单,也不易出现过拟合情况。

2,运用多种回归模型进行拟合,XGBoost、MLP模型与随机森林模型具有最高的准确率,但相对线性回归、SVR模型区别不是特别大,有限时间空间下,使用简单模型也可以获得不错的效果。

3,对SVM模型与随机森林进行过了简单调参,提高了准确率,可对各模型继续调参优化,获得更好的效果。