金融数值方法之回归计算-python实践

python的回归学习

前言

回归和插值是金融中常用的两种数学方法,本章将介绍关于回归的一些常用方法和代码。

一、回归是什么

回归是一种高效的求解函数近似值的工具,不仅对一维函数适用,同样也适用于高维函数。

最小化回归问题表达如下:

在回归的计算中,常用的范式为np.polyfit()、np.polyval()、np.linalg.lstsq()。

二、回归计算的具体实现

首先进行一些准备工作

import numpy as np

import matplotlib.pyplot as plt

from pylab import plt,mpl

plt.style.use('seaborn')

mpl.rcParams['font.family']='serif'

def f(x):

return np.sin(x)+0.5*x

def create_plot(x,y,styles,labels,axlabels):

plt.figure(figsize=(12,10))

for i in range(len(x)):

plt.plot(x[i],y[i],styles[i],label=labels[i])

plt.xlabel(axlabels[0])

plt.ylabel(axlabels[1])

plt.legend(loc=0)

x=np.linspace(-2*np.pi,2*np.pi,50)

create_plot([x],[f(x)],['r'],['f(x)'],['x','f(x)'])

得到一个自定义的函数,如下所示:

1.单项式的回归

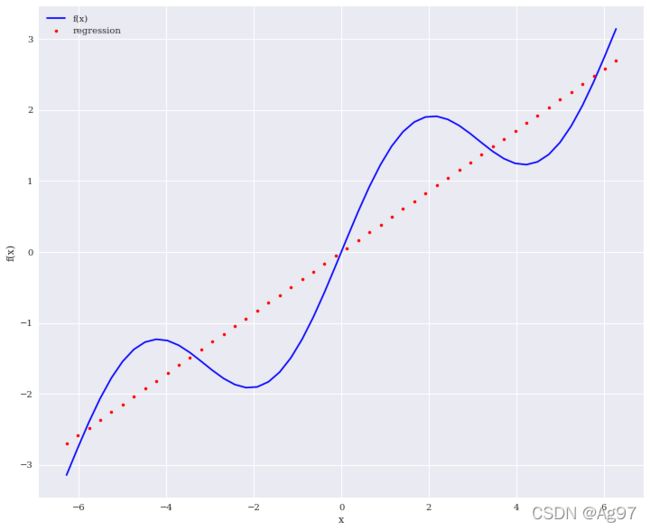

res=np.polyfit(x,f(x),deg=1,full=True)

print(res)

print('-'*108)

print(res[0])

得到参数

(array([ 4.28841952e-01, -5.29906205e-17]), array([21.03238686]), 2, array([1., 1.]), 1.1102230246251565e-14)

------------------------------------------------------------------------------------------------------------

[ 4.28841952e-01 -5.29906205e-17]

使用回归参数求值:

ry=np.polyval(res[0],x)

ry

array([-2.69449345, -2.58451412, -2.4745348 , -2.36455548, -2.25457615,

-2.14459683, -2.0346175 , -1.92463818, -1.81465885, -1.70467953,

-1.5947002 , -1.48472088, -1.37474156, -1.26476223, -1.15478291,

-1.04480358, -0.93482426, -0.82484493, -0.71486561, -0.60488628,

-0.49490696, -0.38492764, -0.27494831, -0.16496899, -0.05498966,

0.05498966, 0.16496899, 0.27494831, 0.38492764, 0.49490696,

0.60488628, 0.71486561, 0.82484493, 0.93482426, 1.04480358,

1.15478291, 1.26476223, 1.37474156, 1.48472088, 1.5947002 ,

1.70467953, 1.81465885, 1.92463818, 2.0346175 , 2.14459683,

2.25457615, 2.36455548, 2.4745348 , 2.58451412, 2.69449345])

create_plot([x,x],[f(x),ry],['b','r.'],['f(x)','regression'],['x','f(x)'])

不太理想,使用五次单项式进行回归

res=np.polyfit(x,f(x),deg=5,full=True)

ry=np.polyval(res[0],x)

create_plot([x,x],[f(x),ry],['b','r.'],['f(x)','regression'],['x','f(x)'])

使用七次单项式进行回归:

res=np.polyfit(x,f(x),deg=7,full=True)

ry=np.polyval(res[0],x)

np.allclose(f(x),x)

False

false说明回归数值与原来的数值不是一样的。

计算mse

# mse计算

np.mean((f(x)-ry)**2)

0.00177691347595176

create_plot([x,x],[f(x),ry],['b','r.'],['f(x)','regression'],['x','f(x)'])

2.单独基函数

单独的基函数

np.linalg.lstsq

numpy.linalg.lstsq(a, b, rcond=‘warn’)

