集成学习:Bagging Boosting&Stacking (二)

集成学习:Bagging Boosting&Stacking

- 5.Python例子

-

- 5.1 Import 库

- 5.2 加载数据,数据处理

-

- 5.2.1 审视数据

- 5.2.2 数据类型字段更改

- 5.2.3 缺失值处理

- 5.2.4 数据转化

- 5.3 划分训练集与测试集

- 5.4 回归模型

-

- 5.4.1 Linear Regression

- 5.4.2 Lasso Regression

- 5.4.3 Elastic Regression

- 5.4.4 KernelRidge Regression

- 5.5 集成模型

-

- 5.5.1 Bagging

- 5.5.2 Boosting

- 5.5.3 Stacking

5.Python例子

这里我们将使用下面这个数据集,使用二手车的12个特征属性,来预测这辆二手车能卖多少w。给把握不住二手车水深的卖家,卖出一个好w。

cars-price

来看下数据的特征名称与特征描述

| 属性 | 描述 |

|---|---|

| Name | 汽车的品牌和型号 |

| Location | 汽车出售或可供购买的地点 |

| Year | 汽车年份 |

| Kilometers_Driven | 前车主在车内行驶的总公里数(单位:KM) |

| Fuel_Type | 燃料类型 |

| Transmission | 变速器类型 |

| Owner_Type | 车子是所属权(是一手还是二手) |

| Mileage | 标准里程,单位为kmpl或km/kg |

| Engine | 发动机的排量(单位:cc) |

| Power | 发动机最大功率 |

| Seats | 车里的座位数 |

| New_Price | 新车的价格 |

| Price | 二手车的价格以10亿卢比为单位 |

5.1 Import 库

MacOs安装lightgbm方法:

#先安装cmake和gcc,安装过的直接跳过前两步

brew install cmake

brew install gcc

git clone --recursive https://github.com/Microsoft/LightGBM

cd LightGBM

#在cmake之前有一步添加环境变量

export CXX=g++-7 CC=gcc-7

mkdir build ; cd build

cmake ..

make -j4

cd ../python-package

sudo python setup.py install

import warnings

from sklearn.model_selection import train_test_split

from sklearn.pipeline import make_pipeline

from sklearn.preprocessing import RobustScaler

from sklearn.linear_model import LinearRegression, Lasso, ElasticNet

from sklearn.kernel_ridge import KernelRidge

from sklearn.ensemble import BaggingRegressor

from sklearn.ensemble import GradientBoostingRegressor

import xgboost as xgb

import lightgbm as lgb

from sklearn.ensemble import StackingRegressor

from sklearn.model_selection import cross_val_score

from sklearn.model_selection import cross_val_predict

from sklearn.metrics import mean_squared_error

warnings.filterwarnings("ignore")

n_jobs=-1

random_state=42

5.2 加载数据,数据处理

data =pd.read_csv('train.csv')

按照之前文章的数据处理方式:

数据处理汇总

5.2.1 审视数据

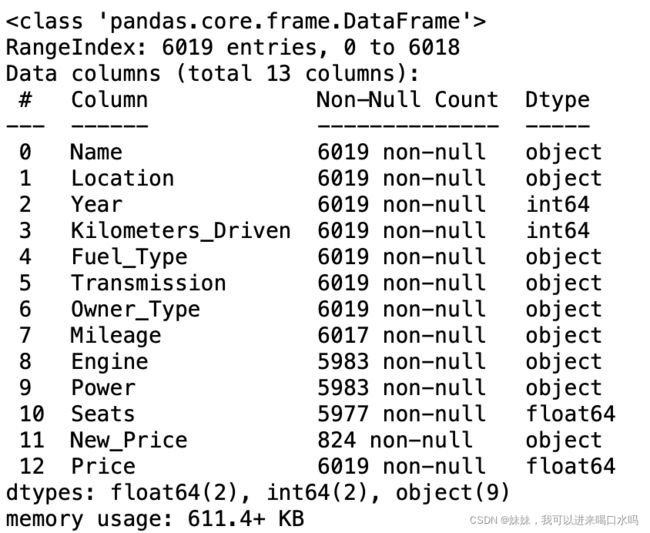

data.info()

data.isnull().sum()

5.2.2 数据类型字段更改

- 去除字段里的单位字符

- 将字符为类别的字段转化为category

- 将汽车的发行年份Year,转化成汽车的年龄Car_Age

- 将汽车Name拆分成公司Company和汽车车型model

data['Mileage']=data['Mileage'].str.rstrip(' kmpl')

data['Mileage']=data['Mileage'].str.rstrip(' km/g')

data['Engine']=data['Engine'].str.rstrip(' CC')

data["Power"]=data['Power'].str.rstrip(' bhp')

data['Power']=data["Power"].replace(regex='null',value=np.nan)

data["Fuel_Type"]=data["Fuel_Type"].astype("category")

data["Transmission"]=data["Transmission"].astype("category")

data["Owner_Type"]=data["Owner_Type"].astype("category")

data["Mileage"]=data["Mileage"].astype("float")

data["Power"]=data["Power"].astype("float")

data["Engine"]=data["Engine"].astype("float")

data['Current_Year']=2022

data['Car_Age']=data['Current_Year']-data['Year']

data['Company']=data['Name'].str.split(' ').str[0]

data['Model']=data['Name'].str.split(' ').str[1]+data['Name'].str.split(' ').str[2]

del data['Current_Year']

del data['Name']

del data['Year']

del data['New_Price']

5.2.3 缺失值处理

mode=data.Mileage.mode()

data['Mileage'].fillna(value=mode[0],inplace=True)

newdata = data.dropna(axis=0)

newdata.info()

