python爬取股票数据

pip install tushare,爬取银行股票数据

对数据进行初步进行整理,用今日的收盘减去昨天的收盘值定义value表示涨跌,并绘图直观表示最近的股票走势图。其实也可以直接根据pchange>0来标签分类的 -_-

import tushare as ts

import pandas as pd

import pandas as pd

#获取中国银行历史数据

df_CB=ts.get_hist_data('601988', start='2015-01-01', end='2017-11-01')

#保存到本地

df_CB.to_csv('G:\\Project\\data\\CB.csv', sep=',' ,index=True)

#读取数据

df_CB=pd.read_csv(r'G:\\Project\\data\\CB.csv',encoding='gbk')

#将日期作为index,顺序排列

df_CB = df_CB.set_index('date')

df_CB = df_CB.sort_index()

#每天的开盘价,收盘价,交易量,价格变化,10天、20天的均价

print df_CB.head() open high close low volume price_change p_change \

date

2015-01-05 4.18 4.50 4.42 4.18 23084548.0 0.27 6.51

2015-01-06 4.38 4.74 4.56 4.28 23127260.0 0.14 3.17

2015-01-07 4.46 4.64 4.54 4.44 15485755.0 -0.02 -0.44

2015-01-08 4.55 4.57 4.33 4.31 14892726.0 -0.21 -4.63

2015-01-09 4.28 4.76 4.47 4.23 22776194.0 0.14 3.23

ma5 ma10 ma20 v_ma5 v_ma10 v_ma20 turnover

date

2015-01-05 4.036 3.862 3.736 20236083.4 20700121.8 18068874.18 1.13

2015-01-06 4.184 3.964 3.791 21016213.4 21901637.0 18406099.90 1.13

2015-01-07 4.322 4.029 3.838 20103937.2 19875380.1 18223578.34 0.76

2015-01-08 4.400 4.090 3.867 19874622.2 18551524.5 18027645.85 0.73

2015-01-09 4.464 4.180 3.901 19873296.6 19332925.8 18291454.08 1.11

#value表示涨跌,表示今日的收盘减去昨天的收盘

value = pd.Series(df_CB['close']-df_CB['close'].shift(1),\

index=df_CB.index)

#第一个值为NaN,将其后向填充

value = value.bfill()

#差值大于0表示涨,置位1

value[value>=0]=1

value[value<0]=0

df_CB['Value']=value

#后向填充空缺值

df_CB=df_CB.fillna(method='bfill')

df_CB=df_CB.astype('float64')

print df_CB.head() open high close low volume price_change p_change \

date

2015-01-05 4.18 4.50 4.42 4.18 23084548.0 0.27 6.51

2015-01-06 4.38 4.74 4.56 4.28 23127260.0 0.14 3.17

2015-01-07 4.46 4.64 4.54 4.44 15485755.0 -0.02 -0.44

2015-01-08 4.55 4.57 4.33 4.31 14892726.0 -0.21 -4.63

2015-01-09 4.28 4.76 4.47 4.23 22776194.0 0.14 3.23

ma5 ma10 ma20 v_ma5 v_ma10 v_ma20 \

date

2015-01-05 4.036 3.862 3.736 20236083.4 20700121.8 18068874.18

2015-01-06 4.184 3.964 3.791 21016213.4 21901637.0 18406099.90

2015-01-07 4.322 4.029 3.838 20103937.2 19875380.1 18223578.34

2015-01-08 4.400 4.090 3.867 19874622.2 18551524.5 18027645.85

2015-01-09 4.464 4.180 3.901 19873296.6 19332925.8 18291454.08

turnover Value

date

2015-01-05 1.13 1.0

2015-01-06 1.13 1.0

2015-01-07 0.76 0.0

2015-01-08 0.73 0.0

2015-01-09 1.11 1.0

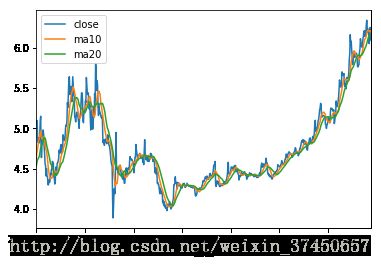

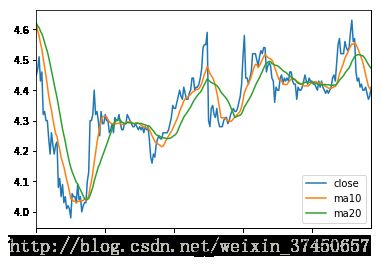

#绘图

%matplotlib inline

Data = df_CB[['open','close','ma5','ma10','ma20']]

Data=Data.astype(float)

Data.plot()

Data.ix['2016-01-01':'2017-01-01'].plot()

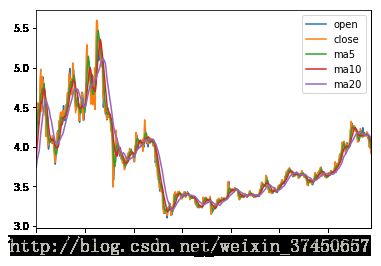

#同理获取中国工商银行等其他银行历史数据

df_gongshang=ts.get_hist_data('601398', start='2015-01-01', end='2017-11-01')

df_gongshang.to_csv('G:\\Project\\data\\gongshang.csv', sep=',' ,index=True)

df_gongshang=pd.read_csv(r'G:\\Project\\data\\gongshang.csv',encoding='gbk')

print df_gongshang.tail() date open high close low volume price_change p_change \

685 2015-01-09 4.82 5.15 4.88 4.74 9915904.0 0.05 1.03

686 2015-01-08 5.05 5.07 4.83 4.80 6920490.5 -0.21 -4.17

687 2015-01-07 5.00 5.10 5.04 4.95 8105967.5 -0.06 -1.18

688 2015-01-06 5.00 5.36 5.10 4.95 14975615.0 0.04 0.79

689 2015-01-05 4.93 5.15 5.06 4.90 13658517.0 0.19 3.90

ma5 ma10 ma20 v_ma5 v_ma10 v_ma20 turnover

685 4.982 4.818 4.628 10715298.8 9210890.05 8513672.29 0.37

686 4.980 4.763 4.614 10832707.4 8843879.40 8431188.07 0.26

687 4.956 4.728 4.600 10841814.8 8930133.55 8525606.67 0.30

688 4.870 4.695 4.571 10993154.7 9866091.80 8553582.62 0.56

689 4.774 4.626 4.533 9339578.6 8973967.90 8094866.02 0.51

#将日期作为index,顺序排列

df_gongshang = df_gongshang.set_index('date')

df_gongshang = df_gongshang.sort_index()

#print df_gongshang.tail()

#绘图

Data_gs = df_gongshang[['close','ma10','ma20']]

Data_gs=Data_gs.astype(float)

Data_gs.plot()

Data_gs.ix['2016-01-01':'2017-01-01'].plot()