评分卡模型python实现

评分卡模型python实现

文章目录

- 评分卡模型python实现

- 一、 实现步骤

- 二、数据预处理

- 1. 加载数据以及去极值

- 2.缺失值处理

- 3.数据分箱

- 3.1 WOE(Weight of Evidence)

- 3.2 IV (information value)

- 4.woe替换

- 5.数据拆分

- 6.数据标准化和SMOTE调整平衡性

- 三、逻辑回归模型

- 1. 训练模型

- 2. 计算权重

- 四、模型验证

- 1.测试集验证

- 2. ROC曲线

- 五.信用评分

- 1.基础分

- 2.各部分评分

- 3.自动评分

首先来介绍几个名词

- 变量分析:确定变量之间是否存在共线性,如存在高度相关,只保存最稳定、预测能力最高的那个。常用方法为VIF(variance inflation factor),即方差膨胀因子进行检验。

- 变量分箱(binning):是对连续变量离散化的称呼。常用的有等距分段、等深分段、最优分段。

- 单因子分析:检测各变量的强度,常用方法为:WOE、IV。

一、 实现步骤

1.对所有数据进行去极值以及缺失值处理;

2.数据拆分,将数据拆分成训练集、测试集;

3.对数据进行WOE离散化处理;

4.检验离散后的数据是否相关,从而决定是否进行降维处理;

5.调整训练集的平衡性;

6.训练模型,并使用测试集调整模型参数;

7.将通过验证后模型的权重提取出来,计算测试样本中每个客户的违约率;

8.用验证机验证模型的有效性及稳定性;

9.通过违约率给客户打分。

二、数据预处理

1. 加载数据以及去极值

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

# 1.载入数据

def load_data():

data = pd.read_csv('/~~~/data.csv', sep=',')

print(data.describe())

return data

df_data = load_data()

# 2.多变量分析,相关性分析

import seaborn as sns

def corr(data):

corr = data.corr()

xticks = list(corr.index)

yticks = list(corr.index)

fig = plt.figure(figsize=(15, 10))

ax1 = fig.add_subplot(1, 1, 1)

sns.heatmap(corr, annot=True, cmap='rainbow', ax=ax1, linewidths=0.5,

annot_kws={'size': 9, 'weight':'bold', 'color':'blue'})

ax1.set_xticklabels(xticks, rotation=35, fontsize=15)

ax1.set_yticklabels(yticks, rotation=0, fontsize=15)

plt.show()

data = df_data.drop(['label'], axis =1)

corr(data)#一般剔除相关系数高于0.6的变量

# 3.去极值

'''

xy=(横坐标,纵坐标) 箭头尖端

xytext=(横坐标,纵坐标) 文字的坐标,指的是最左边的坐标

arrowprops= {

facecolor= '颜色',

shrink = '数字' <1 收缩箭头

}

'''

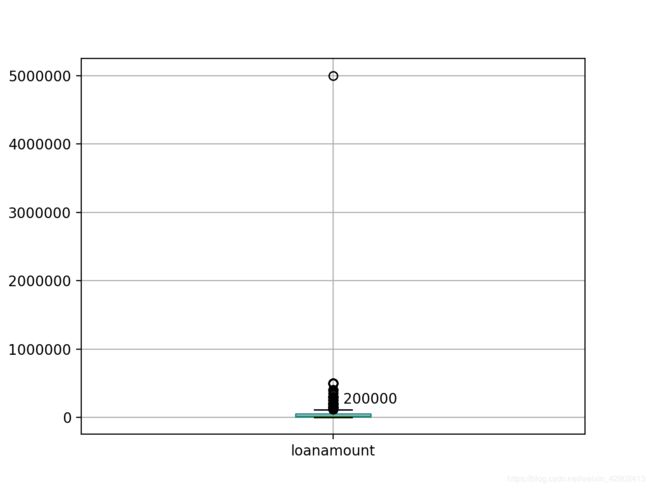

def outlier_check(data, cname):

p = data[[cname]].boxplot(return_type='dict')

print(p)

x_outliers = p['fliers'][0].get_xdata()

y_outliers = p['fliers'][0].get_ydata()

for j in range(1):

plt.annotate(y_outliers[j], xy=(x_outliers[j], y_outliers[j]),

xytext=(x_outliers[j] + 0.02, y_outliers[j]))

plt.show()

