使用akshare下载bar数据导入vnpy数据库

一,mysql创建vnpy数据库

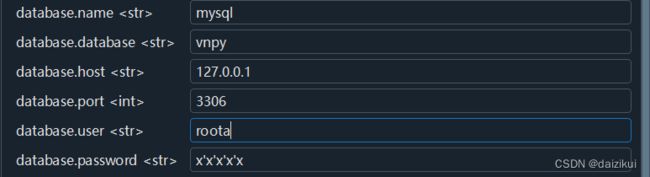

1,使用vnpy配置创建数据库

2,用sql创建数据库

-- vnpy.dbbardata definition

CREATE TABLE `dbbardata` (

`id` int NOT NULL AUTO_INCREMENT,

`symbol` varchar(255) NOT NULL,

`exchange` varchar(255) NOT NULL,

`datetime` datetime NOT NULL,

`interval` varchar(255) NOT NULL,

`volume` double NOT NULL,

`turnover` double NOT NULL,

`open_interest` double NOT NULL,

`open_price` double NOT NULL,

`high_price` double NOT NULL,

`low_price` double NOT NULL,

`close_price` double NOT NULL,

PRIMARY KEY (`id`),

UNIQUE KEY `dbbardata_symbol_exchange_interval_datetime` (`symbol`,`exchange`,`interval`,`datetime`)

) ENGINE=InnoDB DEFAULT CHARSET=utf8mb4 COLLATE=utf8mb4_0900_ai_ci;

-- vnpy.dbbaroverview definition

CREATE TABLE `dbbaroverview` (

`id` int NOT NULL AUTO_INCREMENT,

`symbol` varchar(255) NOT NULL,

`exchange` varchar(255) NOT NULL,

`interval` varchar(255) NOT NULL,

`count` int NOT NULL,

`start` datetime NOT NULL,

`end` datetime NOT NULL,

PRIMARY KEY (`id`),

UNIQUE KEY `dbbaroverview_symbol_exchange_interval` (`symbol`,`exchange`,`interval`)

) ENGINE=InnoDB DEFAULT CHARSET=utf8mb4 COLLATE=utf8mb4_0900_ai_ci;二,代码

objects.py

from dataclasses import field

from datetime import datetime

from enum import Enum

class Exchange(Enum):

"""

Exchange.

"""

# Chinese

CFFEX = "CFFEX" # China Financial Futures Exchange

SHFE = "SHFE" # Shanghai Futures Exchange

CZCE = "CZCE" # Zhengzhou Commodity Exchange

DCE = "DCE" # Dalian Commodity Exchange

INE = "INE" # Shanghai International Energy Exchange

GFEX = "GFEX" # Guangzhou Futures Exchange

SSE = "SSE" # Shanghai Stock Exchange

SZSE = "SZSE" # Shenzhen Stock Exchange

BSE = "BSE" # Beijing Stock Exchange

SHHK = "SHHK" # Shanghai-HK Stock Connect

SZHK = "SZHK" # Shenzhen-HK Stock Connect

SGE = "SGE" # Shanghai Gold Exchange

WXE = "WXE" # Wuxi Steel Exchange

CFETS = "CFETS" # CFETS Bond Market Maker Trading System

XBOND = "XBOND" # CFETS X-Bond Anonymous Trading System

class Interval(Enum):

"""

Interval of bar data.

"""

MINUTE = "1m"

HOUR = "1h"

DAILY = "d"

WEEKLY = "w"

TICK = "tick"

class BarData():

"""

Candlestick bar data of a certain trading period.

"""

symbol: str

exchange: Exchange

datetime: datetime

interval: Interval = None

volume: float = 0

turnover: float = 0

open_interest: float = 0

open_price: float = 0

high_price: float = 0

low_price: float = 0

close_price: float = 0

def __str__(self):

return f"{self.symbol} {self.exchange} {self.datetime} {self.interval} {self.volume} \

{self.turnover} {self.open_interest} {self.open_price} {self.high_price} {self.low_price} {self.close_price}"

def __post_init__(self) -> None:

""""""

self.vt_symbol: str = f"{self.symbol}.{self.exchange.value}"mysql_database.py

from peewee import *

from datetime import *

# 连接 MySQL 数据库

db = MySQLDatabase('vnpy', user='root', password='xxxxxx', host='localhost', port=3306)

class DbBarData(Model):

"""K线数据表映射对象"""

id: AutoField = AutoField()

symbol: str = CharField()

exchange: str = CharField()

datetime: datetime = DateTimeField()

interval: str = CharField()

volume: float = FloatField()

turnover: float = FloatField()

open_interest: float = FloatField()

open_price: float = FloatField()

high_price: float = FloatField()

low_price: float = FloatField()

close_price: float = FloatField()

class Meta:

database = db

indexes: tuple = ((("symbol", "exchange", "interval", "datetime"), True),)

class DbBarOverview(Model):

