kaggle实战:极度不均衡样本下的信用卡数据分析

公众号:尤而小屋

作者:Peter

编辑:Peter

大家好,我是Peter~

今天给大家带来一篇新的kaggle文章:极度不均衡的信用卡数据分析,主要内容包含:

- 理解数据:通过直方图、箱型图等辅助理解数据分布

- 预处理:归一化和分布情况;数据分割

- 随机采样:上采样和下采样,主要是欠采样(下采样)

- 异常检测:如何从数据中找到异常点,并且进行删除

- 数据建模:利用逻辑回归和神经网络进行建模分析

- 模型评价:分类模型的多种评价指标

原notebook地址为:https://www.kaggle.com/code/janiobachmann/credit-fraud-dealing-with-imbalanced-datasets/notebook

所谓的【非均衡】:信用卡数据中欺诈和非欺诈的比例是不均衡的,肯定是非欺诈的比例占据绝大多数。本文提供一种方法:如何处理这种极度不均衡的数据

导入库

导入各种库和包:绘图、特征工程、降维、分类模型、评价指标相关等

基本信息

读取数据,查看基本信息

数据的形状如下:

In [3]:

df.shape

Out[3]:

(284807, 31)

In [4]:

# 缺失值的最大值

df.isnull().sum().max()

Out[4]:

0

结果表明是没有缺失值的。

下面是查看数据中字段的相关类型,我们发现有30个float64类型,1个int64类型

In [5]:

pd.value_counts(df.dtypes)

Out[5]:

float64 30

int64 1

dtype: int64

In [6]:

columns = df.columns

columns

Out[6]:

Index(['Time', 'V1', 'V2', 'V3', 'V4', 'V5', 'V6', 'V7', 'V8', 'V9', 'V10',

'V11', 'V12', 'V13', 'V14', 'V15', 'V16', 'V17', 'V18', 'V19', 'V20',

'V21', 'V22', 'V23', 'V24', 'V25', 'V26', 'V27', 'V28', 'Amount',

'Class'],

dtype='object')

查看数据的统计信息:

df.describe()

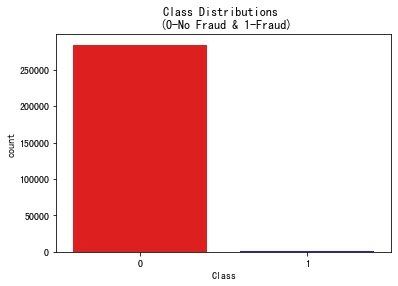

正负样本不均衡

In [8]:

df["Class"].value_counts(normalize=True)

Out[8]:

0 0.998273 # 不欺诈

1 0.001727 # 欺诈

Name: Class, dtype: float64

我们发现属于0类的样本远高于属于1的样本,非常地不均衡。这就是本文重点关注的问题。

In [9]:

# 绘图

colors = ["red", "blue"]

sns.countplot("Class", data=df, palette=colors)

plt.title("Class Distributions \n (0-No Fraud & 1-Fraud)")

plt.show()

通过柱状图也能够明显观察到非欺诈-0 和 欺诈-1的比例是极度不均衡的。

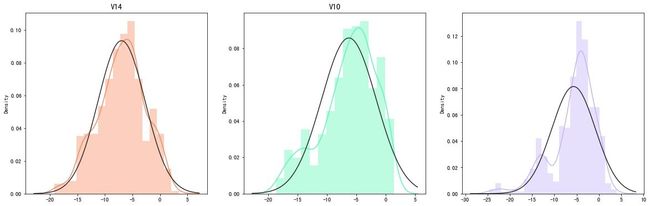

查看特征分布

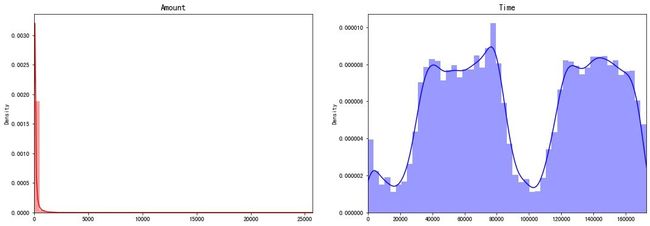

部分特征的分布,发现存在偏态状况:

直方图分布

In [10]:

fig, ax = plt.subplots(1,2,figsize=(18,6))

amount_val = df["Amount"].values

time_val = df["Time"].values

sns.distplot(amount_val, ax=ax[0], color="r")

ax[0].set_title("Amount", fontsize=14)

ax[0].set_xlim([min(amount_val), max(amount_val)]) # 设置范围

sns.distplot(time_val, ax=ax[1], color="b")

ax[1].set_title("Time", fontsize=14)

ax[1].set_xlim([min(time_val), max(time_val)]) # 设置范围

plt.show()

观察两个字段Amount和Time在不同取值下的分布情况,发现:

- Amount的偏态现象严重,极大多数的数据集中在左侧

- Time中,数据主要集中在两个阶段

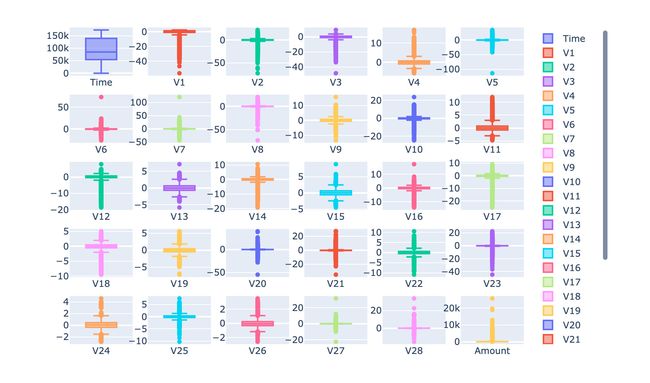

特征分布箱型图

查看每个特征取值的箱型图:

