【量化笔记】ARCH效应检验及GARCH建模的python实现

ARCH效应检验

import pandas as pd

SHret=pd.read_table('TRD_IndexSum.txt', index_col='Trddt', sep='\t')

/Users/yaochenli/anaconda3/lib/python3.7/site-packages/ipykernel_launcher.py:1: FutureWarning: read_table is deprecated, use read_csv instead.

"""Entry point for launching an IPython kernel.

SHret.index=pd.to_datetime(SHret.index)

SHret.head()

| Retindex | |

|---|---|

| Trddt | |

| 2009-01-05 | 0.032904 |

| 2009-01-06 | 0.030004 |

| 2009-01-07 | -0.006780 |

| 2009-01-08 | -0.023821 |

| 2009-01-09 | 0.014205 |

import matplotlib.pyplot as plt

import numpy as np

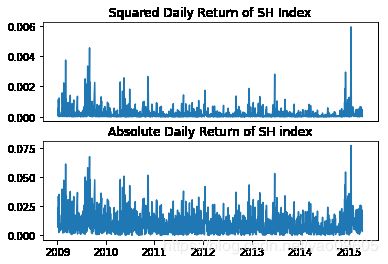

plt.subplot(211)

plt.plot(SHret**2)

plt.xticks([])

plt.title('Squared Daily Return of SH Index')

plt.subplot(212)

plt.plot(np.abs(SHret))

plt.title('Absolute Daily Return of SH index')

/Users/yaochenli/anaconda3/lib/python3.7/site-packages/pandas/plotting/_converter.py:129: FutureWarning: Using an implicitly registered datetime converter for a matplotlib plotting method. The converter was registered by pandas on import. Future versions of pandas will require you to explicitly register matplotlib converters.

To register the converters:

>>> from pandas.plotting import register_matplotlib_converters

>>> register_matplotlib_converters()

warnings.warn(msg, FutureWarning)

Text(0.5, 1.0, 'Absolute Daily Return of SH index')

from statsmodels.tsa import stattools

LjungBox=stattools.q_stat(stattools.acf(SHret**2)[1:13],len(SHret))

LjungBox[1][-1]

2.2324582490602845e-43

p值明显的小于0.05,所以可以拒绝上证指数收益率的平方是白噪声。即原序列存在ARCH效应

GARCH建模 假设GARCH(1,1)

from arch import arch_model

am = arch_model(SHret)

model=am.fit()

Iteration: 1, Func. Count: 6, Neg. LLF: -4464.281255289449

Iteration: 2, Func. Count: 19, Neg. LLF: -4464.512186616303

Iteration: 3, Func. Count: 32, Neg. LLF: -4464.710590460396

Iteration: 4, Func. Count: 45, Neg. LLF: -4464.735814639209

Iteration: 5, Func. Count: 61, Neg. LLF: -4464.735819191423

Positive directional derivative for linesearch (Exit mode 8)

Current function value: -4464.735821909855

Iterations: 9

Function evaluations: 61

Gradient evaluations: 5

/Users/yaochenli/anaconda3/lib/python3.7/site-packages/arch/univariate/base.py:577: ConvergenceWarning:

The optimizer returned code 8. The message is:

Positive directional derivative for linesearch

See scipy.optimize.fmin_slsqp for code meaning.

ConvergenceWarning)

print(model.summary())

Constant Mean - GARCH Model Results

==============================================================================

Dep. Variable: Retindex R-squared: -0.000

Mean Model: Constant Mean Adj. R-squared: -0.000

Vol Model: GARCH Log-Likelihood: 4464.74

Distribution: Normal AIC: -8921.47

Method: Maximum Likelihood BIC: -8900.16

No. Observations: 1522

Date: Wed, Aug 14 2019 Df Residuals: 1518

Time: 14:12:36 Df Model: 4

Mean Model

=============================================================================

coef std err t P>|t| 95.0% Conf. Int.

-----------------------------------------------------------------------------

mu 3.3255e-04 3.181e-04 1.045 0.296 [-2.909e-04,9.561e-04]

Volatility Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

omega 3.7169e-06 8.137e-14 4.568e+07 0.000 [3.717e-06,3.717e-06]

alpha[1] 0.0500 3.320e-04 150.614 0.000 [4.935e-02,5.065e-02]

beta[1] 0.9300 3.204e-03 290.305 0.000 [ 0.924, 0.936]

============================================================================

Covariance estimator: robust

WARNING: The optimizer did not indicate successful convergence. The message was

Positive directional derivative for linesearch. See convergence_flag.

ϵ t = σ t u t \epsilon_t=\sigma_t u_t ϵt=σtut

σ t 2 = 3.7169 ∗ 1 0 − 6 + 0.05 ϵ t − 1 2 + 0.93 σ t − 1 2 \\\sigma^2_t=3.7169*10^{-6}+0.05 \epsilon_{t-1}^2+0.93 \sigma^2_{t-1} σt2=3.7169∗10−6+0.05ϵt−12+0.93σt−12