R语言-ISLR包的weekly数据集进行logistic回归

glm()函数用与拟合广义线性模型,其中参数family:每一种响应分布(指数分布族)允许各种关联函数将均值和线性预测器关联起来

常用family:

binomal(link=‘logit’) ----响应变量服从二项分布,连接函数为logit,即logistic回归

binomal(link=‘probit’) ----响应变量服从二项分布,连接函数为probit

poisson(link=‘identity’) ----响应变量服从泊松分布,即泊松回归

1.加载相关包并查看数据

library(ISLR)

library(broom)

library(tidyverse)

library(ggplot2)

library(MASS)

library(class)

library(caret)

library(e1071)

glimpse(Weekly)

## Observations: 1,089

## Variables: 9

## $ Year 1990, 1990, 1990, 1990, 1990, 1990, 1990, 1990, 1990, 199...

## $ Lag1 0.816, -0.270, -2.576, 3.514, 0.712, 1.178, -1.372, 0.807...

## $ Lag2 1.572, 0.816, -0.270, -2.576, 3.514, 0.712, 1.178, -1.372...

## $ Lag3 -3.936, 1.572, 0.816, -0.270, -2.576, 3.514, 0.712, 1.178...

## $ Lag4 -0.229, -3.936, 1.572, 0.816, -0.270, -2.576, 3.514, 0.71...

## $ Lag5 -3.484, -0.229, -3.936, 1.572, 0.816, -0.270, -2.576, 3.5...

## $ Volume 0.1549760, 0.1485740, 0.1598375, 0.1616300, 0.1537280, 0....

## $ Today -0.270, -2.576, 3.514, 0.712, 1.178, -1.372, 0.807, 0.041...

## $ Direction Down, Down, Up, Up, Up, Down, Up, Up, Up, Down, Down, Up,...

2.对weekly数据进行数值和图像描述统计

summary(Weekly)

## Year Lag1 Lag2 Lag3

## Min. :1990 Min. :-18.1950 Min. :-18.1950 Min. :-18.1950

## 1st Qu.:1995 1st Qu.: -1.1540 1st Qu.: -1.1540 1st Qu.: -1.1580

## Median :2000 Median : 0.2410 Median : 0.2410 Median : 0.2410

## Mean :2000 Mean : 0.1506 Mean : 0.1511 Mean : 0.1472

## 3rd Qu.:2005 3rd Qu.: 1.4050 3rd Qu.: 1.4090 3rd Qu.: 1.4090

## Max. :2010 Max. : 12.0260 Max. : 12.0260 Max. : 12.0260

## Lag4 Lag5 Volume Today

## Min. :-18.1950 Min. :-18.1950 Min. :0.08747 Min. :-18.1950

## 1st Qu.: -1.1580 1st Qu.: -1.1660 1st Qu.:0.33202 1st Qu.: -1.1540

## Median : 0.2380 Median : 0.2340 Median :1.00268 Median : 0.2410

## Mean : 0.1458 Mean : 0.1399 Mean :1.57462 Mean : 0.1499

## 3rd Qu.: 1.4090 3rd Qu.: 1.4050 3rd Qu.:2.05373 3rd Qu.: 1.4050

## Max. : 12.0260 Max. : 12.0260 Max. :9.32821 Max. : 12.0260

## Direction

## Down:484

## Up :605

#cor计算相关系数

cor(Weekly[,-9])

