Home Credit Default Risk 违约风险预测,kaggle比赛,初级篇,LB 0.749

Home Credit Default Risk

- 结论

- 背景知识

- 数据集

- 数据分析

- 平衡度

- 数据缺失

- 数据类型

- 离群值

- 填充缺失值

- 建模

- Logistic Regression

- LightGBM

- Feature importance

- 附录:各字段的意义

结论

数据由Home Credit(中文名:捷信)提供,Home Credit致力于向无银行账户的人群提供信贷。任务要求预测客户是否偿还贷款或遇到困难。使用AUC(ROC)作为模型的评估标准。

本篇博客只对 application_train/application_test的数据进行分析,使用Logistic Regression进行分类预测。通过grid search调节超参数能够得到 public board 0.749,private board 0.748的成绩。而Baseline是0.68810,最好成绩能到0.79857,剩余部分在进阶篇。

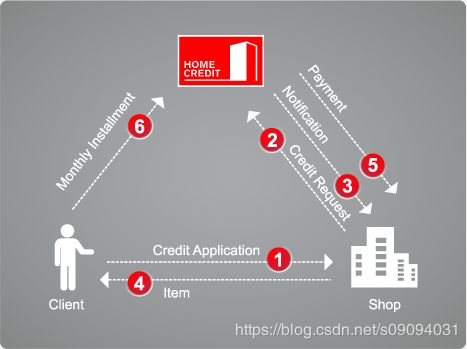

背景知识

Home Credit (捷信)是中东欧以及亚洲领先的消费金融提供商之一。在中东欧(CEE),俄罗斯,独联体国家(CIS)和亚洲各地服务于消费者。

查询用户在征信机构的历史征信记录可以用来作为风险评估的参考,但是征信数据往往不全,因为这些人本身就很少有银行记录。数据集中bureau.csv和 bureau_balance.csv 对应这部分数据。

Home Credit有三类产品,信用卡,POS(消费贷),现金贷。信用卡在欧洲和美国很流行,但在以上这些国家并非如此。所以数据集中信用卡数据偏少。POS只能买东西,现金贷可以得到现金。三类产品都有申请和还款记录。数据集中previous_application.csv, POS_CASH_BALANCE.csv,credit_card_balance.csv,installments_payment.csv对应这部分数据。

三类产品的英文分别是:Revolving loan (credit card),Consumer installment loan (Point of sales loan – POS loan),Installment cash loan。

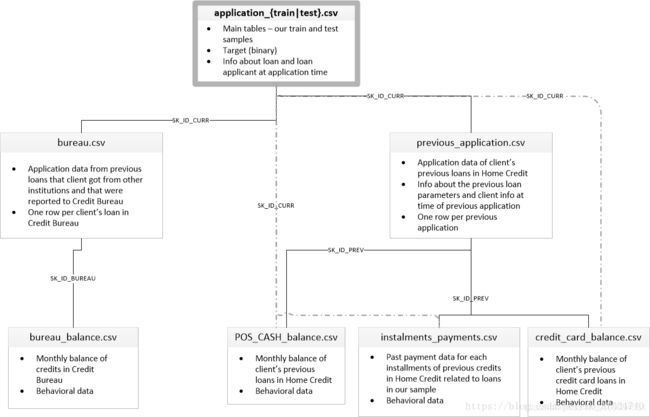

数据集

根据上面的介绍,数据集包括了8个不同的数据文件,就可以分为三大类。

-

application_train, application_test:

训练集包括Home Credit每个贷款申请的信息。每笔贷款都有自己的行,并由SK_ID_CURR标识。训练集的TARGET 0:贷款已还清,1:贷款未还清。

通过这两个文件,就能对这个任务做基本的数据分析和建模,也是本篇博客的内容。 -

bureau, bureau_balance:

