ML-项目-181227-电信公司客户流失项目

建模大致思路

- 数据读取

- 数据清洗

- 两变量假设检验

- 划分训练集和测试集

- 使用训练集做模型进行预测

- 模型检验(混淆矩阵、ROC)

- 模型调优(向前法去除不显著变量、多重共线性)

各变量解释

#subscriberID=“个人客户的ID”

#churn=“是否流失:1=流失”;

#Age=“年龄”

#incomeCode=“用户居住区域平均收入的代码”

#duration=“在网时长”

#peakMinAv=“统计期间内最高单月通话时长”

#peakMinDiff=“统计期间结束月份与开始月份相比通话时长增加数量”

#posTrend=“该用户通话时长是否呈现出上升态势:是=1”

#negTrend=“该用户通话时长是否呈现出下降态势:是=1”

#nrProm=“电话公司营销的数量”

#prom=“最近一个月是否被营销过:是=1”

#curPlan=“统计时间开始时套餐类型:1=最高通过200分钟;2=300分钟;3=350分钟;4=500分钟”

#avPlan=“统计期间内平均套餐类型”

#planChange=“统计期间是否更换过套餐:1=是”

#posPlanChange=“统计期间是否提高套餐:1=是”

#negPlanChange=“统计期间是否降低套餐:1=是”

#call_10086=“拨打10086的次数”

1.数据读取

首先读入数据

#%%

import os

import pandas as pd

#%%

os.chdir(r'D:\data_py\chapter5\ML_project_181227_chapter5')

telecom_churn=pd.read_csv('telecom_churn.csv')

数据有3463个观测,20个变量。

![]()

2.数据清洗

判断数据有多少的NA

telecom_na=pd.isna(telecom_churn)

for name in telecom_na.columns:

print(telecom_na[name].value_counts())

输出结果如图,发现该数据集并无NA

3.两变量假设检验

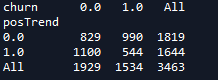

检验posTrend和churn是否相关,因为两变量均为离散性变量,先做列联表

cross_table=pd.crosstab(telecom_churn.posTrend,telecom_churn.churn,margins=True)

cross_table

可见posTrend为1的人流失的比例相对为0的人更少

不妨将列联表化为百分比形式

def percConvert(ser):

return ser/float(ser[2])

cross_table_pct=cross_table.apply(percConvert,axis=1)

cross_table_pct

可见posTrend为0的人违约概率54.4%,为1的人违约概率为33.1%

对两变量进行卡方检验判断相关性

from scipy import stats

print('''chisq=%6.4f

p-value=%6.4f

dof=%i

expected_freq=%s''' %stats.chi2_contingency(cross_table.iloc[:2,:2]))

可见非常显著

4.划分训练集与测试集

train=telecom_churn.sample(frac=0.7,random_state=1234).copy()

test=telecom_churn[~telecom_churn.index.isin(train.index)].copy()

print('训练集样本量: %i \n测试集样本量: %i'%(len(train),len(test)))

划分后得到训练集2424样本,测试集1039样本

![]()

5.使用训练集模型进行预测

5.1单变量预测posTrend,churn

import statsmodels.formula.api as smf

import statsmodels.api as sm

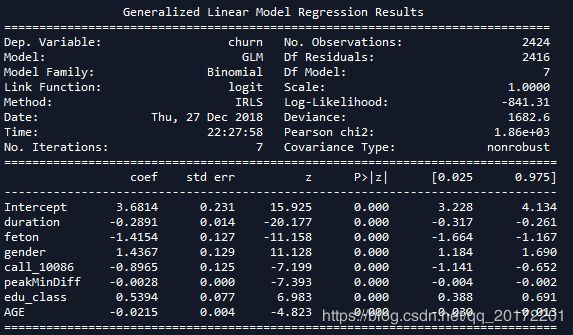

lg=smf.glm('churn~posTrend',data=telecom_churn,family=sm.families.Binomial(sm.families.links.logit)).fit()

lg.summary()

可见

[图片插入]

5.2多变量逻辑回归

对于逻辑回归来说,因变量必须是分类变量,自变量可以是连续变量也可以是分类变量。

#incomeCode#peakMinAv#nrProm#curPlan#avgplan#planChange#negPlanChange 均不相关

formula='''

churn~gender+AGE+edu_class+incomeCode+duration+feton+peakMinAv+peakMinDiff+posTrend+negTrend+nrProm+

curPlan+avgplan+planChange+negPlanChange+call_10086'''

lg_m=smf.glm(formula=formula,data=train,family=sm.families.Binomial(sm.families.links.logit)).fit()

lg_m.summary()

