Python-统计学应用-回归分析

import pandas as pd

import statsmodels.api as sm

import matplotlib.pyplot as plt

import numpy as np

一元线性回归

拟合线性模型主要通过statsmodels包中的OLS类完成

- fit()——得到线性回归的结果

- summary()——看出拟合模型的详细结果

- params()——列入拟合模型的参数

- conf_int()——提供模型参数的置信区间

- fittedvalues——模型的拟合值

- resid——模型的残差值

- aic——赤池信息统计量

- predict()——用拟合模型对新的数据集预测解释变量

trd_index = pd.read_table('TRD_Index.txt', sep='\t')

sh_index = trd_index[trd_index.Indexcd == 1]

sz_index = trd_index[trd_index.Indexcd == 399106]

sh_ret = sh_index.Retindex

sz_ret = sz_index.Retindex

sh_ret.index = sz_ret.index

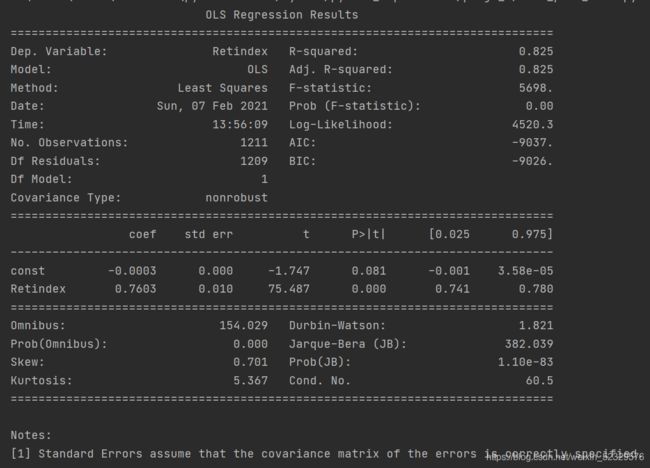

model = sm.OLS(sh_ret, sm.add_constant(sz_ret)).fit()

print(model.summary())

结果:

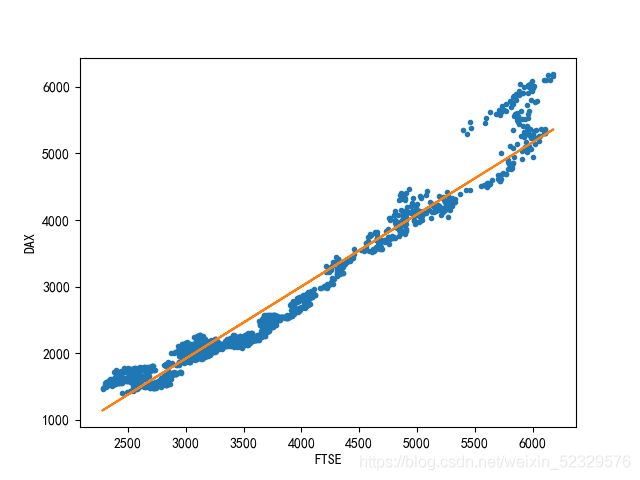

绘制拟合曲线

model = sm.OLS(eu_stock_market.DAX, sm.add_constant(eu_stock_market.FTSE)).fit()

print(model.summary())

plt.plot(eu_stock_market.FTSE, eu_stock_market.DAX, '.',

eu_stock_market.FTSE, model.fittedvalues, '-')

plt.xlabel('FTSE')

plt.ylabel('DAX')

plt.show()

模型检验

- 线性:若因变量与自变量线性相关,残差值应该和拟合值没有任何的系统关联,呈现出围绕0随机分布的状态。

plt.scatter(model.fittedvalues, model.resid)

plt.xlabel('fitted_values')

plt.ylabel('resid')

plt.show()

基本满足该假设。

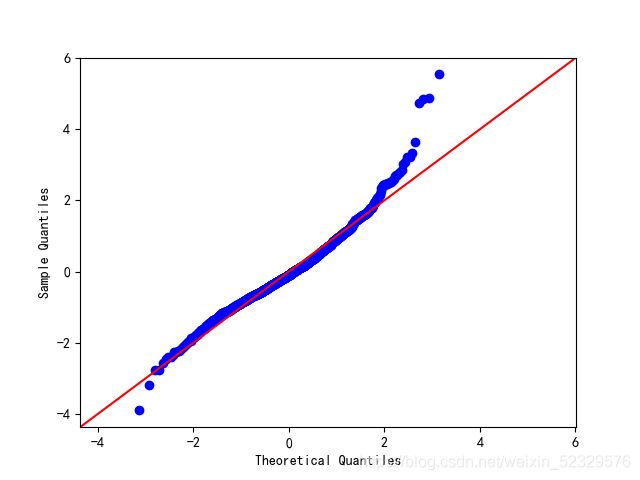

- 正态性:当因变量呈正态分布时,模型的残差项应该是一个均值为0的正态分布。

[正态Q-Q图是在正态分布对应的值下,标准化残差的概率图,若满足正态性假设,那么图上的点应该落在一条直线上,若不是,则违背了正态性的假设]

sm.qqplot(model.resid_pearson, stats.norm, line='45')

plt.show()

