数据挖掘 | 信用卡欺诈预测实战

本篇的数据挖掘实战是以信用卡欺诈的数据集为例,用 Logistic Regression 和 Random Forest 两个分类算法进行预测分析。以下代码是用 Python 3 实现。

首先导入要用到的 Python 包。

import pandas as pd

import numpy as np

import seaborn as sns

import matplotlib.pyplot as plt

import itertools

from sklearn.linear_model import LogisticRegression

from sklearn.model_selection import train_test_split

from sklearn.metrics import confusion_matrix, precision_recall_curve

from sklearn.metrics import roc_curve, auc

from sklearn.preprocessing import StandardScaler

读入数据,数据类型是 .csv 文件。

data = pd.read_csv('./creditcard.csv')

数据初探索

输出 data 的前 5 行,先直观地看一下数据的样子。

data.head(5)

由于属性太多,该图未截取完整。

继续对数据进行探索。

print(data.shape) # 输出行数和列数(284807, 31)

data.columns.tolist() # 显现数据的所有列名称

print(data.describe()) # 对数据的描述性统计

接下来绘制类别的分布,通过直方图可以直观地观察到有多少类,以及每个类的分布。

plt.figure()

ax = sns.countplot(x = 'Class',data = data)

plt.title('class distribution')

plt.show()

观察直方图,我们会发现这是一个二分类的数据集,并且数据分布极为不平衡。毕竟在信用卡违约贷款中,属于欺诈的交易还是极少数的。

具体计算一下总交易数,以及属于欺诈的交易数。

num = len(data)

num_fraud = len(data[data['Class'] == 1])

print("总交易笔数",num)

print("诈骗交易次数", num_fraud)`在这里插入代码片`

print("诈骗交易比例:{:.6f}".format(num_fraud/num))

# 输出结果

总交易笔数 284807

诈骗交易次数 492

诈骗交易比例:0.001727

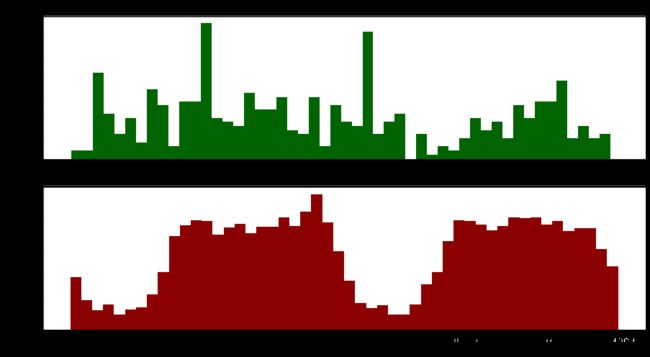

可视化一下在不同的时间点下,正常与欺诈的交易次数的分布。

f, (ax1, ax2) = plt.subplots(2, 1, sharex=True, figsize=(15,8))

bins = 50

ax1.hist(data.Time[data.Class == 1], bins = bins, color = 'darkgreen')

ax1.set_title('Fraudulent transactions')

ax2.hist(data.Time[data.Class == 0], bins = bins, color = 'darkred')

ax2.set_title('Normal transactions')

plt.xlabel('Time')

plt.ylabel('Number of transactions')

plt.show()

数据预处理和特征选择

对Amount进行数据规划范处理,标准化

data['Amount_Norm'] = StandardScaler().fit_transform(data['Amount'].values.reshape(-1,1))

特征选择

y = np.array(data['Class'].tolist())

data = data.drop(['Time','Amount','Class'],axis=1)

X = np.array(data)

建模并评估

逻辑回归算法

train_x, test_x, train_y, test_y = train_test_split(X, y, test_size = 0.1, random_state = 22)

clf = LogisticRegression()

clf.fit(train_x, train_y)

predict_y = clf.predict(test_x)

计算混淆矩阵

cm = confusion_matrix(test_y, predict_y)

# 结果

[[28434 6]

[ 16 25]]

# 准确率为:0.9992275552122467

可视化混淆矩阵

def plot_confusion_matrix(cm, classes, normalize = False, title = 'Confusion matrix"', cmap = plt.cm.Blues) :

plt.figure()

plt.imshow(cm, interpolation = 'nearest', cmap = cmap)

plt.title(title)

plt.colorbar()

tick_marks = np.arange(len(classes))

plt.xticks(tick_marks, classes, rotation = 0)

plt.yticks(tick_marks, classes)

thresh = cm.max() / 2.

for i, j in itertools.product(range(cm.shape[0]), range(cm.shape[1])) :

plt.text(j, i, cm[i, j],

horizontalalignment = 'center',

color = 'white' if cm[i, j] > thresh else 'black')

plt.tight_layout()

plt.ylabel('True label')

plt.xlabel('Predicted label')

plt.show()

class_names = [0,1]

plot_confusion_matrix(cm, classes=class_names,title = 'LR Confusion Matrix')

