LSTM机器学习预测沪深300指数涨跌来交易股指期货

1. 从tushare获取沪深300数据

指标计算模块下载

#!/usr/bin/env python

# -*- coding: utf-8 -*-

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import torch

import tushare as ts

import tool.MyTT as zb

import copy

from sklearn.preprocessing import MinMaxScaler

# ###################数据获取

pro = ts.pro_api('自己的key')

df = pro.index_daily(ts_code='000300.SH', start_date='20060101') # end_date='20220711'

df = df.iloc[::-1]

2. 特征工程

说明:用沪深300当日收益率、5日收益率和5日均线乖离作为输入特征,标签用第二天的收益率。将三个输入特征和标签转换为1和-1,如收益率大于零为1代表张,小于零为-1代表跌。

# 特征工程

df['cma_5'] = zb.MA(df.close.values, 5)

df['atr_5'] = (zb.ATR(df.close.values, df.high.values, df.low.values, 5))/df.close*100

df['syl_1'] = ((df['close']-df['close'].shift(1))/df['close'].shift(1)*100) > 0

df['syl_1'] = df['syl_1'] = (df['syl_1'].astype(int)).replace(0, -1) # 将bool变量转换为1 0数值, 并将0替换为-1

df['syl_5'] = ((df['close']-df['close'].shift(5))/df['close'].shift(5)*100) > 0

df['syl_5'] = df['syl_5'] = (df['syl_5'].astype(int)).replace(0, -1)

df['jxqs_5'] = ((df['close'] > df['cma_5']).astype(int)).replace(0, -1)

df = df.fillna(method='bfill') # 向上填充

sel_col = ['syl_1', 'syl_5', 'jxqs_5']

df_main = copy.deepcopy(df[sel_col])

# 数据归一化,这里本来就是用的1和-1也可以不归一化

scaler = MinMaxScaler(feature_range=(-1, 1))

for col in sel_col: # 这里不能进行统一进行缩放,因为fit_transform返回值是numpy类型

df_main[col] = scaler.fit_transform(df_main[col].values.reshape(-1, 1))

# 将下一日的收盘价作为本日的标签

df_main['target'] = df_main['syl_1'].shift(-1)

# df_main = df_main.dropna() # 使用了shift函数,在最后必然是有缺失值的,这里去掉缺失值所在行

df_main['target'].iloc[-1] = df_main['target'].iloc[-2] # 替换最后一个nan为上一个值

df_main = df_main.astype(np.float32) # 修改数据类型

3. 建立LSTM模型

import torch.nn as nn

input_dim = 3 # 数据的特征数

hidden_dim = 32 # 隐藏层的神经元个数

num_layers = 2 # LSTM的层数

output_dim = 1 # 预测值的特征数(这是预测股票价格,所以这里特征数是1,如果预测一个单词,那么这里是one-hot向量的编码长度)

class LSTM(nn.Module):

def __init__(self, input_dim, hidden_dim, num_layers, output_dim):

super(LSTM, self).__init__()

# Hidden dimensions

self.hidden_dim = hidden_dim

# Number of hidden layers

self.num_layers = num_layers

# Building your LSTM

# batch_first=True causes input/output tensors to be of shape (batch_dim, seq_dim, feature_dim)

self.lstm = nn.LSTM(input_dim, hidden_dim, num_layers, batch_first=True)

# Readout layer 在LSTM后再加一个全连接层,因为是回归问题,所以不能在线性层后加激活函数

self.fc = nn.Linear(hidden_dim, output_dim)

def forward(self, x):

# Initialize hidden state with zeros

h0 = torch.zeros(self.num_layers, x.size(0), self.hidden_dim).requires_grad_()

# 这里x.size(0)就是batch_size

# Initialize cell state

c0 = torch.zeros(self.num_layers, x.size(0), self.hidden_dim).requires_grad_()

# One time step

# We need to detach as we are doing truncated backpropagation through time (BPTT)

# If we don't, we'll backprop all the way to the start even after going through another batch

out, (hn, cn) = self.lstm(x, (h0.detach(), c0.detach()))

4. 按照模型接口组织训练数据

# 创建两个列表,用来存储数据的特征和标签

data_feat, data_target = [], []

# 设每条数据序列有10组数据

seq = 10

for index in range(len(df_main) - seq):

# 构建特征集

data_feat.append(df_main[sel_col][index: index + seq].values)

# 构建target集

data_target.append(df_main['target'][index:index + seq])

# 将特征集和标签集整理成numpy数组

data_feat = np.array(data_feat)

data_target = np.array(data_target)