这两个文件是征信机构提供的,用户在其他金融机构的贷款申请数据,以及每个月的还款欠款记录。一个用户(SK_ID_CURR)可以有多笔贷款申请数据(SK_ID_BUREAU)。 -

previous_application, POS_CASH_BALANCE,credit_card_balance,installments_payment

这四个文件来自Home Credit。用户可能已经在Home Credit 使用过POS服务,信用卡,和申请贷款。这些文件就是相关申请数据和还款记录。一个用户(SK_ID_CURR)可以有多笔历史数据(SK_ID_PREV)。

下图显示了所有数据是如何相关的,通过三个ID将三部分数据联系起来,SK_ID_CURR,SK_ID_BUREAU和SK_ID_PREV。

数据分析

平衡度

从application_train和application_test中读取数据。训练集中一共307511条数据,122个特征。其中违约(Target = 1)的数量为24825,没有违约(Target = 0)的数量282686,imbalance不算严重。

# -*- coding: utf-8 -*-

##307511, 122, 30万数据,28万0, 2万1,这个imbalance不算严重

app_train = pd.read_csv('input/application_train.csv')

app_test = pd.read_csv('input/application_test.csv')

print('training data shape is', app_train.shape)

print(app_train['TARGET'].value_counts())

training data shape is (307511, 122)

0 282686

1 24825

Name: TARGET, dtype: int64

数据缺失

122个特征中,67个特征有缺失,其中49个数据缺失超过47%。

## 67个特征有缺失,49个数据缺失超过47%, 其中47个与住房特征有关,是否可以将这个住房特征用PCA降阶。看其他人如何处理。

## 剩下ext_source 和 own_car_age。或者这49个特征可以尝试删除。

mv = app_train.isnull().sum().sort_values()

mv = mv[mv>0]

mv_rate = mv/len(app_train)

mv_df = pd.DataFrame({'mv':mv, 'mv_rate':mv_rate})

print('number of features with more than 47% missing', len(mv_rate[mv_rate>0.47]))

mv_rate[mv_rate> 0.47]

