Python量化交易实战-37开源项目交易策略可视化

B站配套视频教程观看

PyAlgoTrade:交易策略可视化

PyAlgoTrade利用matplotlib进行交易策略可视化。它做了非常系统的工作,包括买入卖出的交易信号,以及整体的收益和单次收益都可以看到。

我们就来看一下SMA策略可视化的结果是怎么样的

上节课我们利用了backteststragedy里面的方法去跑了交易条件和回测、怎么基于实仓位的判断决定是否买卖股票、这节课就基于当前的SMA策略,来实现可视化 所以之后大家也可以基于现有的框架去测试其他策略,比如说双均线,动量策略的结果,并且将他们可视化。

一、官方示例讲解

来到官方文档的Plotting板块

http://gbeced.github.io/pyalgotrade/docs/v0.20/html/tutorial.html#plotting

from pyalgotrade import strategy

from pyalgotrade.technical import ma

from pyalgotrade.technical import cross

class SMACrossOver(strategy.BacktestingStrategy):

def __init__(self, feed, instrument, smaPeriod):

super(SMACrossOver, self).__init__(feed)

self.__instrument = instrument

self.__position = None

# We'll use adjusted close values instead of regular close values.

self.setUseAdjustedValues(True)

self.__prices = feed[instrument].getPriceDataSeries()

self.__sma = ma.SMA(self.__prices, smaPeriod)

def getSMA(self):

return self.__sma

def onEnterCanceled(self, position):

self.__position = None

def onExitOk(self, position):

self.__position = None

def onExitCanceled(self, position):

# If the exit was canceled, re-submit it.

self.__position.exitMarket()

def onBars(self, bars):

# If a position was not opened, check if we should enter a long position.

if self.__position is None:

if cross.cross_above(self.__prices, self.__sma) > 0:

shares = int(self.getBroker().getCash() * 0.9 / bars[self.__instrument].getPrice())

# Enter a buy market order. The order is good till canceled.

self.__position = self.enterLong(self.__instrument, shares, True)

# Check if we have to exit the position.

elif not self.__position.exitActive() and cross.cross_below(self.__prices, self.__sma) > 0:

self.__position.exitMarket()

这里它定义了一个策略叫做:SMACrossOver。

它和上节课的策略基本是一样的。

它增加了方法:getSMA,用于返回均价的数据。

def onBars(self, bars):函数里面定义了一个策略 买入卖出的规则稍有不同。我们就不借用它的代码,还是用之前的策略。我们主要看它可视化的部分是怎么做的

from pyalgotrade import plotter

from pyalgotrade.barfeed import quandlfeed

from pyalgotrade.stratanalyzer import returns

import sma_crossover

# Load the bar feed from the CSV file

feed = quandlfeed.Feed()

feed.addBarsFromCSV("orcl", "WIKI-ORCL-2000-quandl.csv")

# Evaluate the strategy with the feed's bars.

myStrategy = sma_crossover.SMACrossOver(feed, "orcl", 20)

# Attach a returns analyzers to the strategy.

returnsAnalyzer = returns.Returns()

myStrategy.attachAnalyzer(returnsAnalyzer)

# Attach the plotter to the strategy.

plt = plotter.StrategyPlotter(myStrategy)

# Include the SMA in the instrument's subplot to get it displayed along with the closing prices.

plt.getInstrumentSubplot("orcl").addDataSeries("SMA", myStrategy.getSMA())

# Plot the simple returns on each bar.

plt.getOrCreateSubplot("returns").addDataSeries("Simple returns", returnsAnalyzer.getReturns())

# Run the strategy.

myStrategy.run()

myStrategy.info("Final portfolio value: $%.2f" % myStrategy.getResult())

# Plot the strategy.

plt.plot()

首先,他将sma_crossover作为回测的策略。接着创建数据,然后定义策略,和之前的内容差不多。

# Attach a returns analyzers to the strategy.

returnsAnalyzer = returns.Returns()

myStrategy.attachAnalyzer(returnsAnalyzer)

这里会引用returns库,定义了returns.Returns(),然后myStrategy.attachAnalyzer(returnsAnalyzer)将收益相关的指标当作参数赋值给交易策略。

接下来是要去可视化的部分:

# Attach the plotter to the strategy.

plt = plotter.StrategyPlotter(myStrategy)

# Include the SMA in the instrument's subplot to get it displayed along with the closing prices.

plt.getInstrumentSubplot("orcl").addDataSeries("SMA", myStrategy.getSMA())

# Plot the simple returns on each bar.

plt.getOrCreateSubplot("returns").addDataSeries("Simple returns", returnsAnalyzer.getReturns())

plotter是引入的可视化的工具库。 通过交易策略构造出一个plotter对象。

接着创建一个subplot子画布,然后调用addDataSeries将每日的均价的曲线画出来。

接着创建一个subplot子画布,然后调用addDataSeries将每日的收益率的曲线画出来。

# Run the strategy.

myStrategy.run()

myStrategy.info("Final portfolio value: $%.2f" % myStrategy.getResult())

然后就开始跑这个策略。

# Plot the strategy.

plt.plot()