以下变量与churn无相关性,将从模型中剔除

#incomeCode

#peakMinAv

#nrProm

#curPlan

#avgplan

#planChange

#negPlanChange

6.模型检验

7.模型调优

7.1通过向前法进行模型调优

candidates=['churn','gender','AGE','edu_class','incomeCode','duration','feton','peakMinAv','peakMinDiff','posTrend','negTrend','nrProm','curPlan','avgplan','planChange','negPlanChange','call_10086']

data_for_select=train[candidates]

lg_m1=forward_select(data=data_for_select,response='churn')

向前法操作后,变量由16个变为11个

重新做逻辑回归

formula='''

churn ~ duration + feton + gender + call_10086 + peakMinDiff + edu_class + AGE + posTrend + negTrend + peakMinAv + nrProm'''

lg_m1=smf.glm(formula=formula,data=train,family=sm.families.Binomial(sm.families.links.logit)).fit()

lg_m1.summary()

?回想起似乎向前法只能做一次,删掉不相关的变量后依然会有新的p值大于阈值的变量出现。?

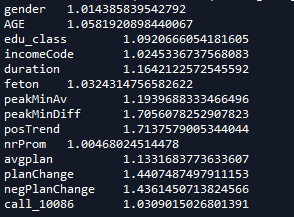

7.2判断是否存在多重共线性

定义vif判别函数

def vif(df,col_i):

from statsmodels.formula.api import ols

cols=list(df.columns)

cols.remove(col_i)

cols_noti=cols

formula = col_i + '~' + '+'.join(cols_noti)

r2=ols(formula,df).fit().rsquared

return 1./(1. -r2)

exog=train[candidates].drop(['churn'],axis=1)

for i in exog.columns:

print(i,'\t',vif(df=exog,col_i=i))

可见posTrend和negTrend存在共线性,curPlan和avgplan存在共线性

删除negTrend和curPlan

可见多重共线性消失

同时删除3个不显著变量posTrend + peakMinAv + nrProm

得到模型

7.3输出模型流失概率

train['proba']=lg_m1.predict(train)

test['proba']=lg_m1.predict(test)

test['proba'].head()

test['prediction']=(test['proba']>0.5).astype('int')

输出结果如下

8.模型评估

首先计算模型预测准确率

import numpy as np

acc=sum(test['prediction']==test['churn'])/np.float(len(test))

print('The accurancy is %.2f' %acc)

预测准确率为0.82

接下来绘制混淆矩阵

pd.crosstab(test.churn,test.prediction,margins=True)

计算可得召回率达到368/456=0.807

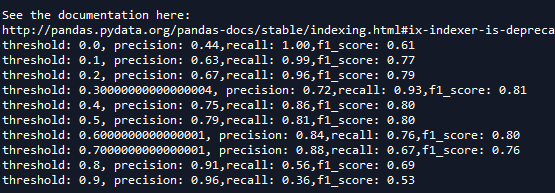

根据f1_score计算可得最佳的阈值应该设为0.3

for i in np.arange(0,1,0.1):

prediction=(test['proba']>i).astype('int')

confusion_matrix=pd.crosstab(test.churn,prediction,margins=True)

precision=confusion_matrix.ix[1,1]/confusion_matrix.ix['All',1]

recall=confusion_matrix.ix[1,1]/confusion_matrix.ix[1,'All']

f1_score=2*(precision*recall)/(precision+recall)

print('threshold: %s, precision: %.2f,recall: %.2f,f1_score: %.2f'%(i,precision,recall,f1_score))

重新计算模型,准确率降为0.81,召回率升为92.5%

绘制ROC曲线

import sklearn.metrics as metrics

import matplotlib.pyplot as plt

fpr_test, tpr_test, th_test=metrics.roc_curve(test.churn,test.proba)

fpr_train,tpr_train,th_train=metrics.roc_curve(train.churn,train.proba)

plt.figure(figsize=[3,3])

plt.plot(fpr_test,tpr_test,'b--')#虚线

plt.plot(fpr_train,tpr_train,'r-')#实线

plt.title('ROC curve')

plt.show()

测试集(虚线)与训练集(实线)拟合的非常好,存在过拟合的可能性较小

print('AUC=%.4f'%metrics.auc(fpr_test,tpr_test))

计算AUC值,再次发现AUC值与阈值无关

![]()

END