2019加密市场金融借贷领域研究报告(英文版) | TokenInsight

数字资产行业在2018下半年开始经历“寒冬”后终于在2019年一季度出现回暖态势。主流加密通证在一季度增幅超过20%,交易活跃度与市场参与人数环比显著提升。

在市场结束一段时间低迷的同时,借贷项目为数字资产持有者提供了在不折价出售数字资产的情况下提高资金流动性的方式。

自2018年Q4以来,借贷市场中入场资金和活跃贷款量持续上升,而这个趋势持续到了2019年Q1,目前仅基于Ethereum的去中心化借贷平台的活跃贷款量已超过2千万USD,较2018年底上升超过30%。

广义来讲的数字资产借贷业务包括所有以数字资产为质押物或贷款的市场活动,借贷双方分别是流动性提供者和需求者。借方资金筹措方式包括平台自筹、平台建立资金池和P2P网络。

值得注意的是,在本文中,TokenInsight仅选取以数字资产借贷为主营业务的项目作为研究对象,考察了30余个数字货币借贷项目在2019年一季度的主要发展情况。相应的,将借贷产品作为平台附加服务的项目(如交易所、钱包或理财平台)将在TokenInsight数字资产理财行业研究中进行讨论。

在本文的研究范畴中,数字资产借贷项目经营模式包括中心化与去中心化借贷,其中产品的类型包括质押法币(或稳定币)贷数字资产、质押数字资产贷法币(或稳定币)以及质押加密通证贷加密通证三种。所有产品均采用超额抵押模式,2019年Q1的数字货币质押率(按照Collateral to Loan方式计算)基本在300%以上。

总体而言,这个行业仍处于幼稚期,借贷规模相比于数字资产在二级市场的交易量体量极小,且产品与服务仍有较大的提升空间。只要有借贷市场就会催生出的同业拆借业务也才刚起步,可查信息极少。但不可否认的是,这些设计精巧的产品为加密市场提供了更多丰富度,也为行业发展开拓了更多可能性。借贷项目的技术创新和项目通过合作实现的新业态非常值得期待。

公众号后台回复“借贷”,即可获得【2019加密市场借贷领域研究报告】中文版和英文版PDF。

TokenInsight 其他领域报告如下,敬请请点击阅读:

区块链与分布式隐私计算行业报告

比特币月报-2019.06

全球加密通证量化基金行业研究报告

2019 Q1交易所行业报告

Preface

Since the second half of 2018, the digital assets industry weathered a severe depressional state. Finally, in Q1 of 2019, the market began to see signs of improvement. The number of mainstream cryptocurrencies rose by more than 20% in Q1 alone. Moreover, exchange activities and market participation increased dramatically. The establishment of lending projects provided crypto asset holders with methods to improve financial liquidity without having to sell their crypto assets at a discount. This was especially useful during a time when the market announced the end of a bleak period. Since Q4 of 2018, the admission of funds and active loan volumes in the lending market were constantly increasing and did not subside until Q1 of 2019. At current, the active volume on decentralized loan platforms merely based on Ethereum has already exceeded 20 million USD, a rise of over 30% from the end of 2018. Crypto asset lending is gradually becoming a preferable choice for users to improve their asset security and reduce their risk.

In a broad sense, crypto asset lending services include all market activities involving crypto assets as collateral for loans. The debit and credit are respectively regarded as the provider and demander of liquidity. For debits, the methods for fundraising consist of self-funding platforms, platform-established capital pools, and P2P networks. It should be noticed that, in this report, TokenInsight only selected projects which emphasized crypto asset lending as their main objective, and mainly investigating their developments during 2019 Q1. Correspondingly, projects (such as exchanges, wallets, and financial management platforms) that take collateralized products as extra services will, otherwise, be discussed in TokenInsight’s research on crypto asset financial management.

In this study, the operation models of crypto asset lending include centralized and the decentralized finance, and the product types which include pledging legal tender (or stablecoins) for crypto assets, pledging crypto assets for legal tender, and pledging crypto tokens for crypto tokens. All of the products covered adopt overcollateralization, the collateralization ratio (calculated with Collateral to Loan method) in 2019 Q1 was roughly over 300%.

In general, this industry remains in a very preliminary stage of development, where loan volumes are extremely small when compared with the trading volume of crypto assets within the secondary market. Additionally, there is still a large room for improvement in the products and services field for this industry. Moreover, it is believed that inter-bank lending services that have always kept up-to-date with the lending and borrowing market may just kick off. However, it cannot be denied that these deliberately designed products have diversified the crypto market and created more possibilities for industry developments. The new prospect brought forth by technological innovation and cooperation of lending projects is true of great and tremendous value to the ecosystem.

1. News on Crypto Asset Loan Industry

1.1 News Tracing

“JANUARY

On January 16th, 2019, Cred put forward CredEarn with which the users of Uphold (a cooperator of Cred) could gain an annual return of 10% from their deposited crypto assets.

Aave, a Fintech supporting ETHLend, acquired two regulatory licenses from the Estonian Financial Intelligence Unit (FIU): one is for cryptocurrency trading, which allows Aave to provide users with various trading services including the exchange between fiat currency, cryptocurrencies, and inter-currency trading; the other is for operating a cryptocurrency wallet, allowing the company to provide wallet services.

According to Celsius Network’s reporting, the company has already issued cryptocurrency loans with a total value of 0.63 billion USD since it began its operation last July.

“FEBRUARY

ETHLend announced that users were able to pledge BTC for LEND tokens. Before then, users were only allowed to use ETH or ERC20 as collateral.

BitBond gained the approval of the German Federal Financial Supervisory Authority (BaFin) to raise funds on Stellar’s blockchain by issuing security tokens.

Nuo has reduced its leverage ratio for users from five times to three times.

Binance Exchange pulled five crypto assets including SALT and Wings (WINDS) on 22nd.

“MARCH

SALT added more options of LTV (Loan to Value), on the basis of “30%”, “40%” and “50%”, options for “60%” and “70%” were also available.

BlockFi put forward deposited income accounts and had received a cryptocurrency deposit worth 25 million dollars in two weeks.

Coindcx, an Indian cryptocurrency exchange, announced that its crypto loan project Dcxlend had gone through beta testing and is prepared for full-on operation. This project supports six kinds of cryptocurrencies: BTC, USDT, ETH, XRP, BNB, and TUSD.

“APRIL

Dharma announced the official public opening of its crypto loan platform. Currently, platform Dharma supports ETH and stablecoin DAI, acquiring 2.7 million USD of mortgage assets after only launching for one week.

According to the results of a community vote, MakerDAO has decided to raise its maintenance fee by 4 percent to 11.5%, marking the fifth time that it’s raised its maintenance fee this year.

Celsius Network allowed Dash users to gain interest from their deposits on its own platform and to apply for loans from Dash directly without the need for lockup periods.