number of features with more than 47% missing 49

EMERGENCYSTATE_MODE 0.473983

TOTALAREA_MODE 0.482685

YEARS_BEGINEXPLUATATION_MODE 0.487810

YEARS_BEGINEXPLUATATION_AVG 0.487810

YEARS_BEGINEXPLUATATION_MEDI 0.487810

FLOORSMAX_AVG 0.497608

FLOORSMAX_MEDI 0.497608

FLOORSMAX_MODE 0.497608

HOUSETYPE_MODE 0.501761

LIVINGAREA_AVG 0.501933

LIVINGAREA_MODE 0.501933

LIVINGAREA_MEDI 0.501933

ENTRANCES_AVG 0.503488

ENTRANCES_MODE 0.503488

ENTRANCES_MEDI 0.503488

APARTMENTS_MEDI 0.507497

APARTMENTS_AVG 0.507497

APARTMENTS_MODE 0.507497

WALLSMATERIAL_MODE 0.508408

ELEVATORS_MEDI 0.532960

ELEVATORS_AVG 0.532960

ELEVATORS_MODE 0.532960

NONLIVINGAREA_MODE 0.551792

NONLIVINGAREA_AVG 0.551792

NONLIVINGAREA_MEDI 0.551792

EXT_SOURCE_1 0.563811

BASEMENTAREA_MODE 0.585160

BASEMENTAREA_AVG 0.585160

BASEMENTAREA_MEDI 0.585160

LANDAREA_MEDI 0.593767

LANDAREA_AVG 0.593767

LANDAREA_MODE 0.593767

OWN_CAR_AGE 0.659908

YEARS_BUILD_MODE 0.664978

YEARS_BUILD_AVG 0.664978

YEARS_BUILD_MEDI 0.664978

FLOORSMIN_AVG 0.678486

FLOORSMIN_MODE 0.678486

FLOORSMIN_MEDI 0.678486

LIVINGAPARTMENTS_AVG 0.683550

LIVINGAPARTMENTS_MODE 0.683550

LIVINGAPARTMENTS_MEDI 0.683550

FONDKAPREMONT_MODE 0.683862

NONLIVINGAPARTMENTS_AVG 0.694330

NONLIVINGAPARTMENTS_MEDI 0.694330

NONLIVINGAPARTMENTS_MODE 0.694330

COMMONAREA_MODE 0.698723

COMMONAREA_AVG 0.698723

COMMONAREA_MEDI 0.698723

dtype: float64

数据类型

122个特征中,65个 浮点类型,41 整型类型,16个非数据特征。对非数据类型特征画图分析其与Target的关系。OCCUPATION_TYPE 和 ORGANIZATION_TYPE可以手动进行数值编码,其余的直接用Onehot encoding。

## 65 浮点,41 整型,16个非数据特征,除了OCCUPATION_TYPE 和 ORGANIZATION_TYPE 其余应该都可以手动编码

categorical = [col for col in app_train.columns if app_train[col].dtypes == 'object']

ct = app_train[categorical].nunique().sort_values()

for col in categorical:

if (col!='OCCUPATION_TYPE') & (col!='ORGANIZATION_TYPE'):

plt.figure(figsize = [10,10])

sns.barplot(y = app_train[col], x = app_train['TARGET'])

# 对特征数为2的特征编码, nunique 和 len(unique)是不一样的,前者不计算null,后者会计算null

from sklearn.preprocessing import LabelEncoder

lb = LabelEncoder()

count = 0

for col in categorical:

if len(app_train[col].unique()) == 2:

count = count + 1

lb.fit(app_train[col])

app_train['o' + col] = lb.transform(app_train[col])

app_test['o' + col] = lb.transform(app_test[col])

# housing type mode, family status的逾期率和分类有一定关系。

# OCCUPATION可以按以下编码

col = 'OCCUPATION_TYPE'

#occ_sort = app_train.groupby(['OCCUPATION_TYPE'])['TARGET'].agg(['mean','count']).sort_values(by = 'mean')

#order1 = list(occ_sort.index)

#plt.figure(figsize = [10,10])

#sns.barplot(y = app_train[col], x = app_train['TARGET'], order = order1)

dict1 = {'Accountants' : 1,

'High skill tech staff':2, 'Managers':2, 'Core staff':2,

'HR staff' : 2,'IT staff': 2, 'Private service staff': 2, 'Medicine staff': 2,

'Secretaries': 2,'Realty agents': 2,

'Cleaning staff': 3, 'Sales staff': 3, 'Cooking staff': 3,'Laborers': 3,

'Security staff': 3, 'Waiters/barmen staff': 3,'Drivers': 3,

'Low-skill Laborers': 4}

app_train['oOCCUPATION_TYPE'] = app_train['OCCUPATION_TYPE'].map(dict1)

app_test['oOCCUPATION_TYPE'] = app_test['OCCUPATION_TYPE'].map(dict1)

plt.figure(figsize = [10,10])

sns.barplot(x = app_train['oOCCUPATION_TYPE'], y = app_train['TARGET'])

##

col = 'ORGANIZATION_TYPE'

#organ_sort = app_train.groupby(['ORGANIZATION_TYPE'])['TARGET'].agg(['mean','count']).sort_values(by = 'mean')

#order1 = list(organ_sort.index)

#plt.figure(figsize = [20,20])

#sns.barplot(y = app_train[col], x = app_train['TARGET'], order = order1)

dict1 = {'Trade: type 4' :1, 'Industry: type 12' :1, 'Transport: type 1' :1, 'Trade: type 6' :1,

'Security Ministries' :1, 'University' :1, 'Police' :1, 'Military' :1, 'Bank' :1, 'XNA' :1,

'Culture' :2, 'Insurance' :2, 'Religion' :2, 'School' :2, 'Trade: type 5' :2, 'Hotel' :2, 'Industry: type 10' :2,

'Medicine' :2, 'Services' :2, 'Electricity' :2, 'Industry: type 9' :2, 'Industry: type 5' :2, 'Government' :2,

