基于python行为评分卡模型

什么是行为评分卡

- 基本定义:根据贷款人放贷后的表现,来预测其未来一段时间内发生逾期或违约风险概率的模型

- 使用场景:在放贷之后、到期之前,即贷中环节

- 使用目的:贷款人在贷款结束之前的逾期/违约风险

下面是案例

对本文有些概念不懂得可以看 信用评分卡模型的建立

数据+代码下载

关于数据

- Loan_Amount:总的额度

- OS:未还金融

- Payment:还款金融

- Spend:使用金额

- Delq:逾期情况

第一步,特征处理

由于数据时已经过初步清洗工作,本次特征工程主要做了变量的衍生工作。

比观察期12个月的数据做了(1,3,6,12)个月的切片,定义以下特征:

- 逾期类型特征

逾期类型的特征在行为评分卡(预测违约行为中),一般是非常显著的变量。

这里取:最大逾期,M0逾期次数,M1逾期次数和M2逾期次数。

定义逾期变量函数,并生成特征。

-

def DelqFeatures(event, window, type): -

''' -

event:事件 -

window:时间窗口,本次模型统一[1,3,6,12], -

type:特征类型(最大逾期,M0逾期次数,M1逾期次数M2,逾期次数) -

''' -

current = 12 -

start = 12 - window + 1 -

delq1 = [event[a] for a in ['Delq1_' + str(t) for t in range(current, start-1, -1)]] -

delq2 = [event[a] for a in ['Delq2_' + str(t) for t in range(current, start-1, -1)]] -

delq3 = [event[a] for a in ['Delq3_' + str(t) for t in range(current, start-1, -1)]] -

if type == 'max delq': -

if max(delq3) == 1: -

return 3 -

elif max(delq2) == 1: -

return 2 -

elif max(delq1) == 1: -

return 1 -

else: -

return 0 -

if type in ['M0 times', 'M1 times', 'M2 times']: -

if type.find('M0')>-1: -

return sum(delq1) -

elif type.find('M1')>-1: -

return sum(delq2) -

else: -

return sum(delq3) -

for t in [1,3,6,12]: -

# (1)过去t时间窗口内的最大逾期状态 -

allFeature.append('maxDelqL'+str(t)+'M') -

trainData['maxDelqL' + str(t) + 'M'] = trainData.apply(lambda x: DelqFeatures(x, t, 'max delq'), axis=1) -

#(2)过去t时间窗口内的,M0,M1,M2的次数 -

allFeature.append('M0FreqL'+str(t)+'M') -

trainData['M0FreqL' + str(t)+ 'M'] = trainData.apply(lambda x: DelqFeatures(x, t,'M0 times'),1) -

allFeature.append('M1FreqL' + str(t) + 'M') -

trainData['M1FreqL' + str(t) + 'M'] = trainData.apply(lambda x: DelqFeatures(x, t, 'M1 times'), 1) -

allFeature.append('M2FreqL' + str(t) + 'M') -

trainData['M2FreqL' + str(t) + 'M'] = trainData.apply(lambda x: DelqFeatures(x, t, 'M2 times'), 1)

- 额度使用类型在行为评分卡模型中,通常是与违约高度相关的。

这里取:平均使用率、最大使用率、使用率增加的月份

定义额度使用函数,并生成特征

-

def UrateFeatures(event, window, type): # 额度使用率特征,平均使用率、最大使用率、使用率增加的月份 -

current = 12 -

start = 12 - window + 1 -

monthlySpend = [event[a] for a in ['Spend_' + str(t) for t in range(current, start-1, -1)]] -

limit = event['Loan_Amount'] -

monthlyUrate = [x / limit for x in monthlySpend] -

if type == 'mean utilization rate': -

return np.mean(monthlyUrate) -

if type == 'max utilization rate': -

return max(monthlyUrate) -

if type == 'increase utilization rate': -

currentUrate = monthlyUrate[0:-1] -

previousUrate = monthlyUrate[1:] -

compareUrate = [int(x[0]>x[1]) for x in zip(currentUrate, previousUrate)] -

return sum(compareUrate) -

''' -

额度使用率类型特征在行为评分卡模型中,通常是与违约率高度相关的 -

''' -

for t in [1,3,6,12]: -

# (1)过去t时间窗口内的最大月额度使用率 -

allFeature.append('maxUrateL' + str(t) + 'M') -

trainData['maxUrateL' + str(t) + 'M'] = trainData.apply(lambda x: UrateFeatures(x, t, 'max utilization rate'), 1) -