数据预处理

数据缩放和分布

针对Amount和Time字段的归一化操作。原始数据中的其他字段已经进行了归一化的操作。

- StandardScaler:将数据减去均值除以标准差

- RobustScaler:如果数据有离群点,有对数据中心化和数据的缩放鲁棒性更强的参数

In [13]:

from sklearn.preprocessing import StandardScaler, RobustScaler

# ss = StandardScaler()

rs = RobustScaler()

# 好方法

df['scaled_amount'] = rs.fit_transform(df['Amount'].values.reshape(-1,1))

df['scaled_time'] = rs.fit_transform(df['Time'].values.reshape(-1,1))

In [14]:

删除原始字段,使用归一化后的字段和数据

df['Amount'].values.reshape(-1,1) # 个人添加

技巧1:新字段位置

将新生成的字段放在最前面

# 把两个缩放的字段放在最前面

# 1、单独提出来

scaled_amount = df['scaled_amount']

scaled_time = df['scaled_time']

# 2、删除原字段信息

df.drop(['scaled_amount', 'scaled_time'], axis=1, inplace=True)

# 3、插入

df.insert(0, 'scaled_amount', scaled_amount)

df.insert(1, 'scaled_time', scaled_time)

分割数据(基于原DataFrame)

在开始进行随机欠采样之前,我们需要将原始数据进行分割。

尽管我们会对数据进行欠采样和上采样,但是我们希望在测试的时候,仍然是使用原始的数据集(原来的数据顺序)

In [18]:

from sklearn.model_selection import train_test_split

from sklearn.model_selection import StratifiedShuffleSplit

查看Class中0-no fraud和1-fraud的比例:

In [19]:

df["Class"].value_counts(normalize=True)

Out[19]:

0 0.998273

1 0.001727

Name: Class, dtype: float64

生成特征数据集X和标签数据y:

In [20]:

X = df.drop("Class", axis=1)

y = df["Class"]

In [21]:

技巧2:生成随机索引

sfk = StratifiedKFold(

n_splits=5, # 生成5份

random_state=None,

shuffle=False)

for train_index, test_index in sfk.split(X,y):

# 随机生成的index

print(train_index)

print("------------")

print(test_index)

# 根据随机生成的索引再生成数据

original_X_train = X.iloc[train_index]

original_X_test = X.iloc[test_index]

original_y_train = y.iloc[train_index]

original_y_test = y.iloc[test_index]

[ 30473 30496 31002 ... 284804 284805 284806]

------------

[ 0 1 2 ... 57017 57018 57019]

[ 0 1 2 ... 284804 284805 284806]

------------

[ 30473 30496 31002 ... 113964 113965 113966]

[ 0 1 2 ... 284804 284805 284806]

------------

[ 81609 82400 83053 ... 170946 170947 170948]

[ 0 1 2 ... 284804 284805 284806]

------------

[150654 150660 150661 ... 227866 227867 227868]

[ 0 1 2 ... 227866 227867 227868]

------------

[212516 212644 213092 ... 284804 284805 284806]

将生成的数据转成numpy数组:

In [22]:

original_Xtrain = original_X_train.values

original_Xtest = original_X_test.values

original_ytrain = original_y_train.values

original_ytest = original_y_test.values

查看训练集 original_ytrain 和 original_ytest 的唯一值以及每个唯一值所占的比例:

In [23]:

技巧3:数据唯一值及比例

# 训练集

# 针对的是numpy数组

train_unique_label, train_counts_label = np.unique(original_ytrain, return_counts=True)

# 测试集

test_unique_label, test_counts_label = np.unique(original_ytest, return_counts=True)

In [24]:

print(train_counts_label / len(original_ytrain))

print(test_counts_label / len(original_ytest))

[0.99827076 0.00172924]

[0.99827952 0.00172048]

欠采样

原理

欠采样也称之为下采样,主要是通过删除原数据中类别较多的数据,从而和类别少的数据达到平衡,以免造成模型的过拟合。

步骤

- 确定数据不平衡度是多少:通过value_counts()来统计,查看每个类别的数量和占比

- 在本例中一旦我们确定了fraud的数量,我们就需要将no-fraud的数量采样和其相同,形成50%:50%

- 实施采样之后,随机打乱采样的子样本

缺点

下采样会造成数据信息的缺失。比如原数据中no-fraud有284315条数据,但是经过欠采样只有492,大量的数据被放弃了。

实施采样

取出欺诈的数据,同时从非欺诈中取出相同长度的数据:

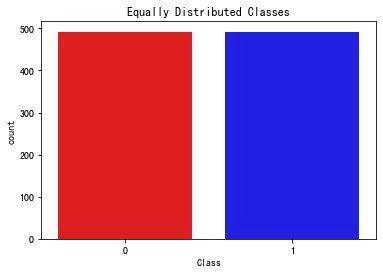

均匀分布

现在我们发现样本是均匀的:

In [28]:

# 显示数量

new_df["Class"].value_counts()

Out[28]:

1 492

0 492

Name: Class, dtype: int64

In [29]:

# 显示比例

new_df["Class"].value_counts(normalize=True)

Out[29]:

1 0.5

0 0.5

Name: Class, dtype: float64

In [30]:

当我们再次查看数据分布的时候发现:已经是均匀分布了

sns.countplot("Class",

data=new_df,

palette=colors)

plt.title("Equally Distributed Classes", fontsize=12)

plt.show()

