数据挖掘 沪深股市预测

导入基本模块库

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from statsmodels.tsa.arima_model import ARMA

import warnings

from itertools import product

from datetime import datetime

warnings.filterwarnings('ignore')

加载数据

# 数据加载

df = pd.read_csv('./shanghai_1990-12-19_to_2019-2-28.csv')

将时间作为df的索引

df.Timestamp = pd.to_datetime(df.Timestamp)

df.index = df.Timestamp

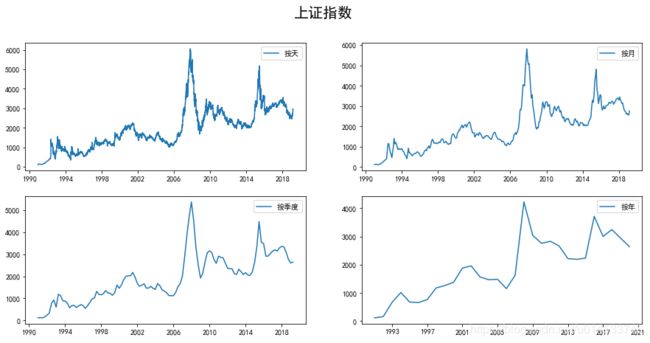

效果如图

数据探索

print(df.head())

按照月,季度,年来统计

df_month = df.resample('M').mean()

df_Q = df.resample('Q-DEC').mean()

df_year = df.resample('A-DEC').mean()

按照天,月,季度,年来显示比特币的走势

fig = plt.figure(figsize=[15, 7])

plt.rcParams['font.sans-serif']=['SimHei'] #用来正常显示中文标签

plt.suptitle('上证指数', fontsize=20)

plt.subplot(221)

plt.plot(df.Price, '-', label='按天')

plt.legend()

plt.subplot(222)

plt.plot(df_month.Price, '-', label='按月')

plt.legend()

plt.subplot(223)

plt.plot(df_Q.Price, '-', label='按季度')

plt.legend()

plt.subplot(224)

plt.plot(df_year.Price, '-', label='按年')

plt.legend()

plt.show()

ARMA模型训练

- 设置参数范围

ps = range(0, 3)

qs = range(0, 3)

parameters = product(ps, qs)

parameters_list = list(parameters)

- 寻找最优ARMA模型参数,即best_aic最小

results = []

best_aic = float("inf") # 正无穷

for param in parameters_list:

try:

model = ARMA(df_month.Price,order=(param[0], param[1])).fit()

except ValueError:

print('参数错误:', param)

continue

aic = model.aic

if aic < best_aic:

best_model = model

best_aic = aic

best_param = param

results.append([param, model.aic])

- 输出最优模型

result_table = pd.DataFrame(results)

result_table.columns = ['parameters', 'aic']

print('最优模型: ', best_model.summary())

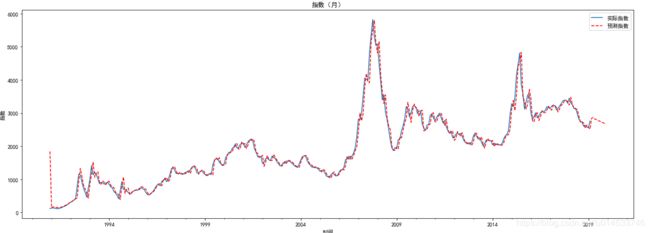

指数预测

我们预测今年一年的上证指数走势,使用pd.date_range生成月字段,freq='MS’代表每月开始的日期。

df_month2 = df_month[['Price']]

date_list=pd.date_range('2019-3-31','2019-12-31', freq='M').tolist()

future = pd.DataFrame(index=date_list, columns= df_month.columns)

df_month2 = pd.concat([df_month2, future])

df_month2['forecast'] = best_model.predict(start=0, end=350)

预测结果显示

plt.figure(figsize=(20,7))

df_month2.Price.plot(label='实际指数')

df_month2.forecast.plot(color='r', ls='--', label='预测指数')

plt.legend()

plt.title('指数(月)')

plt.xlabel('时间')

plt.ylabel('指数)

plt.show()

预测结果图片显示

预测结果数值显示