'Trade: type 2' :2, 'Kindergarten' :2, 'Emergency' :2, 'Industry: type 6' :2, 'Industry: type 2' :2, 'Telecom' :2,

'Other' :3, 'Transport: type 2' :3, 'Legal Services' :3, 'Housing' :3, 'Industry: type 7' :3, 'Business Entity Type 1' :3,

'Advertising' :3, 'Postal':3, 'Business Entity Type 2' :3, 'Industry: type 11' :3, 'Trade: type 1' :3, 'Mobile' :3,

'Transport: type 4' :4, 'Business Entity Type 3' :4, 'Trade: type 7' :4, 'Security' :4, 'Industry: type 4' :4,

'Self-employed' :5, 'Trade: type 3' :5, 'Agriculture' :5, 'Realtor' :5, 'Industry: type 3' :5, 'Industry: type 1' :5,

'Cleaning' :5, 'Construction' :5, 'Restaurant' :5, 'Industry: type 8' :5, 'Industry: type 13' :5, 'Transport: type 3' :5}

app_train['oORGANIZATION_TYPE'] = app_train['ORGANIZATION_TYPE'].map(dict1)

app_test['oORGANIZATION_TYPE'] = app_test['ORGANIZATION_TYPE'].map(dict1)

plt.figure(figsize = [10,10])

sns.barplot(x = app_train['oORGANIZATION_TYPE'], y = app_train['TARGET'])

## 只对这几种进行ordinary编码吧,剩下的用ohe(307511, 127),(48744, 126) drop之后,feature分别为 122,121

discard_features = ['ORGANIZATION_TYPE', 'OCCUPATION_TYPE','FLAG_OWN_CAR','FLAG_OWN_REALTY','NAME_CONTRACT_TYPE']

app_train.drop(discard_features,axis = 1, inplace = True)

app_test.drop(discard_features,axis = 1, inplace = True)

# 然后使用 get_dummies(307511, 169) (48744, 165)

app_train = pd.get_dummies(app_train)

app_test = pd.get_dummies(app_test)

print('Training Features shape: ', app_train.shape)

print('Testing Features shape: ', app_test.shape)

# 有些特征 test里面没有,需要对齐 (307511, 166)(48744, 165)

train_labels = app_train['TARGET']

app_train, app_test = app_train.align(app_test, join = 'inner', axis = 1)

app_train['TARGET'] = train_labels

print('Training Features shape: ', app_train.shape)

print('Testing Features shape: ', app_test.shape)

Training Features shape: (307511, 169)

Testing Features shape: (48744, 165)

Training Features shape: (307511, 166)

Testing Features shape: (48744, 165)

离群值

在特征DAYS_EMPLOYED 里面发现有不正常数据,而这个特征与Target的相关性很强,需要特殊处理。另外增加一个特征,DAYS_EMPLOYED_ANOM,来表征这个特征是否不正常。这种处理应该是对线性方法比较有效,而基于树的方法应该可以自动识别。

## 继续EDA, 在DAYS_EMPLOYED 里面发现有问题数据,这种处理应该是对线性方法有效,boost方法应该可以自动识别。

app_train['DAYS_EMPLOYED'].plot.hist(title = 'DAYS_EMPLOYMENT HISTOGRAM')

app_test['DAYS_EMPLOYED'].plot.hist(title = 'DAYS_EMPLOYMENT HISTOGRAM')

app_train['DAYS_EMPLOYED_ANOM'] = app_train['DAYS_EMPLOYED'] == 365243

app_train['DAYS_EMPLOYED'].replace({365243: np.nan}, inplace = True)

app_test['DAYS_EMPLOYED_ANOM'] = app_test["DAYS_EMPLOYED"] == 365243

app_test["DAYS_EMPLOYED"].replace({365243: np.nan}, inplace = True)

app_train['DAYS_EMPLOYED'].plot.hist(title = 'Days Employment Histogram');

plt.xlabel('Days Employment')

