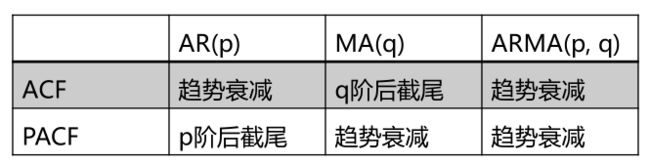

ARIMA模型参数选择

- 检查序列是否平稳

- ARMA定阶

- 通过PACF确定AR的阶数p

- 通过ACF确定MA的阶数q

- 根据参数p,d,q建立模型ARIMA(p,d,q)

# ARIMA模型

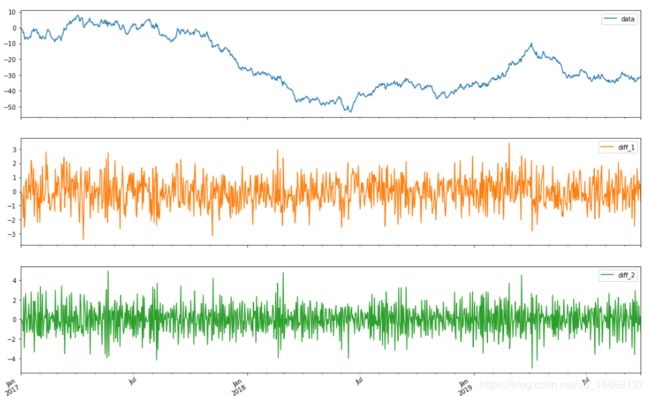

# 平稳性

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

%matplotlib inline

# 构造时间时间序列

df_obj = pd.DataFrame(np.random.randn(1000, 1),

index=pd.date_range('20170101', periods=1000),

columns=['data'])

df_obj['data'] = df_obj['data'].cumsum()

print(df_obj.head())

# 一阶差分处理

df_obj['diff_1'] = df_obj['data'].diff(1)

# 二阶差分处理

df_obj['diff_2'] = df_obj['diff_1'].diff(1)

# 查看图像

df_obj.plot(subplots=True, figsize=(18, 12))

## ACF 和 PACF

from scipy import stats

import statsmodels.api as sm

sm.graphics.tsa.plot_acf(df_obj['data'], lags=20)

sm.graphics.tsa.plot_pacf(df_obj['data'], lags=20)