# (2)过去t时间窗口内的平均月额度使用率 -

allFeature.append('avgUrateL' + str(t) + 'M') -

trainData['avgUrateL' + str(t) + 'M'] = trainData.apply(lambda x: UrateFeatures(x, t, 'mean utilization rate'), 1) -

# (3)过去t时间窗口内,月额度使用率增加的月份,t>1 -

if t > 1: -

allFeature.append('increaseUrateL' + str(t) + 'M') -

trainData['increaseUrateL' + str(t) + 'M'] = trainData.apply(lambda x: UrateFeatures(x, t, 'increase utilization rate'),1)

- 还款类型特征也是行为评分卡模型中常用的特征

这里取(最小还款率、最大还款率、平均还款率)

定义还款类型并生成特征

-

def PaymentFeature(event, window, type): # 还款情况特征(最小还款率、最大还款率、平均还款率) -

current = 12 -

start = 12 - window + 1 -

currentPayment = [event[a] for a in ['Payment_' + str(t) for t in range(current, start-1, -1)]] -

previousOS = [event[a] for a in ['OS_' + str(t) for t in range(current-1, start-2, -1)]] -

monthlyPatRatio = [] -

for Pay_OS in zip(currentPayment, previousOS): -

if Pay_OS[1] > 0: -

payRatio = Pay_OS[0]*1.0 / Pay_OS[1] -

monthlyPatRatio.append(payRatio) -

else: -

monthlyPatRatio.append(1) -

if type == 'min payment ratio': -

return min(monthlyPatRatio) -

if type == 'max payment ratio': -

return max(monthlyPatRatio) -

if type == 'mean payment ratio': -

totoal_payment = sum(currentPayment) -

total_OS = sum(previousOS) -

if total_OS > 0: -

return totoal_payment / total_OS -

else: -

return 1 -

''' -

还款类型特征也是评分卡模型中常用的特征 -

''' -

for t in [1,3,6,12]: -

allFeature.append('maxPayL' + str(t) + 'M') -

trainData['maxPayL' + str(t) + 'M'] = trainData.apply(lambda x: PaymentFeature(x,t,'max payment ratio'),1) -

allFeature.append('minPayL' + str(t) + 'M') -

trainData['minPayL' + str(t) + 'M'] = trainData.apply(lambda x: PaymentFeature(x, t, 'min payment ratio'), 1) -

allFeature.append('avgPayL' + str(t) + 'M') -

trainData['avgPayL' + str(t) + 'M'] = trainData.apply(lambda x: PaymentFeature(x, t, 'mean payment ratio'), 1)

衍生特征的都在这里了:

['maxDelqL1M', 'M0FreqL1M', 'M1FreqL1M', 'M2FreqL1M', 'maxDelqL3M', 'M0FreqL3M', 'M1FreqL3M', 'M2FreqL3M', 'maxDelqL6M', 'M0FreqL6M', 'M1FreqL6M', 'M2FreqL6M', 'maxDelqL12M', 'M0FreqL12M', 'M1FreqL12M', 'M2FreqL12M', 'maxUrateL1M', 'avgUrateL1M', 'maxUrateL3M', 'avgUrateL3M', 'increaseUrateL3M', 'maxUrateL6M', 'avgUrateL6M', 'increaseUrateL6M', 'maxUrateL12M', 'avgUrateL12M', 'increaseUrateL12M', 'maxPayL1M', 'minPayL1M', 'avgPayL1M', 'maxPayL3M', 'minPayL3M', 'avgPayL3M', 'maxPayL6M', 'minPayL6M', 'avgPayL6M', 'maxPayL12M', 'minPayL12M', 'avgPayL12M']