## 提取相关性

correlations = app_train.corr()['TARGET'].sort_values()

print('Most Positive Correlations:\n', correlations.tail(15))

print('\nMost Negative Correlations:\n', correlations.head(15))

Most Positive Correlations:

REG_CITY_NOT_LIVE_CITY 0.044395

FLAG_EMP_PHONE 0.045982

NAME_EDUCATION_TYPE_Secondary / secondary special 0.049824

REG_CITY_NOT_WORK_CITY 0.050994

DAYS_ID_PUBLISH 0.051457

CODE_GENDER_M 0.054713

DAYS_LAST_PHONE_CHANGE 0.055218

NAME_INCOME_TYPE_Working 0.057481

REGION_RATING_CLIENT 0.058899

REGION_RATING_CLIENT_W_CITY 0.060893

oORGANIZATION_TYPE 0.070121

DAYS_EMPLOYED 0.074958

oOCCUPATION_TYPE 0.077514

DAYS_BIRTH 0.078239

TARGET 1.000000

Name: TARGET, dtype: float64

Most Negative Correlations:

EXT_SOURCE_3 -0.178919

EXT_SOURCE_2 -0.160472

EXT_SOURCE_1 -0.155317

NAME_EDUCATION_TYPE_Higher education -0.056593

CODE_GENDER_F -0.054704

NAME_INCOME_TYPE_Pensioner -0.046209

DAYS_EMPLOYED_ANOM -0.045987

FLOORSMAX_AVG -0.044003

FLOORSMAX_MEDI -0.043768

FLOORSMAX_MODE -0.043226

EMERGENCYSTATE_MODE_No -0.042201

HOUSETYPE_MODE_block of flats -0.040594

AMT_GOODS_PRICE -0.039645

REGION_POPULATION_RELATIVE -0.037227

ELEVATORS_AVG -0.034199

Name: TARGET, dtype: float64

填充缺失值

## 特征工程

## 填充缺失值

from sklearn.preprocessing import Imputer, MinMaxScaler

imputer = Imputer(strategy = 'median')

scaler = MinMaxScaler(feature_range = [0,1])

train = app_train.drop(columns = ['TARGET'])

imputer.fit(train)

train = imputer.transform(train)

test = imputer.transform(app_test)

scaler.fit(train)

train = scaler.transform(train)

test = scaler.transform(test)

print('Training data shape: ', train.shape)

print('Testing data shape: ', test.shape)

D:\Anaconda3\lib\site-packages\sklearn\utils\deprecation.py:66: DeprecationWarning: Class Imputer is deprecated; Imputer was deprecated in version 0.20 and will be removed in 0.22. Import impute.SimpleImputer from sklearn instead.

warnings.warn(msg, category=DeprecationWarning)

Training data shape: (307511, 166)

Testing data shape: (48744, 166)

建模

Logistic Regression

使用逻辑回归来建模,使用grid search搜索最佳参数,结果显示 ‘C’ = 1, ‘Penalty’ = 'l1’的时候,性能最好。

##

from sklearn.linear_model import LogisticRegression

from sklearn.model_selection import GridSearchCV

param_grid = {'C' : [0.01,0.1,1,10,100],

'penalty' : ['l1','l2']}

log_reg = LogisticRegression()

grid_search = GridSearchCV(log_reg, param_grid, scoring = 'roc_auc', cv = 5)

grid_search.fit(train, train_labels)

# Train on the training data

log_reg_best = grid_search.best_estimator_

log_reg_pred = log_reg_best.predict_proba(test)[:, 1]

submit = app_test[['SK_ID_CURR']]

submit['TARGET'] = log_reg_pred

submit.head()

submit.to_csv('log_reg_baseline_gridsearch2.csv', index = False)

最后的结果

public board 0.73889

private board 0.73469

LightGBM

folds = KFold(n_splits= num_folds, shuffle=True, random_state=1001)

