Home Credit信贷逾期风险预测

一、引入基础包及文件

#-*- coding:utf-8 –*-

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

import warnings

from sklearn.preprocessing import LabelEncoder, MinMaxScaler, Imputer

pd.set_option("display.max_columns", None)

warnings.filterwarnings("ignore")

df_train = pd.read_csv('F:\credit\\application_train.csv')

df_test = pd.read_csv('F:\credit\\application_test.csv')

二、探索清洗数据

查看train文件基本信息,由于特征列数太多,这里就不详细列出了。重要的特征包括姓名、性别、收入、工作形式、工作年限等

print df_train.shape

(307511, 122)

print df_train.head()

print df_train.describe()

查看test文件基本信息,同样不列出详细列

print df_test.shape

(48744, 121)

train中,TARGET值为1的,说明未按时归还贷款,值为0的,说明按时归还贷款

print df_train['TARGET'].value_counts()

0 282686

1 24825

df_train['TARGET'].plot.hist()

plt.show()

显示只有8%左右的人群是未能按时归还贷款的。

# 遍历所有特征,查看特征中的空值

def mis_val_counts(df):

mis_val = df.isnull().sum()

mis_val_pec = 100*df.isnull().sum()/len(df)

missing_val_counts = pd.concat([mis_val,mis_val_pec],axis=1)

missing_val_counts_colnums = missing_val_counts.rename(columns={0: 'Missing Values', 1: '% of Total Values'})

missing_val_counts_colnums = missing_val_counts_colnums[missing_val_counts_colnums.iloc[:,1]!=0].sort_values('% of Total Values').round(1)

return missing_val_counts_colnums

print mis_val_counts(df_train)

DAYS_LAST_PHONE_CHANGE 1 0.0

CNT_FAM_MEMBERS 2 0.0

AMT_ANNUITY 12 0.0

AMT_GOODS_PRICE 278 0.1

EXT_SOURCE_2 660 0.2

DEF_60_CNT_SOCIAL_CIRCLE 1021 0.3

OBS_60_CNT_SOCIAL_CIRCLE 1021 0.3

DEF_30_CNT_SOCIAL_CIRCLE 1021 0.3

OBS_30_CNT_SOCIAL_CIRCLE 1021 0.3

NAME_TYPE_SUITE 1292 0.4

AMT_REQ_CREDIT_BUREAU_MON 41519 13.5

AMT_REQ_CREDIT_BUREAU_WEEK 41519 13.5

AMT_REQ_CREDIT_BUREAU_DAY 41519 13.5

AMT_REQ_CREDIT_BUREAU_HOUR 41519 13.5

AMT_REQ_CREDIT_BUREAU_QRT 41519 13.5

AMT_REQ_CREDIT_BUREAU_YEAR 41519 13.5

EXT_SOURCE_3 60965 19.8

OCCUPATION_TYPE 96391 31.3

EMERGENCYSTATE_MODE 145755 47.4

TOTALAREA_MODE 148431 48.3

YEARS_BEGINEXPLUATATION_AVG 150007 48.8

YEARS_BEGINEXPLUATATION_MODE 150007 48.8

YEARS_BEGINEXPLUATATION_MEDI 150007 48.8

FLOORSMAX_AVG 153020 49.8

FLOORSMAX_MEDI 153020 49.8

FLOORSMAX_MODE 153020 49.8

HOUSETYPE_MODE 154297 50.2

LIVINGAREA_AVG 154350 50.2

LIVINGAREA_MODE 154350 50.2

LIVINGAREA_MEDI 154350 50.2

... ... ...