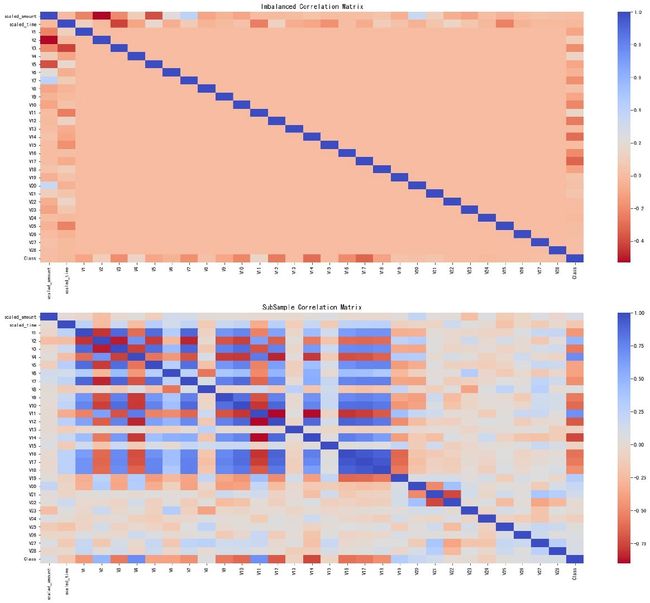

相关性分析

相关性分析主要是通过相关系数矩阵来实现的。下面绘制基于原始数据和欠采样数据的相关系数矩阵图:

系数矩阵热力图

In [31]:

f, (ax1, ax2) = plt.subplots(2,1,figsize=(24, 20))

# 原始数据df

corr = df.corr()

sns.heatmap(corr, cmap="coolwarm_r",annot_kws={"size":20}, ax=ax1)

ax1.set_title("Imbalanced Correlation Matrix", fontsize=14)

# 欠采样数据new_df

new_corr = new_df.corr()

sns.heatmap(new_corr, cmap="coolwarm_r",annot_kws={"size":20}, ax=ax2)

ax2.set_title("SubSample Correlation Matrix", fontsize=14)

plt.show()

小结:

- 正相关:特征V2、V4、V11、V19是正相关的。值越大,结果越可能出现fraud

- 负相关:特征V17, V14, V12 和 V10 是负相关的;值越小,结果越可能出现fraud

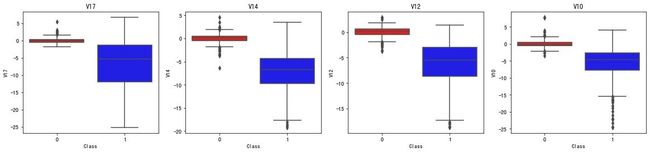

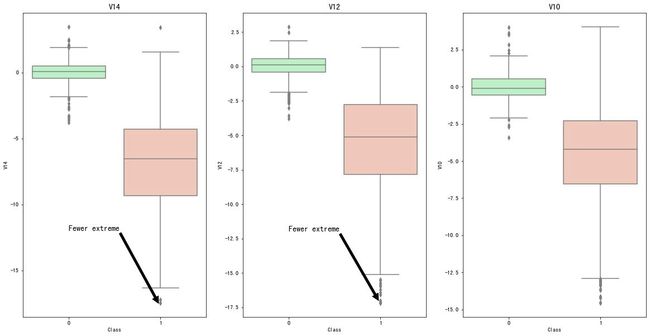

箱型图

In [32]:

负相关的特征箱型图

# 负相关的数据

# 生成4个子图

f, axes = plt.subplots(ncols=4, figsize=(20,4))

sns.boxplot(x="Class", # 分类的类别 0-1

y="V17", # 选择某个字段进行绘图

data=new_df, # 绘图的数据

palette=colors,

ax=axes[0]) # 选择某个ax来绘图

axes[0].set_title('V17') # 子图标题

sns.boxplot(x="Class",

y="V14",

data=new_df,

palette=colors,

ax=axes[1])

axes[1].set_title('V14')

sns.boxplot(x="Class",

y="V12",

data=new_df,

palette=colors,

ax=axes[2])

axes[2].set_title('V12')

sns.boxplot(x="Class",

y="V10",

data=new_df,

palette=colors,

ax=axes[3])

axes[3].set_title('V10')

plt.show()

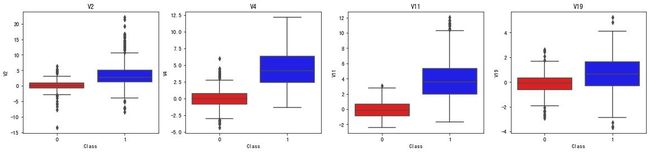

正相关特征的箱型图:

# 正相关

f, axes = plt.subplots(ncols=4, figsize=(20,4))

sns.boxplot(x="Class",

y="V2",

data=new_df,

palette=colors,

ax=axes[0])

axes[0].set_title('V2')

sns.boxplot(x="Class",

y="V4",

data=new_df,

palette=colors,

ax=axes[1])

axes[1].set_title('V4')

sns.boxplot(x="Class",

y="V11",

data=new_df,

palette=colors,

ax=axes[2])

axes[2].set_title('V11')

sns.boxplot(x="Class",

y="V19",

data=new_df,

palette=colors,

ax=axes[3])

axes[3].set_title('V19')

plt.show()

异常检测

目的

异常检测的目的主要是:发现数据中的离群点来进行删除。

方法

- IQR:我们通过第75个百分位和第25个百分位之间的差异来计算。我们的目标是创建一个超过第75和 25 个百分位的阈值,以防某些实例超过此阈值,如果超过阈值该实例将被删除。

- 箱型图boxplot:除了很容易看到第 25 和第 75 个百分位数(正方形的两端)之外,还很容易看到极端异常值(超出下限和上限的点)

异常值去除权衡

在通过四分位法删除异常值的时候,我们通过将一个数字(例如1.5)乘以(四分位距)来确定阈值。该阈值越高,检测到的异常值越少,反之检测到的异常值越多。这个比例(例如1.5)我们可以在实际进行控制

特征分布-直方图

In [34]:

技巧4:删除离群点

删除3个特征下的离群点,以V12为例:

In [35]:

第一步先确定上下分位数的值:

# 数组

v12_fraud = new_df["V12"].loc[new_df["Class"] == 1]

# 25%和75%分位数

q1, q3 = v12_fraud.quantile(0.25), v12_fraud.quantile(0.75)

iqr = q3 - q1

In [36]:

# 确定上下限

v12_cut_off = iqr * 1.5

v12_lower = q1 - v12_cut_off

v12_upper = q3 + v12_cut_off

print(v12_lower)

print(v12_upper)

-17.25930926645337

5.597044719256134

In [37]:

找出满足要求的离群点的数据

# 确定离群点

outliers = [x for x in v12_fraud if x < v12_lower or x > v12_upper]

print(outliers)

print("------------")

print("离群点数量:",len(outliers))

[-17.6316063138707, -17.7691434633638, -18.6837146333443,

-18.5536970096458, -18.0475965708216, -18.4311310279993]

------------

离群点数量: 6

对单个列字段的数据执行下面删除离群点的操作:

In [38]:

# 技巧:如何删除异常值

new_df = new_df.drop(new_df[(new_df["V12"] > v12_upper) | (new_df["V12"] < v12_lower)].index)

new_df

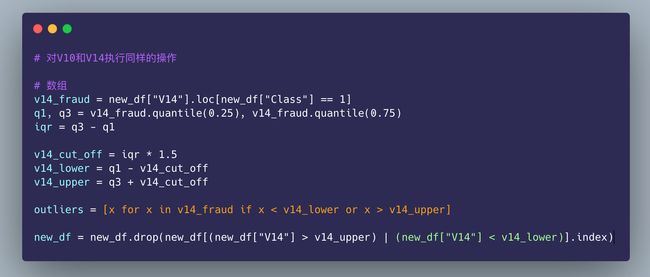

对其他的特征执行相同的操作:

可以看到:欠采样之后的数据原本是984,现在变成了978条数据,删除了6个离群点的数据

In [39]:

In [40]:

# 对V10和V14执行同样的操作

# 数组

v10_fraud = new_df["V10"].loc[new_df["Class"] == 1]

q1, q3 = v10_fraud.quantile(0.25), v10_fraud.quantile(0.75)

iqr = q3 - q1

v10_cut_off = iqr * 1.5

v10_lower = q1 - v10_cut_off

v10_upper = q3 + v10_cut_off

outliers = [x for x in v10_fraud if x < v10_lower or x > v10_upper]

new_df = new_df.drop(new_df[(new_df["V10"] > v10_upper) | (new_df["V10"] < v10_lower)].index)

查看删除了异常点后的数据:

In [42]:

f, (ax1, ax2, ax3) = plt.subplots(1,3,figsize=(20,10))

colors = ['#B3F9C5', '#f9c5b3']

sns.boxplot(x="Class", # 分类字段

y="V14", # y轴的取值

data=new_df, # 数据框

ax=ax1, # 子图

palette=colors)

ax1.set_title("V14", fontsize=14) # 标题

ax1.annotate("Fewer extreme", # 注解

xy=(0.98,-17.5),

xytext=(0,-12),

arrowprops=dict(facecolor="black"),

fontsize=14)

sns.boxplot(x="Class", y="V12", data=new_df, ax=ax2, palette=colors)

ax2.set_title("V12", fontsize=14)

ax2.annotate("Fewer extreme",

xy=(0.98,-17),

xytext=(0,-12),

arrowprops=dict(facecolor="black"),

fontsize=14)

sns.boxplot(x="Class", y="V10", data=new_df, ax=ax3, palette=colors)

ax3.set_title("V10", fontsize=14)

ax3.annotate("Fewer extreme", # 注释名称

xy=(0.98,-16.5), # 位置

xytext=(0,-12), # 注释文本的坐标点,二维元组,默认xy

arrowprops=dict(facecolor="black"), # 箭头颜色

fontsize=14)

plt.show()

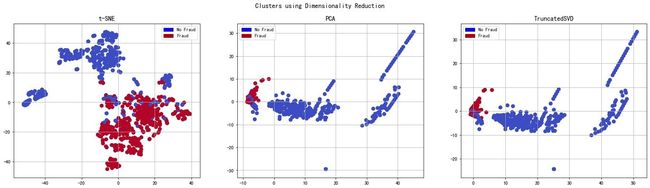

降维和聚类

理解t-SNE

详细地址:https://www.youtube.com/watch?v=NEaUSP4YerM

欠采样数据降维

对3种不同方法实施欠采样:

In [43]:

X = new_df.drop("Class", axis=1)

y = new_df["Class"]

# t-SNE降维

t0 = time.time()

X_reduced_tsne = TSNE(n_components=2,

random_state=42).fit_transform(X.values)

t1 = time.time()

print("T-SNE: ", (t1 - t0))

T-SNE: 5.750015020370483

In [44]:

# PCA降维

t0 = time.time()

X_reduced_pca = PCA(n_components=2,

random_state=42).fit_transform(X.values)

t1 = time.time()

print("PCA: ", (t1 - t0))

PCA: 0.02214193344116211

In [45]:

# TruncatedSVD降维

t0 = time.time()

X_reduced_svd = TruncatedSVD(n_components=2,

algorithm="randomized",

random_state=42).fit_transform(X.values)

t1 = time.time()

print("TruncatedSVD: ", (t1 - t0))

TruncatedSVD: 0.01066279411315918

绘图

In [46]:

f, (ax1, ax2, ax3) = plt.subplots(1,3,figsize=(24,6))

# 标题设置

f.suptitle("Clusters using Dimensionality Reduction", fontsize=14)

blue_patch = mpatches.Patch(color="#0A0AFF", label="No Fraud")

red_patch = mpatches.Patch(color="#AF0000", label="Fraud")

