pytorch 建立LSTM模型实现股价预测

本文参考了这篇知乎文章:https://zhuanlan.zhihu.com/p/128927771,并对其中部分代码进行修改,使其更有可读性。

原版代码和数据见此链接:https://link.zhihu.com/?target=https%3A//github.com/yhannahwang/stock_prediction

本文通过jupyter notebook转化成markdown文件,再放到这里,代码和文字可能会有部分有背景色

阅读本文之前,需要知道LSTM的原理,还有pytorch中LSTM的接口定义,否则读起来很吃力。

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

导入数据,并进行处理

dates = pd.date_range('2010-10-11','2017-10-11',freq = 'B') # 生成时间序列,频率为工作日

# 生成一个只含索引的DataFrame

df_main = pd.DataFrame(index = dates)

df_main

| 2010-10-11 |

|---|

| 2010-10-12 |

| 2010-10-13 |

| 2010-10-14 |

| 2010-10-15 |

| ... |

| 2017-10-05 |

| 2017-10-06 |

| 2017-10-09 |

| 2017-10-10 |

| 2017-10-11 |

1828 rows × 0 columns

df_aaxj = pd.read_csv("data/ETFs/aaxj.us.txt", index_col=0)

df_aaxj

| Open | High | Low | Close | Volume | OpenInt | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2008-08-15 | 44.886 | 44.886 | 44.886 | 44.886 | 112 | 0 |

| 2008-08-18 | 44.564 | 44.564 | 43.875 | 43.875 | 28497 | 0 |

| 2008-08-19 | 43.283 | 43.283 | 43.283 | 43.283 | 112 | 0 |

| 2008-08-20 | 43.918 | 43.918 | 43.892 | 43.892 | 4468 | 0 |

| 2008-08-22 | 44.097 | 44.097 | 44.017 | 44.071 | 4006 | 0 |

| ... | ... | ... | ... | ... | ... | ... |

| 2017-11-06 | 75.900 | 76.530 | 75.890 | 76.530 | 1313730 | 0 |

| 2017-11-07 | 76.490 | 76.580 | 76.090 | 76.185 | 1627277 | 0 |

| 2017-11-08 | 76.370 | 76.590 | 76.290 | 76.570 | 681128 | 0 |

| 2017-11-09 | 76.040 | 76.200 | 75.580 | 76.110 | 1261567 | 0 |

| 2017-11-10 | 76.110 | 76.150 | 75.870 | 76.080 | 619687 | 0 |

2325 rows × 6 columns

# 数据拼接

df_main = df_main.join(df_aaxj)

df_main

| Open | High | Low | Close | Volume | OpenInt | |

|---|---|---|---|---|---|---|

| 2010-10-11 | 55.971 | 56.052 | 55.863 | 56.052 | 268544.0 | 0.0 |

| 2010-10-12 | 55.676 | 55.792 | 55.362 | 55.667 | 817951.0 | 0.0 |

| 2010-10-13 | 56.472 | 56.867 | 56.401 | 56.569 | 999413.0 | 0.0 |

| 2010-10-14 | 56.733 | 56.742 | 56.293 | 56.579 | 661897.0 | 0.0 |

| 2010-10-15 | 56.893 | 56.893 | 56.194 | 56.552 | 245001.0 | 0.0 |

| ... | ... | ... | ... | ... | ... | ... |

| 2017-10-05 | 73.500 | 74.030 | 73.500 | 73.970 | 2134323.0 | 0.0 |

| 2017-10-06 | 73.470 | 73.650 | 73.220 | 73.579 | 2092100.0 | 0.0 |

| 2017-10-09 | 73.500 | 73.795 | 73.480 | 73.770 | 879600.0 | 0.0 |

| 2017-10-10 | 74.150 | 74.490 | 74.150 | 74.480 | 1878845.0 | 0.0 |

| 2017-10-11 | 74.290 | 74.645 | 74.210 | 74.610 | 1168511.0 | 0.0 |

1828 rows × 6 columns

# 绘制收盘价格走势图

df_main[['Close']].plot()

plt.ylabel("stock_price")

plt.title("aaxj ETFs")

plt.show()

# 筛选四个变量,作为数据的输入特征

sel_col = ['Open', 'High', 'Low', 'Close']

df_main = df_main[sel_col]

df_main.head()

| Open | High | Low | Close | |

|---|---|---|---|---|

| 2010-10-11 | 55.971 | 56.052 | 55.863 | 56.052 |

| 2010-10-12 | 55.676 | 55.792 | 55.362 | 55.667 |

| 2010-10-13 | 56.472 | 56.867 | 56.401 | 56.569 |

| 2010-10-14 | 56.733 | 56.742 | 56.293 | 56.579 |

| 2010-10-15 | 56.893 | 56.893 | 56.194 | 56.552 |

# 查看是否有缺失值

np.sum(df_main.isnull())

Open 65

High 65

Low 65

Close 65

dtype: int64

# 缺失值填充

df_main = df_main.fillna(method='ffill') # 缺失值填充,使用上一个有效值

np.sum(df_main.isnull())