1.2 Industry Focuses

“MORE DIVERSIFIED SERVICES

Asset lending platforms provide more diversified services and collateral types for everyone. For instance, ETHLend not only allows users to pledge BTC for LEND tokens but is also adding more alternatives including Huobi token (HT), POA20 (POA), PAXOS (PAX) and USDCoin (USDC) as choices for collateralization. Moreover, DAI, TrueUSD (TUSD) and other stablecoins are also becoming more easily accessible. For Nexo, in addition to the existing options for BTC, ETH, XRP, BNB, and NEXO, it has added Litecoin (LTC) as its latest collateral option. The Ripio Credit Network published an RCNv4 engine labeled “Diaspore” which integrates many new functions and features including multi-credit to multi-debit products. More flexibility is clearly being added to the loan repayment plans due to the permission of payments by installments.

“ASSORTED MEASURES HAVE BEEN ADOPTED TO MAKE ASSETS MORE SECURE

All lending platforms require collateral before lending out debts. While some manage on their own, others entrust the collateral to a third party. The security of collateralized assets cannot afford to be neglected since such a large sum of funds is involved. At present, most platforms actively adopt measures to secure users’ assets before providing their services.

SALT has put forward two new types of insurance for asset securitization: Cyber Liability Insurance aims at protecting SALT when it is under the attack or threats of third-party hackers. Crime Insurance is targeted at protecting users’ crypto assets when fraud or theft occurs. Nexo has always entrusted its users’ assets to BitGo. Up till now, it already has available insurance claims up to 0.1 billion USD provided by Lloyd’s. No extra fees are required from users for this service. Moreover, Cred has also established official cooperation with BitGo and has entrusted users’ crypto assets. BitGo provides a multi-signature guarantee for Cred’s fund security through the multi-signature technique and will effectively reduce the risk of hacker assaults and key thefts, fully improving asset security.

“CLOSE INDUSTRY COOPERATION

In order to strengthen competitiveness and increase service diversity, loan platforms have continuously developed internal and external collaborations. Bloqboard has integrated into MakerDAO protocol from its own loan platform in order to appear more attractive to asset lenders and borrowers. Additionally, Bloqboard has also put forward Maker, Collateralized debt positions (CDP) over the counter (OTC) trading services, in collaboration with cross-border payment platform Wyre. This partnership is aimed at meeting the CDP holders’ demand for purchasing DAI and MKR in a market of insufficient liquidity, to clearing their debts and further facilitate large-scale CDP repayments. Nexo officially joined Binance Info’s transparency plan, in hopes of improving its transparency by sharing news, progress reports, and other related information. In February, Celsius Network announced its cooperation with MakerDAO, on which DAI was hence available. In April, it further announced its cooperation with Staked. Celsius users could deposit their tokens on Staked and gain access to another profit source. Cooperation among different enterprises can stimulate the development of the whole industry while undoubtedly benefiting the company itself.

“INDUSTRY’S CONTINUOUS HOTNESS

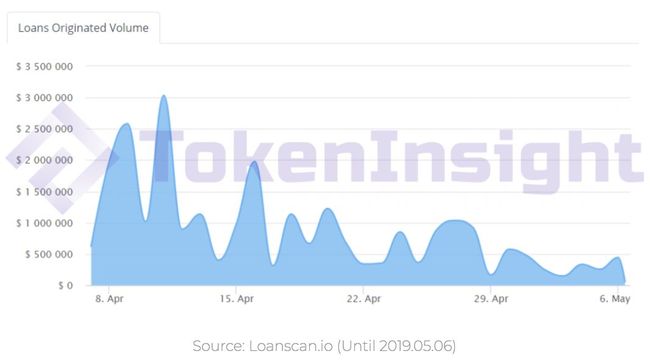

As Bloomberg reported, though having weathered the bear market of 2018, crypto asset loan services remained very popular. Service providers not only gained profits during this time but also continued to expand their services. Celsius Network’s report in January announced that it had issued an accumulated crypto loan worth 630 million dollars since its operation in last July. During the same period, Genesis Global Trading, a subsidiary company of Genesis Capital, also announced that it had given out an accumulated crypto asset loan worth 700 million dollars from March 2018 to January 2019. Even though the combined loan of the four leading loan platforms (Compound, Dharma, dYdX, and MakerDAO) in Q1 of 2019 slid by 18.56% when compared with that in Q4 of 2018, its volume still reached over 60 million dollars1. Moreover, in April, Dharma put forward a loan platform which supported ETH and stablecoin DAI, receiving collateral assets worth about 2.7 million dollars within a week of its launch. The combined loan volume of Compound, Dharma, and MakerDAO in the past 30 days has reached 26 million dollars, which reveals that crypto asset lending services have remained popular.

Figure 1-1 Combined Loan Volume of Compound, Dharma, and MakerDAO in Recent 30 day (Unit: USD)

2. A View of Industry

2.1 Main Participants of Loan

In the crypto asset lending market, the main subjects of supply and demand of products and services can be classified into three tiers: technology, applications, and exchanges. This refers to the projects that provide loan protocols based on blockchain platforms, loan platforms, and suppliers and demanders of liquidity respectively. Besides, between loan platforms and users, some projects lower user threshold by offering services such as credit card payment options. The foundational designs of the lending platforms determine whether the projects are centralized or decentralized.

Figure 2-1 Lending Market Distribution Diagram

2.2 Classification of Market Participants

Participants in the lending industry ecosystem can be classified in greater detail. As the industry still remains in its early stages of development, with basic functions yet to be perfected and complemented. It goes without saying that even though there are many projects working on the loan business, lending is performed in various ways and provides different services. In terms of users, there are conspicuous differences between user images of suppliers and demanders. We will focus on deconstructing and analyzing the different conditions of market participants respectively from the aspects of projects and users.

2.2.1 Centralized and Decentralized Models

Figure2-2 Comparison Between Decentralized and Centralized Lending

2.2.2 Matching Methods of Loan

When satisfying the demands of borrowers, there may be specific or non-specific lenders. The former one processes the lending by peer-to-peer matches in the market while the latter one gives out the loan after gathering the fund of many lenders.

Figure 2-3 A View of Crypto Asset Lending Industry

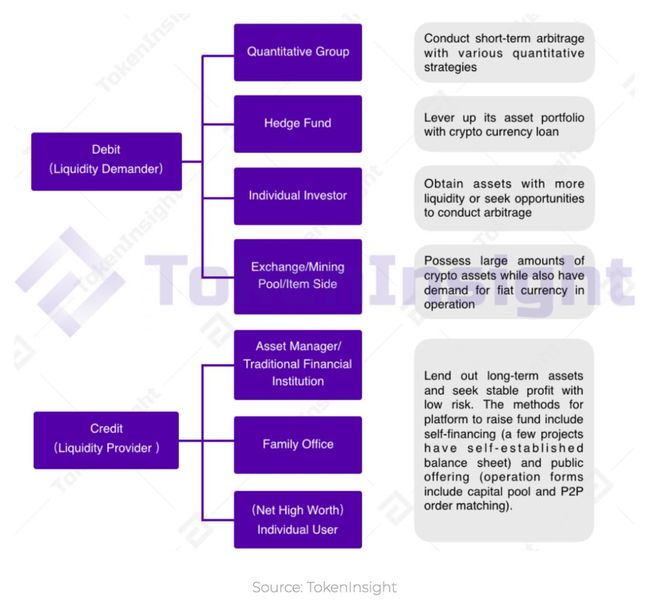

2.2.3 The Credit and Debit in the Loan Market

When TokenInsight interviewed many of the leading loan projects on the current market, most of them demonstrated that their major clients were professional investors who usually required relatively large loan volumes. The most demanding products were loans between crypto assets and fiat currency. Loans among cryptocurrencies were relatively less popular with less lending orders and smaller borrower population sizes.

