【卡尔曼滤波器-Python】The g-h filter

【卡尔曼滤波器-Python】The g-h filter

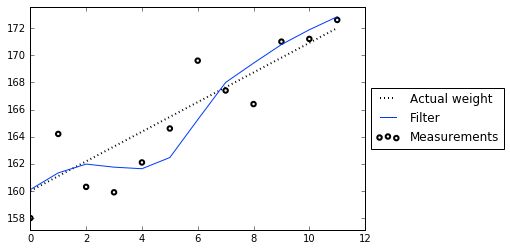

The g-h filter是kalman的基本思想。通过经验值来改进测量值,达到滤波的效果。举个例子,假如有一个人有一天的重量是160斤,并且接下来每天的体重都会增加一斤,但是我们通过体重计测得的数据分别如下所示

[158.0, 164.2, 160.3, 159.9, 162.1, 164.6,169.6, 167.4, 166.4, 171.0, 171.2, 172.6]

滤波的过程如下

- 根据线性增长确定真实值

- 计算残差,真实值与测量值

- 根据残差的大小,在h因子的作用下确定下次增长率

- 根据残差的大小,在g因子的作用下确定估计值,即滤波后的结果

测试代码如下

from gh_internal import plot_g_h_results

import book_plots

import numpy as np

def g_h_filter(data,x0,dx,g,h,dt=1.,pred=None):

x=x0

results=[]

for z in data:

x_est=x+(dx*dt)

dx=dx

if pred is not None:

pred.append(x_est)

residual=z-x_est

dx=dx+h*(residual)/dt

x=x_est+g*residual

results.append(x)

return np.array(results)

weights=np.array([158.0, 164.2, 160.3, 159.9, 162.1, 164.6,

169.6, 167.4, 166.4, 171.0, 171.2, 172.6])

book_plots.plot_track([0, 11], [160, 172], label='Actual weight')

data = g_h_filter(data=weights, x0=160, dx=1, g=3./10, h=1./3, dt=1.)

plot_g_h_results(weights, data);

[1] Kalman_and_Bayesian_FIlters_in_Python

[2] https://github.com/rlabbe/Kalman-and-Bayesian-Filters-in-Python