# t-SNE

ax1.scatter(X_reduced_tsne[:,0],

X_reduced_tsne[:,1],

c=(y==0),

cmap="coolwarm",

label="No Fraud",

linewidths=2

)

ax1.scatter(X_reduced_tsne[:,0],

X_reduced_tsne[:,1],

c=(y==0),

cmap="coolwarm",

label="Fraud",

linewidths=2

)

ax1.set_title("t-SNE", fontsize=14) # 子图标题设置

ax1.grid(True) # 设置网格

ax1.legend(handles=[blue_patch,red_patch]) # 设置图例

# PCA

ax2.scatter(X_reduced_pca[:,0],

X_reduced_pca[:,1],

c=(y==0),

cmap="coolwarm",

label="No Fraud",

linewidths=2

)

ax2.scatter(X_reduced_pca[:,0],

X_reduced_pca[:,1],

c=(y==0),

cmap="coolwarm",

label="Fraud",

linewidths=2

)

ax2.set_title("PCA", fontsize=14) # 标题设置

ax2.grid(True) # 设置网格

ax2.legend(handles=[blue_patch,red_patch])

# TruncatedSVD

ax3.scatter(X_reduced_svd[:,0],

X_reduced_svd[:,1],

c=(y==0),

cmap="coolwarm",

label="No Fraud",

linewidths=2

)

ax3.scatter(X_reduced_svd[:,0],

X_reduced_svd[:,1],

c=(y==0),

cmap="coolwarm",

label="Fraud",

linewidths=2

)

ax3.set_title("TruncatedSVD", fontsize=14) # 标题设置

ax3.grid(True) # 设置网格

ax3.legend(handles=[blue_patch,red_patch])

plt.show()

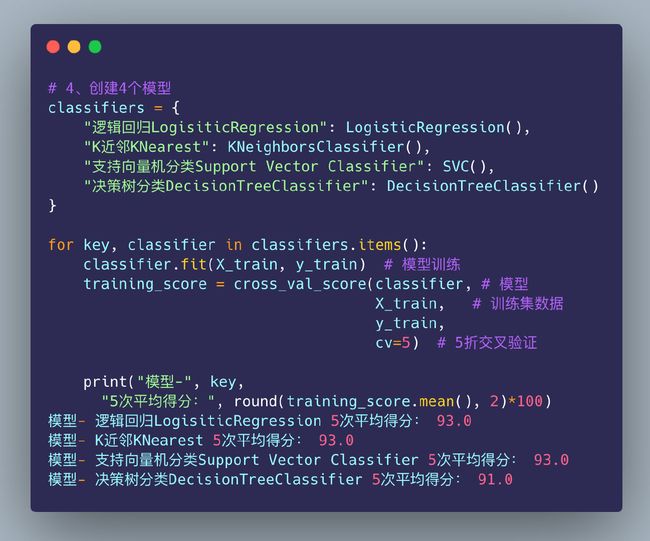

基于欠采样的分类建模

4个分类模型

采用4个不同模型的分类来训练数据,看哪个模型在欺诈数据上表现的更好。首先需要对数据进行划分:训练集和测试集

In [47]:

# 1、特征和标签数据

X = new_df.drop("Class", axis=1)

y = new_df["Class"]

In [48]:

原始数据的划分:

# 2、数据已经归一化,直接切分

from sklearn.model_selection import train_test_split

# 8-2的比例

X_train, X_test, y_train, y_test = train_test_split(X,y,test_size=0.2,random_state=44)

In [49]:

# 3、将数据转成数组,然后传给模型

X_train = X_train.values

X_test = X_test.values

y_train = y_train.values

y_test = y_test.values

In [50]:

对划分的原始数据实施交叉验证和计算得分:

网格搜索

针对不同测模型实施网格搜索,寻找最优参数

In [51]:

from sklearn.model_selection import GridSearchCV

# 逻辑回归

lr_params = {"penalty":["l1", "l2"],

"C": [0.001, 0.01, 0.1, 1, 10, 100, 1000]

}

grid_lr = GridSearchCV(LogisticRegression(), lr_params)

grid_lr.fit(X_train, y_train)

# 最好的参数组合

best_para_lr = grid_lr.best_estimator_

best_para_lr

Out[51]:

LogisticRegression(C=0.1)

In [52]:

# k近邻

knn_params = {"n_neighbors": list(range(2,5,1)),

"algorithm":["auto","ball_tree","kd_tree","brute"]

}

grid_knn = GridSearchCV(KNeighborsClassifier(), knn_params)

grid_knn.fit(X_train, y_train)

# 最好的参数组合

best_para_knn = grid_knn.best_estimator_

best_para_knn

Out[52]:

KNeighborsClassifier(n_neighbors=2)

In [53]:

# 支持向量机分类

svc_params = {"C":[0.5, 0.7, 0.9, 1],

"kernel":["rbf","poly","sigmoid","linear"]

}

grid_svc = GridSearchCV(SVC(), svc_params)

grid_svc.fit(X_train, y_train)

best_para_svc = grid_svc.best_estimator_

best_para_svc

Out[53]:

SVC(C=0.9, kernel='linear')

In [54]:

# 决策树

dt_params = {"criterion":["gini","entropy"],

"max_depth":list(range(2, 5, 1)),

"min_samples_leaf": list(range(5,7,1))

}

grid_dt = GridSearchCV(DecisionTreeClassifier(), dt_params)

grid_dt.fit(X_train, y_train)

best_para_dt = grid_dt.best_estimator_

best_para_dt

Out[54]:

DecisionTreeClassifier(max_depth=3, min_samples_leaf=5)

重新训练并评分

基于最优参数重新计算得分:

In [55]:

lr_score = cross_val_score(best_para_lr, X_train, y_train,cv=5)

print("逻辑回归交叉验证得分:", round(lr_score.mean() * 100, 2).astype(str) + "%")