ELEVATORS_AVG 163891 53.3

ELEVATORS_MEDI 163891 53.3

ELEVATORS_MODE 163891 53.3

NONLIVINGAREA_MEDI 169682 55.2

NONLIVINGAREA_MODE 169682 55.2

NONLIVINGAREA_AVG 169682 55.2

EXT_SOURCE_1 173378 56.4

BASEMENTAREA_MEDI 179943 58.5

BASEMENTAREA_AVG 179943 58.5

BASEMENTAREA_MODE 179943 58.5

LANDAREA_MODE 182590 59.4

LANDAREA_MEDI 182590 59.4

LANDAREA_AVG 182590 59.4

OWN_CAR_AGE 202929 66.0

YEARS_BUILD_MODE 204488 66.5

YEARS_BUILD_MEDI 204488 66.5

YEARS_BUILD_AVG 204488 66.5

FLOORSMIN_MODE 208642 67.8

FLOORSMIN_MEDI 208642 67.8

FLOORSMIN_AVG 208642 67.8

LIVINGAPARTMENTS_MODE 210199 68.4

LIVINGAPARTMENTS_MEDI 210199 68.4

LIVINGAPARTMENTS_AVG 210199 68.4

FONDKAPREMONT_MODE 210295 68.4

NONLIVINGAPARTMENTS_MEDI 213514 69.4

NONLIVINGAPARTMENTS_MODE 213514 69.4

NONLIVINGAPARTMENTS_AVG 213514 69.4

COMMONAREA_MODE 214865 69.9

COMMONAREA_AVG 214865 69.9

COMMONAREA_MEDI 214865 69.9

查看所有文本类型的特征,以及每个特征中唯一值的数量

print df_train.select_dtypes('object').apply(pd.Series.nunique)

NAME_CONTRACT_TYPE 2

CODE_GENDER 3

FLAG_OWN_CAR 2

FLAG_OWN_REALTY 2

NAME_TYPE_SUITE 7

NAME_INCOME_TYPE 8

NAME_EDUCATION_TYPE 5

NAME_FAMILY_STATUS 6

NAME_HOUSING_TYPE 6

OCCUPATION_TYPE 18

WEEKDAY_APPR_PROCESS_START 7

ORGANIZATION_TYPE 58

FONDKAPREMONT_MODE 4

HOUSETYPE_MODE 3

WALLSMATERIAL_MODE 7

EMERGENCYSTATE_MODE 2

在文本类别数据中,把类别数量小于等于2的特征经过标签化处理,然后全部进行独热编码处理。

for colnums in df_train:

if df_train[colnums].dtype == 'object':

if len(list(df_train[colnums].unique())) <= 2:

le.fit(df_train[colnums])

df_train[colnums] = le.transform(df_train[colnums])

df_test[colnums] = le.transform(df_test[colnums])

df_train = pd.get_dummies(df_train)

df_test = pd.get_dummies(df_test)

print('Training Features shape: ', df_train.shape)

print('Testing Features shape: ', df_test.shape)

('Training Features shape: ', (307511, 243))

('Testing Features shape: ', (48744, 239))

训练集比测试集多了4列,需要删除对齐

df_train_labels = df_train['TARGET']

df_train, df_test = df_train.align(df_test,join= 'inner',axis=1)

df_train['TARGET'] = df_train_labels

print('Training Features shape: ', df_train.shape)

print('Testing Features shape: ', df_test.shape)

('Training Features shape: ', (307511, 240))

('Testing Features shape: ', (48744, 239))

这里多的一列是TARGET

在之前的describe中发现年龄一栏是负值,故转化为正值

print df_train['DAYS_BIRTH'].describe()

count 307511.000000

mean -16036.995067

std 4363.988632

min -25229.000000

25% -19682.000000

50% -15750.000000

75% -12413.000000

max -7489.000000

df_train['DAYS_BIRTH'] = abs(df_train['DAYS_BIRTH'])

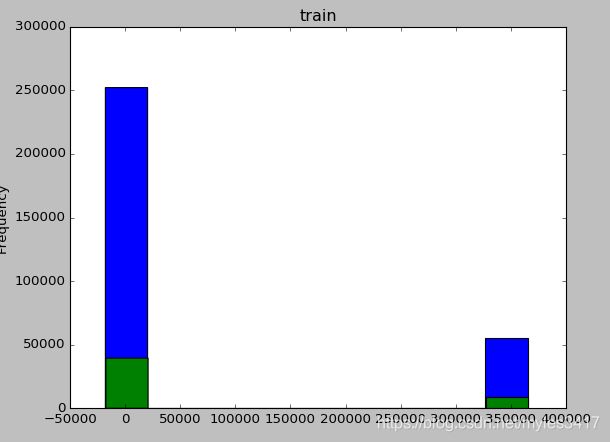

查看工龄特征,发现最大值有异常,超过1000年。

print df_train['DAYS_EMPLOYED'].describe()