Open 0

High 0

Low 0

Close 0

dtype: int64

# 数据缩放

from sklearn.preprocessing import MinMaxScaler

scaler = MinMaxScaler(feature_range=(-1, 1))

for col in sel_col: # 这里不能进行统一进行缩放,因为fit_transform返回值是numpy类型

df_main[col] = scaler.fit_transform(df_main[col].values.reshape(-1,1))

# 将下一日的收盘价作为本日的标签

df_main['target'] = df_main['Close'].shift(-1)

df_main.head()

| Open | High | Low | Close | target | |

|---|---|---|---|---|---|

| 2010-10-11 | -0.089800 | -0.135104 | -0.074936 | -0.106322 | -0.129274 |

| 2010-10-12 | -0.107350 | -0.150977 | -0.104289 | -0.129274 | -0.075502 |

| 2010-10-13 | -0.059996 | -0.085348 | -0.043415 | -0.075502 | -0.074905 |

| 2010-10-14 | -0.044469 | -0.092979 | -0.049742 | -0.074905 | -0.076515 |

| 2010-10-15 | -0.034950 | -0.083761 | -0.055543 | -0.076515 | -0.068407 |

df_main.dropna() # 使用了shift函数,在最后必然是有缺失值的,这里去掉缺失值所在行

df_main = df_main.astype(np.float32) # 修改数据类型

建立LSTM模型

import torch.nn as nn

input_dim = 4 # 数据的特征数

hidden_dim = 32 # 隐藏层的神经元个数

num_layers = 2 # LSTM的层数

output_dim = 1 # 预测值的特征数

#(这是预测股票价格,所以这里特征数是1,如果预测一个单词,那么这里是one-hot向量的编码长度)

class LSTM(nn.Module):

def __init__(self, input_dim, hidden_dim, num_layers, output_dim):

super(LSTM, self).__init__()

# Hidden dimensions

self.hidden_dim = hidden_dim

# Number of hidden layers

self.num_layers = num_layers

# Building your LSTM

# batch_first=True causes input/output tensors to be of shape (batch_dim, seq_dim, feature_dim)

self.lstm = nn.LSTM(input_dim, hidden_dim, num_layers, batch_first=True)

# Readout layer 在LSTM后再加一个全连接层,因为是回归问题,所以不能在线性层后加激活函数

self.fc = nn.Linear(hidden_dim, output_dim)

def forward(self, x):

# Initialize hidden state with zeros

h0 = torch.zeros(self.num_layers, x.size(0), self.hidden_dim).requires_grad_()

# 这里x.size(0)就是batch_size

# Initialize cell state

c0 = torch.zeros(self.num_layers, x.size(0), self.hidden_dim).requires_grad_()

# One time step

# We need to detach as we are doing truncated backpropagation through time (BPTT)

# If we don't, we'll backprop all the way to the start even after going through another batch

out, (hn, cn) = self.lstm(x, (h0.detach(), c0.detach()))

out = self.fc(out)

return out

按照模型的接口组织数据

# 创建两个列表,用来存储数据的特征和标签

data_feat, data_target = [],[]

# 设每条数据序列有20组数据

seq = 20

for index in range(len(df_main) - seq):

# 构建特征集

data_feat.append(df_main[['Open', 'High', 'Low', 'Close']][index: index + seq].values)

# 构建target集

data_target.append(df_main['target'][index:index + seq])

# 将特征集和标签集整理成numpy数组

data_feat = np.array(data_feat)

data_target = np.array(data_target)

训练集与测试集的划分

# 这里按照8:2的比例划分训练集和测试集

test_set_size = int(np.round(0.2*df_main.shape[0])) # np.round(1)是四舍五入,

train_size = data_feat.shape[0] - (test_set_size)

print(test_set_size) # 输出测试集大小

print(train_size) # 输出训练集大小

366

1442

trainX = torch.from_numpy(data_feat[:train_size].reshape(-1,seq,4)).type(torch.Tensor)

# 这里第一个维度自动确定,我们认为其为batch_size,因为在LSTM类的定义中,设置了batch_first=True

testX = torch.from_numpy(data_feat[train_size:].reshape(-1,seq,4)).type(torch.Tensor)

trainY = torch.from_numpy(data_target[:train_size].reshape(-1,seq,1)).type(torch.Tensor)

testY = torch.from_numpy(data_target[train_size:].reshape(-1,seq,1)).type(torch.Tensor)

print('x_train.shape = ',trainX.shape)

print('y_train.shape = ',trainY.shape)

print('x_test.shape = ',testX.shape)

print('y_test.shape = ',testY.shape)

x_train.shape = torch.Size([1442, 20, 4])

y_train.shape = torch.Size([1442, 20, 1])

x_test.shape = torch.Size([366, 20, 4])

y_test.shape = torch.Size([366, 20, 1])

建立数据导入器(略)