#变量loanamount

outlier_check(df_data, 'loanamount')

删除1000000以上的:

df_data = df_data[df_data['loanamount']<1000000]

2.缺失值处理

查看有无缺失值

def check_na(data):

print(data.isnull().sum())

check_na(df_data)

#out:

risk 0

cycletime 0

loanamount 0

loanpurpose 0

seniority 0

monthlyincome 0

incometype 0

删除极值后,数据集无缺失值。

缺失值的具体处理方法可参考: https://blog.csdn.net/weixin_42902413/article/details/87856623

3.数据分箱

在Excel中计算各分箱的IV值,取IV最大的数据分箱。

3.1 WOE(Weight of Evidence)

对分箱后的每组数据求woe。公式如下:

W i = l n ( p ( y i ) p ( n i ) ) W_i = ln(\frac{p(y_i)}{p(n_i)}) Wi=ln(p(ni)p(yi))

其中, p ( y i ) p(y_i) p(yi)表示当前条件下风险用户占总风险用户的比例, p ( n i ) p(n_i) p(ni)表示当前条件小无风险用户占无风险用户的比例。

对上述公式变换后得到:

W i = l n ( p ( y i ) p ( n i ) ) = l n ( y i / y t n i / n t ) = l n ( y i / n i y t / n t ) W_i = ln(\frac{p(y_i)}{p(n_i)}) = ln(\frac{y_i/y_t}{n_i/n_t})=ln(\frac{y_i/ni}{y_t/n_t}) Wi=ln(p(ni)p(yi))=ln(ni/ntyi/yt)=ln(yt/ntyi/ni)

WOE表示当前分组里风险用户和无风险用户的比值,和所有样本中风险用户和无风险用户的比值的差异。WOE越大,说明这种差异越大,这个分组里样本有风险的可能性就越大。

3.2 IV (information value)

衡量某一个变量的信息量。

计算公式为:

I V i = ( p ( y i ) − p ( n i ) ) ∗ W i , I V = ∑ i = 1 n ( I V i ) IV_i = (p(y_i)-p(n_i))*W_i, IV = \sum_{i=1}^{n}(IV_i) IVi=(p(yi)−p(ni))∗Wi,IV=i=1∑n(IVi)

IV值对应的预测能力

| IV | 预测能力 |

|---|---|

| <0.03 | 无预测能力 |

| 0.03~0.09 | 低 |

| 0.1~0.29 | 中 |

| 0.3~0.49 | 高 |

| >=0.5 | 极高 |

如果IV等于负或者正无穷时,都是没有意义的。针对某些风险比例为0或者100%的分组,建议做如下处理:

- 如果有可能,直接把这个分组作为一个规则,作为模型的前置条件或补充条件;

- 重新对变量进行离散化或分组,使每个组的风险比例不为0%且不为100%。(尤其当某个分组样本过少时,要采用这种方法)

- 如果上述两种方法都无用时,建议人工把该分组的风险数据和无风险数量进行一定的调整。(即0调成1,或1调成0)

根据IV值来调整分箱结构并重新计算WOE和IV,知道IV达到最大值,此时的分箱效果最好。

# 数据分箱

# 1)自动分箱

def mono_bin(Y, X, n):

r = 0

badNum = Y.sum()

goodNum = Y.count() - Y.sum()

while abs(r) < 1:

d1 = pd.DataFrame({'X': X, 'Y': Y, 'Bucket': pd.qcut(X, n)})

d2 = d1.groupby('Bucket', as_index=True)