## Year Lag1 Lag2 Lag3 Lag4

## Year 1.00000000 -0.032289274 -0.03339001 -0.03000649 -0.031127923

## Lag1 -0.03228927 1.000000000 -0.07485305 0.05863568 -0.071273876

## Lag2 -0.03339001 -0.074853051 1.00000000 -0.07572091 0.058381535

## Lag3 -0.03000649 0.058635682 -0.07572091 1.00000000 -0.075395865

## Lag4 -0.03112792 -0.071273876 0.05838153 -0.07539587 1.000000000

## Lag5 -0.03051910 -0.008183096 -0.07249948 0.06065717 -0.075675027

## Volume 0.84194162 -0.064951313 -0.08551314 -0.06928771 -0.061074617

## Today -0.03245989 -0.075031842 0.05916672 -0.07124364 -0.007825873

## Lag5 Volume Today

## Year -0.030519101 0.84194162 -0.032459894

## Lag1 -0.008183096 -0.06495131 -0.075031842

## Lag2 -0.072499482 -0.08551314 0.059166717

## Lag3 0.060657175 -0.06928771 -0.071243639

## Lag4 -0.075675027 -0.06107462 -0.007825873

## Lag5 1.000000000 -0.05851741 0.011012698

## Volume -0.058517414 1.00000000 -0.033077783

## Today 0.011012698 -0.03307778 1.000000000

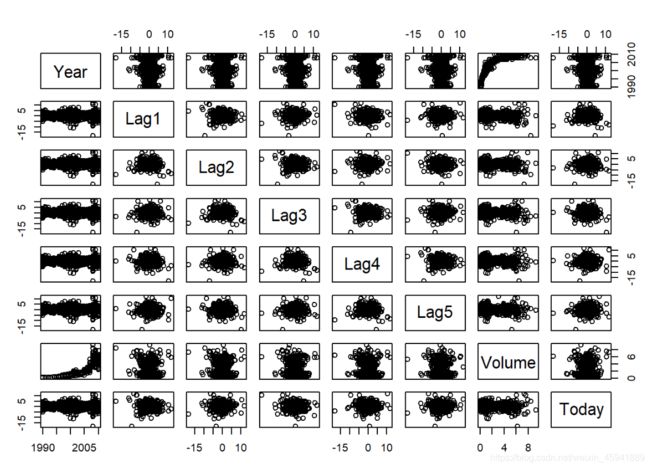

#绘制散点矩阵图

pairs(Weekly[,-9])

从相关系数矩阵和散点矩阵图可以看出:滞后时间变量Lag1~Lag2之间没有显著性关系,但交易量Volume随时间不断有明显的增加

下面对Volume随时间变化的趋势绘图

#判断Weekly中Lag1列往下移一行的数据与TOday列是否对应相等,从而判断数据是否按周增加

#lead(1:5,n=2L)运行结果3 4 5 NA NA;

#lag(1:5,n=2L)运行结果NA NA 1 2 3

Weekly %>%

filter(lead(Lag1) != Today) %>%

nrow()

## [1] 0

#按年分类并找出每年第一周的周序号

Weekly$Week<-1:nrow(Weekly)

Year_breaks<-Weekly%>%group_by(Year)%>%summarise(Week=min(Week))

#按周绘制交易量随时间的变化折线图

ggplot(Weekly,aes(x=Week,y=Volume))+

geom_line()+ #绘制折线图

geom_smooth()+ #添加平滑趋势曲线

theme_light() + #设置主题

scale_x_continuous(breaks = Year_breaks$Week,minor_breaks = NULL,labels = Year_breaks$Year)+

#如何按自己的意愿设置X轴的标签

labs(title = "Average Daily share trades vs Time",

x = "Time",

y = "volume")

