引言:在准备九月份的华为杯,入门选择了司守奎老师的教材《数学建模算法与应用》,书中仅提供了lingo和matlab的版本,但是python的数据处理能力更加出色,因此考虑在学习的过程中将代码全部用python实现。

第一章:线性规划

基础代码:(例题1.1)

'''

max z = 4x+3y

2x+y <= 10

x+y <= 8

y <= 7

x,y >= 0

'''

import numpy as np

from scipy.optimize import linprog

c = np.array([-4,-3])

A = np.array([[2,1],[1,1],[0,1]])

b = np.array([10,8,7])

x_bounds = (0,None)

y_bounds = (0,None)

res = linprog(c,A_ub=A,b_ub=b,bounds=[x_bounds,y_bounds])

print("Optimal value:", -res.fun)

print("Optimal value:",res.x)

基础代码:(例题1.2)

'''

max w = 2x+3y-5z

x+y+z = 7

2x-5y+z >= 10

x+3y+z <= 12

x,y,z >= 0

'''

import numpy as np

from scipy.optimize import linprog

c = np.array([-2,-3,5])

A = np.array([[-2,5,-1],[1,3,1]])

b = np.array([-10,12])

A_ = np.array([[1,1,1]])

b_ = np.array([7])

x_bounds = (0,None)

y_bounds = (0,None)

z_bounds = (0,None)

res = linprog(c,A_ub=A,b_ub=b,A_eq=A_,b_eq=b_,bounds=[x_bounds,y_bounds,z_bounds])

print("Optimal value:", -res.fun)

print("Optimal value:",res.x)

基础代码:(例题1.3)

'''

min w = 2x+3y+z

x+4y+2z >= 8

3x+2y >= 6

x,y,z >= 0

'''

import numpy as np

from scipy.optimize import linprog

c = np.array([2,3,1])

A = np.array([[-1,-4,-2],[-3,-2,0]])

b = np.array([-8,-6])

x_bounds = (0,None)

y_bounds = (0,None)

z_bounds = (0,None)

res = linprog(c,A_ub=A,b_ub=b,bounds=[x_bounds,y_bounds,z_bounds])

print("Optimal value:", res.fun)

print("Optimal value:",res.x)

基础代码:(例题1.5)

import numpy as np

from scipy.optimize import linprog

c = np.array([1,1,2,2,3,3,4,4])

A = np.array([[1,-1,-1,1,-1,1,1,-1],[1,-1,-1,1,1,-1,-3,3],[1,-1,-1,1,-2,2,3,-3]])

b = np.array([-2,-1,-1/2])

u1_bounds = (0,None)

u2_bounds = (0,None)

u3_bounds = (0,None)

u4_bounds = (0,None)

v1_bounds = (0,None)

v2_bounds = (0,None)

v3_bounds = (0,None)

v4_bounds = (0,None)

res = linprog(c,A_ub=A,b_ub=b,bounds=[u1_bounds,v1_bounds,u2_bounds,v2_bounds,u3_bounds,v3_bounds,u4_bounds,v4_bounds])

print("Optimal value:", res.fun)

print("Optimal value:",res.x)

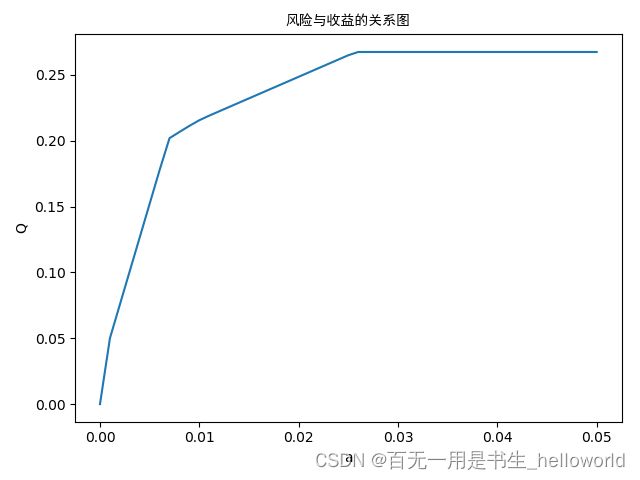

基础代码:(投资的收益与风险----------------模型一)

'''

模型一:固定风险水平 优化收益

'''

import numpy as np

from scipy.optimize import linprog

import matplotlib.pyplot as plt

def model(a):

c = np.array([-(0.05),-(0.28-0.01),-(0.21-0.02),-(0.23-0.045),-(0.25-0.065)])

A = np.array([[0,0.025,0,0,0],[0,0,0.015,0,0],[0,0,0,0.055,0],[0,0,0,0,0.026]])

b = np.array([a,a,a,a])

A_ = np.array([[(1),(1+0.01),(1+0.02),(1+0.045),(1+0.065)]])

b_ = np.array([1])

x1_bounds = (0,None)

x2_bounds = (0,None)

x3_bounds = (0,None)

x4_bounds = (0,None)

x5_bounds = (0,None)

res = linprog(c,A_ub=A,b_ub=b,A_eq =A_,b_eq=b_,bounds=[x1_bounds,x2_bounds,x3_bounds,x4_bounds,x5_bounds])

return -res.fun

def draw(x,y):

x = x

y = y

plt.plot(x, y)

plt.xlabel('a')

plt.ylabel('Q')

plt.title('风险与收益的关系图',fontproperties='SimHei')

plt.show()

if __name__ == '__main__':

a = 0;

x = [0];

y = [0];

while a < 0.05:

y_res = model(a)

a = a+0.001

x.append(a)

y.append(y_res)

draw(x,y)

- 思考:虽然根据关系图可以确定转折点的大致范围,但是怎么确定这个具体值是多少是个问题哎?而且步长为0.001,终止条件为0.05也是根据经验设定的吧,在开始的时候如果没有设定好【巧合值】的话可能连转折点都很难发现。