第二步进行分箱和WOE编码

分箱和WOE编码都是有监督的处理方式,要求每一箱的同时存在好、坏样本,一般分箱数量不超过5

scorecard_function是自定义的函数,详情见源码

类别型变量:过去t时间内最大的逾期状态

需要检查与坏样本的相关度

-

print(trainData.groupby(['maxDelqL1M'])['label'].mean()) -

print(trainData.groupby(['maxDelqL3M'])['label'].mean()) -

print(trainData.groupby(['maxDelqL6M'])['label'].mean()) -

print(trainData.groupby(['maxDelqL12M'])['label'].mean())

所有的结果都是单调递增或递减的,检查通过。

maxDelqL1M 0 0.102087 1 0.109065 2 0.514403 3 0.956710 Name: label, dtype: float64 maxDelqL3M 0 0.047477 1 0.050318 2 0.434509 3 0.958009 Name: label, dtype: float64 maxDelqL6M 0 0.047886 1 0.050380 2 0.265044 3 0.549407 Name: label, dtype: float64 maxDelqL12M 0 0.070175 1 0.044748 2 0.182365 3 0.380687 Name: label, dtype: float64

-

################################### -

# 2, 分箱,计算WOE并编码 -

################################### -

''' -

对类别型变量的分箱和WOE计算 -

可以通过计算取值个数的方式判断是否是类别变量 -

''' -

categoricalFeatures = [] -

numericalFeatures = [] -

WOE_IV_dict = {} -

for var in allFeature: -

if len(set(trainData[var])) > 5: -

numericalFeatures.append(var) -

else: -

categoricalFeatures.append(var) -

not_monotone = [] -

for var in categoricalFeatures: -

#检查bad rate在箱中的单调性 -

if not scorecard_function.BadRateMonotone(trainData, var, 'label'): -

not_monotone.append(var) -

print(not_monotone.append(var))

不单调的变量有:['M1FreqL3M', 'M2FreqL3M', 'maxDelqL12M'],下面对它们进行处理

trainData.groupby(['M2FreqL3M'])['label'].count() M2FreqL3M 0 27456 1 585 2 55 3 3 Name: label, dtype: int64

将 M2FreqL3M>=1的合并为一组,检查M1FreqL3M单调性

-

# 将 M2FreqL3M>=1的合并为一组,计算WOE和IV -

trainData['M2FreqL3M_Bin'] = trainData['M2FreqL3M'].apply(lambda x: int(x>=1)) -

trainData.groupby(['M2FreqL3M_Bin'])['label'].mean() -

WOE_IV_dict['M2FreqL3M_Bin'] = scorecard_function.CalcWOE(trainData, 'M2FreqL3M_Bin', 'label') -

trainData.groupby(['M1FreqL3M'])['label'].mean() #检查单调性

M1FreqL3M 0 0.049511 1 0.409583 2 0.930825 3 0.927083 Name: label, dtype: float64 M1FreqL3M 0 22379 1 4800 2 824 3 96 Name: label, dtype: int64

除了M1FreqL3M=3外, 其他组别的bad rate单调。 # 此外,M1FreqL3M=0 占比很大,因此将M1FreqL3M>=1的分为一组

对其他单调的类别型变量,检查是否有一箱的占比低于5%。 如果有,将该变量进行合并

-

small_bin_var = [] -

large_bin_var = [] -

N = trainData.shape[0] -

for var in categoricalFeatures: -

if var not in not_monotone: -

total = trainData.groupby([var])[var].count() -

pcnt = total * 1.0 / N -

if min(pcnt)<0.05: -

small_bin_var.append({var:pcnt.to_dict()}) -

else: -

large_bin_var.append(var) -

for i in small_bin_var: -

print (i) -

''' -

{'maxDelqL1M': {0: 0.60379372931421049, 1: 0.31880138083205806, 2: 0.069183956724438597, 3: 0.0082209331292928574}} -