On the other hand, although crypto asset loans were partly aimed at providing a channel for the long-tailed people without the permission of centralized credit threshold certifications, there is a distance between prospect and reality. At present, the lenders of crypto assets mainly consist of quantitative groups, hedge funds, and active traders while the borrowers mainly include asset managers and high net worth individual investors on the family-enterprise level. Although the development, transfer of the account, and settlement of some decentralized financial products have been decentralized, funds have still shown a pattern of centralized flow. There is still a long way to go for inclusive finance to become a reality.

Figure 2-4 The Subjects of Credit and Debit and Their Motivation

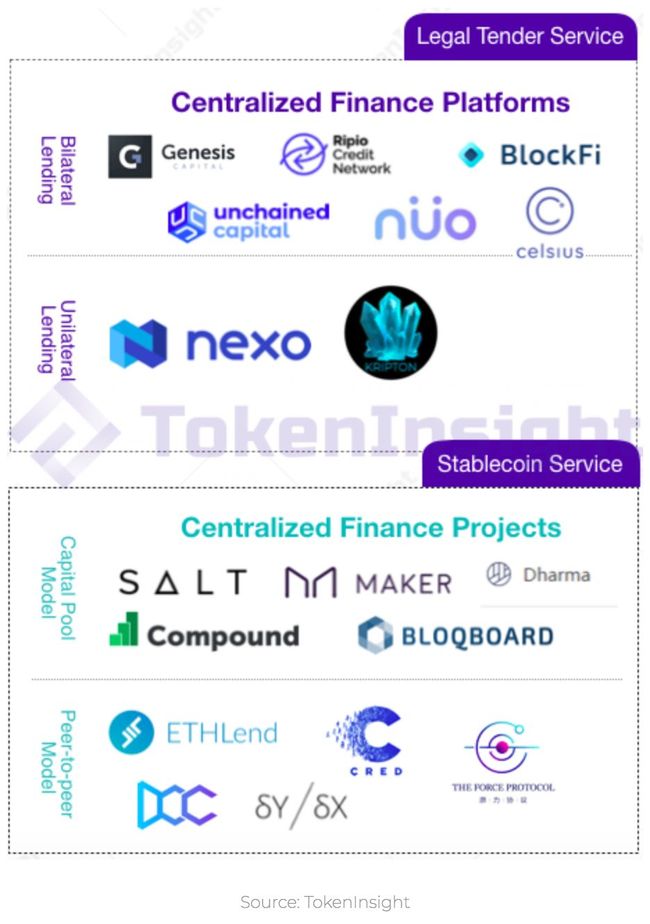

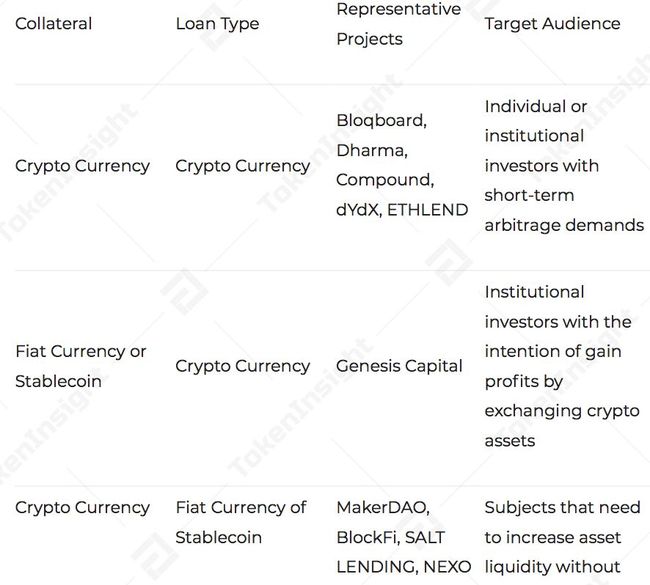

2.2.4 Service Types

According to the types of collateral assets and loans, lending services can be classified into three groups. For different products, borrowers and lenders have different incentives. For centralized platforms, available crypto assets are mainly mainstream cryptocurrencies, such as BTC, LTC, BCH, and XRP; and where USD is the dominant fiat currency while the EUR is also available on a few platforms. At present, the major decentralized lending platforms are mainly centralized around the Ethereum platform, supporting the loans of tokens of the ERC20 standard2. Although most projects provide support for ERC20 standard assets, a large part of loan volumes mainly comprises of mainstream cryptocurrencies.

In general, centralized platforms provide channels for more convenient exchange in fiat currency, attracting more sidelined funds into the industry. Meanwhile, for the financial institutions managing assets on a larger scale, centralized platforms seem to appear more attractive when compared with traditional institutions because of their advantages in regulatory compliance, liquidity, and services.

Figure 2-5 Product Types

Source: TokenInsight

2.3 Characteristics of Loan Projects

“PROJECTS WITH CLEAR STRATIFICATION AND SPECIFICATION

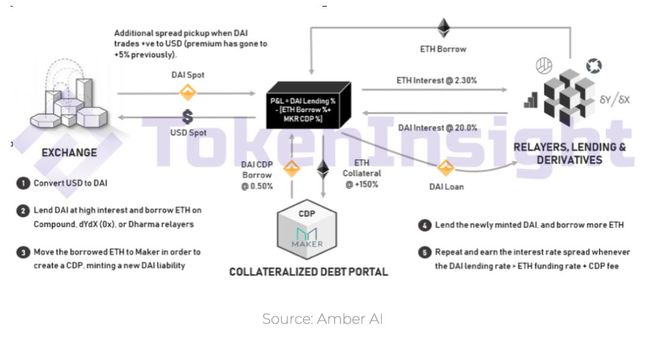

The industry remains in an early stage of development and is still relatively small scaled, with disparity among them being relatively large; internal competition has not yet emerged, and all parties actively seek cooperation. Arbitragers can seek more opportunities from the compliance of different projects. For example, Amber AI once published a report in which it analyzed arbitrage3 possibilities by combining MakerDAO,Compound, and other projects. Such a market with detailed and specialized labor division stimulates the joint development of all participants in the ecosystem and can possibly evade vicious competition during the period of rapid growth, which facilitates the industry focusing on long-term developments.