# 因为数据量不大,所以这里就不再划分batch,即认为batch_size=1442,

# 这里只是演示一下数据导入器,我们并不使用

batch_size=1442

train = torch.utils.data.TensorDataset(trainX,trainY)

test = torch.utils.data.TensorDataset(testX,testY)

train_loader = torch.utils.data.DataLoader(dataset=train,

batch_size=batch_size,

shuffle=False)

test_loader = torch.utils.data.DataLoader(dataset=test,

batch_size=batch_size,

shuffle=False)

训练模型

# 实例化模型

model = LSTM(input_dim=input_dim, hidden_dim=hidden_dim, output_dim=output_dim, num_layers=num_layers)

# 定义优化器和损失函数

optimiser = torch.optim.Adam(model.parameters(), lr=0.01) # 使用Adam优化算法

loss_fn = torch.nn.MSELoss(size_average=True) # 使用均方差作为损失函数

# 设定数据遍历次数

num_epochs = 100

# 打印模型结构

print(model)

LSTM(

(lstm): LSTM(4, 32, num_layers=2, batch_first=True)

(fc): Linear(in_features=32, out_features=1, bias=True)

)

# 打印模型各层的参数尺寸

for i in range(len(list(model.parameters()))):

print(list(model.parameters())[i].size())

torch.Size([128, 4])

torch.Size([128, 32])

torch.Size([128])

torch.Size([128])

torch.Size([128, 32])

torch.Size([128, 32])

torch.Size([128])

torch.Size([128])

torch.Size([1, 32])

torch.Size([1])

# train model

hist = np.zeros(num_epochs)

for t in range(num_epochs):

# Initialise hidden state

# Don't do this if you want your LSTM to be stateful

# model.hidden = model.init_hidden()

# Forward pass

y_train_pred = model(trainX)

loss = loss_fn(y_train_pred, trainY)

if t % 10 == 0 and t !=0: # 每训练十次,打印一次均方差

print("Epoch ", t, "MSE: ", loss.item())

hist[t] = loss.item()

# Zero out gradient, else they will accumulate between epochs 将梯度归零

optimiser.zero_grad()

# Backward pass

loss.backward()

# Update parameters

optimiser.step()

Epoch 10 MSE: 0.01842750422656536

Epoch 20 MSE: 0.008485360071063042

Epoch 30 MSE: 0.004656758159399033

Epoch 40 MSE: 0.0032537723891437054

Epoch 50 MSE: 0.002434148220345378

Epoch 60 MSE: 0.0020096886437386274

Epoch 70 MSE: 0.0018414082005620003

Epoch 80 MSE: 0.0017679394222795963

Epoch 90 MSE: 0.0017151187639683485

# 计算训练得到的模型在训练集上的均方差

y_train_pred = model(trainX)

loss_fn(y_train_pred, trainY).item()

0.0016758530400693417

测试模型

# make predictions

y_test_pred = model(testX)

loss_fn(y_test_pred, testY).item()

0.004057767800986767

# 从结果来看,有些过拟合

绘制效果图

"训练集效果图"

# 无论是真实值,还是模型的输出值,它们的维度均为(batch_size, seq, 1),seq=20

# 我们的目的是用前20天的数据预测今天的股价,所以我们只需要每个数据序列中第20天的标签即可

# 因为前面用了使用DataFrame中shift方法,所以第20天的标签,实际上就是第21天的股价

pred_value = y_train_pred.detach().numpy()[:,-1,0]

true_value = trainY.detach().numpy()[:,-1,0]

plt.plot(pred_value, label="Preds") # 预测值

plt.plot(true_value, label="Data") # 真实值

plt.legend()

plt.show()

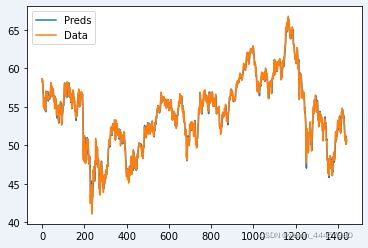

# 纵坐标还有负的,因为前面进行缩放,现在让数据还原成原来的大小

# invert predictions

pred_value = scaler.inverse_transform(pred_value.reshape(-1, 1))

true_value = scaler.inverse_transform(true_value.reshape(-1, 1))

plt.plot(pred_value, label="Preds") # 预测值

plt.plot(true_value, label="Data") # 真实值

plt.legend()

plt.show()

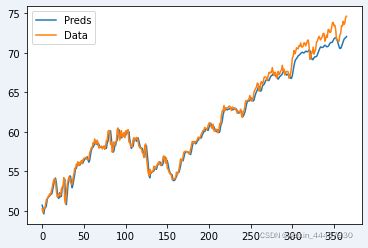

"测试集效果图"

pred_value = y_test_pred.detach().numpy()[:,-1,0]

true_value = testY.detach().numpy()[:,-1,0]

pred_value = scaler.inverse_transform(pred_value.reshape(-1, 1))

true_value = scaler.inverse_transform(true_value.reshape(-1, 1))

plt.plot(pred_value, label="Preds") # 预测值

plt.plot(true_value, label="Data") # 真实值

plt.legend()

plt.show()

前面还拟合的比较好,但是到了后面的时期就不太准确了,可能与前面模型出现过拟合有关系