{'M2FreqL1M': {0: 0.99177906687070716, 1: 0.0082209331292928574}} -

{'maxDelqL3M': {0: 0.22637816292394747, 1: 0.57005587387451506, 2: 0.18068258656891703, 3: 0.022883376632620377}} -

{'maxDelqL6M': {0: 0.057226235809103528, 1: 0.58489625965336844, 2: 0.31285810882949572, 3: 0.045019395708032317}} -

{'M2FreqL6M': {0: 0.95498060429196774, 1: 0.04003701199330937, 2: 0.0045909107085661408, 3: 0.00032029609594647497, 4: 7.1176910210327775e-05}} -

{'M2FreqL12M': {0: 0.92334246770347694, 1: 0.066514822591551295, 2: 0.0092174098722374465, 3: 0.00081853446741876937, 4: 0.00010676536531549166}} -

''' -

#对于M2FreqL1M、M2FreqL6M和M2FreqL12M,由于有部分箱占了很大比例,故删除 -

allFeatures.remove('M2FreqL1M') -

allFeatures.remove('M2FreqL6M') -

allFeatures.remove('M2FreqL12M') -

#对于small_bin_var中的其他变量,将最小的箱和相邻的箱进行合并并计算WOE -

trainData['maxDelqL1M_Bin'] = trainData['maxDelqL1M'].apply(lambda x: scorecard_function.MergeByCondition(x, ['==0', '==1', '>=2'])) -

trainData['maxDelqL3M_Bin'] = trainData['maxDelqL3M'].apply(lambda x: scorecard_function.MergeByCondition(x, ['==0', '==1', '>=2'])) -

trainData['maxDelqL6M_Bin'] = trainData['maxDelqL6M'].apply(lambda x: scorecard_function.MergeByCondition(x, ['==0', '==1', '>=2'])) -

for var in ['maxDelqL1M_Bin','maxDelqL3M_Bin','maxDelqL6M_Bin']: -

WOE_IV_dict[var] = scorecard_function.CalcWOE(trainData, var, 'label') -

''' -

对于不需要合并、原始箱的bad rate单调的特征,直接计算WOE和IV -

''' -

for var in large_bin_var: -

WOE_IV_dict[var] = scorecard_function.CalcWOE(trainData, var, 'label') -

''' -

对于数值型变量,需要先分箱,再计算WOE、IV -

分箱的结果需要满足: -

1,箱数不超过5 -

2,bad rate单调 -

3,每箱占比不低于5% -

''' -

bin_dict = [] -

for var in numericalFeatures: -

binNum = 5 -

newBin = var + '_Bin' -

bin = scorecard_function.ChiMerge(trainData, var, 'label', max_interval=binNum, minBinPcnt = 0.05) -

trainData[newBin] = trainData[var].apply(lambda x: scorecard_function.AssignBin(x, bin)) -

# 如果不满足单调性,就降低分箱个数 -

while not scorecard_function.BadRateMonotone(trainData, newBin, 'label'): -

binNum -= 1 -

bin = scorecard_function.ChiMerge(trainData, var, 'label', max_interval=binNum, minBinPcnt=0.05) -

trainData[newBin] = trainData[var].apply(lambda x: scorecard_function.AssignBin(x, bin)) -

WOE_IV_dict[newBin] = scorecard_function.CalcWOE(trainData, newBin, 'label') -

bin_dict.append({var:bin})