接着将所有的数据绘制出来。

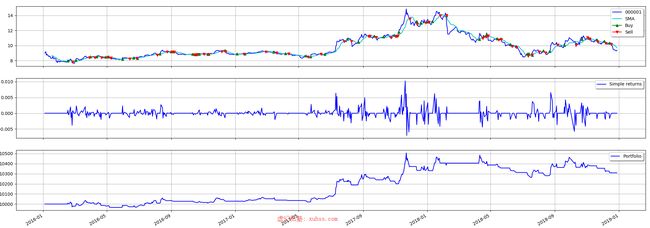

蓝色的是价格曲线,SMA是淡绿色的线,就是它的20天的平均价格。红色箭头是卖出标记 绿色箭头是买入标记。

可视化的好处是让非常直观的看到你的策略是合理的,如果都是低买高卖,那就很好对吧。、

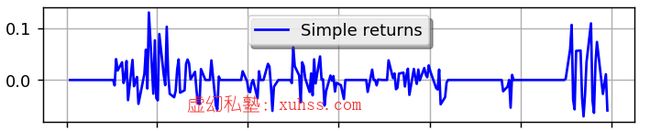

接着画出simple return(单次收益),也就是每一次赚了或亏了多少。

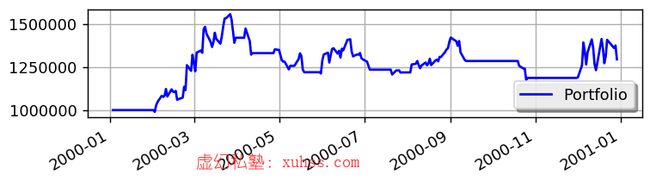

接着是portfolio,你可以看作每次操作后的累计的总收益、。

二、实战

将可视化的代码复制过去即可。

#使用pyalgotrade进行数据回测

import pyalgotrade

from pyalgotrade import strategy

from pyalgotrade.barfeed import quandlfeed

from pyalgotrade_tushare import tools, barfeed

from pyalgotrade.technical import ma

from pyalgotrade import plotter

from pyalgotrade.barfeed import quandlfeed

from pyalgotrade.stratanalyzer import returns

def safe_round(value, digits):

if value is not None:

value = round(value, digits)

return value

class MyStrategy(strategy.BacktestingStrategy):

def __init__(self, feed, instrument, smaPeriod):

super(MyStrategy, self).__init__(feed, 10000)

self.__position = None

self.__instrument = instrument

# # We'll use adjusted close values instead of regular close values.

# self.setUseAdjustedValues(True)

self.__sma = ma.SMA(feed[instrument].getPriceDataSeries(), smaPeriod)

def getSMA(self):

return self.__sma

def onEnterOk(self, position):

execInfo = position.getEntryOrder().getExecutionInfo()

#self.info("BUY at $%.2f" % (execInfo.getPrice()))

def onEnterCanceled(self, position):

self.__position = None

def onExitOk(self, position):

execInfo = position.getExitOrder().getExecutionInfo()

#self.info("SELL at $%.2f" % (execInfo.getPrice()))

self.__position = None

def onExitCanceled(self, position):

# If the exit was canceled, re-submit it.

self.__position.exitMarket()

def onBars(self, bars):

# Wait for enough bars to be available to calculate a SMA.

if self.__sma[-1] is None:

return

bar = bars[self.__instrument]

# If a position was not opened, check if we should enter a long position.

if self.__position is None:

if bar.getPrice() > self.__sma[-1]:

# Enter a buy market order for 10 shares. The order is good till canceled.

self.__position = self.enterLong(self.__instrument, 100, True)

# Check if we have to exit the position.

elif bar.getPrice() < self.__sma[-1] and not self.__position.exitActive():

self.__position.exitMarket()

def run_strategy(smaPeriod):

# Load the bar feed from the CSV file

instruments = ["000001"]

feeds = tools.build_feed(instruments, 2016, 2018, "histdata")

#print(feeds)

# Evaluate the strategy with the feed's bars.

myStrategy = MyStrategy(feeds, instruments[0], smaPeriod)

# myStrategy.run()

# # 打印总持仓:(cash + shares * price) (持有现金 + 股数*价格)

# print("Final portfolio value: $%.2f" % myStrategy.getBroker().getEquity())

# Attach a returns analyzers to the strategy.

returnsAnalyzer = returns.Returns()

myStrategy.attachAnalyzer(returnsAnalyzer)

# Attach the plotter to the strategy.

plt = plotter.StrategyPlotter(myStrategy)

# Include the SMA in the instrument's subplot to get it displayed along with the closing prices.

plt.getInstrumentSubplot(instruments[0]).addDataSeries("SMA", myStrategy.getSMA())

# Plot the simple returns on each bar.

plt.getOrCreateSubplot("returns").addDataSeries("Simple returns", returnsAnalyzer.getReturns())

# Run the strategy.

myStrategy.run()

myStrategy.info("Final portfolio value: $%.2f" % myStrategy.getResult())

# Plot the strategy.

plt.plot()

# for i in range(10, 30):

run_strategy(11)

运行

可以看到获取到了可视化的内容。

我们将时间缩短,方便具体看一下交易策略的内容。将时间改为2020-2021:

feeds = tools.build_feed(instruments, 2020, 2021, "histdata")