钉钉杯初赛A题建模-多模型融合预测银行卡诈骗模型(详细代码、解释)

钉钉杯初赛A题建模-多模型融合预测银行卡诈骗模型

前言:

8月10结束的钉钉杯a题,整体简单,建模整体代码分享如下,主要是进行了多个模型投票法融合的模型。

数据+全部代码:

链接:https://pan.baidu.com/s/1SZtLsuPHSmlaOy111uW_YA

提取码:xx78

1、对数据进行前两列特征数据进行标准化

2、采用上采样和下采样进行数据处理,使数据极不平衡得到处理

3、使用上采样和下采样的数据分别用第一阶段的5个模型进行训练和预测

4、模型优化,使用roc_auc曲线选出最好的三个模型进行保存,在第三阶段进行模型融合

5、加载四个模型融合为一个模型

6、对融合后的模型进行训练和模型评估

7、混淆矩阵查看模型的效果

数据读取与查看

读取数据

import pandas as pd

import numpy as np

df=pd.read_csv("数据集/card_transdata.csv",encoding='utf-8') #文件路径为绝对路径,根据自己电脑文件夹的路径修改

df

| distance_from_home | distance_from_last_transaction | ratio_to_median_purchase_price | repeat_retailer | used_chip | used_pin_number | online_order | fraud | |

|---|---|---|---|---|---|---|---|---|

| 0 | 57.877857 | 0.311140 | 1.945940 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 |

| 1 | 10.829943 | 0.175592 | 1.294219 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 2 | 5.091079 | 0.805153 | 0.427715 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 |

| 3 | 2.247564 | 5.600044 | 0.362663 | 1.0 | 1.0 | 0.0 | 1.0 | 0.0 |

| 4 | 44.190936 | 0.566486 | 2.222767 | 1.0 | 1.0 | 0.0 | 1.0 | 0.0 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 999995 | 2.207101 | 0.112651 | 1.626798 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 |

| 999996 | 19.872726 | 2.683904 | 2.778303 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 |

| 999997 | 2.914857 | 1.472687 | 0.218075 | 1.0 | 1.0 | 0.0 | 1.0 | 0.0 |

| 999998 | 4.258729 | 0.242023 | 0.475822 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 |

| 999999 | 58.108125 | 0.318110 | 0.386920 | 1.0 | 1.0 | 0.0 | 1.0 | 0.0 |

1000000 rows × 8 columns

查看数据情况

df.info()

RangeIndex: 1000000 entries, 0 to 999999

Data columns (total 8 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 distance_from_home 1000000 non-null float64

1 distance_from_last_transaction 1000000 non-null float64

2 ratio_to_median_purchase_price 1000000 non-null float64

3 repeat_retailer 1000000 non-null float64

4 used_chip 1000000 non-null float64

5 used_pin_number 1000000 non-null float64

6 online_order 1000000 non-null float64

7 fraud 1000000 non-null float64

dtypes: float64(8)

memory usage: 61.0 MB

- 数据的类型基本是float64。即都是数字形式

- 数据中没有空行

# 介绍数据集各列的 数据统计情况

df.describe()

| distance_from_home | distance_from_last_transaction | ratio_to_median_purchase_price | repeat_retailer | used_chip | used_pin_number | online_order | fraud | |

|---|---|---|---|---|---|---|---|---|

| count | 1000000.000000 | 1000000.000000 | 1000000.000000 | 1000000.000000 | 1000000.000000 | 1000000.000000 | 1000000.000000 | 1000000.000000 |

| mean | 26.628792 | 5.036519 | 1.824182 | 0.881536 | 0.350399 | 0.100608 | 0.650552 | 0.087403 |

| std | 65.390784 | 25.843093 | 2.799589 | 0.323157 | 0.477095 | 0.300809 | 0.476796 | 0.282425 |

| min | 0.004874 | 0.000118 | 0.004399 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 |

| 25% | 3.878008 | 0.296671 | 0.475673 | 1.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 |

| 50% | 9.967760 | 0.998650 | 0.997717 | 1.000000 | 0.000000 | 0.000000 | 1.000000 | 0.000000 |

| 75% | 25.743985 | 3.355748 | 2.096370 | 1.000000 | 1.000000 | 0.000000 | 1.000000 | 0.000000 |

| max | 10632.723672 | 11851.104565 | 267.802942 | 1.000000 | 1.000000 | 1.000000 | 1.000000 | 1.000000 |

