python线性回归实例_线性回归的几个例子

线性回归的概念:

给定数据集D = {(x1, y1), (x2, y2)........(xm, ym)},向量x和结果y均属于实数空间R。“线性回归”试图学得一个线性模型以尽可能准确的预测实值进行标记。

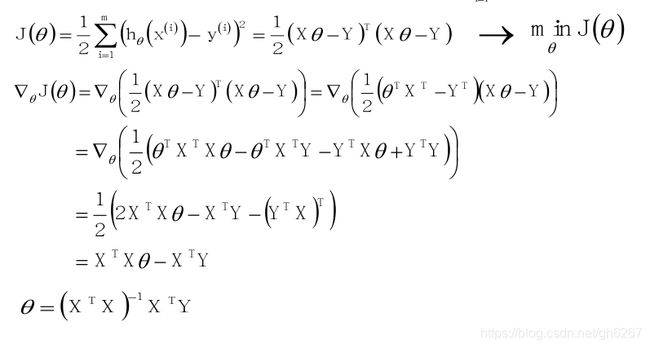

其数学表达式如下图所示:

再定义损失函数:

其中h(x)为预测值,y为真实值

现在就是要找到一个θ使得J(θ)的值最小

(1)标准公式法:

然而实际情况下

![]() 往往不满秩,为了解决这个问题,常见的做法是引入正则项。

往往不满秩,为了解决这个问题,常见的做法是引入正则项。

即:

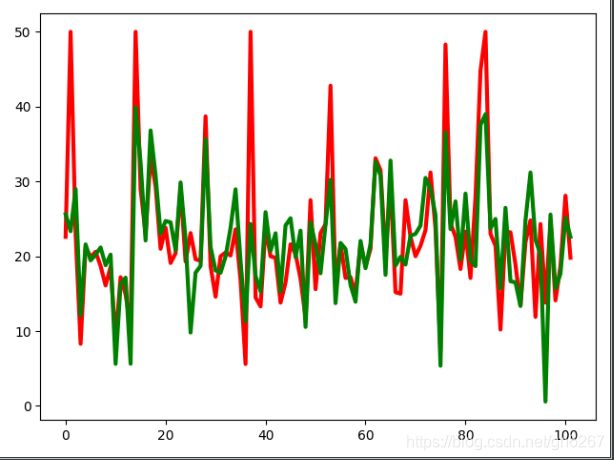

下面的例子是用线性回归预测波士顿的房价:

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from sklearn.linear_model import LinearRegression, LassoCV, RidgeCV, ElasticNetCV

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import StandardScaler

def notEmpty(s):

return s != ''

df = pd.read_csv('../datas/housing.data', header=None)

datas = np.empty((len(df), 14))

for i, d in enumerate(df.values):

d = list(map(float, filter(notEmpty, d[0].split(' '))))

datas[i] = np.array(d)

x, y = np.split(datas, (13, ), axis=1)

ss = StandardScaler()

x_train, x_test, y_train, y_test = train_test_split(x, y, test_size=0.2, random_state=0)

x_train = ss.fit_transform(x_train)

x_test = ss.transform(x_test)

model = LinearRegression()

model.fit(x_train, y_train)

print(model.score(x_train, y_train))

print(model.score(x_test, y_test))

ln_x_test = range(len(x_test))

y_predict = model.predict(x_test)

plt.plot(ln_x_test, y_predict, 'g-', lw=2)

plt.plot(ln_x_test, y_test, 'r-', lw = 2)

plt.show()

结果如下图所示:

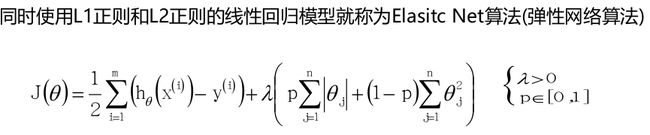

为了防止数据过拟合我们可以加入正则项

如下图所示:

使用L2正则的线性回归模型就称为Ridge回归(岭回归)

使用L1正则的线性回归模型就称为LASSO回归(Least Absolute Shrinkage and Selection Operator)

Ridge(L1-norm)和LASSO(L2-norm)比较

L2-norm中,由于对于各个维度的参数缩放是在一个圆内缩放的,不可能导致

有维度参数变为0的情况,那么也就不会产生稀疏解;实际应用中,数据的维度

中是存在噪音和冗余的,稀疏的解可以找到有用的维度并且减少冗余,提高回归

预测的准确性和鲁棒性(减少了overfitting)(L2-norm可以达到最终解的稀疏性的要求)

Ridge模型具有较高的准确性、鲁棒性以及稳定性;LASSO模型具有较高的求解

速度。

四种回归的对比代码如下:

import numpy as np

import matplotlib as mpl

import matplotlib.pyplot as plt

import pandas as pd

import warnings

import sklearn

from sklearn.linear_model import LinearRegression, LassoCV, RidgeCV, ElasticNetCV

from sklearn.preprocessing import PolynomialFeatures

from sklearn.pipeline import Pipeline

plt.rcParams['font.sans-serif'] = ['SimHei']

plt.rcParams['font.serif'] = ['SimHei']

plt.rcParams['axes.unicode_minus'] = False

np.random.seed(100)

np.set_printoptions(linewidth=1000, suppress=True)