# Create arrays and dataframes to store results

oof_preds = np.zeros(train_df.shape[0])

sub_preds = np.zeros(test_df.shape[0])

feature_importance_df = pd.DataFrame()

feats = [f for f in train_df.columns if f not in ['TARGET','SK_ID_CURR','SK_ID_BUREAU','SK_ID_PREV','index']]

for n_fold, (train_idx, valid_idx) in enumerate(folds.split(train_df[feats], train_df['TARGET'])):

train_x, train_y = train_df[feats].iloc[train_idx], train_df['TARGET'].iloc[train_idx]

valid_x, valid_y = train_df[feats].iloc[valid_idx], train_df['TARGET'].iloc[valid_idx]

# LightGBM parameters found by Bayesian optimization

clf = LGBMClassifier(

nthread=4,

n_estimators=10000,

learning_rate=0.02,

num_leaves=34,

colsample_bytree=0.9497036,

subsample=0.8715623,

max_depth=8,

reg_alpha=0.041545473,

reg_lambda=0.0735294,

min_split_gain=0.0222415,

min_child_weight=39.3259775,

silent=-1,

verbose=-1, )

clf.fit(train_x, train_y, eval_set=[(train_x, train_y), (valid_x, valid_y)],

eval_metric= 'auc', verbose= 200, early_stopping_rounds= 200)

oof_preds[valid_idx] = clf.predict_proba(valid_x, num_iteration=clf.best_iteration_)[:, 1]

sub_preds += clf.predict_proba(test_df[feats], num_iteration=clf.best_iteration_)[:, 1] / folds.n_splits

fold_importance_df = pd.DataFrame()

fold_importance_df["feature"] = feats

fold_importance_df["importance"] = clf.feature_importances_

fold_importance_df["fold"] = n_fold + 1

feature_importance_df = pd.concat([feature_importance_df, fold_importance_df], axis=0)

print('Fold %2d AUC : %.6f' % (n_fold + 1, roc_auc_score(valid_y, oof_preds[valid_idx])))

del clf, train_x, train_y, valid_x, valid_y

gc.collect()

print('Full AUC score %.6f' % roc_auc_score(train_df['TARGET'], oof_preds))

