利用LSTM进行股票预测分析

需要使用的库:

- tushare

- pytorch

- pandas

- numpy

- matplotlib

1. 数据导入

import tushare as ts

ts.set_token('98edbe9c3e444002decb09646838a02f0307e41bd5ce51bb5b2a99c8')

ts_pro = ts.pro_api()

help(ts)

Help on package tushare:

NAME

tushare - # -*- coding:utf-8 -*-

PACKAGE CONTENTS

bond (package)

coins (package)

data (package)

fund (package)

futures (package)

internet (package)

pro (package)

stock (package)

subs (package)

trader (package)

util (package)

VERSION

1.2.62

AUTHOR

Jimmy Liu

FILE

e:\anaconda3\lib\site-packages\tushare\__init__.py

# 股票代码

ts_code = '002069.SZ'

# 开始时间

start_date = '2006-01-01'

# 结束时间

end_date = '2020-01-01'

df = ts_pro.daily(

ts_code=ts_code,

start_date=start_date,

end_date=end_date)

# 将获取的文件存储在本地

df.to_csv('002069.csv', index=0)

import pandas as pd

df = pd.read_csv('002069.csv')

# 按照时间进行排序,方便预测处理

df = df.sort_values(['trade_date'], ascending=True)

# 简要查看文件信息

df.head()

| ts_code | trade_date | open | high | low | close | pre_close | change | pct_chg | vol | amount | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 3034 | 002069.SZ | 20060928 | 60.89 | 64.48 | 58.00 | 62.11 | 25.00 | 37.11 | 148.44 | 169301.73 | 1.028809e+06 |

| 3033 | 002069.SZ | 20060929 | 64.10 | 67.00 | 62.48 | 62.99 | 62.11 | 0.88 | 1.42 | 49290.44 | 3.182028e+05 |

| 3032 | 002069.SZ | 20061009 | 63.00 | 66.15 | 62.16 | 65.00 | 62.99 | 2.01 | 3.19 | 28449.04 | 1.827514e+05 |

| 3031 | 002069.SZ | 20061010 | 64.89 | 71.50 | 64.00 | 71.49 | 65.00 | 6.49 | 9.98 | 34935.76 | 2.381439e+05 |

| 3030 | 002069.SZ | 20061011 | 70.20 | 71.80 | 69.22 | 69.99 | 71.49 | -1.50 | -2.10 | 15807.24 | 1.109196e+05 |

2. 数据预处理

# 选取这几个属性作为输入特征

use_cols = ['open', 'high', 'low', 'close', 'pre_close', 'vol', 'amount']

df = df[use_cols]

df.head()

| open | high | low | close | pre_close | vol | amount | |

|---|---|---|---|---|---|---|---|

| 3034 | 60.89 | 64.48 | 58.00 | 62.11 | 25.00 | 169301.73 | 1.028809e+06 |

| 3033 | 64.10 | 67.00 | 62.48 | 62.99 | 62.11 | 49290.44 | 3.182028e+05 |

| 3032 | 63.00 | 66.15 | 62.16 | 65.00 | 62.99 | 28449.04 | 1.827514e+05 |

| 3031 | 64.89 | 71.50 | 64.00 | 71.49 | 65.00 | 34935.76 | 2.381439e+05 |

| 3030 | 70.20 | 71.80 | 69.22 | 69.99 | 71.49 | 15807.24 | 1.109196e+05 |

# 为了归一化后复现原来数据

close_min = df['close'].min()

close_max = df['close'].max()

# 归一化处理(0,1)

df=df.apply(lambda x:(x-min(x))/(max(x)-min(x)))

df.head()

| open | high | low | close | pre_close | vol | amount | |

|---|---|---|---|---|---|---|---|

| 3034 | 0.401512 | 0.416768 | 0.404243 | 0.401345 | 0.151699 | 0.166571 | 0.800115 |

| 3033 | 0.423566 | 0.433710 | 0.436792 | 0.407265 | 0.401345 | 0.047720 | 0.247007 |

| 3032 | 0.416008 | 0.427995 | 0.434467 | 0.420787 | 0.407265 | 0.027080 | 0.141577 |

| 3031 | 0.428993 | 0.463964 | 0.447835 | 0.464447 | 0.420787 | 0.033504 | 0.184693 |

| 3030 | 0.465476 | 0.465981 | 0.485760 | 0.454356 | 0.464447 | 0.014561 | 0.085666 |

import numpy as np

# 序列长度为30,即用前一个月的数据预测之后一天的数据

sequence = 30

X = []

Y = []

for i in range(df.shape[0]-sequence):

# 选择use_cols作为特征

X.append(np.array(df.iloc[i:(i+sequence),].values, dtype=np.float))

# 选择close作为标签输出

Y.append(np.array(df.iloc[(i+sequence),3],dtype=np.float))

# 划分训练集和测试集

trainx, trainy = X[:int(0.8*df.shape[0])], Y[:int(0.8*df.shape[0])]

testx, testy = X[int(0.8*df.shape[0]):], Y[int(0.8*df.shape[0]):]

print(len(trainx))

print(len(testx))

2428

577

import torch

import torch.utils.data as Data

torch.manual_seed(1)

