Python【相关矩阵】和【协方差矩阵】

文章目录

- 相关系数矩阵

- 协方差矩阵

- 补充

- 协方差

- 相关系数

- EXCEL也能做

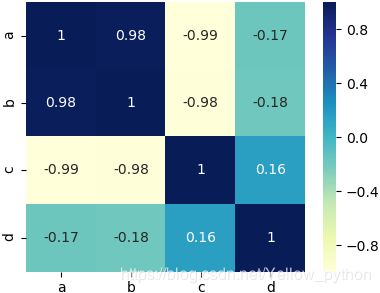

相关系数矩阵

- pandas.DataFrame(数据).corr()

import pandas as pd

df = pd.DataFrame({

'a': [11, 22, 33, 44, 55, 66, 77, 88, 99],

'b': [10, 24, 30, 48, 50, 72, 70, 96, 90],

'c': [91, 79, 72, 58, 53, 47, 34, 16, 10],

'd': [99, 10, 98, 10, 17, 10, 77, 89, 10]})

df_corr = df.corr()

# 可视化

import matplotlib.pyplot as mp, seaborn

seaborn.heatmap(df_corr, center=0, annot=True, cmap='YlGnBu')

mp.show()

协方差矩阵

- numpy.cov(数据)

import numpy as np

matric = [

[11, 22, 33, 44, 55, 66, 77, 88, 99],

[10, 24, 30, 48, 50, 72, 70, 96, 90],

[91, 79, 72, 58, 53, 47, 34, 16, 10],

[55, 20, 98, 19, 17, 10, 77, 89, 14]]

covariance_matrix = np.cov(matric)

# 可视化

print(covariance_matrix)

import matplotlib.pyplot as mp, seaborn

seaborn.heatmap(covariance_matrix, center=0, annot=True, xticklabels=list('abcd'), yticklabels=list('ABCD'))

mp.show()

补充

协方差

C o v ( X , Y ) = E [ ( X − E [ X ] ) ( Y − E [ Y ] ) ] = E [ X Y ] − 2 E [ Y ] [ X ] + E [ X ] [ Y ] = E [ X Y ] − E [ X ] [ Y ] Cov(X,Y) = E[(X-E[X])(Y-E[Y])] \newline = E[XY] - 2E[Y][X] + E[X][Y] \\ = E[XY] - E[X][Y] Cov(X,Y)=E[(X−E[X])(Y−E[Y])]=E[XY]−2E[Y][X]+E[X][Y]=E[XY]−E[X][Y]

相关系数

r ( X , Y ) = C o v ( X , Y ) V a r [ X ] V a r [ Y ] r(X,Y) = \frac{Cov(X,Y)}{\sqrt{Var[X]Var[Y]}} r(X,Y)=Var[X]Var[Y]Cov(X,Y)

EXCEL也能做

CORREL函数