private board 0.74847

public board0.74981

Feature importance

附录:各字段的意义

| 字段 | 含义 |

|---|---|

| SK_ID_CURR | 此次申请的ID |

| TARGET | 申请人本次申请的还款风险:1-风险较高;0-风险较低 |

| NAME_CONTRACT_TYPE | 贷款类型:cash(现金)还是revolving(周转金,一次申请,多次循环提取) |

| CODE_GENDER | 申请人性别 |

| FLAG_OWN_CAR | 申请人是否有车 |

| FLAG_OWN_REALTY | 申请人是否有房 |

| CNT_CHILDREN | 申请人子女个数 |

| AMT_INCOME_TOTAL | 申请人收入状况 |

| AMT_CREDIT | 此次申请的贷款金额 |

| AMT_ANNUITY | 贷款年金 |

| AMT_GOODS_PRICE | 如果是消费贷款,改字段表示商品的实际价格 |

| NAME_TYPE_SUITE | 申请人此次申请的陪同人员 |

| NAME_INCOME_TYPE | 申请人收入类型 |

| NAME_EDUCATION_TYPE | 申请人受教育程度 |

| NAME_FAMILY_STATUS | 申请人婚姻状况 |

| NAME_HOUSING_TYPE | 申请人居住状况(租房,已购房,和父母一起住等) |

| REGION_POPULATION_RELATIVE | 申请人居住地人口密度,已标准化 |

| DAYS_BIRTH | 申请人出生日(距离申请当日的天数,负值) |

| DAYS_EMPLOYED | 申请人当前工作的工作年限(距离申请当日的天数,负值) |

| DAYS_REGISTRATION | 申请人最近一次修改注册信息的时间(距离申请当日的天数,负值) |

| DAYS_ID_PUBLISH | 申请人最近一次修改申请贷款的身份证明文件的时间(距离申请当日的天数,负值) |

| FLAG_MOBIL | 申请人是否提供个人电话(1-yes,0-no) |

| FLAG_EMP_PHONE | 申请人是否提供家庭电话(1-yes,0-no) |

| FLAG_WORK_PHONE | 申请人是否提供工作电话(1-yes,0-no) |

| FLAG_CONT_MOBILE | 申请人个人电话是否能拨通(1-yes,0-no) |

| FLAG_EMAIL | 申请人是否提供电子邮箱(1-yes,0-no) |

| OCCUPATION_TYPE | 申请人职务 |

| REGION_RATING_CLIENT | 本公司对申请人居住区域的评分等级(1,2,3) |

| REGION_RATING_CLIENT_W_CITY | 在考虑所在城市的情况下,本公司对申请人居住区域的评分等级(1,2,3) |

| WEEKDAY_APPR_PROCESS_START | 申请人发起申请日是星期几 |

| HOUR_APPR_PROCESS_START | 申请人发起申请的hour |

| REG_REGION_NOT_LIVE_REGION | 申请人提供的的永久地址和联系地址是否匹配(1-不匹配,2-匹配,区域级别的) |

| REG_REGION_NOT_WORK_REGION | 申请人提供的的永久地址和工作地址是否匹配(1-不匹配,2-匹配,区域级别的) |

| LIVE_REGION_NOT_WORK_REGION | 申请人提供的的联系地址和工作地址是否匹配(1-不匹配,2-匹配,区域级别的) |

| REG_CITY_NOT_LIVE_CITY | 申请人提供的的永久地址和联系地址是否匹配(1-不匹配,2-匹配,城市级别的) |

| REG_CITY_NOT_WORK_CITY | 申请人提供的的永久地址和工作地址是否匹配(1-不匹配,2-匹配,城市级别的) |

| LIVE_CITY_NOT_WORK_CITY | 申请人提供的的联系地址和工作地址是否匹配(1-不匹配,2-匹配,城市级别的) |

| ORGANIZATION_TYPE | 申请人工作所属组织类型 |

| EXT_SOURCE_1 | 外部数据源1的标准化评分 |

| EXT_SOURCE_2 | 外部数据源2的标准化评分 |

| EXT_SOURCE_3 | 外部数据源3的标准化评分 |

| APARTMENTS_AVG <----> EMERGENCYSTATE_MODE | 申请人居住环境各项指标的标准化评分 |

| OBS_30_CNT_SOCIAL_CIRC LE <----> DEF_60_CNT_SOCIAL_CIRCLE | 这部分字段含义没看懂 |

| DAYS_LAST_PHONE_CHANGE | 申请人最近一次修改手机号码的时间(距离申请当日的天数,负值) |

| FLAG_DOCUMENT_2 <----> FLAG_DOCUMENT_21 | 申请人是否额外提供了文件2,3,4. . .21 |

| AMT_REQ_CREDIT_BUREAU_HOUR | 申请人发起申请前1个小时以内,被查询征信的次数 |

| AMT_REQ_CREDIT_BUREAU_DAY | 申请人发起申请前一天以内,被查询征信的次数 |

| AMT_REQ_CREDIT_BUREAU_WEEK | 申请人发起申请前一周以内,被查询征信的次数 |

| AMT_REQ_CREDIT_BUREAU_MONTH | 申请人发起申请前一个月以内,被查询征信的次数 |

| AMT_REQ_CREDIT_BUREAU_QRT | 申请人发起申请前一个季度以内,被查询征信的次数 |

| AMT_REQ_CREDIT_BUREAU_YEAR | 申请人发起申请前一年以内,被查询征信的次数 |

从表中就可以大致猜测出一些信息,例如:OCCUPATION_TYPE,NAME_INCOME_TYPE以及ORGANIZATION_TYPE应该有很强的线性相关性;DAYS_LAST_PHONE_CHANGE,HOUR_APPR_PROCESS_START等信息可能不是重要的特征;可以在后面的特征分析时加以验证并采取特定的降维手段