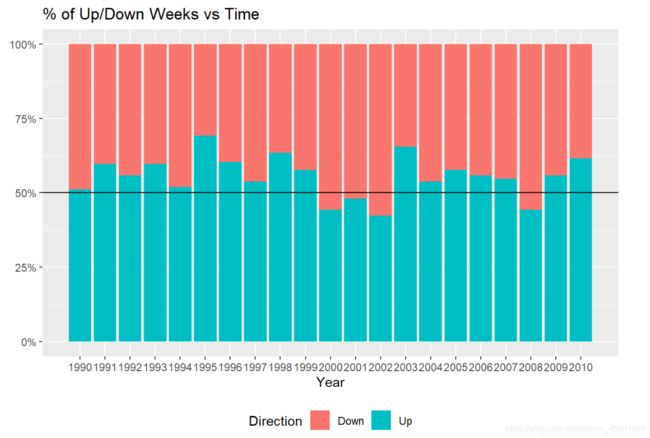

下面绘制Direction随时间变化图,只有(2000、2001、2002、2008)这四年50%以上的周没看到正回报

#绘制堆积直方图

ggplot(Weekly,aes(x=Year,fill=Direction))+

geom_bar(position = "fill")+

geom_hline(yintercept = 0.5,col="black")+ #绘制y=0.5的水平参考线

scale_x_continuous(breaks =seq(1990,2010),minor_breaks = NULL,labels = Year_breaks$Year )+

scale_y_continuous(labels = scales::percent_format())+ #把y轴数值设为百分比制

theme(axis.title.y =element_blank(),legend.position = "bottom")+ #取消y轴的标题

ggtitle("% of Up/Down Weeks vs Time")

#分别计算出现Down和Up的概率

Week.probs<-prop.table(table(Weekly$Direction))

Week.probs

## Down Up

## 0.4444444 0.5555556

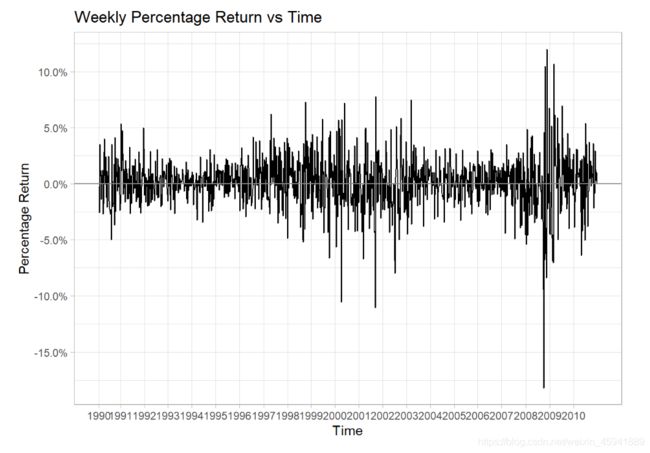

#绘制随时间变化的周波动

ggplot(Weekly, aes(x = Week, y = Today/100 )) + #Today/100进行百分比化处理

geom_line()+

scale_x_continuous(breaks = Year_breaks$Week,minor_breaks = NULL,labels = Year_breaks$Year)+

scale_y_continuous(labels = scales::percent_format(),breaks = seq(-0.2,0.2,0.05))+

geom_hline(yintercept = 0,col="grey55")+ #绘制基准线

theme_light()+

labs(title = "Weekly Percentage Return vs Time",

x="Time",

y="Percentage Return")

3.用整个数据集建立logistic回归

#进行logistic回归拟合

glm.fit=glm(Direction~Lag1+Lag2+Lag3+Lag4+Lag5+Volume,data = Weekly,family = binomial)

summary(glm.fit)

##

## Call:

## glm(formula = Direction ~ Lag1 + Lag2 + Lag3 + Lag4 + Lag5 +

## Volume, family = binomial, data = Weekly)

##

## Deviance Residuals:

## Min 1Q Median 3Q Max

## -1.6949 -1.2565 0.9913 1.0849 1.4579

##

## Coefficients:

## Estimate Std. Error z value Pr(>|z|)

## (Intercept) 0.26686 0.08593 3.106 0.0019 **

## Lag1 -0.04127 0.02641 -1.563 0.1181

## Lag2 0.05844 0.02686 2.175 0.0296 *

## Lag3 -0.01606 0.02666 -0.602 0.5469

## Lag4 -0.02779 0.02646 -1.050 0.2937

## Lag5 -0.01447 0.02638 -0.549 0.5833

## Volume -0.02274 0.03690 -0.616 0.5377

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## (Dispersion parameter for binomial family taken to be 1)