count 307511.000000

mean 63815.045904

std 141275.766519

min -17912.000000

25% -2760.000000

50% -1213.000000

75% -289.000000

max 365243.000000

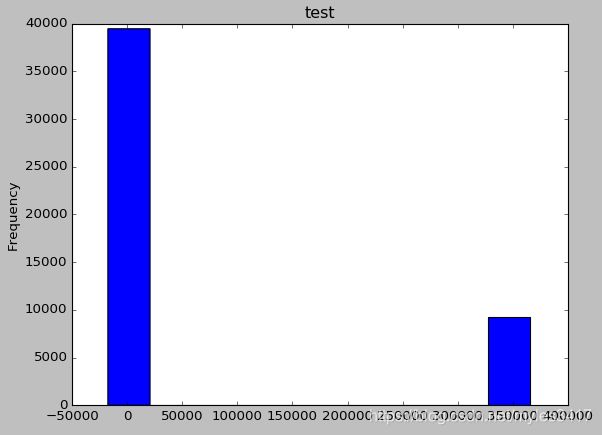

可以看到,test文件有相同的情况

df_train['DAYS_EMPLOYED'].plot.hist()

plt.title('train')

plt.show()

df_test['DAYS_EMPLOYED'].plot.hist()

plt.title('test')

plt.show()

查看具体异常值

a = df_train[df_train['DAYS_EMPLOYED']>50000]['DAYS_EMPLOYED']

print np.unique(a)

[365243]

a = df_test[df_test['DAYS_EMPLOYED']>50000]['DAYS_EMPLOYED']

print np.unique(a)

[365243]

train与test文件,工龄的异常值都是365243,这里先将他们转为na,后面再做处理。

df_train['DAYS_EMPLOYED'] = df_train['DAYS_EMPLOYED'].replace({365243: np.nan})

df_test['DAYS_EMPLOYED'] = df_test['DAYS_EMPLOYED'].replace({365243: np.nan})

三、因子分析

查看各个独立特征与标签之间的相关度,除了三个外部因素之外(文档中未给出外部因素的意义,中年龄相关性较高,其次是工龄与城市评级。

print abs(df_train.corr()['TARGET']).sort_values().tail(10)

NAME_EDUCATION_TYPE_Higher education 0.056593

NAME_INCOME_TYPE_Working 0.057481

REGION_RATING_CLIENT 0.058899

REGION_RATING_CLIENT_W_CITY 0.060893

DAYS_EMPLOYED 0.074958

DAYS_BIRTH 0.078239

EXT_SOURCE_1 0.155317

EXT_SOURCE_2 0.160472

EXT_SOURCE_3 0.178919

TARGET 1.000000

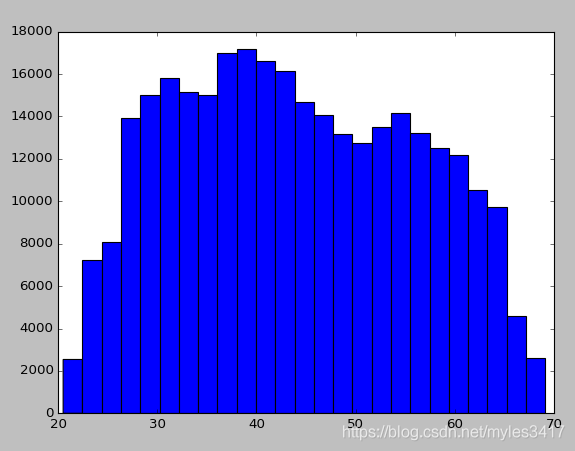

这里年龄是用天表示的,这里加一个AGE特征,用年表示年龄

查看年龄分布

df_train['AGE'] = df_train['DAYS_BIRTH']/365

plt.hist(df_train['AGE'],bins=25)

plt.show()

