python量化策略——多均值-趋势-股债轮动-策略

- 考虑两种资产,股票和债券。根据星号轮动配置。

- 构建多个动量,当同时满足时,买入信号(股票)

- 读取数据,并计算t1、t2、t3、t4和t5天的均值,

- if DF[i]>nmean3[i] and DF[i]>nmean4[i] and DF[i]>n*mean5[i] 则 买入股票,else:买入债券

运行下程序,需要获取财经数据库的token码,这里获取token

"""

@dazip

"""

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from datetime import datetime, date

from statsmodels.regression import linear_model

import statsmodels.api as sm

import threading

from queue import Queue

import math

import tushare as ts

import matplotlib

import talib

import seaborn as sns

sns.set(style="darkgrid", palette="muted", color_codes=True)

from scipy import stats,integrate

%matplotlib inline

sns.set(color_codes=True)

matplotlib.rcParams['axes.unicode_minus']=False

plt.rcParams['font.sans-serif'] = ['SimHei'] # 中文显示

plt.rcParams['axes.unicode_minus'] = False # 用来正常显示负号

code1="000001.SH"

code2="000012.SH"

#freq=65

def momentum(freq=65,test_start="20100101",test_end="20201001",t1=5,t2=10,t3=15,t4=20,t5=25,n=1):

#读取数据

def dataread():

ts.set_token('toke码')#需要获取token码https://tushare.pro/register?reg=385920

pro = ts.pro_api()

df_stock=pro.index_daily(ts_code=code1, start_date=test_start, end_date=test_end, fields='close,trade_date')

df_bond=df=pro.index_daily(ts_code=code2,start_date=test_start, end_date=test_end , fields='trade_date,close')

return df_stock,df_bond

df_stock,df_bond=dataread()

#计算均值,时间为t1 t2 t3 t4

def mean(t):

df_stock.index=pd.to_datetime(df_stock.trade_date)

return df_stock.close.sort_index().rolling(window=t).mean()

def ret_base():

df_stock.index=pd.to_datetime(df_stock.trade_date)

df_bond.index =pd.to_datetime(df_bond.trade_date)

ret_stock=(df_stock.close-df_stock.close.shift(-1))/df_stock.close.shift(-1)

ret_bond= (df_bond.close- df_bond.close.shift(-1))/df_bond.close.shift(-1)

return ret_stock,ret_bond.sort_index()

def ret_same_time(x):

return x[x.index>=mean(max(t1,t2,t3,t4,t5)).dropna().index[0] ]

ret_stock=ret_same_time(ret_base()[0]).sort_index()#ret_base()[0][ret_base()[0].index>=mean(max(t1,t2,t3,t4,t5)).dropna().index[0] ]

ret_bond= ret_same_time(ret_base()[1] )#ret_base()[1][ret_base()[1].index>=mean(max(t1,t2,t3,t4,t5)).dropna().index[0] ]

DF=ret_same_time(df_stock.close).sort_index()

mean1=ret_same_time(mean(t1))

mean2=ret_same_time(mean(t2))

mean3=ret_same_time(mean(t3))

mean4=ret_same_time(mean(t4))

mean5=ret_same_time(mean(t5))

def sig_fun():

sig_stock=pd.Series(0,ret_stock.index )

sig_bond= pd.Series(0,ret_bond.sort_index().index)

for i in range(math.ceil(len(ret_stock)/freq)-1):

if DF[i*freq]>n*mean1[i*freq] and DF[i*freq]>n*mean2[i*freq] and DF[i*freq]>n*mean3[i*freq] and DF[i*freq]>n*mean4[i*freq] and DF[i*freq]>n*mean5[i*freq]:

for j in range(i*freq,(1+i)*freq):

sig_stock[j]=1

sig_bond[j]=0

else:

for j in range(i*freq,(i+1)*freq):

sig_stock[j]=0

sig_bond[j]=1

for i in range(freq*(math.ceil(len(ret_stock)/freq)-1),len(ret_bond)):

k=freq*(math.ceil(len(ret_stock)/freq)-1)

if DF[k]>mean1[k] and DF[k]>mean2[k] and DF[k]>mean3[k] and DF[k]>mean4[k] and DF[k]>mean5[k]:

sig_stock[i]=1

sig_bond[i]=0

else:

sig_stock[i]=0

sig_bond[i]=1

return sig_stock,sig_bond

sig_stock,sig_bond=sig_fun()

ret=(ret_stock*sig_stock+ret_bond*sig_bond) .sort_index()