Figure 2-6 Cross-Platform Arbitrage Description

“USERS ARE HIGHLY DIVERSIFIED, BUT THE MAIN BULK OF LOAN COMES FROM INSTITUTIONAL INVESTORS

As mentioned above, it is because crypto asset loans inherited the nature of the crypto market —— open to the public without specific targets. On the other hand, it is a necessary consequence of centralized fund flows. At the current stage, though the users of crypto asset loans are diversified, centralized organizations borrow most of the loan volume. What’s worth mentioning is that, as different projects choose different development directions, the size of the exchange volume is not adequate enough to be seen as the standard to measure the quality of the platforms at present.

“DOWNTURN OF CRYPTO MARKETS IS POSSIBLY RESPONSIBLE FOR THE UPSWING OF THE CRYPTO LOAN MARKET

In Q1 of 2019, the fund volume of the loan industry experienced an outburst which was likely to carry on into Q2. This industry may be negatively related to that of the crypto markets as there was obviously a stronger intention to pledge crypto assets over borrowing fiat currency. However, it is yet to be discovered whether such loan incentives will attract more participants in a warmer crypto market.

2.4 Main Risks of Loan Industry

2.4.1 Liquidity Risk

Though the loan market has undergone rapid growth in the last two quarters, with the industry remaining in a depressed state, it still faces obstacles such as insufficient liquidity, unbalanced loan volume distribution, and incomplete interest rate setting mechanisms. Active loan volume is still far less than the exchange volume seen on the secondary market, the number of active participants population engaged in the market is relatively small4, and the number of active addresses in seven days remains at the level seen in the thousands5. With insufficient liquidity, industry development may be hindered by low market efficiency.

2.4.2 Technology Risk

Technology risks are mainly reflected in three aspects: market convergence, cross-chain interactions, and application development. First, current loan platforms are not able to share liquidity, and neither have the loan products been standardized, a trading cycle is yet to be formed in the market. Second, on the infrastructure level, as underlying blockchain networks have not developed inter-blockchain functions, the trading of underlying assets is stampeded. Especially for those decentralized platforms, in a non-interactive environment, they can only establish themselves on Ethereum where assets are more centralized. This is also the major bottleneck faced by current decentralized loan platforms. Finally, the loan products still cannot realize user-friendliness because of the incomplete facilities at the application level, which is still an obstacle to develop customers.

2.4.3 Asset Risk

The value of crypto assets have high volatility and are constantly confronted with volitility. Therefore, a complicated mechanism is needed to ensure that the collateralization ratio stays in a reasonable range. If not, the asset would be extremely easy to be liquidated.

2.4.4 Credit Risk

Though decentralized platforms have realized on-chain hosting, and some centralized platforms operate under this supervision system, users still need to somewhat trust the platform. Thus, complete distrust has not been realized. Moreover, the operations of different platforms are relatively independent, and there has not yet existed a set of credit investigation standards universally applicable to users. Hence, the credit risk for both platforms and users is still a problem that lies ahead.

3. Analysis of the Important Aspects of Loan Business

The relatively important analytical aspects of the loan business include collateral types, calculating method, the collateralized ratio value, interest rate information, whether there are other charges, the form of hosting, whether there is a mechanism for stablecoin participation, the function of platform tokens, and others.

TokenInsight tries to depict a clearer and complete image of the developments of the loan industry from the aspects mentioned above.

3.1 Collateral Asset

Based on different types of collateral assets, sample projects can be divided into two groups: the mono-collateral projects and the multi-collateral ones. As the value of crypto assets have high volatility, most platforms accept only assets with a relatively high market value at present.

For example, among the decentralized samples, Dharma accepts only the lending and borrowing of ETH and DAI; Compound supports ETH, DAI, BAT, and REP. The centralized platform Celsius, however, makes ETH, DAI, USDC, TUSD, PAX, GUSD, BTC, ZRX, OMG, LTC, BCH, DASH, XLM, XRP, ZEC, and BTG all available.

On the same page with the overall blockchain industry, loan projects also progress rapidly and universally towards a goal that more types of collateral can be accepted. Such as MakerDAO in the sample. Its first-version DAI token accepted only ETH as collateral, but, according to its white paper, the updated DAI will support more token types, which will be realized in July 2019. Therefore, investors should keep an eye on the news of the platforms’ official website to get more informed on which types of crypto assets are supported.

3.2 Collateralization Ratio

The calculation of the collateralization ratio is rather crucial to the project’s risk management. In the traditional finance industry, collateralization ratio = (loan principal + loan interest) / collateral valuation * 100%. The collateralization ratio of the bank is normally around 70%, with certain fluctuations depending on the borrower’s creditworthiness, collateral value, loan term, and other factors. Crypto asset’s collateralization ratio is the same, equal to market value ratio of loan asset to collateral asset, namely the Loan to Value Ratio (LTV).

Some platforms adopt a collateralization ratio that is equal to the market value ratio of the collateral asset to loan asset, namely the Collateral to Loan Ratio (CTL), which is normally greater than 1. As the value of crypto asset possesses high volatility, the risk of the crypto market is far greater than that of the traditional market; being that the collateralization ratio is also highly volatile.

For instance: BlockFi official website revealed its LTV Ratio at 50%; Cred LBA white paper revealed its CTL Ratio at 125%; the average collateralization ratio of Dharma in Q1 of 2019 is 154%; that of dYdX is 214%; MakerDAO, 352%; that of Compound is rather high up to 882%6, because Compound burdens relatively higher risk as the platform provides loan for the borrower in advance before matching the actual lender.

Figure 3-1 MakerDAO’s Collateralization Ratio in Real Time

Figure 3-2 The Collateralization Ratio of Compound, Dharma, MakerDAO in Real Time

3.3 Interest Rate

Interest rates are an important factor in consideration when borrowing or lending tokens. The traditional financial industry is already mature with a bunch of products, but different products will provide investors with different interest rates according to different risk levels and loan terms. Though crypto asset loans are still in its early stages, the interest rate is also determined according to different levels of risk and returns from the assets. At present, the interest rates of platforms are mainly related to an asset’s liquidity and volatility, and platforms usually accept only the tokens with large market value and good liquidity.

Similar to the traditional financial market, there are two types of interest rates for crypto asset loans: fixed and floating. Some platforms adopt fixed interest rates, such as Unchained Capital which, as is shown on its official website. The firm has interest rates at 7.25%, 8.50%, 9.00%, 11.50% and 13.00% for three months, six months, one year, two years, and three years or more respectively. Cred LBA, as its white paper reveals, has an interest rate at 12% while Nexo, on its official website, announces an annual interest rate at above 8%. Dcxlend, a crypto loan project subsidiary to Indian cryptocurrency exchange Coindcx, supports six types of cryptocurrencies: BTC, USDT, BNB, XRP, ETH and TUSD, and as its official website reveals, the monthly interest rates for them are respectively 1.5%, 1%, 0.5%, 0.5%, 0.75%, and 1%.