逻辑回归交叉验证得分: 93.63%

In [56]:

knn_score = cross_val_score(best_para_knn, X_train, y_train,cv=5)

print("KNN交叉验证得分:", round(knn_score.mean() * 100, 2).astype(str) + "%")

KNN交叉验证得分: 93.37%

In [57]:

svc_score = cross_val_score(best_para_svc, X_train, y_train,cv=5)

print("SVC交叉验证得分:", round(svc_score.mean() * 100, 2).astype(str) + "%")

SVC交叉验证得分: 93.5%

In [58]:

dt_score = cross_val_score(best_para_dt, X_train, y_train,cv=5)

print("决策树交叉验证得分:", round(dt_score.mean() * 100, 2).astype(str) + "%")

决策树交叉验证得分: 93.24%

小结:通过不同模型的交叉验证得分我们发现,逻辑回归模型是最高的

基于欠采样数据的交叉验证

主要是基于Near-Miss算法来实现欠采样:

- Near-miss-1:选择到最近的三个样本平均距离最小的多数类样本

- Near-miss-2:选择到最远的三个样本平均距离最小的多数类样本

- Near-miss-3:为每个少数类样本选择给定数目的最近多数类样本

- 最远距离:选择到最近的三个样本平均距离最大的多样类样本

In [59]:

undersample_X = df.drop("Class", axis=1)

undersample_y = df["Class"]

sfk = StratifiedKFold(

n_splits=5, # 5次交叉验证

random_state=None,

shuffle=False)

for train_index , test_index in sfk.split(undersample_X,undersample_y):

# 每次随机生成的验证集和测试集的索引号

# print("Train: ", train_index)

# print("Test: ", test_index)

undersample_Xtrain = undersample_X.iloc[train_index] # 根据索引号来确定数据

undersample_Xtest = undersample_X.iloc[test_index]

undersample_ytrain = undersample_y.iloc[train_index]

undersample_ytest = undersample_y.iloc[test_index]

# 数据转成numpy数组

undersample_Xtrain = undersample_Xtrain.values

undersample_Xtest = undersample_Xtest.values

undersample_ytrain = undersample_ytrain.values

undersample_ytest = undersample_ytest.values

# 5个评价指标

undersample_accuracy = []

undersample_precision = []

undersample_recall = []

undersample_f1 = []

undersample_auc = []

使用近邻缺失Near-Miss算法来查看数据分布:

In [60]:

undersample_X = df.drop("Class", axis=1)

undersample_y = df["Class"]

X_nearmiss, y_nearmiss = NearMiss().fit_resample(undersample_X.values, undersample_y.values)

print("NearMiss Label Distributions: {}", format(Counter(y_nearmiss)))

NearMiss Label Distributions: {} Counter({0: 492, 1: 492})

以网格搜索过后的逻辑回归模型来实施交叉验证:

In [61]:

for train, test in sfk.split(undersample_Xtrain, undersample_ytrain):

undersample_pipeline = imbalanced_make_pipeline(NearMiss(sampling_strategy="majority"), best_para_lr)

# 模型训练:传入训练X-y

undersample_model = undersample_pipeline.fit(undersample_Xtrain[train], undersample_ytrain[train])

# 对测试集预测-Xtrain

undersample_prediction = undersample_model.predict(undersample_Xtrain[test])

# y_test真实值和预测值的评分

undersample_accuracy.append(undersample_pipeline.score(original_Xtrain[test], original_ytrain[test]))

undersample_precision.append(precision_score(original_ytrain[test], undersample_prediction))

undersample_recall.append(recall_score(original_ytrain[test], undersample_prediction))

undersample_f1.append(f1_score(original_ytrain[test], undersample_prediction))

undersample_auc.append(roc_auc_score(original_ytrain[test], undersample_prediction))

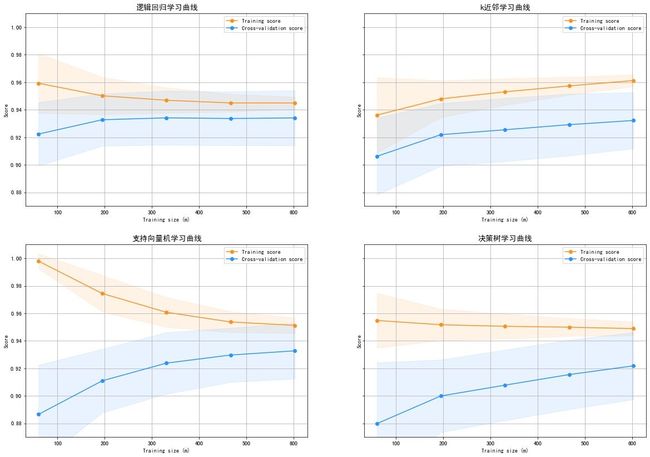

绘制学习曲线

In [62]:

from sklearn.model_selection import ShuffleSplit, learning_curve

In [63]:

def plot_learning_curve(est1,est2,est3,est4,X,y,ylim=None,cv=None,n_jobs=1,train_sizes=np.linspace(0.1, 1, 5)):

f, ((ax1,ax2), (ax3,ax4)) = plt.subplots(2,2,figsize=(20,14), sharey=True)

if ylim is not None:

plt.ylim(*ylim)