#cum=np.cumprod(1+ret.tail(len(ret)-1))

def ret_port( ret_bond,ret_stock):

ret=ret_bond*sig_bond+ret_stock*sig_stock

ret=ret.sort_index().dropna()

ret_stock=ret_stock.sort_index()

ret_bond =ret_bond.sort_index()

cum_bond=np.cumprod(1+ret_bond)

cum_stock=np.cumprod(1+ret_stock)

cum=np.cumprod(1+ret)

return cum,cum_stock,cum_bond,ret

cum,cum_stock,cum_bond,ret=ret_port( ret_bond,ret_stock)

#画图

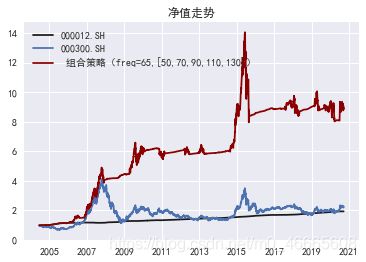

def plot():

plt.plot(cum_bond ,label="000012.SH",color='k',linestyle='-')

plt.plot(cum_stock,label="000300.SH",color='b',linestyle='-')

plt.plot(cum,label=" 组合策略(freq=65,[50,70,90,110,130]) ",color='darkred',linestyle='-')

plt.title("净值走势")

plt.legend(loc="upper left")

#结果描述统计

def performance(port_ret):

port_ret=port_ret.sort_index(ascending=True)

first_date = port_ret.index[0]

final_date = port_ret.index[-1]

time_interval = (final_date - first_date).days * 250 / 365

# calculate portfolio's indicator

nv = (1 + port_ret).cumprod()

arith_mean = port_ret.mean() * 250

geom_mean = (1 + port_ret).prod() ** (250 / time_interval) - 1

sd = port_ret.std() * np.sqrt(250)

mdd = ((nv.cummax() - nv) / nv.cummax()).max()

sharpe = (geom_mean - 0) / sd

calmar = geom_mean / mdd

result = pd.DataFrame({'算术平均收益': [arith_mean], '几何平均收益': [geom_mean], '波动率': [sd],

'最大回撤率': [mdd], '夏普比率': [sharpe], '卡尔曼比率': [calmar]})

print (result)

return plot(),performance(ret)

if __name__=="__main__":

momentum(freq=65,test_start="20041201",test_end="20201001",t1=50,t2=70,t3=90,t4=110,t5=130,n=1)

算术平均收益 几何平均收益 波动率 最大回撤率 夏普比率 卡尔曼比率

0.153452 0.144932 0.168716 0.433393 0.85903 0.334412

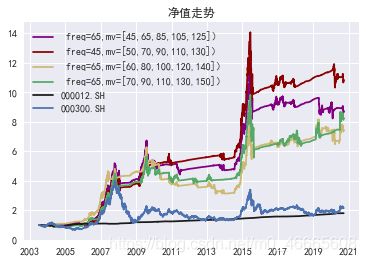

其他结果

其他策略

1.python量化——alpha股票-指数期货对冲策略

2.多因子选股策略

3.海龟交易策略

4.移动平均策略——单/双均线策略

5.改进的美林时钟(介绍)

6.改进的美林时钟策略(一)

7.改进的美林时钟策略(二)

8.改进的美林时钟策略(三)

9.F-F三因子(改进代码+结果)

10.移动波动率策略

11.趋势追踪动量策略

这里获取token码