Compared with the fixed rate, the floating one is susceptible to market change. Investors, therefore, need to make their choice after evaluating risk and return. Typical platforms adopting floating interest rates include Compound and MakerDAO.

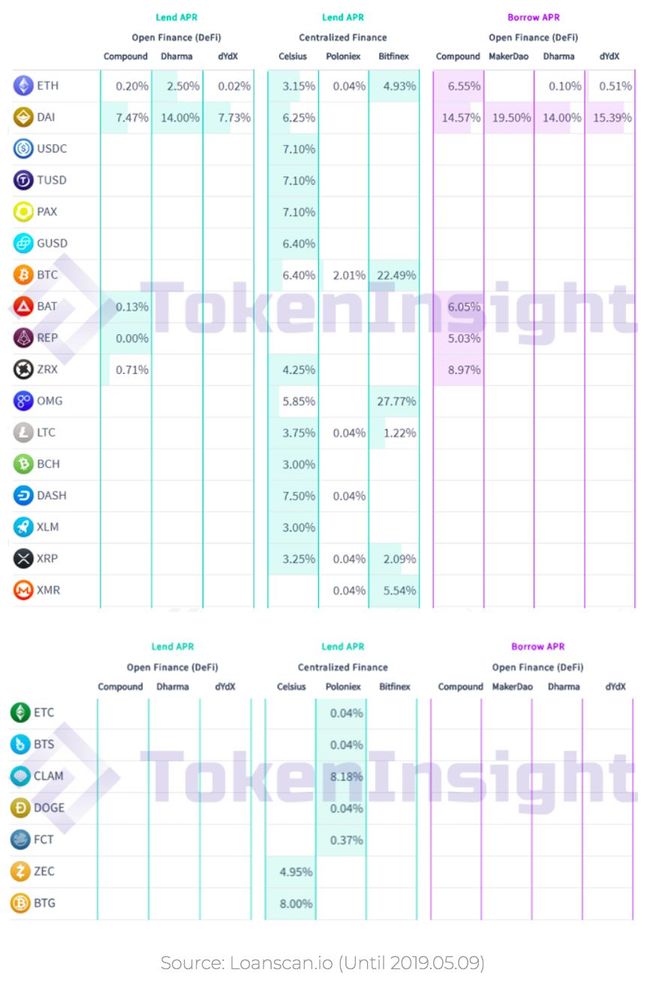

Figure 3-3 The Loan Interest Rate of Typical Centralized and Decentralized Platforms

3.4 Other Charges

The forms of charges within the crypto asset loan market are diversified.

No extra service fees: Nexo and Bitleague do not charge a service fee of any kind.

Origination Fees: BitBond charges a 2-3% origination fee and a repayment fee according to loan terms: 0.5% for three months, 0.7% for six months, 1.5% for twelve months. Unchained Capital is similar, charging an origination fee according to the term of loan contracts. The longer the term, the higher the charge.

Membership Fees: SALT charges a membership fee for different levels: regular members are charged 1 SALT annually, only allowed to borrow USD for 3-24 months; senior members are charged 30 SALT annually, and is provided with loans of USD, EUR, GBP, JPY and RMB, the loan term extending to a range from 1 hour to 36 months; enterprise-customized members are able to lend out any crypto asset promissory, and the loan term can also be negotiated. As for the project Cred LBA, by paying a membership fee, people are also allowed to join its API to enjoy the network service.

Request Fees and Funding Fees: ETHLend has set a loan request fee and loan funding fee, but a 25% discount is available when using the tokens from its platform.

Floating Service Fee: The Celsius charges a floating service fee based on the interest rate for the users, but the concrete number is not revealed in the white book.

3.5 Hosting

As all crypto asset lending platforms require collateral from loan applicants, the security of these collateralized assets is of great concern. Same to traditional finance, some platforms have adopted hosting to strengthen the security of the user’s asset. The current forms of hosting adopted are listed below:

Platform Hosting: Some platforms directly manage customers’ collateralized assets after they deposit the currencies as required. Like BTCPOP, it does not depend on a third party but keeps the collateral in an offline repository while a small part of the collateral remains accessible through the online wallet so as to maintain a certain degree of liquidity. SALT demands that users should deposit the collateral in its specially-set-up wallet and the corresponding secret keys are totally saved offline. MakerDAO keeps the collateral in CDP, a collateral depot.

Cooperative Hosting: Under this situation, the keys generated from depositing collateral are held together by multi-parties. Unchained Capital requires users to upload the keys from cooperative hardware wallets. With the keys, it establishes a website link exclusive to lending and borrowing. The collateral is kept in multi-signature addresses. While the keys are simultaneously held by the borrowers, platforms, and the Citadel SPV, the withdrawal of collateral entails two or three keys.

Escrow: some platforms do not keep the collateral on their own but entrust it to a third-party organization. For example, both Celsius Network and Nexo entrust users’ collaterals to BitGo, a third-party organization.

Lockup by Smart Contract: some platforms, such as Bloqboard, Nuo, ETHLend, The Force Protocol and others, directly lock up users’ collaterals with the smart contracts developed by third parties or themselves and thus do not need hosting of any kind. On Bloqboard platform, borrowers, if they want to borrow fund from the working capital pool, need to deposit their collaterals into Compound smart contracts before applying for a loan; if they want to conduct peer-to-peer borrowing, need to deposit collateral into Dharma smart contracts. The collaterals of Nuo users are all locked up in the accounts based on platform smart contracts.

3.6 Mechanism of Stablecoin Participation

Crypto assets have undoubted advantages over traditional fiat currency. However, partly because of high volatility in their prices, they still cannot be taken as daily-use currency until the initiation of secure stablecoins. In the field of crypto lending, new mechanisms combined with stablecoins emerge innovatively, with the MakerDAO project as a representative.

MakerDAO creates a stablecoin system based on DAI, a type of crypto asset. In short, DAI is a stable coin supported by the collateral assets, and its price is stabilized by the US dollar. MakerDAO allows users to utilize their assets on Ethereum to conduct leverage operations. After being created, like other crypto assets, DAI also can be freely given them to others, using that to pay for products and services, or stored for the long term.

This innovative and effective stablecoin system quickly pushed MakerDAO into a dominant position within the overall industry. In 2019 Q1, MakerDAO’s outstanding debt is high up to 88,499,048 dollars7, like 28 times as that of Compound, 153 times as that of Dharma and 1,241 times as that of dYdX…

3.7 Platform Token

Many platforms have published their own tokens while some clearly announced that they had no previous intention of publishing any tokens. Such as Unchained Capital, it made claims that it has no interest in creating token or using token to conduct financing. The functions of existing tokens can be concluded in the following aspects as below:

Admissions to the Platform: for some platforms, possessing a certain amount of the tokens published by their own is the basic requirement for their users. Such as Celsius, it requires that, in order to become a member of Celsius Network community, a customer must have at least one CEL. And for ZPER ecosystem, ZPR tokens are the intermediates to maintain and activate the network.

