matlab机器学习预测股价+python爬虫

python3+matlab机器学习预测上证指数

爬虫爬去数据后,使用matlab的神经网络框架和径向基网络框架,通过前五天股市的开盘价预测后一天的收盘价。

配置python3环境,通过python爬虫爬取数据

pip3安装baostock pandas xlwt

爬取选定时期的股票当天开盘价、收盘价、当天收盘价等参数

并生成训练集及测试集

import baostock as bs

import pandas as pd

import sys

try:

stock = sys.argv[1]

print(stock)

except:

stock='sh.000001' #可选择股票

#if(sys.argv[1] == 1){

# stock = 'sh.' + str(stock2)

# }

#else{stock = 'sz.' + str(stock2)}

# 登陆系统

lg = bs.login()

# 显示登陆返回信息

print('login respond error_code:'+lg.error_code)

print('login respond error_msg:'+lg.error_msg)

# 获取股票信息

#rs = bs.query_hs300_stocks()

#rs = bs.query_all_stock('2020-12-04')

rs = bs.query_history_k_data_plus(stock,

"date,code,open,high,low,close,preclose,volume,amount,adjustflag,turn,tradestatus,pctChg",

start_date='2019-01-01', end_date='2019-12-20',

frequency="d", adjustflag="3")

print('query_hs300 error_code:'+rs.error_code)

print('query_hs300 error_msg:'+rs.error_msg)

# 打印结果集

hs300_stocks = []

while (rs.error_code == '0') & rs.next():

# 获取一条记录,将记录合并在一起

hs300_stocks.append(rs.get_row_data())

result = pd.DataFrame(hs300_stocks, columns=rs.fields)

# 结果集输出到csv文件

result.to_csv("./stock_info_train.csv", encoding="gbk", index=False)

result.to_excel("./stock_info_train.xls")

print(result)

# 获取股票信息

#rs = bs.query_hs300_stocks()

#rs = bs.query_all_stock('2020-12-04')

#601857

rs = bs.query_history_k_data_plus(stock,

"date,code,open,high,low,close,preclose,volume,amount,adjustflag,turn,tradestatus,pctChg",

start_date='2020-06-01', end_date='2029-7-20',

frequency="d", adjustflag="3")#超过会自动截止到最新日期

print('query_hs300 error_code:'+rs.error_code)

print('query_hs300 error_msg:'+rs.error_msg)

# 打印结果集

hs300_stocks = []

while (rs.error_code == '0') & rs.next():

# 获取一条记录,将记录合并在一起

hs300_stocks.append(rs.get_row_data())

result = pd.DataFrame(hs300_stocks, columns=rs.fields)

# 结果集输出到csv文件

result.to_csv("./stock_info_test.csv", encoding="gbk", index=False)

result.to_excel("./stock_info_test.xls")

print(result)

# 登出系统

bs.logout()

将xls数据导入matlab

clear all;

%stock = 'sh.002415';

%stock=inputdlg('input the code of stock');

system('conda activate tushare')

system('python get_stock_info.py sz.608891')

%[~, numdata]=xlsread('stock_info_train.xls',1,'D2:N200');%读取历史数据

numdata1=csvread('stock_info_train.csv',1,2,[1 2 199 6])%读取历史数据

%numdata2=csvread('stock_info_train.csv',1,7,[1 7 199 8])%读取历史数据

numdata3=csvread('stock_info_train.csv',1,10,[1 10 199 12])%读取历史数据

numdata=[numdata1 numdata3];

numdata;

[~, date]=xlsread('stock_info_train.xls',1,'B2:B200');%读取日期

数据处理

for i=1:1:193

P(i,:)=numdata(i+5,4);

end

T = 1:1:40

for i=1:1:194

ram = []

for j=1:1:5

ram = [ram numdata(i+j-1,:)]

end

T = [T ; ram]

end

T=T((2:1:194),:);

T=T';

P=P'

[Tn,minT,maxT,Pn,minP,maxP] = premnmx(T,P); %数据归一化处理

建立神经网络

%建立神经网络

net=newff(minmax(Tn),[150,1],{'purelin','purelin'},'trainlm');

net.trainparam.show=50; %显示迭代过程

net.trainparam.lr=0.005; %学习率

net.trainparam.epochs=3000; %最大训练次数

net.trainparam.min_grad=1e-14; %最大训练次数

net.trainparam.goal=1e-12; %训练要求精度

net.trainparam.mc=0; %动量因子

[net,tr]=train(net ,Tn,Pn); %训练bp网络

或建立径向基网络

net = newrb(Tn,Pn,0,1,100); %建立径向基网络

导入测试数据

%read the test data

numdata_test1=csvread('stock_info_test.csv',1,2,[1 2 199 6]);%读取历史数据

numdata_test2=csvread('stock_info_test.csv',1,10,[1 10 199 12]);%读取历史数据

numdata_test=[numdata_test1 numdata_test2];

[~, date_test]=xlsread('stock_info_test.xls',1,'B2:B200');%读取日期

for i=1:1:193

P_test(i,:)=numdata_test(i+5,4);

end

T_test = 1:1:40;

for i=1:1:194

ram = [];

for j=1:1:5

ram = [ram numdata_test(i+j-1,:)];

end

T_test = [T_test ; ram];

end

T_test=T_test((2:1:194),:);

T_test=T_test';