# ############## 训练集与测试集的划分 todo

# 这里按照9:1的比例划分训练集和测试集

test_set_size = int(np.round(1*df_main.shape[0])) # np.round(1)是四舍五入,

train_size = data_feat.shape[0] - (test_set_size)

print(test_set_size) # 输出测试集大小

print(train_size) # 输出训练集大小

trainX = torch.from_numpy(data_feat[800:train_size].reshape(-1, seq, input_dim)).type(torch.Tensor)

# 这里第一个维度自动确定,我们认为其为batch_size,因为在LSTM类的定义中,设置了batch_first=True

testX = torch.from_numpy(data_feat[train_size:].reshape(-1, seq, input_dim)).type(torch.Tensor)

testX2 = torch.from_numpy(data_feat[2000:].reshape(-1, seq, input_dim)).type(torch.Tensor)

trainY = torch.from_numpy(data_target[800:train_size].reshape(-1, seq, 1)).type(torch.Tensor)

testY = torch.from_numpy(data_target[train_size:].reshape(-1, seq, 1)).type(torch.Tensor)

testY2 = torch.from_numpy(data_target[2000:].reshape(-1, seq, 1)).type(torch.Tensor)

print('x_train.shape = ', trainX.shape)

print('y_train.shape = ', trainY.shape)

print('x_test.shape = ', testX.shape)

print('x_test.shape2 = ', testX2.shape)

print('y_test.shape = ', testY.shape)

5. 训练模型

import torch.utils.data

batch_size = train_size # 等于训练集大小

train = torch.utils.data.TensorDataset(trainX, trainY)

test = torch.utils.data.TensorDataset(testX, testY)

train_loader = torch.utils.data.DataLoader(dataset=train,

batch_size=batch_size,

shuffle=False)

test_loader = torch.utils.data.DataLoader(dataset=test,

batch_size=batch_size,

shuffle=False)

# 实例化模型

model = LSTM(input_dim=input_dim, hidden_dim=hidden_dim, output_dim=output_dim, num_layers=num_layers)

# 定义优化器和损失函数

optimiser = torch.optim.Adam(model.parameters(), lr=0.01) # 使用Adam优化算法

loss_fn = torch.nn.MSELoss(size_average=True) # 使用均方差作为损失函数

# 打印模型结构

print(model)

# 打印模型各层的参数尺寸

for i in range(len(list(model.parameters()))):

print(list(model.parameters())[i].size())

# 设定数据遍历次数

num_epochs = 90

# 训练模型

hist = np.zeros(num_epochs)

for t in range(num_epochs):

y_train_pred = model(trainX)

loss = loss_fn(y_train_pred, trainY)

if t % 10 == 0 and t != 0: # 每训练十次,打印一次均方差,

print("训练次数 ", t, "均方差RMSE: ", loss.item())

hist[t] = loss.item()

# Zero out gradient, else they will accumulate between epochs 将梯度归零

optimiser.zero_grad()

# Backward pass

loss.backward()

# Update parameters

optimiser.step()

- 计算训练得到的模型在训练集上的均方差

y_train_pred = model(trainX)

loss_fn(y_train_pred, trainY).item()

6. 做出预测

y_test_pred = model(testX2)

loss_fn(y_test_pred, testY2).item()

pred_value = y_test_pred.detach().numpy()[:, -1, 0]

true_value = testY2.detach().numpy()[:, -1, 0]

data2 = pd.read_csv('公式读写数据库配置文件 - syl.csv')

data2['块名'] = ['hs300ycsyl' for var in range(len(pred_value))]

data2['键名'] = df['trade_date'][-len(pred_value):].values

data2['值'] = pred_value[:, 0] # 有归一化时用

# data2['值'] = pred_value

# data2 = pd.DataFrame(pred_value[:, 0], df['trade_date'][-len(pred_value):].values)

data2.to_csv('hs300ycsyl.csv', index=None, encoding='utf_8_sig')

print('样本外开始日期=', df['trade_date'][-len(testX):].values[0])

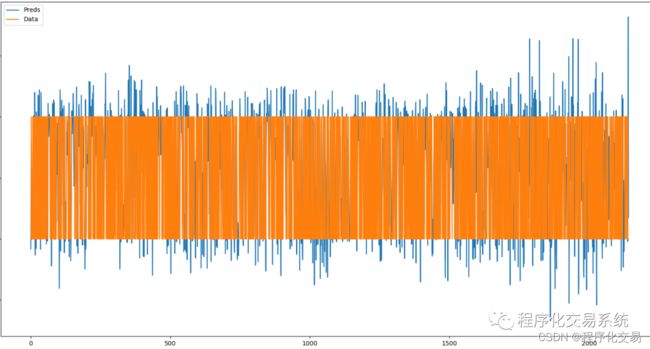

plt.plot(pred_value, label="Preds") # 预测值

plt.plot(true_value, label="Data") # 真实值

plt.legend()

plt.show()