第三步,单变量和多变量分析

逻辑回归对样本特征的线性相关比较敏感,因此在建立模型之前要对变量进行剔除。

单变量分析,本次样本特征不多,IV选择放宽到>0.02

多变量分析,计算每个样本特征共线性,相关系数>0.7,剔除IV较低的一个。

-

############################## -

# 3, 单变量分析和多变量分析 # -

############################## -

# 选取IV高于0.02的变量 -

high_IV = [(k,v['IV']) for k,v in WOE_IV_dict.items() if v['IV'] >= 0.02] -

high_IV_sorted = sorted(high_IV, key=lambda k: k[1],reverse=True) -

for (var,iv) in high_IV: -

newVar = var+"_WOE" -

trainData[newVar] = trainData[var].map(lambda x: WOE_IV_dict[var]['WOE'][x]) -

''' -

比较两两线性相关性。如果相关系数的绝对值高于阈值,剔除IV较低的一个 -

''' -

deleted_index = [] -

cnt_vars = len(high_IV_sorted) -

for i in range(cnt_vars): -

if i in deleted_index: -

continue -

x1 = high_IV_sorted[i][0]+"_WOE" -

for j in range(cnt_vars): -

if i == j or j in deleted_index: -

continue -

y1 = high_IV_sorted[j][0]+"_WOE" -

roh = np.corrcoef(trainData[x1],trainData[y1])[0,1] -

if abs(roh)>0.7: -

x1_IV = high_IV_sorted[i][1] -

y1_IV = high_IV_sorted[j][1] -

if x1_IV > y1_IV: -

deleted_index.append(j) -

else: -

deleted_index.append(i) -

single_analysis_vars = [high_IV_sorted[i][0]+"_WOE" for i in range(cnt_vars) if i not in deleted_index] -

X = trainData[single_analysis_vars] -

f, ax = plt.subplots(figsize=(10, 8)) -

corr = X.corr() -

sns.heatmap(corr, mask=np.zeros_like(corr, dtype=np.bool), cmap=sns.diverging_palette(220, 10, as_cmap=True),square=True, ax=ax)

剩余变量的相关系数热力图

多变量分析,计算VIF。最大的VIF是 3.429,小于10,因此这一步认为没有多重共线性

-

''' -

多变量分析:VIF -

''' -

X = np.matrix(trainData[single_analysis_vars]) -

VIF_list = [variance_inflation_factor(X, i) for i in range(X.shape[1])] -

print (max(VIF_list)) -

# 最大的VIF是 3.429,小于10,因此这一步认为没有多重共线性 -

multi_analysis = single_analysis_vars

第四步,建立逻辑回归模型预测违约

-

################################ -

# 4, 建立逻辑回归模型预测违约 # -

################################ -

X = trainData[multi_analysis] -

X['intercept'] = [1] * X.shape[0] -

y = trainData['label'] -

logit = sm.Logit(y, X) -

logit_result = logit.fit() -

pvalues = logit_result.pvalues -

params = logit_result.params -

fit_result = pd.concat([params,pvalues],axis=1) -

fit_result.columns = ['coef','p-value'] -

fit_result = fit_result.sort_values(by = 'coef') -

print(fit_result)

以下变量系数为正,需要单独和label做逻辑回归验证 increaseUrateL3M_WOE minPayL6M_Bin_WOE avgUrateL12M_Bin_WOE minPayL1M_Bin_WOE M0FreqL6M_Bin_WOE minPayL3M_Bin_WOE

-

sm.Logit(y, trainData['increaseUrateL3M_WOE']).fit().params # -0.995312 -

sm.Logit(y, trainData['minPayL6M_Bin_WOE']).fit().params # -0.807779 -

sm.Logit(y, trainData['avgUrateL12M_Bin_WOE']).fit().params # -1.0179 -

sm.Logit(y, trainData['minPayL1M_Bin_WOE']).fit().params # -0.969236 -

sm.Logit(y, trainData['M0FreqL6M_Bin_WOE']).fit().params # -1.032842 -

sm.Logit(y, trainData['minPayL3M_Bin_WOE']).fit().params # -0.829298

单独建立回归模型,系数为负,与预期相符,说明仍然存在多重共线性 下一步,用GBDT跑出变量重要性,挑选出合适的变量

-

clf = ensemble.GradientBoostingClassifier() -

gbdt_model = clf.fit(X, y) -

importace = gbdt_model.feature_importances_.tolist() -

featureImportance = zip(multi_analysis,importace) -

featureImportanceSorted = sorted(featureImportance, key=lambda k: k[1],reverse=True) -