"""K线汇总数据表映射对象"""

id: AutoField = AutoField()

symbol: str = CharField()

exchange: str = CharField()

interval: str = CharField()

count: int = IntegerField()

start: datetime = DateTimeField()

end: datetime = DateTimeField()

class Meta:

database = db

indexes: tuple = ((("symbol", "exchange", "interval"), True),)

main.py

import re

from datetime import datetime, time

from typing import List

import akshare as ak

from mysql_database import db

import pandas as pd

from akshare import futures_zh_daily_sina, futures_zh_minute_sina

from peewee import chunked, ModelSelect

from db.objects import BarData, Exchange, Interval

from db.mysql_database import DbBarData, DbBarOverview

def save_bar_data(bars: List[BarData], stream: bool = False) -> bool:

"""保存K线数据"""

# 读取主键参数

bar: BarData = bars[0]

symbol: str = bar.symbol

exchange: Exchange = bar.exchange

interval: Interval = bar.interval

# 将BarData数据转换为字典,并调整时区

data: list = []

for bar in bars:

# bar.datetime = convert_tz(bar.datetime)

d: dict = bar.__dict__

d["exchange"] = d["exchange"].value

d["interval"] = d["interval"].value

# d.pop("gateway_name")

# d.pop("vt_symbol")

data.append(d)

# 使用upsert操作将数据更新到数据库中

with db.atomic():

for c in chunked(data, 50):

DbBarData.insert_many(c).on_conflict_replace().execute()

# 更新K线汇总数据

overview: DbBarOverview = DbBarOverview.get_or_none(

DbBarOverview.symbol == symbol,

DbBarOverview.exchange == exchange.value,

DbBarOverview.interval == interval.value,

)

index_end = len(bars) - 1

if not overview:

overview: DbBarOverview = DbBarOverview()

overview.symbol = symbol

overview.exchange = exchange.value

overview.interval = interval.value

overview.start = bars[0].datetime

overview.end = bars[index_end].datetime

overview.count = len(bars)

elif stream:

overview.end = bars[index_end].datetime

overview.count += len(bars)

else:

overview.start = min(bars[0].datetime, overview.start)

overview.end = max(bars[index_end].datetime, overview.end)

s: ModelSelect = DbBarData.select().where(

(DbBarData.symbol == symbol)

& (DbBarData.exchange == exchange.value)

& (DbBarData.interval == interval.value)

)

overview.count = s.count()

overview.save()

return True

def convert_to_bardata(row):

"""Convert a row of Pandas DataFrame to BarData object."""

bar = BarData()

bar.symbol = row['symbol']

bar.exchange = Exchange(row['exchange'])

bar.datetime = datetime.strptime(row['datetime'], '%Y-%m-%d %H:%M:%S')

bar.interval = row['interval']

bar.volume = row['volume'] # 成交量

bar.turnover = None # 成交额

bar.open_interest = row['hold'] # 持仓量

bar.open_price = row['open']

bar.high_price = row['high']

bar.low_price = row['low']

bar.close_price = row['close']

return bar

interval_dict = {

'1': Interval.MINUTE,

'60': Interval.HOUR

}

# 交易所上市品种简称

d = {

Exchange.DCE: ('A', 'C', 'Y', 'FB', 'L', 'J', 'PG', 'PP', 'RR', 'EG', 'M', 'CS', 'B', 'EB', 'I', 'JD', 'P', 'V', 'JM', 'LH'),

Exchange.CZCE: ('CJ', 'PF', 'SA', 'TA', 'SR', 'CF', 'FG', 'UR', 'AP', 'PK', 'OI', 'RM', 'SF', 'CY', 'RS', 'MA', 'SM'),

Exchange.SHFE: ('WR', 'BU', 'HC', 'AU', 'NI', 'SN', 'RU', 'CU', 'AL', 'ZN', 'PB', 'SP', 'AG', 'RB', 'SS', 'FU'),

Exchange.INE: ('LU', 'BC', 'SC', 'NR')

}

def get_exchange(symbol:str):

p = re.match(r'^[A-Za-z]+', symbol).group().upper()

for exchange in d.keys():

for s in d.get(exchange):

# 打印每个值

if p == s:

return exchange.value

def get_data(symbol: str, interval: str):

df = pd.DataFrame()

if interval in ['1', '60']:

df = futures_zh_minute_sina(symbol, interval)

df['interval'] = interval_dict.get(interval)

elif interval == Interval.DAILY.value:

df = futures_zh_daily_sina(symbol)

df['interval'] = Interval.DAILY

df['datetime'] = df['date'] + ' 00:00:00'

df['symbol'] = symbol.upper()

df['exchange'] = get_exchange(symbol)

return df

if __name__ == '__main__':

symbol = 'cu2409'

interval = 'd' # 可以是 '1' ,'60' ,'d' 代表1分钟,1小时,1天

df = get_data(symbol, interval)

list = []

list = df.apply(convert_to_bardata, axis=1)

save_bar_data(list)

print(list)

运行结果

三,查看数据

dbbardata 表  dbbarovervice表

dbbarovervice表