Payment and Discounts on Service Fees: some platforms, such as MakerDAO, Traxia, Cred, Distributed Credit Chain and others, stipulate that their platform tokens are the only form for paying service fees (platform licensing fee, transaction service fee, stability fee and so on). Some platforms also promised a discount on service fees when using its platform token for payments. For instance, when paying with platform tokens, The Force Protocol offers a discount on transaction service fees; the ETHLend will reduce the platform licensing fee by 25%.

Discounts on Interest: paying loan interest with platform tokens will also gain a discount. For example, Celsius provides a 20% discount when paying the loan interest with CEL. Cred and SALT also provide similar discounts but have not published their set discount rates.

Incentive Mechanisms: some platform tokens act as incentives. For example, Cred will, with LBA, reward those developers with a contribution to services or to those users bringing in new borrowers. ETHLend adopts the same strategy. Moreover, Distributed Credit Chain uses DCC as their reward for the user’s credit accumulation, encouraging the users to repay on time.

Platform Management: on Traxia, The Force Protocol, MakerDAO and other platforms, for users, having platform tokens means having the right to participate in platform management.

Membership Proof: on some platforms, the platform tokens act as a certificate of membership. Only by having corresponding platform tokens can they enjoy the special services from the platform. For example, the users having CEL are able to skip the process of queuing and apply for loans immediately.

Collateral: most platforms do not accept the platform tokens as collateral while some do. On Nexo, users will have a 50% discount on loan interest if they pledge NEXO; and The Force Protocol will raise the Loan-to-Value Ratio (LTV Ratio) for the users pledging FOR.

4. Law and Compliance

4.1 Compliance Condition of Platforms

“A FEW PLATFORMS REVEALED THAT THEY HAVE OBTAINED THE LICENSE WHILE MOST DO NOT.

At the beginning of 2019, Malaysia announced that

At the current stage, different countries have different styles of supervising crypto assets, and the supervision environment of the loan industry as a newly-emerged field is also filled with chaos, which is exactly why a revelation of license acquisition will make the platforms more convective. Common users are more prone to believe in the platforms with licenses, but the platforms that have revealed their compliance only occupy a small proportion. As far as TokenInsight is concerned, these platforms that have exposed their information in compliance include:

ETHLend

Aave, a Fintech company supporting ETHLend, acquired two regulatory licenses from Estonian Financial Intelligence Unit (FIU): one is the Cryptocurrency Exchange License, which allowed Aave to provide users with various cryptocurrency trading services and settlements, including the exchange between fiat currency and cryptocurrency and inter-currency trading; the other is the Cryptocurrency Wallet License, which allows the company to provide crypto wallet services.

Cred LBA

This January, Cred LBA acquired the California Finance Lender’s License from the government of California, America, which allows Cred LBA to provide lending and borrowing services based on cryptocurrencies in California. While California owns nearly half the crypto funds in America, equal to 12% of that of global blockchain and cryptocurrency business8, the acquisition of this license will expedite the platform’s further expansion in the international market.

BitBond

In October 2016, BitBond, a financial service company, was endowed with a license by German Federal Financial Supervisory Authority (BaFin) and was allowed it to conduct financing business for small enterprises within Germany and on a global scale, independent from the banks. In February 2019, BitBond was permitted by the German Supervision Organization to raise funds through a security token offering (STO). It plans on issuing and selling BitBond Tokens that have a nominal value of 1 euro (BB1). STO will utilize its profits to establish BitBonds core loan business. This business is open to small enterprises and free agents. The company is audited and regulated by EY.

Nexo; Unchained Capital

Nexo was established and funded by Credissimo, a European Fintech that has operated for over 10 years. It is currently under the custody of European banks and regulators and is audited by Deloitte. According to its official website, this platform currently owns the following licenses: California’s Finance Lender’s License, Financial Institution License, Virtual Currency Wallet License, and Virtual Currency Exchange License. Unchained Capital also owns Finance Lender’s license, which means that platforms are able to provide crypto currency-backed loan services for local customers and enterprises in California.

Genesis Capital

Genesis Global Trading, subordinate to Genesis Capital has gained BitLicense from New York State’s National Department of Financial Services, which means that the platform can conduct crypto currency-related business in New York State and exploit its withholding crypto assets to perform exchanges with institutional investors.

4.2 Compliance Risk

Some of the severe issues faced by the loan industry are the qualification risks of loan servers for crypto tokens, risk management measures’ effectiveness, compliance, and the insurance payback of principal and interest rates.

In Texas, from the US, issued an urgent injunction on DavorCoin, a loan project in February 2018. It pointed out that DavorCoin had issued unregistered securities, misguiding and beguiling investors with fake information. The project claimed that investors could use DavorCoin to apply for loans and gain a profit of 513 dollars each day by selecting a lockup period of 120 days, which means investors could earn a profit of 3591 dollars every seven days and by the end of August 23th, 2018, the ‘Principle Release Date’ obtain a total profit of 107,217 dollars. Many users weren’t able to remain sane and alert facing such a tempting yield.

Most of the loan platforms currently provide services for customers on a global scale. It would require joint efforts of platforms and regulators to figure out how to operate in different countries with compliance and avoid all sorts of risks. As in the traditional financial field, users should fully understand the risks they are potentially facing and judge their risk tolerance with a clear head while acquiring the services in the crypto loan industry.

5. Users and Community Activity

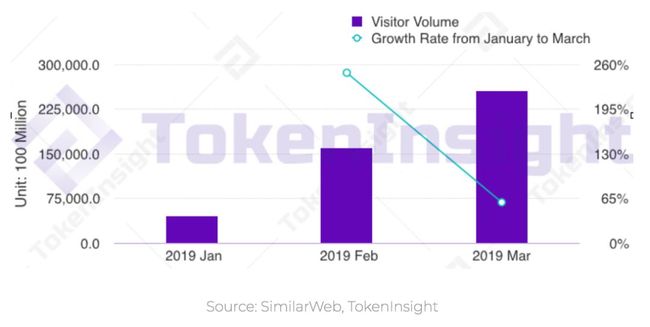

5.1 Visitor Volume

TokenInsight has investigated and recorded more than 30 digital asset loan projects and monitored their data. The visitor volume can to some extent reflect the community foundation of the lending platforms, but the visitor number is usually far larger than that of the actual users. Viewing from the visitor volume, in 2019, from January to March, the users of loan platforms maintained a constant increase, and the growth rate in February reached 248% while in March underwent a slight drop but still kept rising by 60%.

Figure 5-1 The Monthly Visitor Volume of Loan Platforms

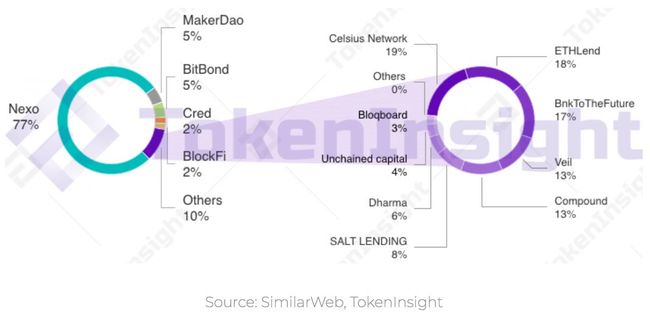

Among over 30 loan platforms from our statistics, the Top 5 occupy 90% of the visitor volume among which Nexo has the largest proportion, about 77% of the total. In the rest 23%, MakerDAO and BitBond occupy approximately 5% each, having a comparatively big share. In terms of visitor number, Nexo has a big lead in its usage and acceptance degree, taking up a large share of the market.