5.2.4 数据转化

将特征类型为category,转化成ensemble类型

newdata=pd.get_dummies(newdata)

5.3 划分训练集与测试集

y=newdata[['Price']]

del train['Price']

x=train

X_train, X_test, y_train, y_test = train_test_split(x, y, test_size= 0.2, random_state = random_state)

print(f'Training set--> X_train shape= {X_train.shape}, y_train shape= {y_train.shape}')

print(f'Holdout set--> X_test shape= {X_test.shape}, y_test shape= {y_test.shape}')

![]()

我们将使用均方根误差(RMSE)度量来比较分数。由于这个指标不是现成的,我们将为它创建一个函数。

注:RMSE公制用于以与标签价值相同的计量单位表示损失

models_scores = [] # To store model scores

def rmse(model):

model.fit(X_train, y_train)

y_pred = model.predict(X_test)

return mean_squared_error(y_test, y_pred, squared= False)

5.4 回归模型

5.4.1 Linear Regression

linear_regression = make_pipeline(LinearRegression())

score = rmse(linear_regression)

models_scores.append(['LinearRegression', score])

print(f'LinearRegression Score= {score}')

5.4.2 Lasso Regression

lasso = make_pipeline(RobustScaler(), Lasso(alpha=0.0005, random_state= random_state))

score = rmse(lasso)

models_scores.append(['Lasso', score])

print(f'Lasso Score= {score}')

5.4.3 Elastic Regression

elastic_net = make_pipeline(RobustScaler(), ElasticNet(alpha=0.0005, l1_ratio= .9, random_state= random_state))

score = rmse(elastic_net)

models_scores.append(['ElasticNet', score])

print(f'ElasticNet Score= {score}')

5.4.4 KernelRidge Regression

kernel_ridge= KernelRidge(alpha=0.6, kernel='polynomial', degree=2, coef0=2.5)

score = rmse(kernel_ridge)

models_scores.append(['KernelRidge', score])

print(f'KernelRidge Score= {score}')

5.5 集成模型

5.5.1 Bagging

def bagging_predictions(estimator):

"""

I/P

estimator: The base estimator from which the ensemble is grown.

O/P

br_y_pred: Predictions on test data for the base estimator.

"""

regr = BaggingRegressor(base_estimator=estimator,

n_estimators=10,

max_samples=1.0,

bootstrap=True, # Samples are drawn with replacement

n_jobs= n_jobs,

random_state=random_state).fit(X_train, y_train)

br_y_pred = regr.predict(X_test)

rmse_val = mean_squared_error(y_test, br_y_pred, squared= False) # squared= False > returns Root Mean Square Error

print(f'RMSE for base estimator {regr.base_estimator_} = {rmse_val}\n')

return br_y_pred

predictions = np.column_stack((bagging_predictions(linear_regression),

bagging_predictions(lasso),

bagging_predictions(elastic_net),

bagging_predictions(kernel_ridge)))

print(f"Bagged predictions shape: {predictions.shape}")

y_pred = np.mean(predictions, axis=1)

print("Aggregated predictions (y_pred) shape", y_pred.shape)

rmse_val = mean_squared_error(y_test, y_pred, squared= False) # squared= False > returns Root Mean Square Error

models_scores.append(['Bagging', rmse_val])

print(f'\nBagging RMSE= {rmse_val}')

![]()

5.5.2 Boosting

GradientBoostingRegressor

gradient_boosting_regressor= GradientBoostingRegressor(n_estimators=3000, learning_rate=0.05,

max_depth=4, max_features='sqrt',

min_samples_leaf=15, min_samples_split=10,

loss='huber', random_state = random_state)

score = rmse(gradient_boosting_regressor)

models_scores.append(['GradientBoostingRegressor', score])

print(f'GradientBoostingRegressor Score= {score}')

![]()

XGBRegressor

xgb_regressor= xgb.XGBRegressor(colsample_bytree=0.4603, gamma=0.0468,

learning_rate=0.05, max_depth=3,

min_child_weight=1.7817, n_estimators=2200,

reg_alpha=0.4640, reg_lambda=0.8571,

subsample=0.5213,verbosity=0, nthread = -1, random_state = random_state)

score = rmse(xgb_regressor)

models_scores.append(['XGBRegressor', score])

print(f'XGBRegressor Score= {score}')

LGBMRegressor

lgbm_regressor= lgb.LGBMRegressor(objective='regression',num_leaves=5,

learning_rate=0.05, n_estimators=720,

max_bin = 55, bagging_fraction = 0.8,

bagging_freq = 5, feature_fraction = 0.2319,

feature_fraction_seed=9, bagging_seed=9,

min_data_in_leaf =6, min_sum_hessian_in_leaf = 11,random_state = random_state)

score = rmse(lgbm_regressor)

models_scores.append(['LGBMRegressor', score])

print(f'LGBMRegressor Score= {score}')

5.5.3 Stacking

estimators = [ ('elastic_net', elastic_net), ('kernel_ridge', kernel_ridge),('xgb_regressor', xgb_regressor) ]

stack = StackingRegressor(estimators=estimators, final_estimator= lasso, cv= 5, n_jobs= n_jobs, passthrough = True)

stack.fit(X_train, y_train)

pred = stack.predict(X_test)

rmse_val = mean_squared_error(y_test, pred, squared= False) # squared= False > returns Root Mean Square Error

models_scores.append(['Stacking', rmse_val])

print(f'rmse= {rmse_val}')

汇总一下

pd.DataFrame(models_scores).sort_values(by=[1], ascending=True)