完美解决共线性数据的问题

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import statsmodels.api as sm

import statsmodels.stats.outliers_influence

from statsmodels.stats.outliers_influence import variance_inflation_factor

Ols

data=pd.read_csv("C:/Users/可乐怪/Desktop/线性回归2021/linear2021.csv")

data.insert(4,'constant',1)

model=sm.OLS(data['y'],data.iloc[:,:5]).fit()

print(model.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.542

Model: OLS Adj. R-squared: 0.501

Method: Least Squares F-statistic: 13.32

Date: Wed, 22 Dec 2021 Prob (F-statistic): 3.07e-07

Time: 13:22:25 Log-Likelihood: -64.548

No. Observations: 50 AIC: 139.1

Df Residuals: 45 BIC: 148.7

Df Model: 4

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

x1 0.7096 0.469 1.513 0.137 -0.235 1.654

x2 0.5776 1.498 0.386 0.702 -2.439 3.594

x3 0.6079 1.476 0.412 0.682 -2.365 3.581

x4 1.0829 0.271 3.995 0.000 0.537 1.629

constant 2.6947 0.620 4.348 0.000 1.447 3.943

==============================================================================

Omnibus: 0.050 Durbin-Watson: 1.891

Prob(Omnibus): 0.975 Jarque-Bera (JB): 0.229

Skew: -0.041 Prob(JB): 0.892

Kurtosis: 2.679 Cond. No. 42.7

==============================================================================

VIF>10,存在多共线性

from statsmodels.stats.outliers_influence import variance_inflation_factor

vif=[]

for i in range(4):

a=round(variance_inflation_factor(data.iloc[:,:5].values,i),2)

vif.insert(i,a)

print(vif)

[10.42, 30.38, 36.02, 1.08]

Ridge 回归

标准化数据做回归

data_scale=pd.DataFrame()

from sklearn import preprocessing

data_scale['y'] =preprocessing.scale(data['y'])

data_scale['x1'] =preprocessing.scale(data['x1'])

data_scale['x2'] =preprocessing.scale(data['x2'])

data_scale['x3'] =preprocessing.scale(data['x3'])

data_scale['x4']=preprocessing.scale(data['x4'])

data_scale.insert(1,'constant',1)

model2=sm.OLS(data_scale['y'],data_scale.iloc[:,2:]).fit()

print(model2.summary())

OLS Regression Results

=======================================================================================

Dep. Variable: y R-squared (uncentered): 0.542

Model: OLS Adj. R-squared (uncentered): 0.502

Method: Least Squares F-statistic: 13.62

Date: Wed, 22 Dec 2021 Prob (F-statistic): 2.12e-07

Time: 13:51:57 Log-Likelihood: -51.417

No. Observations: 50 AIC: 110.8

Df Residuals: 46 BIC: 118.5

Df Model: 4

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

x1 0.4926 0.322 1.530 0.133 -0.156 1.141

x2 0.2144 0.550 0.390 0.698 -0.893 1.321

x3 0.2493 0.599 0.416 0.679 -0.956 1.454

x4 0.4191 0.104 4.039 0.000 0.210 0.628

==============================================================================

Omnibus: 0.050 Durbin-Watson: 1.891

Prob(Omnibus): 0.975 Jarque-Bera (JB): 0.229

Skew: -0.041 Prob(JB): 0.892

Kurtosis: 2.679 Cond. No. 12.2

==============================================================================

from sklearn.linear_model import Ridge

k=np.linspace(0,1,100)#(start, end, num=num_points)使k属于[0,1]

y=data_scale['y']

x=data_scale.iloc[:,2:]

θ1=[]

θ2=[]

θ3=[]

θ4=[]

for i in range(len(k)):

ridge = Ridge(k[i])

ridge =ridge .fit(x, y)

θ1.append(ridge.coef_[0])

θ2.append(ridge.coef_[1])

θ3.append(ridge.coef_[2])

θ4.append(ridge.coef_[3])

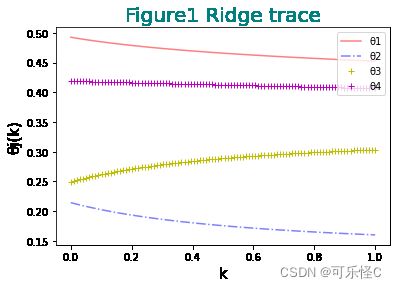

plt.plot(k,θ1,'r',alpha=0.5,)

plt.plot(k,θ2,'b-.',alpha=0.5)

plt.plot(k,θ3,'y+')

plt.plot(k,θ4,'m+')

plt.xlabel('k',size=15)

plt.ylabel('θj(k)',size=15)

plt.legend(['θ1', 'θ2', 'θ3','θ4'], loc='upper right')

plt.title('Figure1 Ridge trace',size=20,c='teal')

plt.show()

由Ridge trace可知去除x2然后做回归

model2=sm.OLS(data['y'],data[['x1','x4','x3']]).fit()

print(model2.summary())

OLS Regression Results

=======================================================================================

Dep. Variable: y R-squared (uncentered): 0.968

Model: OLS Adj. R-squared (uncentered): 0.966

Method: Least Squares F-statistic: 480.7

Date: Wed, 22 Dec 2021 Prob (F-statistic): 2.94e-35

Time: 14:01:26 Log-Likelihood: -73.676

No. Observations: 50 AIC: 153.4

Df Residuals: 47 BIC: 159.1

Df Model: 3

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

x1 0.5201 0.191 2.725 0.009 0.136 0.904

x4 2.1311 0.151 14.160 0.000 1.828 2.434

x3 1.7593 0.277 6.362 0.000 1.203 2.316

==============================================================================

Omnibus: 0.426 Durbin-Watson: 2.274

Prob(Omnibus): 0.808 Jarque-Bera (JB): 0.584

Skew: -0.110 Prob(JB): 0.747

Kurtosis: 2.518 Cond. No. 4.63

==============================================================================

拟合完美R^2=0.968

数据文件

链接:https://pan.baidu.com/s/12rI3jTX0cQ6UQu_R1jQpDA

提取码:hd5k