英文部分及图片来自“经济学人”杂志。译文是个人学习、欣赏语言之用,谢绝转载或用于任何商业用途。本人同意平台在接获有关著作权人的通知后,删除文章。

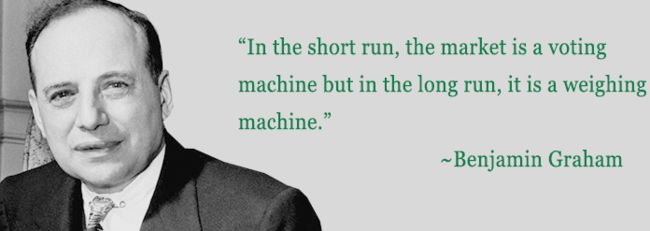

IN HIS classic, “The Intelligent Investor”, first published in 1949, Benjamin Graham, a Wall Street sage, distilled what he called his secret of sound investment into three words: “margin of safety”. The price paid for a stock or a bond should allow for human error, bad luck or, indeed, many things going wrong at once. In a troubled world of trade tiffs and nuclear braggadocio, such advice should be especially worth heeding. Yet rarely have so many asset classes—from stocks to bonds to property to bitcoins—exhibited such a sense of invulnerability.

华尔街传奇本杰明·格雷厄姆在自己1949年首次出版的经典著作《聪明的投资者》中,将他声称的稳健投资的秘密浓缩为四个字: “安全边际”。也就是说,在为股票或债券支付对价时应该考虑人为失误,糟糕的坏运气以及诸多不利因素同时出现的情形。在充斥着贸易争端和核讹诈的乱世里,这些建议尤其值得特别留意。然而如今却有如此多的投资品(从股票到债券,从房地产到比特币)罕见地展现出了一种无往而不利的气势。

Dear assets are hardly the product of euphoria. No one would mistake the bloodless run-up in global stockmarkets, credit and property over the past eight years for a reprise of the “roaring 20s”, or even an echo of the dotcom mania of the late 1990s. Yet only at the peak of those two bubbles has America’s S&P 500 been higher as a multiple of earnings measured over a ten-year cycle. Rarely have creditors demanded so little insurance against default, even on the riskiest “junk” bonds. And rarely have property prices around the world towered so high. American house prices have bounced back since the financial crisis and are above their long-term average relative to rents. Those in Britain are well above it. And in Canada and Australia, they are in the stratosphere. Add to this the craze for exotica, such as cryptocurrencies (see Free exchange), and the world is in the throes of a bull market in everything.

昂贵的资产并非兴奋的产物。没有人会把过去八年来全球股市、信贷市场和房地产市场兵不血刃的上涨归结为“咆哮的20年代”甚或是20世纪90年代末网络狂热的重演。然而,只有在这两次泡沫的顶峰时期,美国标准普尔500指数才高过了以十年周期衡量的企业盈利倍数。债权人很少只索取如此之少的违约保险,即使是在风险最高的垃圾级债券上也是如此。全球房地产价格如此之高着实罕见。自金融危机以来,美国房价已反弹至租售比高于长期平均的水平。英国的房价则要远高于美国。而加拿大和澳大利亚的房价更是飞上了天。再加上对新奇投资品(比如加密数字货币)的狂热,整个世界正处于牛市带来的剧痛之中。

Where’s the beef?

牛肉在哪里?

Asset-price booms are a source of cheer, but also anxiety. There are two immediate reasons to worry. First, markets have been steadily rising against a backdrop of extraordinarily loose monetary policy. Central banks have kept short-term interest rates close to zero since the financial crisis of 2007-08 and have helped depress long-term rates by purchasing $11trn-worth of government bonds through quantitative easing. Only now are they starting to unwind these policies. The Federal Reserve has raised rates twice this year and will soon start to sell its bondholdings. Other central banks will eventually follow. If today’s asset prices have been propped up by central-bank largesse, its end could prompt a big correction. Second, signs are appearing that fund managers, desperate for higher yields, are becoming increasingly incautious. Consider, for instance, investors’ recent willingness to buy Eurobonds issued by Iraq, Ukraine and Egypt at yields of around 7%.