# print('d1的类型是:', type(d1), 'd2的类型是:', type(d2))

r, p = stats.spearmanr(d2.mean().X, d2.mean().Y)

n = n-1

d3 = pd.DataFrame()

d3['min'] = d2.min().X

d3['max'] = d2.max().X

d3['badcostum'] = d2.sum().Y #坏样本的个数

# print("badNum is :", badNum, "d3['badcostum'] is:", d3['badcostum'])

d3['goodcostum'] = d2.count().Y - d2.sum().Y #好样本的个数

d3['total'] = d2.count().Y

d3['bad_rate'] = d2.sum().Y/d2.count().Y

d3['woe'] = np.log(d3['badcostum']/d3['goodcostum']*(goodNum/badNum))

iv = ((d3['badcostum']/badNum - d3['goodcostum']/goodNum)*d3['woe']).sum()

d3['iv'] = iv

woe = list(d3['woe'].round(6))

cut = list(d3['max'].round(6))

cut.insert(0, float('-inf'))

cut[-1] = float('inf')

return d3, iv, cut, woe

# # 2)手动分箱(离散变量)

def hand_bin(Y, X, cut):

badNum = Y.sum()

goodNum = Y.count() - Y.sum()

d1 = pd.DataFrame({'X': X, 'Y': Y, 'Bucket':pd.cut(X, cut)})

d2 = d1.groupby('Bucket', as_index=True)

d3 = pd.DataFrame()

d3['min'] = d2.min().X

d3['max'] = d2.max().X

d3['badcostum'] = d2.sum().Y

d3['goodcostum'] = d2.count().Y - d2.sum().Y

d3['total'] = d2.count().Y

d3['bad_rate'] = d2.sum().Y/d2.count().Y

# print('d3["bad_rate"] is:', d3['bad_rate'])

d3['woe'] = np.log(d3['badcostum']/d3['goodcostum']*(goodNum/badNum))

iv = ((d3['badcostum']/badNum - d3['goodcostum']/goodNum) * d3['woe']).sum()

d3['iv'] = iv

woe = list(d3['woe'].round(6))

return d3, iv, cut, woe

#对于不能自动分箱的特征,进行手动分箱,自定义cut

ninf = float('-inf')

pinf = float('inf')

cut1 = [ninf, 100, 200, 300, 500, pinf]

cut4 = [ninf, 100, 500, pinf]

cut5 = [ninf, 112, 182, pinf]

cut7 = [ninf, 1, 3, pinf]

cut8 = [ninf, 398, 1000, 5000, pinf]

cut9 = [ninf, 0, 60, 200, pinf]

cut11 = [ninf, 0, 1]

#数据分箱

dfx1, ivx1, cutx1, woex1 = hand_bin(df_data['survival'], df_data['certify_time'], cut1)

dfx2, ivx2, cutx2, woex2 = mono_bin(df_data['survival'], df_data['collect'], n=10)

dfx3, ivx3, cutx3, woex3 = mono_bin(df_data['survival'], df_data['collect_amount'], n=10)

dfx4, ivx4, cutx4, woex4 = hand_bin(df_data['survival'], df_data['collect_coupon_amount'], cut4)

dfx5, ivx5, cutx5, woex5 = hand_bin(df_data['survival'], df_data['least_collect'], cut5)

dfx6, ivx6, cutx6, woex6 = mono_bin(df_data['survival'], df_data['scan'], n=10)

dfx7, ivx7, cutx7, woex7 = hand_bin(df_data['survival'], df_data['pay'], cut7)

dfx8, ivx8, cutx8, woex8 = hand_bin(df_data['survival'], df_data['pay_amount'], cut8)

dfx9, ivx9, cutx9, woex9 = hand_bin(df_data['survival'], df_data['pay_coupon_amount'], cut9)

dfx10, ivx10, cutx10, woex10 = mono_bin(df_data['survival'], df_data['age'], n=10)

dfx11, ivx11, cutx11, woex11 = hand_bin(df_data['survival'], df_data['sex'], cut11)