显示模型评估结果

def show_metrics():

tp = cm[1,1]

fn = cm[1,0]

fp = cm[0,1]

tn = cm[0,0]

print('精确率: {:.3f}'.format(tp/(tp+fp)))

print('召回率: {:.3f}'.format(tp/(tp+fn)))

print('F1值: {:.3f}'.format(2*(((tp/(tp+fp))*(tp/(tp+fn)))/((tp/(tp+fp))+(tp/(tp+fn))))))

show_metrics()

# 结果

精确率: 0.806

召回率: 0.610

F1值: 0.694

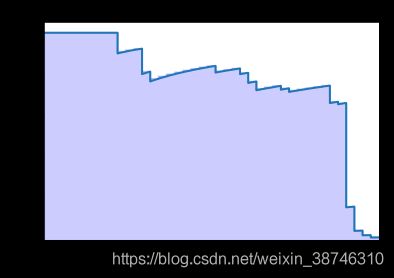

绘制精确率-召回率曲线

def plot_precision_recall():

plt.step(recall, precision, color = 'b', alpha = 0.2, where = 'post')

plt.fill_between(recall, precision, step ='post', alpha = 0.2, color = 'b')

plt.plot(recall, precision, linewidth=2)

plt.xlim([0.0,1])

plt.ylim([0.0,1.05])

plt.xlabel('Recall Rate')

plt.ylabel('Precision Rate')

plt.title('Recall-Precision Curve')

plt.show()

precision, recall, thresholds = precision_recall_curve(test_y, score_y)

plot_precision_recall()

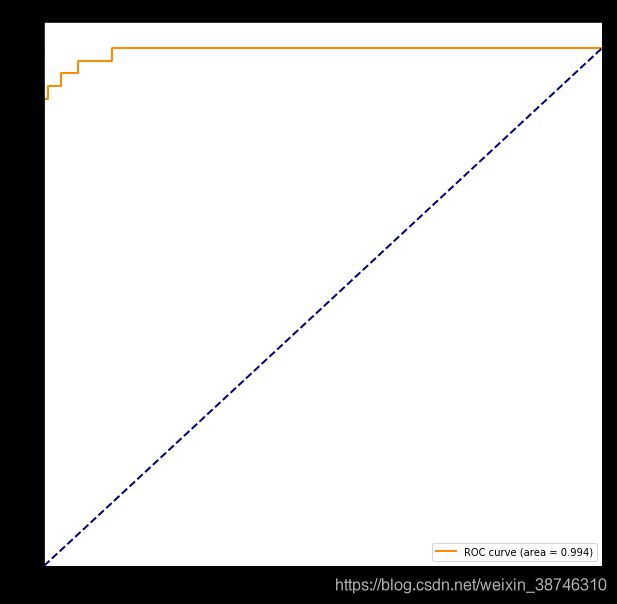

绘制 AUC 曲线

def auc_curve(y,prob):

fpr,tpr,threshold = roc_curve(y,prob) ###计算真正率和假正率

roc_auc = auc(fpr,tpr) ###计算auc的值

plt.figure()

lw = 2

plt.figure(figsize=(10,10))

plt.plot(fpr, tpr, color='darkorange',

lw=lw, label='ROC curve (area = %0.3f)' % roc_auc) ###假正率为横坐标,真正率为纵坐标做曲线

plt.plot([0, 1], [0, 1], color='navy', lw=lw, linestyle='--')

plt.xlim([0.0, 1.0])

plt.ylim([0.0, 1.05])

plt.xlabel('False Positive Rate')

plt.ylabel('True Positive Rate')

plt.title('Receiver operating characteristic example')

plt.legend(loc="lower right")

plt.show()

auc_curve(test_y, score_y)

随机森林

接下来用随机森林进行预测

from sklearn.ensemble import RandomForestClassifier

clf = RandomForestClassifier()

clf.fit(train_x, train_y)

predict_y = clf.predict(test_x)

acc = clf.score(test_x, test_y)

print(acc)

# 0.9997191109862715

混淆矩阵为:

[[28438 2]

[ 6 35]]

召回率、准确率和F1值为:

精确率: 0.946

召回率: 0.854

F1值: 0.897

召回率-准确率曲线为:

AUC曲线:

总结:

- 采用 LR 和 RFC 都没有经过调参,采用的是默认参数,经过调参后表现应该会更好一些。

- 在没有经过调参的两个算法中,Random Forest 明显是表现地更佳一些。

- 用我的电脑在训练数据的时候,发现 Logistic Regression 会快好多。