资产价格的繁荣即是快乐的由来,也是焦虑的源泉。令人担心的直接原因有两个。首先,在异常宽松的货币政策背景下,市场行情一直在稳步攀升。自2007-08年金融危机以来,各国央行一直将短期利率维持在接近于零的水平上,并通过量化宽松政策购买了高达11万亿美元的政府债券,从而压低了长期利率。直到现在,央行才开始解除这些政策。美联储今年已两次加息。很快它将开始抛售其持有的债券。其他国家央行最终也会效仿。如果说目前资产价格的上涨是由央行的慷慨作为支撑,那么这些政策的终结可能会引发一次大调整。其次,种种迹象表明基金经理们正变得越来越不谨小慎微。对获取更高的收益他们有些如饥似渴。例如,投资者近期愿意购买由伊拉克、乌克兰和埃及发行的收益率约为7%的欧洲债券。

But look carefully at the broader picture, and there is some logic to the ongoing rise in asset prices. In part it is a response to an improving world economy. In the second quarter of this year global GDP grew at its fastest pace since 2010, as a recovery in emerging markets added impetus to longer-standing upswings in Europe and America. As our special report this week argues, emerging-market economies have come out of testing times in far more resilient shape.

但如果把观察的视野放得更广一些我们就会发现资产价格的持续上涨有其内在的逻辑性。在一定程度上,这是对世界经济不断改善的反应。今年二季度,全球GDP取得了自2010年以来的最快增长。而新兴市场的复苏为欧洲和美国更持久的上升势头增添了动力。正如我们本周的特别报道指出的那样,新兴市场经济体已经走出了测试时代,它们已经变得更具韧性。

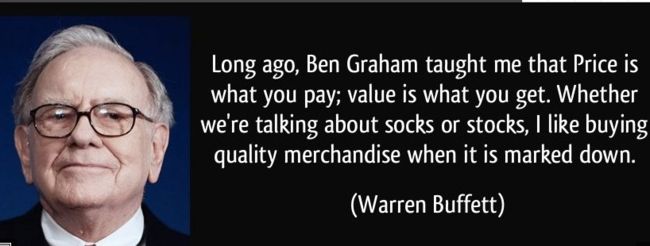

More significant still is the behaviour of long-term interest rates. They have fallen steadily since the 1980s and remain close to historic lows. And that underpins all sorts of other asset prices. A widespread concern is that the Fed and its peers have grossly distorted bond markets and, by extension, the price of all assets. Warren Buffett, the most famous disciple of Ben Graham, said this week that stocks would look cheap in three years’ time if interest rates were one percentagepoint higher, but not if they were three percentage points higher. But if interest rates and bond yields were unjustifiably low, inflation would take off—and puzzlingly it hasn’t. This suggests that factors beyond the realm of monetary policy have been a bigger cause of low long-term rates. The most important is an increase in the desire to save, as ageing populations set aside a larger share of income for retirement. Just as the supply of saving has risen, demand for it has fallen. Stagnant wages and the lower price of investment goods mean companies are flush with cash. All this suggests that interest rates will stay low by historical standards.

长期利率的运行轨迹则更为重要。自上世纪80年代以来,它们一直在稳步下降。现在它仍然在历史低点附近运行。这种情况支撑了各类资产的价格。人们普遍担心美联储及各国央行严重扭曲了债券市场,并由此推高了所有投资品的价格。沃伦·巴菲特是本杰明·格雷厄姆最著名的信徒。他在本周表示,如果利率提高一个百分点,那么以三年的周期来看股价还算便宜;但如果利率提高三个百分点,那就是另一回事了。如果利率和债券收益率低到不合理的程度,一般来说通胀就会抬头,但令人困惑的是事实并非如此。这表明,超出货币政策范围的其它因素才是长期低利率的更大原因。其中最重要的是民众储蓄意愿的增加。这是因为人口老龄化使得人们在收入中为退休后的生活预留了更多。在储蓄供给增加的同时,对借贷的需求却在下降。停滞的工资增长和较低的投资品价格意味着公司的现金普遍充裕。所有这些都表明利率还将维持在历史较低的水平上。