# list -> numpy

trainx = np.array(trainx)

trainy = np.array(trainy)

testx = np.array(testx)

testy = np.array(testy)

# numpy -> torch

trainx = torch.from_numpy(trainx)

trainy = torch.from_numpy(trainy)

testx = torch.from_numpy(testx)

testy = torch.from_numpy(testy)

print('trainx size: ', trainx.size())

print('trainy size: ', trainy.size())

print('testx size: ', testx.size())

print('testy size: ', testy.size())

trainx size: torch.Size([2428, 30, 7])

trainy size: torch.Size([2428])

testx size: torch.Size([577, 30, 7])

testy size: torch.Size([577])

# 批处理 batch的大小为32

train_dataset = Data.TensorDataset(trainx, trainy)

test_dataset = Data.TensorDataset(testx, testy)

train_loader = Data.DataLoader(

dataset=train_dataset,

batch_size=32,

shuffle=True,

num_workers=2

)

test_loader = Data.DataLoader(

dataset=test_dataset,

batch_size=32,

shuffle=True,

num_workers=2

)

3. 定义网络模型

input_size = 7

seq_len = 30

hidden_size = 32

output_size = 1

import torch.nn as nn

import torch.nn.functional as F

from torch.autograd import Variable

class MyNet(nn.Module):

def __init__(self, input_size=input_size, hidden_size=hidden_size, output_size=output_size):

super(MyNet, self).__init__()

self.input_size = input_size

self.hidden_size = hidden_size

self.output_size = output_size

self.lstm = nn.LSTM(input_size=input_size, hidden_size=hidden_size, batch_first=True)

self.fc = nn.Linear(self.hidden_size*seq_len, self.output_size)

def forward(self, input):

out,_ = self.lstm(input)

b, s, h = out.size()

out = self.fc(out.reshape(b, s*h))

return out

net = MyNet()

print(net)

MyNet(

(lstm): LSTM(7, 32, batch_first=True)

(fc): Linear(in_features=960, out_features=1, bias=True)

)

4. 选择损失函数及优化器

import torch.optim as optim

from tqdm import tqdm

loss_function = nn.MSELoss()

optimizer = optim.Adam(net.parameters(), lr=0.001)

for epoch in tqdm(range(100)):

total_loss = 0

for _,(data, label) in enumerate(train_loader):

data = Variable(data).float()

pred = net(data)

label = Variable(label).float()

label = label.unsqueeze(1)

loss = loss_function(pred, label)

loss.backward()

optimizer.step()

optimizer.zero_grad()

total_loss += loss.item()

if (epoch+1) % 10 == 0:

print('Epoch: ', epoch+1, ' loss: ', total_loss)

10%|█ | 10/100 [00:17<02:32, 1.70s/it]Epoch: 10 loss: 0.03518655754669453

20%|██ | 20/100 [00:34<02:14, 1.68s/it]Epoch: 20 loss: 0.023873500191257335

30%|███ | 30/100 [00:53<02:11, 1.88s/it]Epoch: 30 loss: 0.02149457185441861

40%|████ | 40/100 [01:14<02:07, 2.13s/it]Epoch: 40 loss: 0.017912164659719565

50%|█████ | 50/100 [01:31<01:25, 1.72s/it]Epoch: 50 loss: 0.013031252356086043

60%|██████ | 60/100 [01:51<01:14, 1.87s/it]Epoch: 60 loss: 0.014165752041662927

70%|███████ | 70/100 [02:10<01:02, 2.09s/it]Epoch: 70 loss: 0.011516284157551127

80%|████████ | 80/100 [02:27<00:35, 1.79s/it]Epoch: 80 loss: 0.01033103184090578

90%|█████████ | 90/100 [02:47<00:17, 1.74s/it]Epoch: 90 loss: 0.010540407126427453

100%|██████████| 100/100 [03:07<00:00, 1.88s/it]Epoch: 100 loss: 0.01101792572899285

5. 测试模型

pred_list = []

label_list = []

for _, (data, label) in enumerate(test_loader):

data = Variable(data).float()

pred = net(data)

pred_list.extend(pred.data.squeeze(1).tolist())

label_list.extend(label.tolist())

pred_list[:5]

[0.003661651164293289,

0.004493666812777519,

0.017206232994794846,

0.004013188183307648,

-0.003268543630838394]

label_list[:5]

[0.005449041372351158,

0.007938109653548601,

0.015136226034308779,

0.00538176925664312,

0.0014127144298688192]

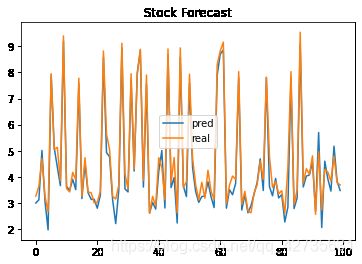

简单查看预测结果与真实值,发现相差不是特别明显

import matplotlib.pyplot as plt

plt.plot([i*(close_max-close_min)+close_min for i in pred_list[:100]] , label='pred')

plt.plot([i*(close_max-close_min)+close_min for i in label_list[:100]], label='real')

plt.title('Stock Forecast')

plt.legend()

plt.show()