# 模型1

train_sizes, train_scores, test_scores = learning_curve(

est1, X, y, cv=cv, n_jobs=n_jobs, train_sizes=train_sizes)

train_scores_mean = np.mean(train_scores, axis=1) # 训练集的均值和方差

train_scores_std = np.std(train_scores, axis=1)

test_scores_mean = np.mean(test_scores, axis=1) # 测试集的均值和方差

test_scores_std = np.std(test_scores, axis=1)

ax1.fill_between(train_sizes, train_scores_mean - train_scores_std, # 填充区域的设置

train_scores_mean + train_scores_std, alpha=0.1,

color="#ff9124")

ax1.fill_between(train_sizes, test_scores_mean - test_scores_std,

test_scores_mean + test_scores_std, alpha=0.1,

color="#2492ff")

ax1.plot(train_sizes, train_scores_mean,

'o-', color="#ff9124",

label="Training score") # 绘制训练集得分

ax1.plot(train_sizes, test_scores_mean,

'o-', color="#2492ff",

label="Cross-validation score") # 绘制交叉验证得分

ax1.set_title("逻辑回归学习曲线", fontsize=14)

ax1.set_xlabel('Training size (m)') # 两个轴的标题

ax1.set_ylabel('Score')

ax1.grid(True) # 网格显示

ax1.legend(loc="best") # 图例位置

# 模型2-knn

train_sizes, train_scores, test_scores = learning_curve(

est2, X, y, cv=cv, n_jobs=n_jobs, train_sizes=train_sizes)

train_scores_mean = np.mean(train_scores, axis=1)

train_scores_std = np.std(train_scores, axis=1)

test_scores_mean = np.mean(test_scores, axis=1)

test_scores_std = np.std(test_scores, axis=1)

ax2.fill_between(train_sizes, train_scores_mean - train_scores_std,

train_scores_mean + train_scores_std, alpha=0.1,

color="#ff9124")

ax2.fill_between(train_sizes, test_scores_mean - test_scores_std,

test_scores_mean + test_scores_std, alpha=0.1, color="#2492ff")

ax2.plot(train_sizes, train_scores_mean, 'o-', color="#ff9124",

label="Training score")

ax2.plot(train_sizes, test_scores_mean, 'o-', color="#2492ff",

label="Cross-validation score")

ax2.set_title("k近邻学习曲线", fontsize=14)

ax2.set_xlabel('Training size (m)')

ax2.set_ylabel('Score')

ax2.grid(True)

ax2.legend(loc="best")

# 模型3-支持向量机

train_sizes, train_scores, test_scores = learning_curve(

est3, X, y, cv=cv, n_jobs=n_jobs, train_sizes=train_sizes)

train_scores_mean = np.mean(train_scores, axis=1)

train_scores_std = np.std(train_scores, axis=1)

test_scores_mean = np.mean(test_scores, axis=1)

test_scores_std = np.std(test_scores, axis=1)

ax3.fill_between(train_sizes, train_scores_mean - train_scores_std,

train_scores_mean + train_scores_std, alpha=0.1,

color="#ff9124")

ax3.fill_between(train_sizes, test_scores_mean - test_scores_std,

test_scores_mean + test_scores_std, alpha=0.1, color="#2492ff")

ax3.plot(train_sizes, train_scores_mean, 'o-', color="#ff9124",

label="Training score")

ax3.plot(train_sizes, test_scores_mean, 'o-', color="#2492ff",

label="Cross-validation score")

ax3.set_title("支持向量机学习曲线", fontsize=14)

ax3.set_xlabel('Training size (m)')

ax3.set_ylabel('Score')

ax3.grid(True)

ax3.legend(loc="best")

# 模型4-决策树

train_sizes, train_scores, test_scores = learning_curve(

est4, X, y, cv=cv, n_jobs=n_jobs, train_sizes=train_sizes)

train_scores_mean = np.mean(train_scores, axis=1)

train_scores_std = np.std(train_scores, axis=1)

test_scores_mean = np.mean(test_scores, axis=1)

test_scores_std = np.std(test_scores, axis=1)

ax4.fill_between(train_sizes, train_scores_mean - train_scores_std,

train_scores_mean + train_scores_std, alpha=0.1,

color="#ff9124")

ax4.fill_between(train_sizes, test_scores_mean - test_scores_std,

test_scores_mean + test_scores_std, alpha=0.1, color="#2492ff")

ax4.plot(train_sizes, train_scores_mean, 'o-', color="#ff9124",

label="Training score")

ax4.plot(train_sizes, test_scores_mean, 'o-', color="#2492ff",

label="Cross-validation score")

ax4.set_title("决策树学习曲线", fontsize=14)

ax4.set_xlabel('Training size (m)')

ax4.set_ylabel('Score')

ax4.grid(True)

ax4.legend(loc="best")

return plt

In [64]:

cv = ShuffleSplit(n_splits=100,

test_size=0.2,

random_state=42

)

plot_learning_curve(best_para_lr, # 传入4种模型

best_para_knn,

best_para_svc,

best_para_dt,

X_train,

y_train,

(0.87,1.01),

cv=cv,

n_jobs=4

)

plt.show

roc曲线

In [65]:

from sklearn.metrics import roc_curve, roc_auc_score

from sklearn.model_selection import cross_val_predict

In [66]:

lr_pred = cross_val_predict(best_para_lr,

X_train,

y_train,

cv=5,

# method="decision_function"

)

knn_pred = cross_val_predict(best_para_knn,

X_train,

y_train,

cv=5

)

svc_pred = cross_val_predict(best_para_svc,

X_train,

y_train,

cv=5

)

dt_pred = cross_val_predict(best_para_dt,

X_train,

y_train,

cv=5

)

In [67]:

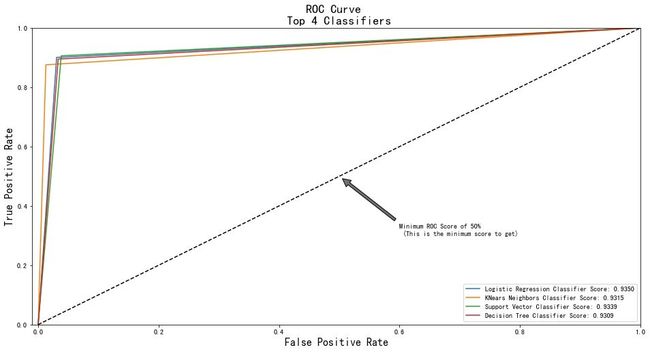

print('Logistic Regression: ', roc_auc_score(y_train, lr_pred))

print('KNears Neighbors: ', roc_auc_score(y_train, knn_pred))

print('Support Vector Classifier: ', roc_auc_score(y_train, svc_pred))

print('Decision Tree Classifier: ', roc_auc_score(y_train, dt_pred))

Logistic Regression: 0.934970120644943

KNears Neighbors: 0.9314677528469951

Support Vector Classifier: 0.9339060209719247

Decision Tree Classifier: 0.930932179501635

In [68]:

log_fpr, log_tpr, log_thresold = roc_curve(y_train, lr_pred)

knear_fpr, knear_tpr, knear_threshold = roc_curve(y_train, knn_pred)

svc_fpr, svc_tpr, svc_threshold = roc_curve(y_train, svc_pred)

tree_fpr, tree_tpr, tree_threshold = roc_curve(y_train, dt_pred)

# 绘制tpr-fpr得分图

def graph_roc_curve_multiple(log_fpr, log_tpr, knear_fpr, knear_tpr, svc_fpr, svc_tpr, tree_fpr, tree_tpr):

plt.figure(figsize=(16,8))

plt.title('ROC Curve \n Top 4 Classifiers', fontsize=18)

plt.plot(log_fpr, log_tpr, label='Logistic Regression Classifier Score: {:.4f}'.format(roc_auc_score(y_train, lr_pred)))

plt.plot(knear_fpr, knear_tpr, label='KNears Neighbors Classifier Score: {:.4f}'.format(roc_auc_score(y_train, knn_pred)))

plt.plot(svc_fpr, svc_tpr, label='Support Vector Classifier Score: {:.4f}'.format(roc_auc_score(y_train, svc_pred)))

plt.plot(tree_fpr, tree_tpr, label='Decision Tree Classifier Score: {:.4f}'.format(roc_auc_score(y_train, dt_pred)))

plt.plot([0, 1], [0, 1], 'k--')

plt.axis([-0.01, 1, 0, 1])

plt.xlabel('False Positive Rate', fontsize=16)

plt.ylabel('True Positive Rate', fontsize=16)

plt.annotate('Minimum ROC Score of 50% \n (This is the minimum score to get)',

xy=(0.5, 0.5),

xytext=(0.6, 0.3),

arrowprops=dict(facecolor='#6E726D', shrink=0.05),

)

plt.legend()

graph_roc_curve_multiple(log_fpr, log_tpr, knear_fpr, knear_tpr, svc_fpr, svc_tpr, tree_fpr, tree_tpr)

plt.show()

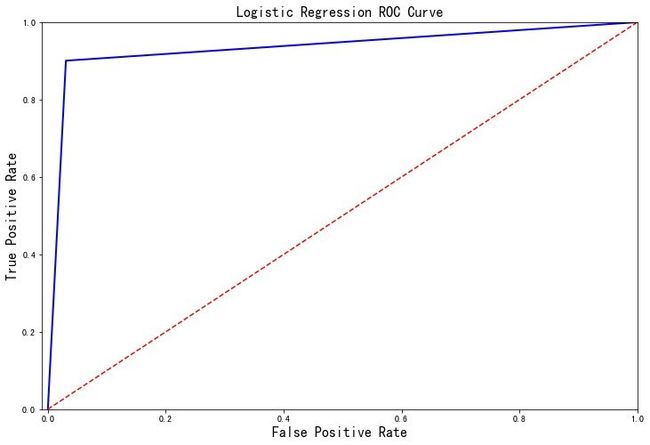

探索逻辑回归评价指标

探索在逻辑回归模型的分类评价指标:

In [69]:

def logistic_roc_curve(log_fpr, log_tpr):

plt.figure(figsize=(12,8))

plt.title('Logistic Regression ROC Curve', fontsize=16)

plt.plot(log_fpr, log_tpr, 'b-', linewidth=2)

plt.plot([0, 1], [0, 1], 'r--')

plt.xlabel('False Positive Rate', fontsize=16)

plt.ylabel('True Positive Rate', fontsize=16)

plt.axis([-0.01,1,0,1])

logistic_roc_curve(log_fpr, log_tpr)

plt.show()

from sklearn.metrics import precision_recall_curve

precision, recall, threshold = precision_recall_curve(y_train, lr_pred)

In [71]:

from sklearn.metrics import recall_score, precision_score, f1_score, accuracy_score

y_pred = best_para_lr.predict(X_train)

# Overfitting Case

print('---' * 20)

print('Recall Score: {:.2f}'.format(recall_score(y_train, y_pred)))

print('Precision Score: {:.2f}'.format(precision_score(y_train, y_pred)))

print('F1 Score: {:.2f}'.format(f1_score(y_train, y_pred)))

print('Accuracy Score: {:.2f}'.format(accuracy_score(y_train, y_pred)))

print('---' * 20)

print("Accuracy Score: {:.2f}".format(np.mean(undersample_accuracy)))

print("Precision Score: {:.2f}".format(np.mean(undersample_precision)))

print("Recall Score: {:.2f}".format(np.mean(undersample_recall)))

print("F1 Score: {:.2f}".format(np.mean(undersample_f1)))

print('---' * 20)

------------------------------------------------------------

# 基于原数据

Recall Score: 0.92

Precision Score: 0.79

F1 Score: 0.85

Accuracy Score: 0.84

------------------------------------------------------------

# 基于欠采样的数据

Accuracy Score: 0.75

Precision Score: 0.00

Recall Score: 0.24

F1 Score: 0.00

------------------------------------------------------------