N = 10

x = np.linspace(0, 6, N) + np.random.rand(N)

y = 1.8 * x ** 3 + x ** 2 - 14 * x - 7 + np.random.randn(N)

x.shape = -1, 1

y.shape = -1, 1

models = [

Pipeline([

('Poly', PolynomialFeatures()),

('Linear', LinearRegression())

]),

Pipeline([

('Poly', PolynomialFeatures()),

('Linear', RidgeCV(alphas=np.logspace(-3, 2, 50), fit_intercept=False))

]),

Pipeline([

('Poly', PolynomialFeatures()),

('Linear', LassoCV(alphas=np.logspace(-3, 2, 50), fit_intercept=False))

]),

Pipeline([

('Poly', PolynomialFeatures()),

('Linear', ElasticNetCV(alphas=np.logspace(-3, 2, 50), fit_intercept=False))

])

]

plt.figure(facecolor='w')

degree = np.arange(1, N, 2)

dm = degree.size

colors = []

for c in np.linspace(16711689, 255, dm):

c = int(c)

colors.append('#%06x' % c)

title = [u'Linear_Regression', u'Ridge_Regression', u'Lasso_Regression', u'Elastic_Net']

for t in range(4):

model = models[t]

plt.subplot(2, 2, t + 1)

plt.plot(x, y, 'ro', ms=10, zorder=N)

for i, d in enumerate(degree):

model.set_params(Poly__degree=d)

model.fit(x, y.ravel())

lin = model.get_params('Linear')['Linear']

output = u'%s:%d阶, 系数为:' % (title[t], d)

print(output, lin.coef_.ravel())

x_hat = np.linspace(x.min(), x.max(), num=100)

x_hat.shape = -1, 1

y_hat = model.predict(x_hat)

s = model.score(x, y)

z = N - 1 if (d == 2) else 0

label = u'%dscala, Accuracy rate=%.3f' % (d, s)

plt.plot(x_hat, y_hat, color=colors[i], lw=2, alpha=0.75, label=label, zorder=z)

plt.legend(loc='upper left')

plt.grid(True)

plt.title(title[t])

plt.xlabel('X', fontsize=16)

plt.ylabel('Y', fontsize=16)

plt.tight_layout(1, rect=(0, 0, 4, 2))

plt.show()

结果如下所示:

(2)梯度下降法:

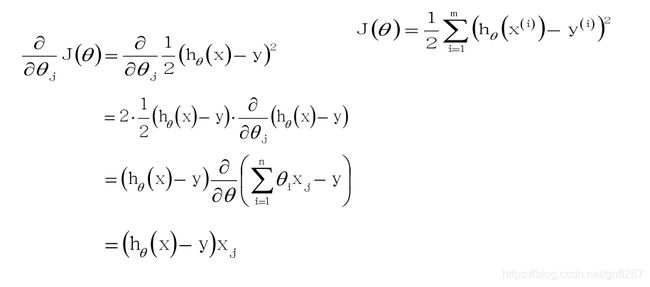

1.梯度下降算法:

对J(θ)使用梯度下降法:

梯度下降法又分为批量梯度下降(BGD),随机梯度下降(SGD),小批量梯度下降(MBGD)

BGD和SGD的比较:

(1)SGD速度比BGD快(迭代次数少)

(2)SGD在某些情况下(全局存在多个相对最优解/J(θ)不是一个二次),SGD有可能跳出某些小的局部最优解,所以不会比BGD坏,BGD一定能够得到一个局部最优解(在线性回归模型中一定是得到一个全局最优解)。

(3)SGD由于随机性的存在可能导致最终结果比BGD的差。

如果即需要保证算法的训练过程比较快,又需要保证最终参数训练的准确率,而这正是小批量梯度下降法(Mini-batch Gradient Descent,简称MBGD)的初衷。MBGD中不是每拿一个样本就更新一次梯度,而且拿b个样本(b一般为10)的平均梯度作为更新方向。

下面是利用随机梯度下降法实现“波士顿房价预测”的代码:

import numpy as np

import pandas as pd

import matplotlib as mpl

import time

import matplotlib.pyplot as plt

import sklearn

from sklearn.linear_model import LinearRegression, LassoCV, RidgeCV, ElasticNetCV, SGDRegressor

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import StandardScaler

from sklearn.preprocessing import PolynomialFeatures

from sklearn.pipeline import Pipeline

from sklearn.model_selection import GridSearchCV

def notEmpty(s):

return s != ''

fd = pd.read_csv('../datas/housing.data', header=None)

datas = np.empty((len(fd.values), 14))

for (i, d) in enumerate(fd.values):

d = list(map(float, filter(notEmpty, d[0].split(' '))))

datas[i] = np.array(d)

x, y = np.split(datas, (13, ), axis=1)

x_train, x_test, y_train, y_test = train_test_split(x, y, test_size=0.2, random_state=0)

ss = StandardScaler()

x_train = ss.fit_transform(x_train)

x_test = ss.transform(x_test)

model = SGDRegressor(loss='squared_loss',penalty='l2',alpha=0.01,max_iter=1000)

model.fit(x_train, y_train)

y_predict = model.predict(x_test)

print("训练值得分:", model.score(x_train, y_train))

print("测试值得分:", model.score(x_test, y_test))

ln_x = range(len(x_test))

plt.plot(ln_x, y_test, 'r-', lw = 3)

plt.plot(ln_x, y_predict, 'g-', lw = 3)

plt.show()

结果如下: