- REGULATORY FRAMEWORKS AROUND THE GLOBE

在全球范围内的监管框架

Regulations intended to increase financial innovation and competition kicked off the momentum towards Open Banking.

用于增加金融创新和竞争的法规推动了开放银行的发展势头。

(注:之前有kick start 这里又有 kick off呼应。Regulations intended to …competition 省略定语从句的that,Regulations that intended to … 为kicked off的主语)

Following the UK and Europe’s lead, other countries and regions have caught on, though with different oversight approaches ranging from issuing high-level guiding principles, to mandating banks to open access to their accounts, to building nationwide infrastructure.

跟随着欧洲和英国的带领下,其他国家和地区也跟上脚步,尽管采用不同的监督方法,从发布高级指导原则,到要求银行开放账户、建立全国性的基础设施。

Consortia, which include commercial, regulatory, and non- governmental policy participants, are taking up the baton where government directives leave off. While most attention has been paid to technical API definitions, there is a growing realization that governance issues such as data ownership, privacy, and responsibility in case of data breach will require a combination of compliance and consensual best practices.

包括商业,监管和非政府政策参与者在内的联盟正在政府指令断片的地方接过指挥棒。虽然最受关注的是技术API的定义,但人们越来越意识到,数据所有权、隐私、以及数据泄露的责任等治理问题将需要在服从与协商中组合出最佳实践。

The first, soft deadlines for support of Open Banking regulations occurred in the past year. Hard deadlines for full implementation are pending in 2019, even as regulations continue to evolve.

首先,鼓励开放银行活动的监管条例建议期限已在去年到期。尽管监管条例仍在不断演变,但全面执行的最后期限将在2019年截止。

(注:Soft deadlines 与 Hard deadlines,前者是指建议日期,后者是强制日期,在完成一项任务时,建议日期是一种建议,在建议日期之后强制日期之前完成也是可以的,但强制日期是必须完成的截止日。support作为名词,意思有鼓励、建议。)

Regulatory development in different countries

不同国家的监管发展

United Kingdom

英国

The UK is the de facto leader in Open Banking driven by activist regulators providing detailed specificationsand access requirements.

英国活跃的监管机构提供详细的规范和访问要求,使其成为开放银行活动事实上的领导者。

(注:de facto 拉丁语:事实上的)

The Open Banking Implementation Entity (OBIE) is responsible for creating relevant standards, under the governance of the Competition and Markets Authority (CMA) and in collaboration with banks, building societies, financial technology companies, third-party providers, and consumer groups.

开放银行实施实体(OBIE)负责在竞争和市场管理局(CMA)的治理下,与银行、购房互助协会、金融技术公司,第三方提供商和消费者团体合作,制定相关标准。

The standards cover the core components of technical specifications, security, customer experience, and conformance & certification.

这些标准涵盖了技术规范的核心组件、安全性、客户体验以及一致性和认证。

Europe

欧洲

The second Payment Services Directive (PSD2) requires banks to open up their data to third-parties, causing a revolution in the payments domain.

支付服务指令第二版(PSD2)要求银行向第三方开放数据,从而引发支付领域的革命。

EU member states were expected to incorporate this directive into their national laws by 2018.

预计欧盟成员国将在2018年之前将该指令纳入其国家法律。

(注:过去将来时,虽然用的是过去一般时,但expect是预计将来发生的事情,所以是在过去预计将来的事情)

However, there exists uncertainty surrounding many aspects of PSD2, such as API implementation and technical dissimilarities.

然而,PSD2的许多方面存在不确定性,例如API实现和技术差异。

The European Banking Authority’s Regulatory Technical Standards (RTS) only specify technical framework conditions related to payments (cards and e-wallets).

欧洲银行管理局的监管技术标准(RTS)仅规定了与支付(卡和电子钱包)相关的技术框架条件。

Its next specification on the critical issues of strong customer authentication and secure standards of communication is to be released on 14 September, 2019.

其关于强客户认证和安全通信标准等关键问题的下一个规范将于2019年9月14日发布。

This, coupled with the absence of a pan-European implementation entity, has caused a significant gap affecting PSD2.

除此之外,加上泛欧实施实体的缺失,已经成了影响PSD2的显著问题。

The Swiss Open Finance API (SOFA), driven by the Swiss Fintech Innovation Association (SFTI), aims to implement standardized APIs for their Open Banking sector.

由瑞士金融科技创新协会(SFTI)推动的瑞士开放金融API(SOFA)旨在为其开放银行领域实施标准化API。

The common standard will have huge implications and benefit the overall financial industry including customers.

通用标准将产生巨大影响,并使包括客户在内的整个金融行业受益。

United States of America

美国

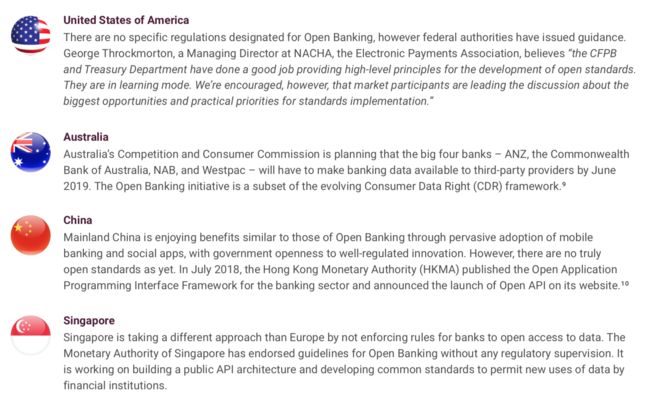

There are no specific regulations designated for Open Banking, however federal authorities have issued guidance.

没有为开放银行指定具体规定,但联邦当局已发布指导。

George Throckmorton, a Managing Director at NACHA, the Electronic Payments Association, believes “the CFPB and Treasury Department have done a good job providing high-level principles for the development of open standards.

电子支付协会、NACHA的常务董事George Throckmorton认为,“CFPB和财政部已经在为开放标准的制定提供高水平原则方面做的非常完美。

(NACHA:National Automated Clearing House Association 国家自动清算所协会

CFPB:Consumer Financial Protection Bureau 消费者金融保护局)

They are in learning mode. We’re encouraged, however, that market participants are leading the discussion about the biggest opportunities and practical priorities for standards implementation.”

并处于不断学习中。然而,我们感到鼓舞的是,市场参与者正引领讨论标准实施的最大机遇和实践优先项。

Australia

澳大利亚

Australia’s Competition and Consumer Commission is planning that the big four banks – ANZ, the Commonwealth Bank of Australia, NAB, and Westpac – will have to make banking data available to third-party providers by June 2019.

澳大利亚竞争和消费者委员会计划,四大银行:澳新银行、澳大利亚联邦银行、NAB和西太平洋银行、将必须在2019年6月之前向第三方提供商提供银行数据。

The Open Banking initiative is a subset of the evolving Consumer Data Right (CDR) framework.

开放银行倡议是不断进化的消费者数据权利(CDR)框架的一个子集。

China

中国

Mainland China is enjoying benefits similar to those of Open Banking through pervasive adoption of mobile banking and social apps, with government openness to well-regulated innovation.

中国大陆基于手机银行的普遍采用和社交应用,享受与开放式银行类似的好处,政府对规范创新持开放态度。

(注:well-regulated 这个词很魔幻,参看这句话 A well regulated militia being necessary to the security of a free state, the right of the people to keep and bear arms shall not be infringed. 可以自行google这句话的出处)

However, there are no truly open standards as yet.

但是,目前还没有真正的开放标准。

(注:官方指导标准即将到来……)

In July 2018, the Hong Kong Monetary Authority (HKMA) published the Open Application Programming Interface Framework for the banking sector and announced the launch of Open API on its website.

2018年7月,香港金融管理局(HKMA)发布了银行业开放应用程序编程接口框架,并宣布在其网站上推出Open API。

Singapore

新加坡

Singapore is taking a different approach than Europe by not enforcing rules for banks to open access to data.

新加坡采取了与欧洲不同的做法,没有强制要求让银行开放数据访问。

The Monetary Authority of Singapore has endorsed guidelines for Open Banking without any regulatory supervision.

新加坡金融管理局在没有任何监管监督的情况下批准了开放银行业务指引。

It is working on building a public API architecture and developing common standards to permit new uses of data by financial institutions.

致力于构建公共API架构并制定通用标准,以允许金融机构对数据进行新的使用。

Regulatory differences hinder but don’t halt progress

监管差异导致阻碍但却阻碍不了进程

There is a tension between the global nature of financial services and local approaches to Open Banking regulation.

对于开放银行的监管来说,在全球性金融服务与地方法律之间存在着矛盾。

Since consumer payments have common characteristics, why not strive for globally-standard APIs?

由于消费者支付具有共同特征,为什么不力求全球标准API?

Long-time industry executives expressed skepticism to LendIt that this will occur.

资深业界高管们对朗迪表示出“这将会发生”的怀疑。

Different locations possess different philosophies about the roles of government and free - market forces in driving innovation.

关于政府和自由市场势力在推动创新中的角色,不同地区拥有不同的理念。

With a related standard, ISO-20022 for financial transactions, the industry has arrived at variations by region while still implementing it worldwide.

业界已经按区域实现了通过ISO-20022相关标准进行金融交易的改变,同时也在全球范围内实施推广。

Similar variances in Open Banking could give advantage to the largest banks that can invest across regions, bias fintechs to focus on just one market initially, and encourage enterprise technologists to offer cross-API integration hubs.

开放式银行中类似差异可以为最大的银行提供优势,这些银行可以跨地区投资、在最初影响金融科技只关注一个市场,并鼓励企业技术人员提供跨API集成平台。

Imagine if the banking sector was as open to universal standards as the telecom industry, where typing a dozen digits on a phone places a call anywhere in the world.

想象一下,如果银行业像电信业一样开放世界标准,像在电话上输入几个数字就能打到世界上任何地方。