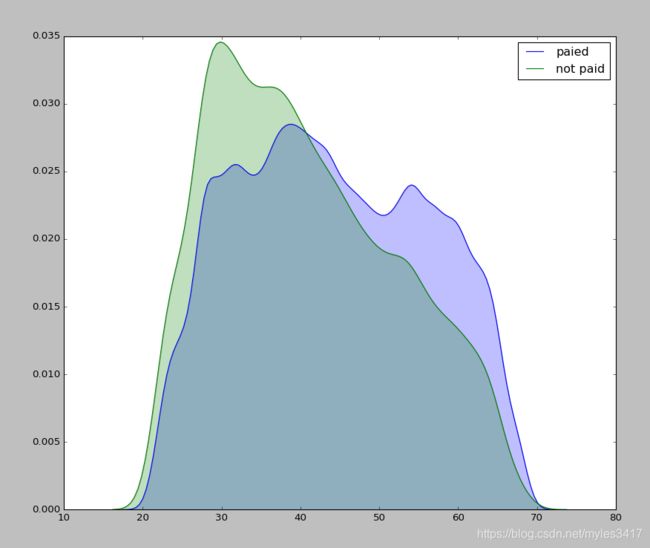

查看年龄与逾期之间的分布,可以看到年轻越小,逾期的概率越大

plt.figure(figsize = (12, 10))

sns.kdeplot(df_train.loc[df_train['TARGET']==0, 'AGE'],label= 'paied',shade=True)

sns.kdeplot(df_train.loc[df_train['TARGET']==1, 'AGE'],label= 'not paid',shade=True)

plt.show()

将年龄分为11个分组,查看各个年龄分组的平均逾期率,可以看到,平均逾期率随着年龄增长而降低

age_data = df_train[['TARGET', 'DAYS_BIRTH', 'AGE']]

age_data['AGE_BINNED'] = pd.cut(age_data['AGE'], bins=np.linspace(20, 70, num=11))

age_group = age_data.groupby('AGE_BINNED').mean()

AGE_BINNED

(65.0, 70.0] 0.037270

(60.0, 65.0] 0.052737

(55.0, 60.0] 0.055314

(50.0, 55.0] 0.066968

(45.0, 50.0] 0.074171

(40.0, 45.0] 0.078491

(35.0, 40.0] 0.089414

(30.0, 35.0] 0.102814

(25.0, 30.0] 0.111436

(20.0, 25.0] 0.123036

四、特征处理

把标签从训练集中除去。之后用IMputer处理空置,用各个特征的中位数填充。随后全部进行归一化处理,最终train与test的特征数一致。

train = df_train.drop('TARGET',axis=1)

train = train.drop('AGE',axis=1)

feature_names = list(train.columns)

test = df_test.copy()

imputer = Imputer(strategy='median')

sclar = MinMaxScaler(feature_range=(0,1))

imputer.fit(train)

train = imputer.transform(train)

test = imputer.transform(test)

sclar.fit(train)

train = sclar.transform(train)

test = sclar.transform(test)

print train.shape

print test.shape

(307511L, 239L)

(48744L, 239L)

五、建模

使用逻辑斯特线性回归进行预测,并求出每个分类的概率,最后将结果保存在CSV中

from sklearn.linear_model import LogisticRegression

log_reg = LogisticRegression(C=0.0001, max_iter=100)

log_reg.fit(train, df_train_labels)

pre_values = log_reg.predict_proba(test)[:,1]

results = pd.DataFrame({'ID':df_test['SK_ID_CURR'], 'TARGET':pre_values})

results.to_csv('F:\\credit\predict_values.csv')

print results.head(15)

0 100001 0.087932

1 100005 0.164337

2 100013 0.110671

3 100028 0.076574

4 100038 0.155924

5 100042 0.074731

6 100057 0.107673

7 100065 0.144810

8 100066 0.061533

9 100067 0.121077

10 100074 0.094727

11 100090 0.144906

12 100091 0.140260

13 100092 0.132175

14 100106 0.185343

在结果中,越接近于0,逾期风险越小。