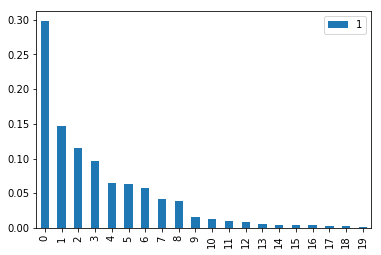

pd.DataFrame(featureImportanceSorted).plot(kind='bar')

上图中可以看出前4个变量重要度较高,先用前四个变量生成模型,再按重要程度每次加一个变量,剔除结果参数为负或p值超过0.1的变量

-

# 先假定模型可以容纳4个特征,再逐步增加特征个数,直到有特征的系数为正,或者p值超过0.1 -

n = 4 -

featureSelected = [i[0] for i in featureImportanceSorted[:n]] -

X_train = X[featureSelected+['intercept']] -

logit = sm.Logit(y, X_train) -

logit_result = logit.fit() -

pvalues = logit_result.pvalues -

params = logit_result.params -

fit_result = pd.concat([params,pvalues],axis=1) -

fit_result.columns = ['coef','p-value'] -

''' -

coef p-value -

maxDelqL3M_Bin_WOE -0.895654 0.000000e+00 -

increaseUrateL6M_Bin_WOE -1.084713 1.623441e-84 -

M0FreqL3M_WOE -0.436273 1.556517e-74 -

avgUrateL1M_Bin_WOE -0.629355 7.146665e-16 -

avgUrateL3M_Bin_WOE -0.570670 8.207241e-12 -

intercept -1.831752 0.000000e+00 -

''' -

while(n -

nextVar = featureImportanceSorted[n][0] -

featureSelected = featureSelected + [nextVar] -

X_train = X[featureSelected+['intercept']] -

logit = sm.Logit(y, X_train) -

logit_result = logit.fit() -

params = logit_result.params -

print ("current var is ",nextVar,' ', params[nextVar]) -

if max(params) < 0: -

n += 1 -

else: -

featureSelected.remove(nextVar) -

n += 1 -

X_train = X[featureSelected+['intercept']] -

logit = sm.Logit(y, X_train) -

logit_result = logit.fit() -

pvalues = logit_result.pvalues -

params = logit_result.params -

fit_result = pd.concat([params,pvalues],axis=1) -

fit_result.columns = ['coef','p-value'] -

fit_result = fit_result.sort_values(by = 'p-value')

p值大于0.1d的单独检验显著性

-

largePValueVars = pvalues[pvalues>0.1].index -

for var in largePValueVars: -

X_temp = X[[var, 'intercept']] -

logit = sm.Logit(y, X_temp) -

logit_result = logit.fit() -

pvalues = logit_result.pvalues -

print ("The p-value of {0} is {1} ".format(var, str(pvalues[var])))

显然,单个变量的p值是显著地。说明任然存在着共线性。 可用L1约束,直到所有变量显著

-

X2 = X[featureSelected+['intercept']] -

for alpha in range(100,0,-1): -

l1_logit = sm.Logit.fit_regularized(sm.Logit(y, X2), start_params=None, method='l1', alpha=alpha) -

pvalues = l1_logit.pvalues -

params = l1_logit.params -

if max(pvalues)>=0.1 or max(params)>0: -

break -

bestAlpha = alpha + 1 -

l1_logit = sm.Logit.fit_regularized(sm.Logit(y, X2), start_params=None, method='l1', alpha=bestAlpha) -

params = l1_logit.params -

params2 = params.to_dict() -

featuresInModel = [k for k, v in params2.items() if k!='intercept' and v < -0.0000001] -

print(featuresInModel) -

X_train = X[featuresInModel + ['intercept']] -

logit = sm.Logit(y, X_train) -

logit_result = logit.fit() -

trainData['pred'] = logit_result.predict(X_train) -

ks = scorecard_function.KS(trainData, 'pred', 'label') -

auc = roc_auc_score(trainData['label'],trainData['pred'])