# print('dfx1', dfx1, ivx1, cutx1, woex1)

4.woe替换

# woe替换

def replace_woe(X, cut, woe):

x_woe = pd.cut(X, cut, labels=woe)

return x_woe

df_data['certify_time'] = Series(replace_woe(df_data['certify_time'], cutx1, woex1))

df_data['collect'] = Series(replace_woe(df_data['collect'], cutx2, woex2))

df_data['collect_amount'] = Series(replace_woe(df_data['collect_amount'], cutx3, woex3))

df_data['collect_coupon_amount'] = Series(replace_woe(df_data['collect_coupon_amount'], cutx4, woex4))

df_data['least_collect'] = Series(replace_woe(df_data['least_collect'], cutx5, woex5))

df_data['scan'] = Series(replace_woe(df_data['scan'], cutx6, woex6))

df_data['pay'] = Series(replace_woe(df_data['pay'], cutx7, woex7))

df_data['pay_amount'] = Series(replace_woe(df_data['pay_amount'], cutx8, woex8))

df_data['pay_coupon_amount'] = Series(replace_woe(df_data['pay_coupon_amount'], cutx9, woex9))

df_data['age'] = Series(replace_woe(df_data['age'], cutx10, woex10))

df_data['sex'] = Series(replace_woe(df_data['sex'], cutx11, woex11))

iv = [ivx1, ivx2, ivx3, ivx4, ivx5, ivx6, ivx7, ivx8, ivx9, ivx10, ivx11]

# print('iv is :', iv)

#去除IV值较小的两列

df_data = df_data.drop(['age', 'sex'], axis=1)

cut = [cutx1, cutx2, cutx3, cutx4, cutx5, cutx6, cutx7, cutx8, cutx9]

woe = [woex1, woex2, woex3, woex4, woex5, woex6, woex7, woex8, woex9]

5.数据拆分

拆分成训练集和测试集

# 拆分数据,测试集、训练集

from random import sample

def data_sample(inputX, index, test_Ratio=0.2):

data_array = np.atleast_1d(inputX) #将给定的所有数组,output的arrays中的所有array的维数均大于等于1

class_array = np.unique(data_array)

test_list = []

train_list = []

for c in class_array:

temp = []

for i, value in enumerate(data_array):

if value == c:

temp.append(index[i])

test_list.extend(sample(temp, int(len(temp)*test_Ratio)))

return list(set(index) - set(test_list)), test_list

def split_sample(data):

train_list, test_list = data_sample(data['risk'].tolist(), data.index.tolist())

df_train_section = data.ix[train_list, :]

df_test_section = data.ix[test_list, :]

return df_train_section, df_test_section

df_train, df_test = split_sample(df_data)

print(len(df_train), len(df_test)) # 8000 1999

6.数据标准化和SMOTE调整平衡性

(1)数据标准化之前先将属性和标签拆分开,再对属性进行标准化:

# 1.df_train,训练集

Y_train = df_train['risk'].values.tolist()

X_train = df_train.drop(['risk'], axis=1)

std_series = X_train.std()

mean_series = X_train.mean()

X_train = X_train.add(mean_series).div(std_series)

# 2.df_test,测试集

Y_test = df_test['risk'].values.tolist()

X_test = df_test.drop(['risk'], axis=1)

std_series = X_test.std()

mean_series = X_test.mean()

X_test = X_test.add(mean_series).div(std_series)

(2)由于风险用户占比较少,数据存在不平衡性。而逻辑回归模型倾向于自动删除高风险的用户,因此采用SMOTE法过采样违约用户,使得训练样本尽量平衡。

from collections import Counter

print(Counter(Y_train)) # 计算训练集中0和1的比例

from imblearn.over_sampling import SMOTE

smo = SMOTE(ratio={1: 4000}, random_state=42, n_jobs=1)

X_train, Y_train = smo.fit_sample(X_train, Y_train)

print(Counter(Y_train))