##

## Null deviance: 1496.2 on 1088 degrees of freedom

## Residual deviance: 1486.4 on 1082 degrees of freedom

## AIC: 1500.4

##

## Number of Fisher Scoring iterations: 4

tidy(glm.fit) #将模型输出结果转化为数据框

## # A tibble: 7 x 5

## term estimate std.error statistic p.value

##

## 1 (Intercept) 0.267 0.0859 3.11 0.00190

## 2 Lag1 -0.0413 0.0264 -1.56 0.118

## 3 Lag2 0.0584 0.0269 2.18 0.0296

## 4 Lag3 -0.0161 0.0267 -0.602 0.547

## 5 Lag4 -0.0278 0.0265 -1.05 0.294

## 6 Lag5 -0.0145 0.0264 -0.549 0.583

## 7 Volume -0.0227 0.0369 -0.616 0.538

结果输出的z-statistic(z-value)的计算方法跟线性回归的T检验一样,z值的绝对值较大表明拒绝原假设H0:βj=0

由各个预测变量的P值可以看出,Lag2是显著性变量

4.计算混淆矩阵和整体预测率

#预测函数predict

#参数response告诉R只用输出概率P(Y=1|X)

#如果不给predict提供预测预测数据集,它会自动拟合logistic回归的训练数据的概率

glm.probs=predict(glm.fit,type = "response")

glm.probs[1:5] #这些值对应市场是上涨而不是下跌的概率

## 1 2 3 4 5

## 0.6086249 0.6010314 0.5875699 0.4816416 0.6169013

#contrasts函数创建了一个哑变量

contrasts(Weekly$Direction)

## Up

## Down 0

## Up 1

#将用logistic回归的训练数据的预测结果转化为变化方向

glm.pred=rep("Down",1089)

glm.pred[glm.probs>.5]='Up'

#计算预测结果与原来结果的混淆矩阵,从而计算预测一致的概率

attach(Weekly)

table(glm.pred,Direction)

## Direction

## glm.pred Down Up

## Down 54 48

## Up 430 557

mean(glm.pred==Direction)

## [1] 0.5610652

用caret::confusionMatrix计算混淆矩阵

#用caret::confusionMatrix计算混淆矩阵

attach(Weekly)

## The following objects are masked from Weekly (pos = 3):

##

## Direction, Lag1, Lag2, Lag3, Lag4, Lag5, Today, Volume, Week, Year

Predicted<-factor(ifelse(predict(glm.fit,type = "response")<.5,"Down","Up"))

confusionMatrix(Predicted,Direction,positive = "Up")

## Confusion Matrix and Statistics

##

## Reference

## Prediction Down Up

## Down 54 48

## Up 430 557

##

## Accuracy : 0.5611

## 95% CI : (0.531, 0.5908)

## No Information Rate : 0.5556

## P-Value [Acc > NIR] : 0.369

##

## Kappa : 0.035

##

## Mcnemar's Test P-Value : <2e-16

##

## Sensitivity : 0.9207

## Specificity : 0.1116

## Pos Pred Value : 0.5643

## Neg Pred Value : 0.5294

## Prevalence : 0.5556

## Detection Rate : 0.5115

## Detection Prevalence : 0.9063

## Balanced Accuracy : 0.5161

##

## 'Positive' Class : Up

prop.table(table(Predicted))

## Predicted

## Down Up

## 0.09366391 0.90633609

5.用2009年之前的训练数据拟合logistic回归模型,其中只把Lag2作为预测变量,计算混淆矩阵的和测试集(2009和2010年)中总体预测准确率

#用1990-2008年的训练数据来拟合logistic回归模型,只把lag2作为预测变量,计算2009-2010的预测准确率

attach(Weekly)

train=(Year<2009) #生成一个对应的布尔向量

#布尔向量可用于获取某个矩阵的行或子列

Weekly.2009=Weekly[!train,] #测试集数据

dim(Weekly.2009) #查看该数据的维度

## [1] 104 10

glm.fit1<-glm(Direction~Lag2,data = Weekly,family = binomial,subset = train)