第五步,在测试集上测试模型

-

################################## -

# 5,在测试集上测试逻辑回归的结果 # -

################################### -

# 准备WOE编码后的变量 -

modelFeatures = [i.replace('_Bin','').replace('_WOE','') for i in featuresInModel] -

numFeatures = [i for i in modelFeatures if i in numericalFeatures] -

charFeatures = [i for i in modelFeatures if i in categoricalFeatures] -

testData['maxDelqL1M'] = testData.apply(lambda x: DelqFeatures(x,1,'max delq'),axis=1) -

testData['maxDelqL3M'] = testData.apply(lambda x: DelqFeatures(x,3,'max delq'),axis=1) -

testData['M0FreqL3M'] = testData.apply(lambda x: DelqFeatures(x,3,'M0 times'),axis=1) -

testData['M1FreqL6M'] = testData.apply(lambda x: DelqFeatures(x, 6, 'M1 times'), axis=1) -

testData['M2FreqL3M'] = testData.apply(lambda x: DelqFeatures(x, 3, 'M2 times'), axis=1) -

testData['avgUrateL1M'] = testData.apply(lambda x: UrateFeatures(x,1, 'mean utilization rate'),axis=1) -

testData['avgUrateL3M'] = testData.apply(lambda x: UrateFeatures(x,3, 'mean utilization rate'),axis=1) -

testData['increaseUrateL6M'] = testData.apply(lambda x: UrateFeatures(x, 6, 'increase utilization rate'),axis=1) -

testData['M2FreqL3M_Bin'] = testData['M2FreqL3M'].apply(lambda x: int(x>=1)) -

testData['maxDelqL1M_Bin'] = testData['maxDelqL1M'].apply(lambda x: scorecard_function.MergeByCondition(x, ['==0', '==1', '>=2'])) -

testData['maxDelqL3M_Bin'] = testData['maxDelqL3M'].apply(lambda x: scorecard_function.MergeByCondition(x, ['==0', '==1', '>=2'])) -

for var in numFeatures: -

newBin = var+"_Bin" -

bin = list([i.values() for i in bin_dict if var in i][0])[0] -

testData[newBin] = testData[var].apply(lambda x: scorecard_function.AssignBin(x, bin)) -

finalFeatures = [i+'_Bin' for i in numFeatures] + ['M2FreqL3M_Bin','maxDelqL1M_Bin','maxDelqL3M_Bin','M0FreqL3M'] -

for var in finalFeatures: -

var2 = var+"_WOE" -

testData[var2] = testData[var].apply(lambda x: WOE_IV_dict[var]['WOE'][x]) -

X_test = testData[featuresInModel] -

X_test['intercept'] = [1]*X_test.shape[0] -

testData['pred'] = logit_result.predict(X_test) -

ks = scorecard_function.KS(testData, 'pred', 'label') -

auc = roc_auc_score(testData['label'],testData['pred']) -

print(ks, auc)

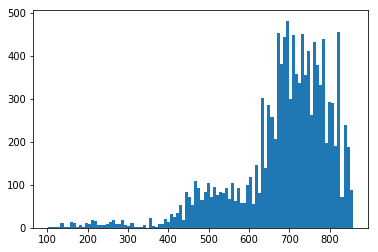

第六步,计算测试集的评分卡得分

-

########################## -

# 6,在测试集上计算分数 # -

########################## -

BasePoint, PDO = 500,50 -

testData['score'] = testData['pred'].apply(lambda x: scorecard_function.Prob2Score(x, BasePoint, PDO)) -

plt.hist(testData['score'],bins=100) -

plt.show()

测试集用户的得分分布