三、逻辑回归模型

1. 训练模型

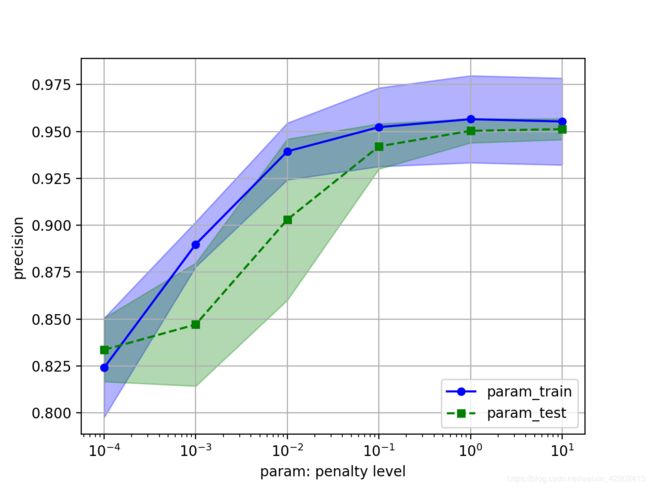

首先,为了确保数据进模型之前已经标准化,由于前面步骤已经标准化过了,接下来直接引入逻辑回归模型,并使用L2正则化防止过拟合。

其中正则化强度C由验证曲线validation_curve来确定,具体代码如下:

from sklearn.model_selection import validation_curve

from sklearn.linear_model import LogisticRegression

param_range = [0.001, 0.01, 0.1, 1, 10]

# 使用逻辑回归的验证器,验证的参数是C,3折交叉验证

train_scores, test_scores = validation_curve(estimator=LogisticRegression(dual=True),

X=X_train, y=Y_train, param_name='C', param_range=param_range, cv=3)

train_mean = np.mean(train_scores, axis=1)

train_std = np.std(train_scores, axis=1)

test_mean = np.mean(test_scores, axis=1)

test_std = np.std(test_scores, axis=1)

plt.plot(param_range, train_mean, color='b', marker='o', markersize=5, label='param_train')

plt.fill_between(param_range, train_mean+train_std, train_mean-train_std, alpha=0.3, color='b')

plt.plot(param_range, test_mean, ls='--', color='g', marker='s', markersize=5, label='param_test')

plt.fill_between(param_range, test_mean+test_std, test_mean-test_std, alpha=0.3, color='g')

plt.grid()

plt.xscale('log')

plt.xlabel('param: penalty level')

plt.ylabel('precision')

plt.legend(loc='lower right')

plt.show()

验证曲线如下:(取C=0.1)

2. 计算权重

# 得出权重

from sklearn.linear_model import LogisticRegression

LR = LogisticRegression(dual=True, C=1)

LR.fit(X_train, Y_train)

weight = LR.coef_[0]

intercept = LR.intercept_[0]

coe = list(weight)

coe.append(intercept)

四、模型验证

1.测试集验证

测试集精度:

from sklearn import metrics

y_pred = LR.predict(X_test)

print(metrics.confusion_matrix(Y_test, y_pred))#输出混淆矩阵

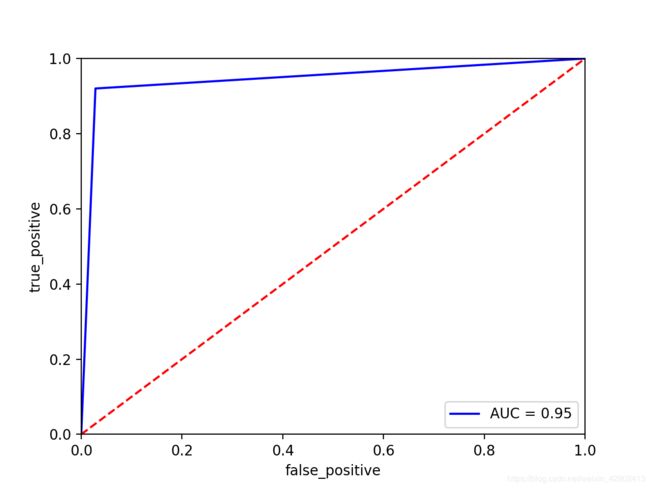

2. ROC曲线

from sklearn import metrics

fpr, tpr, threshold = metrics.roc_curve(Y_test, y_pred)

rocauc = metrics.auc(fpr, tpr)

plt.plot(fpr, tpr, 'b', label='AUC = %0.2f' % rocauc)

plt.legend(loc='lower right')

plt.plot([0, 1], [0, 1], 'r--')

plt.xlim([0, 1])

plt.ylim([0, 1])

plt.ylabel('true_positive')

plt.xlabel('false_positive')

plt.show()