Figure 5-2 The Quarterly Visitor Proportion of Lending Platforms

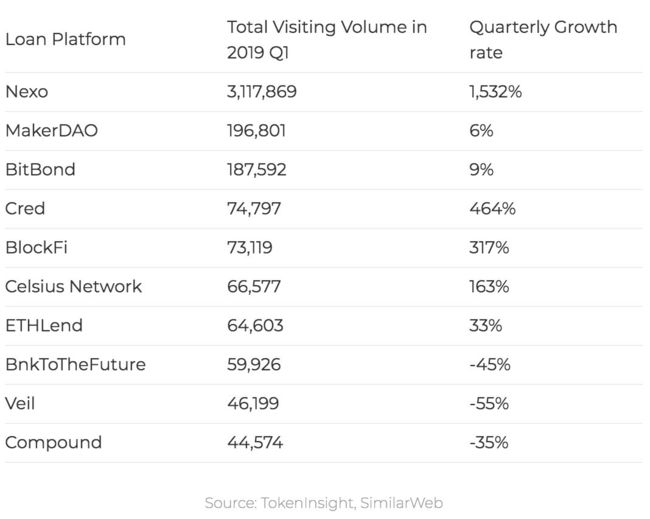

From the change of visitor volume, in the first quarter, Nexo, Cred, BlockFi, Celsius Network, and ETHLend remained the top 5 in growth rates. Particularly, Nexo’s visitors increased by 1500% when compared with that early in this quarter while those of Cred, BlockFi, Celsius Network also rose by more than 100%. BnkToTheFuture, Veil, and Compound, ranging from 8 to 10, however, shrank to different extents. According to statistics, it can be conjectured that the convergence of loan platforms might have occurred in the first quarter, which is, users move from the smaller platforms to the larger ones.

Figure 5-3 The Quarterly Visiting Volume Change of Top10 Loan Platforms

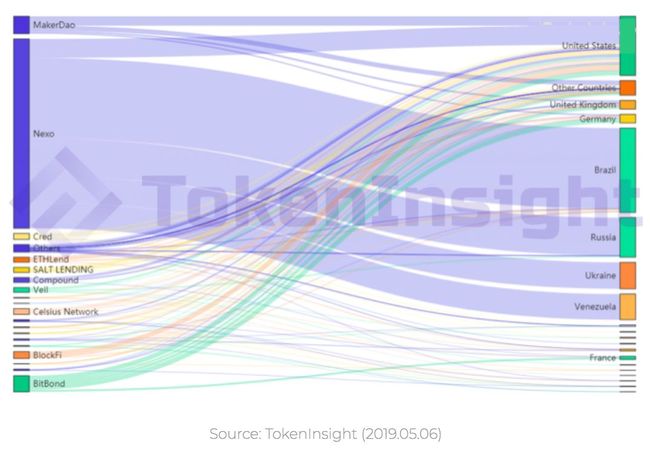

By monitoring the visitor sources, TokenInsight finds out that most of Nexo visitors are from South America and Eastern Europe. The visitors from the United States have diverse choices and do not concentrate on a single platform. Brazil has become the country with the largest population of loan platform visitors. Most platforms (except Nexo) have relatively scattered visitor distribution and do not monopolize in the market.

Figure 5-4 The Distribution of Loan Platform Visitors

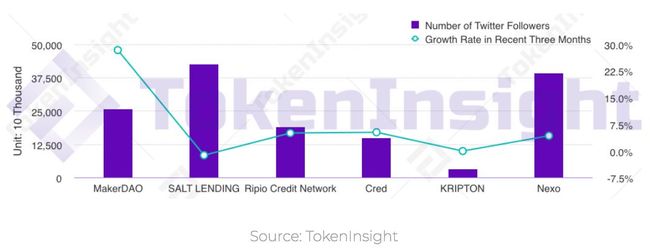

5.2 Community Heat

Among the 6 loan platforms in statistics, SALT LENDING and Nexo own the most Twitter followers. In terms of the community popularity, these two platforms attract relatively high attention. MakerDAO has had large growth in Twitter followers in the recent three months. In April, MakerDAO’s community voted on the stability fee adjustment and underwent personnel turnover, drawing a certain amount of market attention.

Figure 5-5 The Number and Growth Rate of Twitter Followers of Some Loan Platforms

6. Opinions about the Industry

TokenInsight has interviewed some leading projects in crypto asset loan market and acquired the following information:

Q: Which quality is most concerned by customers when they choose a loan platform? And, in your opinion, what is the major impediment to the development of the crypto asset loan business?

A: Before choosing a platform, they will first consider the security of assets and then the interest rate. First, the theft of users’ funds is not a rare phenomenon in the crypto market, so when they pledge their asset onto the platform, security has the priority. That also explains why SALT allocates most of its resources to develop platform techniques and self-hosting systems. We believe that the capacity of the crypto market in the future will be far larger than that of today as more and more traditional investment organizations entering the field of cryptocurrency, and we are now actively preparing ourselves for future development.

—— Daniyal Inamullah

Manager, Capital Markets at SALT

Q: As a loan platform specifically aimed at organizations, what is Genesis Capital’s user structure like? And what subjects are included in the loan market participants that you provide service for?

A: From the beginning, we offered the loan with self-raised funds which later was not adequate to satisfy the demands anymore. Then we began accepting the customers who acted as lenders and were usually organizations with huge capital reserves. Also, we do not accept retail business, mainly serving the organizations or companies. Genesis Capital has reached a lending volume of 1,500 million dollars in Q1 of 2019, with, however, actually only hundreds of customers.

Q: The bear market period of cryptocurrency may be the rising period of the loan market. However, as the cryptocurrency market recently gets warmer, what will the loan market be like in this period?

A: Indeed, in the bear market of cryptocurrency, there is a giant supply of a collateral crypto asset. But in the recent bull market, some long-term cryptocurrency holders also expect a stable return. In the current loan market, the major asset for lending and borrowing is still BTC which takes up 90% of the total volume. The development of the loan business in a bull market is worth further observation.

—— Roshun Patel

Analyst at Genesis Capital

7. Introduction to Key Projects

7.1 The Force Protocol

The Force Protocol is a development platform that, based on the mainstream public-chain system and underlying inter-blockchain protocol and through the abstraction and encapsulation of the distributed financial business process, empowers the decentralized financial application with an all-in-one solution in the form of SDK or API.