P_test=P_test'

% numdataT_test = numdata_test';

% P_test = numdataT_test(4,:);%目标值

% T_test = numdataT_test;

% P_test = P_test(2:99);

% T_test = T_test(:,(1:1:98));

[Tn_test,minT_test,maxT_test,Pn_test,minP_test,maxP_test] = premnmx(T_test,P_test); %数据归一化处理

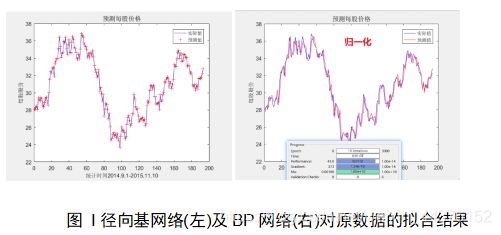

预测并绘图

Out2 = sim(net, Tn_test);

%a1 = (1:1:93);

a1 = (1:1:193);

a2=postmnmx(Out2,minP_test,maxP_test);

plot(a1,P_test,'b-',a1,a2,'r-');

%plot(a1,P_test,'.');

title('预测每股价格','FontSize',12);

xlabel('统计时间2014.9.1-2015.11.10','FontSize',10);

ylabel('每股股价','FontSize',10);

%hold on

%plot(a1,a2,'r--');

legend('实际值','预测值');

clc

对原数据的拟合情况

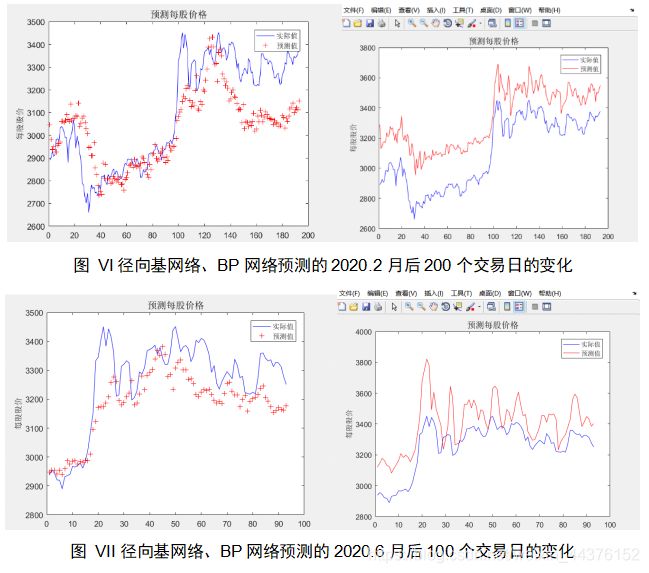

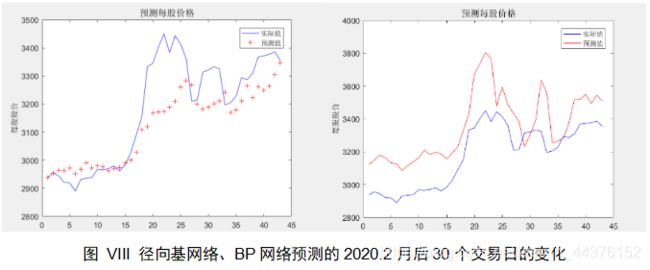

预测结果

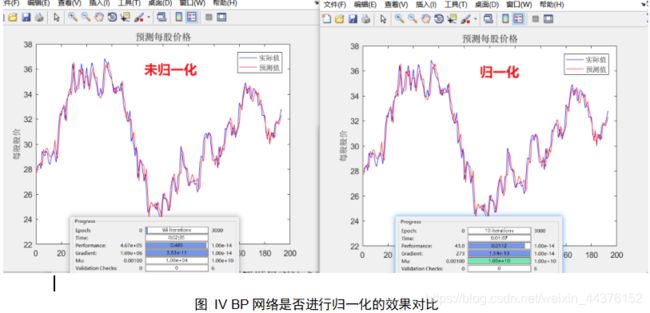

对是否进行归一化的训练效果进行了比较

- 对于未进行归一化的数据,在导入训练网络后,在相同的训练目标下,迭代了98层,运行了2:35后梯度已无法下降,于是提前结束训练。进行归一化的数据在导入网络后,网络迭代了十层,运行了1:07后,达到了更小的梯度。

综上,验证了数据归一化可使不同量纲下的数据归一化到合理的范围,有利于模型的泛化性,不易造成梯度爆炸,同时标准化减少了计算量,帮助模型更快收敛。

归一化,真是个好东西,之前不应该嫌弃她的。

简单总结

- 数据的归一化还是非常有必要的,他可使不同量纲下的数据归一化到合理的范围,有利于模型的泛化性,不易造成梯度爆炸,同时标显著减少了计算量,帮助模型更快收敛。

- 径向基网络和BP网络相比较,径向基网络在创建时更加快速,但BP网络在后续数据预测方面更有优势。

- 股市有风险,投资需谨慎。

数据的归一化还是非常有必要的,他可使不同量纲下的数据归一化到合理的范围,有利于模型的泛化性,不易造成梯度爆炸,同时标显著减少了计算量,帮助模型更快收敛。

12.径向基网络和BP网络相比较,径向基网络在创建时更加快速,但BP网络在后续数据预测方面更有优势。

13.股市有风险,投资需谨慎。