ROC曲线如下:

五.信用评分

个人总评分 = 基础分+各部分得分

1.基础分

基础分值定为600分,PDO(比率翻倍的分值)好坏比定为20.

import math

p = 20/math.log(2)

q = 600 - 20 * math.log(20)/math.log(1)

baseScore = round(q + p * coe[0], 0)

2.各部分评分

def get_score(coe, woe, factor):

# print('coe, woe, factor are:', coe, woe, factor)

scores = []

for w in woe:

score = round(coe * w * factor, 0)

scores.append(score)

return scores

x1 = get_score(coe[0], woe[0], p)

x2 = get_score(coe[1], woe[1], p)

x3 = get_score(coe[2], woe[2], p)

x4 = get_score(coe[3], woe[3], p)

x5 = get_score(coe[4], woe[4], p)

x6 = get_score(coe[5], woe[5], p)

x7 = get_score(coe[6], woe[6], p)

x8 = get_score(coe[7], woe[7], p)

x9 = get_score(coe[8], woe[8], p)

score = [x1, x2, x3, x4, x5, x6, x7, x8, x9]

3.自动评分

因为是先分箱再进行数据切分的,对测试集也进行了woe值替换,所以要用woe值进行对比;如果先进行数据切分,不对测试集进行woe值替换,则用cut值进行比较

1)定义函数

#定义评分计算函数

def compute_score(series, woe, score):

list = []

# print('series.iloc[1]={}'.format(series.iloc[1]))

print('woe={}'.format(woe))

print('score={}'.format(score))

for i in range(len(series)):

value = series.iloc[i]

print('value={}'.format(value))

s = []

for j in range(len(woe)):

if value == woe[j]:

print('woe={}'.format(woe))

s = score[j]

print('s = {}'.format(s))

# ss.append(s)

list.append(s)

# print('list={}'.format(list))

# list = pd.Series(list)

# print('list={}'.format(list))

return list

2)计算各测试集的分值

# 计算

df_test['x1'] = compute_score(df_test['certify_time'], woe[0], x1)

#print(df_test['x1'])

#print(pd.DataFrame({"certify_time": df_test['certify_time'], 'x1': df_test['x1']}))

df_test['x2'] = compute_score(df_test['collect'], woe[1], x2)

df_test['x3'] = compute_score(df_test['collect_amount'], woe[2], x3)

df_test['x4'] = compute_score(df_test['collect_coupon_amount'], woe[3], x4)

df_test['x5'] = compute_score(df_test['least_collect'], woe[4], x5)

df_test['x6'] = compute_score(df_test['scan'], woe[5], x6)

df_test['x7'] = compute_score(df_test['pay'], woe[6], x7)

df_test['x8'] = compute_score(df_test['pay_amount'], woe[7], x8)

df_test['x9'] = compute_score(df_test['pay_coupon_amount'], woe[8], x9)

df_test['score'] = baseScore + df_test['x1'] + df_test['x2'] + df_test['x3'] + df_test['x4'] + df_test['x5'] + df_test['x6'] + df_test['x7'] + df_test['x8'] + df_test['x9']

# print(df_test['x1'].head())

print(df_test['score'].head())

输出结果:

id score

2797 432.0

4480 430.0

7864 401.0

8418 393.0

9077 401.0

至此,第一次评分卡流程走完了,当然还有很多可以优化的地方。后面也许会更新另一个实际项目,加油!