With distributed cryptocurrency financial service protocol, it hopes to provide solutions for the cross-platform asset transferring, the in-depth transaction sharing, the issuing of the stablecoin of inter-blockchain asset collateral, security token issuing, on-chain payment, transaction settlement, and other financial demands. By adopting ERC-20 smart contracts, The Force Protocol also issues FOR tokens as community reward, service fee discount, collateral, and other certificates.

With technicians as a majority, the team of The Force Protocol has a certain amount of experience on blockchain, internet finance and traditional finance, which is helpful to their further development in the crypto asset loan market.

As a project in the early stage, The Force Protocol has a relatively comprehensive consideration of its business model. Of course, the technology still needs to be examined by future product performance and reality practice.

7.2 MakerDAO

MakerDAO is one of the most important projects in the decentralized loan. Until May 2019, the ETHs locked up in Maker smart contract as CDP (Collateral Debt Position) occupied 1.926% of total issued volume, over 80% of the collateral asset of all decentralized loan projects. Therefore, MakerDAO is the decentralized finance project (DeFi) with currently the largest active user population, the biggest loan trading volume and the highest smart contract calling frequency. It is also an important participant of Ethereum ecology, having a certain degree of influence on ETH flowing. The decentralized stablecoin DAI, which is issued by Maker DAO, plays a fundamental role in the field of DeFi.

Although MakerDAO takes the leading position across the industry, its development is still hindered by its mono-collateral rule of lending and borrowing, unavailability of inter-blockchain function, centralization of stable-fee setting mechanism and other problems.

However, in recent days, MakerDAO constantly makes certain adjustments dealing with the problems mentioned above, which will be first revealed in its new version in this July. It will be able to accept multi types of collateral for borrowing DAI and the derivatives of DAI will be more diverse. MakerDAO will also make in-time fix and improvement in response to the abnormality of smart contract and defects of MKR administration mechanisms.

8. Description of the List and Rating Method

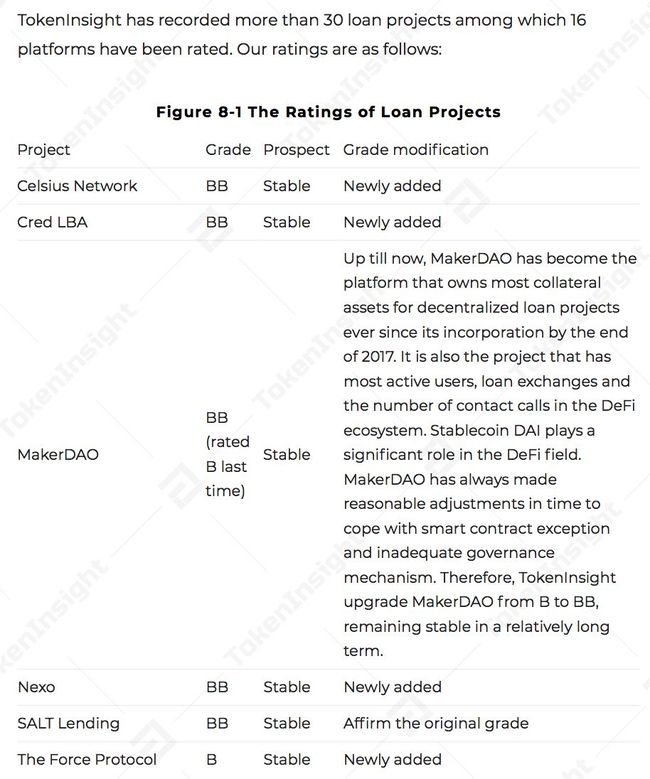

8.1 Rating Result of Loan Projects

TokenInsight has recorded more than 30 loan projects among which 16 platforms have been rated. Our ratings are as follows:

Figure 8-1 The Ratings of Loan Projects

8.2 Description of Rating Aspects

As the current crypto token market develops rapidly and the loan platforms are in the early stage of practice, the future of this industry remains unclear. However, the loan market is one of the important markets that are bound to emerge following the advent of new asset types, with capital raising in the future which cannot be underestimated. Dedicating to tracking and researching blockchain projects, TokenInsight will keep constant and close attention on the loan market derived from the financial field.

The existing rating process is based on an adequate understanding of the current loan market and platforms, determining the core factors for evaluating the loan platform before measuring those core factors with specific indexes and running those index results through standardized interval process and finally getting the rating results. Our rating aspects will be updated according to the development of the market.

Figure 8-2 The Aspects of Rating Lending Platforms

| First-Class Index | Secon-Class Index | Third-Class Index Description |

| Team Evaluation | Technology | The comprehensive strength of CTO and the team |

| Management | The comprehensive strength of CEO and the team management | |

| Sales | The comprehensive marketing ability of the team | |

| Industry Experience | The team’s experience in related industries and blockchain | |

| Investment organizations and cooperators | The strength of investment organizations, technical cooperators and financial organization cooperators and so on | |

| Consultant Team | Including technology advisors, industry and law compliance consultants, audits and others | |

| Project Evaluation | Market | Market capacity, competition intensity, and others |

| Project Analysis | The feasibility of the solution to the current problems of the project | |

| Project Practice | Including the project’s progress, plans for future, security, development transparency, and others |

Source: TokenInsight

Figure 8-3 The Aspects of Rating Lending Platforms (Continue)

| First-Class Index | Second-Class Index | Third-Class Index Description |

| Project Evaluation | Services | The comprehensive rating score of the liquidity, the transaction speed, the rates of interest rate and fee, the responding speed of customer service and others |

| Compliance | The comprehensive rating score of the licenses of a service provider, cryptocurrency trading and others | |

| Operational Risks | The comprehensive rating score of the collateral types and mechanisms, the security of customers’ fund and information and others | |

| Security of Asset Management | The rating score of the capital reserve, asset auditing, and others | |

| Ecology Evaluation | Community Heat | The rating score of the users’ population, public attention, and others |

| Heat | The comprehensive rating score of the project’s global influence | |

| Token Economy Model | The comprehensive rating score of the token applying scope, incentive mechanisms, and others | |

| Token Distribution | The rating score of TokenICO condition, ban-lifting mechanisms, and others | |

| Token Ledge | Whether the block transaction information is accessible | |

| Secondary Market | The comprehensive rating score of market cap, liquidity, and others |

Source: TokenInsight

微信小程序

Tokenin指数? Token白皮书? TIindex指数?

往日精选

去中心化交易所报告 | TokenInsight

数字资产管理报告 | TokenInsight

2019加密金融借贷报告 | TokenInsight

全球加密通证量化基金行业研究报告

底层公链行业2019 Q1报告 | TokenInsight

交易所行业2019 Q1报告 | TokenInsight

公众平台及联系方式

官网:https://tokenin.cn

微博:@TokenInsight

电报中文:https://t.me/TokenInsightChinese

电报英文:https://t.me/TokenInsightOfficial

推特:https://twitter.com/TokenInsight

商务合作:[email protected]

查看项目报告请到官网

thttps://tokenin.cn/report