Beware of the bull

牛市需谨慎

Still the most dangerous, anti-Graham motto of investing is “this time is different”. It would be daft to assume that asset prices must remain high come what may. Many hazards could derail the economy and financial markets, from a debt crisis in China to an American-led trade war or an outbreak of fighting on the Korean peninsula. And when the next recession comes, policymakers have less fiscal and monetary ammunition to fight it than they had in previous downturns. Prudence therefore suggests caution.

格雷厄姆反对者的投资座右铭是“这次将与以往不同”。这种心理最为危险。不论何种情况,资产价格必须维持在高位,这种假设本身就是愚蠢的。从中国的债务危机到美国领导的贸易战,或者朝鲜半岛爆发战争等等,这些可能的危险都可能使经济和金融市场脱离正轨。当下一次衰退来临之时,政策制定者们的财政和货币手段比上一次经济衰退时还要少。审慎的建议是务必谨慎行事。

One option is for central bankers to raise rates more enthusiastically and less predictably, to jolt financial markets and remind investors that the world is volatile. Yet there are obvious perils with this course. The tightening might prove excessive, tipping economies into recession. And with inflation in most big economies below central bankers’ target, sharply higher rates are hard to square with their mandate.

一种选择是让央行行长们更积极地加息并增加加息的不可预测性,以此震动金融市场。这样可以提醒投资者世界的反复无常。然而,这种做法的危险也显而易见。紧缩政策可能会过度,从而将经济推向衰退之中。由于多数大型经济体的通胀率都低于央行行长的目标,大幅提高利率与他们的使命很难相符。

Instead, caution calls for gradualism. To minimise disruption, the reversal of quantitative easing should be stretched out. The Federal Reserve has set a good precedent by proposing to reduce its bondholdings at a leisurely pace and flagging the change well in advance. When the time comes, its peers should followsuit. Of these, the European Central Bank faces the trickiest challenge, because it has acted as, in effect, the backstop to euro-zone bond markets, a mechanism that otherwise the currency bloc still lacks.

相反,谨慎的做法是渐进主义。为了尽量减少其破坏性,定量宽松政策的逆转过程需要适当延长。美联储的做法就提供了一个良好的先例。它建议以从容的节奏减少其债券持有量,并在变化之前就提前做好警示。当时机成熟之时,其他央行也应该会纷纷效仿。其中欧洲央行面临的挑战最为棘手,因为它实际上起到了欧元区债券市场的支撑作用,而欧元区债券市场仍然缺乏这种运行机制。

But the main safety valve lies elsewhere, with banks and investors. Bitter experience has shown that debt-funded assets can magnify losses, causing financial crises. For this reason banks must be able to withstand any reversal of today’s high asset prices and low defaults. That means raising bank capital in places where it is too low, especially the euro zone, and not backsliding on strenuous “stress tests” as America’s Treasury proposes. In the end, however, there may be no escape for investors from the low future returns and even losses that high asset prices imply. They and regulators should take a leaf out of “The intelligent Investor”, and make sure that they have a margin of safety.

但是,主安全阀在于别处,比如银行和投资者。惨痛的经验表明,举债经营的资产可以放大损失,进而引发金融危机。因此,银行必须经受得住当前资产高价格和低违约率的任何反转。这意味着在银行资本金太低的国家(尤其是欧元区)需要注入银行资本,而不是像美国财政部建议的那样,在严格的“压力测试”上做出倒退。最终,投资者可能无法摆脱未来低回报的命运,甚至需要承担高资产价格所暗示的损失。投资者和监管机构都应该效仿“聪明的投资者”,确保自己有足够的安全边际。