*残差在两端出现了较为严重的偏离,数据可能不满足正态性假设。

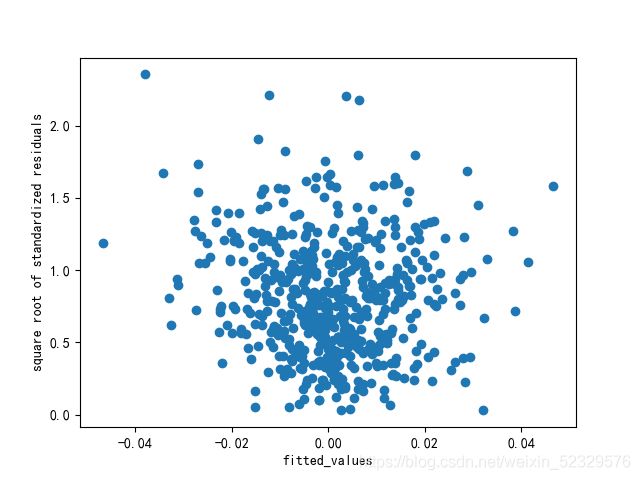

- 同方差性:若满足不变方差假设,那么再位置尺度图上,各点分布应该呈现出一条水平的宽度一致的条带形状。

plt.scatter(model.fittedvalues,model.resid_pearson**0.5)

plt.xlabel('fitted_values')

plt.ylabel('square root of standardized residuals')

plt.show()

基本满足该假设。

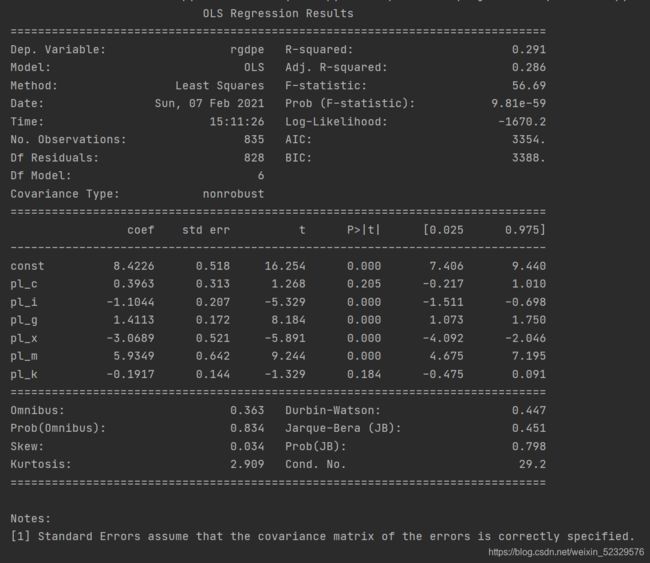

多元线性回归

penn = pd.read_csv('Penn World Table——1.csv')

model = sm.OLS(np.log(penn.rgdpe), sm.add_constant(penn.iloc[:, -6:])).fit()

print(model.summary())

其中pl_c, pl_k不显著。

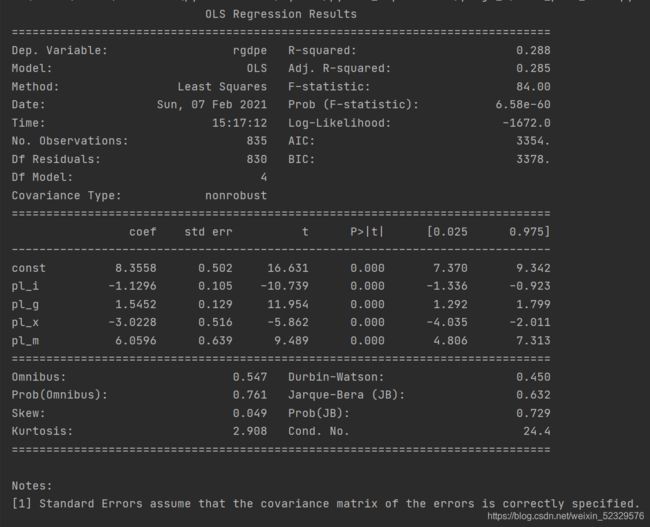

自变量共线性因素的新模型

print(penn.iloc[:, -6:].corr())

# 结果

# pl_c pl_i pl_g pl_x pl_m pl_k

# pl_c 1.000000 0.718931 0.636698 0.078841 0.213328 0.553757

# pl_i 0.718931 1.000000 0.259183 0.072019 0.139333 0.779306

# pl_g 0.636698 0.259183 1.000000 0.130729 0.256069 0.211259

# pl_x 0.078841 0.072019 0.130729 1.000000 0.477304 -0.065623

# pl_m 0.213328 0.139333 0.256069 0.477304 1.000000 0.000531

# pl_k 0.553757 0.779306 0.211259 -0.065623 0.000531 1.000000

可以看出,pl_c和多个变量之间存在较强的相关性且pl_k和pl_i的相关系数也较大。

优化模型为:

model = sm.OLS(np.log(penn.rgdpe), sm.add_constant(penn.iloc[:, -5:-1])).fit()

print(model.summary())

示例

Y = b0 + b1X + b2X **2 + ε , ε~N(0, δ **2)

x = [20, 25, 30, 35, 40, 50, 60, 65, 70, 75, 80, 90]

y = [1.81, 1.7, 1.65, 1.55, 1.48, 1.4, 1.3, 1.26, 1.24, 1.21, 1.2, 1.18]

plt.scatter(x, y)

plt.show()

independent = np.array([x, [i ** 2 for i in x]]).T

model = sm.OLS(y, sm.add_constant(independent)).fit()

print(model.summary())

print(model.predict(np.array([1, 95, 95 ** 2])).T)

当ethnicity的数据非数值时:

import statsmodels.formula.api as smf

cps = pd.read_csv('CPS1988.csv')

model = smf.ols('np.log(wage)~experience+education+ethnicity',

data=cps).fit()

print(model.summary())

model2 = smf.ols('np.log(wage)~experience+np.power(experience,2)+education+ethnicity',

data=cps).fit()

print(model2.summary())