将least-squares解返回线性矩阵方程。

lstsq的输出包括四部分:回归系数、残差平方和、自变量X的秩、X的奇异值。一般只需要回归系数就可以了。

matrix=np.zeros((3+1,len(x)))

matrix[3,:]=x**3

matrix[2,:]=x**2

matrix[1,:]=x**1

matrix[0,:]=x**0

reg=np.linalg.lstsq(matrix.T,f(x),rcond=None)

reg[0].round(4)

ry=np.dot(reg[0].round(4),matrix)

ry

array([-2.19670554, -2.20978519, -2.2100222 , -2.19796307, -2.17415429,

-2.13914236, -2.09347378, -2.03769503, -1.97235262, -1.89799303,

-1.81516277, -1.72440833, -1.6262762 , -1.52131289, -1.41006488,

-1.29307866, -1.17090075, -1.04407762, -0.91315578, -0.77868173,

-0.64120195, -0.50126293, -0.35941119, -0.21619321, -0.07215549,

0.07215549, 0.21619321, 0.35941119, 0.50126293, 0.64120195,

0.77868173, 0.91315578, 1.04407762, 1.17090075, 1.29307866,

1.41006488, 1.52131289, 1.6262762 , 1.72440833, 1.81516277,

1.89799303, 1.97235262, 2.03769503, 2.09347378, 2.13914236,

2.17415429, 2.19796307, 2.2100222 , 2.20978519, 2.19670554])

create_plot([x,x],[f(x),ry],['b','r.'],['f(x)','regression'],['x','f(x)'])

不太理想,将基函数中引入sinx函数

matrix[3,:]=np.sin(x)

reg=np.linalg.lstsq(matrix.T,f(x),rcond=None)

ry=np.dot(reg[0].round(4),matrix)

np.allclose(f(x),ry)

np.mean((f(x)-ry)**2)

create_plot([x,x],[f(x),ry],['b','r.'],['f(x)','regression'],['x','f(x)'])

3.有噪声的数据

# 有噪声的数据

xn=np.linspace(-2*np.pi,2*np.pi,50)

xn=xn+0.15*np.random.standard_normal(len(xn))

yn=f(xn)+0.15*np.random.standard_normal(len(xn))

reg=np.polyfit(xn,yn,7)

ry=np.polyval(reg,xn)

ry

array([-3.0627005 , -2.60200449, -2.38959333, -2.14942554, -2.01409671,

-1.50484513, -1.226107 , -1.17844569, -1.16512748, -1.23329004,

-1.26882923, -1.38858866, -1.47419669, -1.59087693, -1.83814445,

-1.81224556, -1.8320825 , -1.84258301, -1.60920776, -1.61014972,

-1.38753972, -1.01243076, -0.97922089, -0.47757572, -0.26812475,

0.47485607, 0.37666023, 0.83580311, 1.39354247, 1.4589287 ,

1.47395115, 1.73692656, 1.82542423, 1.86622981, 1.91271619,

1.82514849, 1.62685373, 1.71879336, 1.54893674, 1.29743082,

1.21692138, 1.21670403, 1.21887745, 1.34122101, 1.48378654,

1.68455375, 2.39712865, 2.67237991, 3.06596453, 3.46057519])

create_plot([xn,xn],[yn,ry],['b','r.'],['f(xn)','regression'],['xn','f(xn)'])

4.未排序的数据

# 未排序的数据

xu=np.random.rand(50)*4*np.pi-2*np.pi

yu=f(xu)

reg=np.polyfit(xu,yu,5)

ry=np.polyval(reg,xu)

create_plot([xu,xu],[f(xu),ry],['b.','ro'],['f(xu)','regression'],['xu','f(xu)'])

5.多维的数据

# 多维

def fm(p):

x,y=p

return np.sin(x)+0.25*x+np.sqrt(y)+0.05*y**2

x=np.linspace(0,10,20)

y=np.linspace(0,10,20)

X,Y=np.meshgrid(x,y)

z=fm((X,Y))

x=X.flatten()

y=Y.flatten()

from mpl_toolkits.mplot3d import Axes3D

fig=plt.figure(figsize=(12,10))

ax=fig.gca(projection='3d')

surf=ax.plot_surface(X,Y,z,rstride=2,cstride=2,cmap='coolwarm',linewidth=0.5,

antialiased=True)

ax.set_xlabel('x')

ax.set_ylabel('y')

ax.set_zlabel('f(x,y)')

matrix=np.zeros((len(x),6+1))

matrix[:,6]=np.sqrt(y)

matrix[:,5]=np.sin(x)

matrix[:,4]=y**2

matrix[:,3]=x**2

matrix[:,2]=y

matrix[:,1]=x

matrix[:,0]=1

reg=np.linalg.lstsq(matrix,fm((x,y)),rcond=None)

rz=np.dot(matrix,reg[0].round(4)).reshape(20,20)

from mpl_toolkits.mplot3d import Axes3D

fig=plt.figure(figsize=(12,10))

ax=fig.gca(projection='3d')

surf1=ax.plot_surface(X,Y,z,rstride=2,cstride=2,cmap='coolwarm',linewidth=0.5,

antialiased=True)

surf2=ax.plot_wireframe(X,Y,rz,rstride=2,cstride=2,label='regression')

ax.set_xlabel('x')

ax.set_ylabel('y')

ax.set_zlabel('f(x,y)')

ax.legend()

fig.colorbar(surf,shrink=0.5,aspect=5)

总结

金融数值方法中的回归计算。