# or glm.fit1<-glm(Direction~Lag2,data = Weekly[train,],family = binomial)

summary(glm.fit1)

##

## Call:

## glm(formula = Direction ~ Lag2, family = binomial, data = Weekly,

## subset = train)

##

## Deviance Residuals:

## Min 1Q Median 3Q Max

## -1.536 -1.264 1.021 1.091 1.368

##

## Coefficients:

## Estimate Std. Error z value Pr(>|z|)

## (Intercept) 0.20326 0.06428 3.162 0.00157 **

## Lag2 0.05810 0.02870 2.024 0.04298 *

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## (Dispersion parameter for binomial family taken to be 1)

##

## Null deviance: 1354.7 on 984 degrees of freedom

## Residual deviance: 1350.5 on 983 degrees of freedom

## AIC: 1354.5

##

## Number of Fisher Scoring iterations: 4

glm.probs1<-predict(glm.fit1,Weekly.2009,type = "response")

glm.pred1<-rep("Down",104)

glm.pred1[glm.probs1>.5]="Up"

attach(Weekly.2009)

table(glm.pred1,Direction)

## Direction

## glm.pred1 Down Up

## Down 9 5

## Up 34 56

mean(glm.pred1==Direction)

## [1] 0.625

用caret::confusionMatrix计算混淆矩阵

predicted1<-factor(ifelse(predict(glm.fit1,Weekly.2009,type = "response")<.5,"Down","Up"))

confusionMatrix(data = predicted1,reference=Weekly.2009$Direction,positive = "Up")

## Confusion Matrix and Statistics

##

## Reference

## Prediction Down Up

## Down 9 5

## Up 34 56

##

## Accuracy : 0.625

## 95% CI : (0.5247, 0.718)

## No Information Rate : 0.5865

## P-Value [Acc > NIR] : 0.2439

##

## Kappa : 0.1414

##

## Mcnemar's Test P-Value : 7.34e-06

##

## Sensitivity : 0.9180

## Specificity : 0.2093

## Pos Pred Value : 0.6222

## Neg Pred Value : 0.6429

## Prevalence : 0.5865

## Detection Rate : 0.5385

## Detection Prevalence : 0.8654

## Balanced Accuracy : 0.5637

##

## 'Positive' Class : Up

##

No Information Rate:0.5865,即表明测试数据的58.65%为最大分类(Up),因此这是分类器的一个基准线

Accuracy:0.625>0.5865

我们为单面测试提供了p值,以查看准确性是否优于“无信息率”。 P值[Acc> NIR]:0.2439> 0.05⟹没有明显的证据表明我们的分类器优于基线策略。

完整代码

library(ISLR)

library(broom)

library(tidyverse)

library(ggplot2)

library(MASS)

library(class)

library(caret)

library(e1071)

glimpse(Weekly)

summary(Weekly)

#cor计算相关系数

cor(Weekly[,-9])

#绘制散点矩阵图

pairs(Weekly[,-9])

#判断Weekly中Lag1列往下移一行的数据与TOday列是否对应相等,从而判断数据是否按周增加

#lead(1:5,n=2L)运行结果3 4 5 NA NA;

#lag(1:5,n=2L)运行结果NA NA 1 2 3

Weekly %>%

filter(lead(Lag1) != Today) %>%

nrow()

#按年分类并找出每年第一周的周序号

Weekly$Week<-1:nrow(Weekly)

Year_breaks<-Weekly%>%group_by(Year)%>%summarise(Week=min(Week))

#按周绘制交易量随时间的变化折线图

ggplot(Weekly,aes(x=Week,y=Volume))+

geom_line()+ #绘制折线图

geom_smooth()+ #添加平滑趋势曲线

theme_light() + #设置主题

scale_x_continuous(breaks = Year_breaks$Week,minor_breaks = NULL,labels = Year_breaks$Year)+