• 看图拟合的可以

7. 将拟合的涨跌结果导出tb交易开拓者能识别的数据格式,然后导入tb本地数据库,读取进行回测

data2 = pd.DataFrame({'块名': [], '键名': [], '值': []})

data2['块名'] = ['hs300ycsyl' for var in range(len(pred_value))]

data2['键名'] = df['trade_date'][-len(pred_value):].values

data2['值'] = pred_value[:, 0] # 有归一化时用

• tb交易开拓者策略编写,预测值大于0时做多,小于0时开空,反手策略。

//------------------------------------------------------------------------

// 简称: lstm_hc

// 名称: 机器学习回测

// 类别: 公式应用

// 类型: 用户应用

// 输出: Void

//------------------------------------------------------------------------

Params

//此处添加参数

Vars

Series<Numeric> yc_close;

Series<Numeric> jiaoyiri;

Defs

//此处添加公式函数

Events

//初始化事件函数,策略运行期间,首先运行且只有一次,应用在订阅数据等操作

OnInit()

{

//与数据源有关

Range[0:DataCount-1]

{

//=========数据源相关设置==============

//AddDataFlag(Enum_Data_RolloverBackWard()); //设置后复权

//AddDataFlag(Enum_Data_RolloverRealPrice()); //设置映射真实价格

AddDataFlag(Enum_Data_AutoSwapPosition()); //设置自动换仓

AddDataFlag(Enum_Data_IgnoreSwapSignalCalc()); //设置忽略换仓信号计算

Bool ret = SetSwapPosVolType(2); //设置自动换仓量类型

//AddDataFlag(Enum_Data_OnlyDay()); //设置仅日盘

//AddDataFlag(Enum_Data_OnlyNight()); //设置仅夜盘

//AddDataFlag(Enum_Data_NotGenReport()); //设置数据源不参与生成报告标志

//=========交易相关设置==============

//MarginRate rate;

//rate.ratioType = Enum_Rate_ByFillAmount; //设置保证金费率方式为成交金额百分比

//rate.longMarginRatio = 0.1; //设置保证金率为10%

//rate.shortMarginRatio = 0.2; //设置保证金率为20%

//SetMarginRate(rate);

CommissionRate tCommissionRate;

tCommissionRate.ratioType = Enum_Rate_ByFillAmount;

tCommissionRate.openRatio = 1; //设置开仓手续费为成交金额的5%%

tCommissionRate.closeRatio = 1; //设置平仓手续费为成交金额的2%%

tCommissionRate.closeTodayRatio = 1; //设置平今手续费为0

SetCommissionRate(tCommissionRate); //设置手续费率

SetSlippage(Enum_Rate_PointPerHand,2); //设置滑点为2跳/手

//=========交易相关设置==============

SetInitCapital(10000000); //设置初始资金为100万

}

//Bar更新事件函数,参数indexs表示变化的数据源图层ID数组

OnBar(ArrayRef<Integer> indexs)

{

jiaoyiri = TrueDate();

if(jiaoyiri<>jiaoyiri[1]) data1.yc_close = Value(GetTBProfileString("hs300ycsyl",text(data1.Date)));

Commentary("预测收益率="+Text(data1.yc_close));

if(MarketPosition != 1 and data1.yc_close != InvalidNumeric and data1.yc_close>0.5)

{

Buy(1, Open);

}

if(MarketPosition != -1 and data1.yc_close != InvalidNumeric and data1.yc_close<-0.5)

{

SellShort(1, Open);

}

}

//------------------------------------------------------------------------

// 编译版本 2023/02/01 084226

// 版权所有 jinxin168

// 更改声明 TradeBlazer Software保留对TradeBlazer平台

// 每一版本的TradeBlazer公式修改和重写的权利

//------------------------------------------------------------------------

8. 信号与回测结果

• 下面是样本内信号,非常好。

• 下面是样本外信号,一般。

• 下面是回测结果。

结论:从回测结果看,有点过拟合,给的三个特征也不是很好,可以加入更多相关性强的特征,注意,类似于价格的特征需要做平稳性检验。