#如何按自己的意愿设置X轴的标签

labs(title = "Average Daily share trades vs Time",

x = "Time",

y = "volume")

#绘制堆积直方图

ggplot(Weekly,aes(x=Year,fill=Direction))+

geom_bar(position = "fill")+

geom_hline(yintercept = 0.5,col="black")+ #绘制y=0.5的水平参考线

scale_x_continuous(breaks =seq(1990,2010),minor_breaks = NULL,labels = Year_breaks$Year )+

scale_y_continuous(labels = scales::percent_format())+ #把y轴数值设为百分比制

theme(axis.title.y =element_blank(),legend.position = "bottom")+ #取消y轴的标题

ggtitle("% of Up/Down Weeks vs Time")

#分别计算出现Down和Up的概率

Week.probs<-prop.table(table(Weekly$Direction))

Week.probs

#绘制随时间变化的周波动

ggplot(Weekly, aes(x = Week, y = Today/100 )) + #Today/100进行百分比化处理

geom_line()+

scale_x_continuous(breaks = Year_breaks$Week,minor_breaks = NULL,labels = Year_breaks$Year)+

scale_y_continuous(labels = scales::percent_format(),breaks = seq(-0.2,0.2,0.05))+

geom_hline(yintercept = 0,col="grey55")+ #绘制基准线

theme_light()+

labs(title = "Weekly Percentage Return vs Time",

x="Time",

y="Percentage Return")

#进行logistic回归拟合

glm.fit=glm(Direction~Lag1+Lag2+Lag3+Lag4+Lag5+Volume,data = Weekly,family = binomial)

summary(glm.fit)

tidy(glm.fit) #将模型输出结果转化为数据框

#预测函数predict

#参数response告诉R只用输出概率P(Y=1|X)

#如果不给predict提供预测预测数据集,它会自动拟合logistic回归的训练数据的概率

glm.probs=predict(glm.fit,type = "response")

glm.probs[1:5] #这些值对应市场是上涨而不是下跌的概率

#contrasts函数创建了一个哑变量

contrasts(Weekly$Direction)

#将用logistic回归的训练数据的预测结果转化为变化方向

glm.pred=rep("Down",1089)

glm.pred[glm.probs>.5]='Up'

#计算预测结果与原来结果的混淆矩阵,从而计算预测一致的概率

attach(Weekly)

table(glm.pred,Direction)

mean(glm.pred==Direction)

#用caret::confusionMatrix计算混淆矩阵

attach(Weekly)

Predicted<-factor(ifelse(predict(glm.fit,type = "response")<.5,"Down","Up"))

confusionMatrix(Predicted,Direction,positive = "Up")

prop.table(table(Predicted))

#用1990-2008年的训练数据来拟合logistic回归模型,只把lag2作为预测变量,计算2009-2010的预测准确率

attach(Weekly)

train=(Year<2009) #生成一个对应的布尔向量

#布尔向量可用于获取某个矩阵的行或子列

Weekly.2009=Weekly[!train,] #测试集数据

dim(Weekly.2009) #查看该数据的维度

glm.fit1<-glm(Direction~Lag2,data = Weekly,family = binomial,subset = train)

# or glm.fit1<-glm(Direction~Lag2,data = Weekly[train,],family = binomial)

summary(glm.fit1)

glm.probs1<-predict(glm.fit1,Weekly.2009,type = "response")

glm.pred1<-rep("Down",104)

glm.pred1[glm.probs1>.5]="Up"

attach(Weekly.2009)

table(glm.pred1,Direction)

mean(glm.pred1==Direction)

#用confusionMatrix生成混淆矩阵

predicted1<-factor(ifelse(predict(glm.fit1,Weekly.2009,type = "response")<.5,"Down","Up"))

confusionMatrix(data = predicted1,reference=Weekly.2009$Direction,positive = "Up")

参考kaggle搬运加工练习小姐妹

原文参考:https://www.kaggle.com/lmorgan95/islr-classification-ch-4-solutions