- 可以观察到distance_from_home(银行卡交易地点与家的距离)和distance_from_last_transaction(与上次交易发生的距离)的方差相对于其他特征很大

数据分析可视化

print('distance_from_home不是诈骗统计:'+str(len(df.loc[(df['fraud'] == 0),'distance_from_home'])))

print('distance_from_home是诈骗统计:'+str(len(df.loc[(df['fraud'] == 1),'distance_from_home'])))

print('distance_from_last_transaction不是诈骗统计:'+str(len(df.loc[(df['fraud'] == 0),'distance_from_last_transaction'])))

print('distance_from_last_transaction是诈骗统计:'+str(len(df.loc[(df['fraud'] == 1),'distance_from_last_transaction'])))

print('ratio_to_median_purchase_price不是诈骗统计:'+str(len(df.loc[(df['fraud'] == 0),'ratio_to_median_purchase_price'])))

print('ratio_to_median_purchase_price是诈骗统计:'+str(len(df.loc[(df['fraud'] == 1),'ratio_to_median_purchase_price'])))

distance_from_home不是诈骗统计:912597

distance_from_home是诈骗统计:87403

distance_from_last_transaction不是诈骗统计:912597

distance_from_last_transaction是诈骗统计:87403

ratio_to_median_purchase_price不是诈骗统计:912597

ratio_to_median_purchase_price是诈骗统计:87403

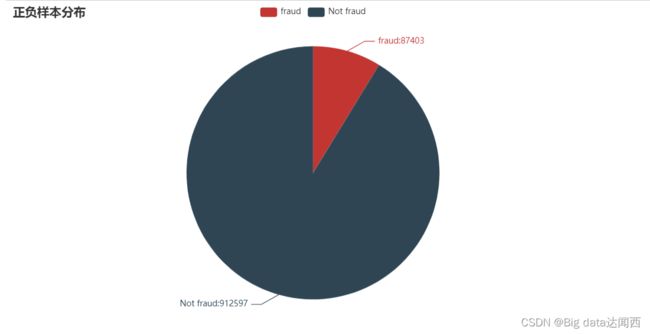

查看正负样本数量:

from pyecharts.charts import Pie

from pyecharts import options as opts

L1=['fraud','Not fraud']

num=[87403,912597]

c=Pie()

c.add("",[list(z) for z in zip(L1,num)])

c.set_global_opts(title_opts=opts.TitleOpts(title="正负样本分布"))

c.set_series_opts(label_opts=opts.LabelOpts(formatter="{b}:{c}"))

c.render_notebook()

-

从中我们可以观察到,正样本数量远远大于负样本数量,正负样本数量不均衡。

-

大部分分类器的输出类别是基于阈值的,如小于0.5的为反例,大于则为正例。在数据不平衡时,默认的阈值会导致模型输出倾向与类别数据多的类别

-

这里我们采用下采样的方法平衡数据

下采样 :从大量的正样本中挑选若干个,使得正样本和负样本数目一样小

观察distance_from_home和是否诈骗的关系

#### 观察distance和是否诈骗的关系

import matplotlib.pyplot as plt

# 构建两个子图

f, (ax1, ax2) = plt.subplots(2, 1, sharex=True, figsize=(16,4))

# 设置柱状宽度

bins = 30

# 统计欺诈案例的交易金额

ax1.hist(df["distance_from_home"][df["fraud"]== 1], bins = bins)

ax1.set_title('Fraud')

# 统计正常案例的交易金额

ax2.hist(df["distance_from_home"][df["fraud"] == 0], bins = bins)

ax2.set_title('Not Fraud')

# 画坐标系

plt.xlabel('distance')

plt.ylabel('Number of Transactions')

plt.yscale('log')

plt.show() # 展示图像

- k可以看出咋骗集中在distance大约为500以内,说明可能是同城诈骗居多。

观察distance_from_last_transaction:和是否诈骗的关系

#### 观察distance和是否诈骗的关系

import matplotlib.pyplot as plt

# 构建两个子图

f, (ax1, ax2) = plt.subplots(2, 1, sharex=True, figsize=(16,4))

# 设置柱状宽度

bins = 30

# 统计欺诈案例的交易金额

ax1.hist(df["distance_from_last_transaction"][df["fraud"]== 1], bins = bins)

ax1.set_title('Fraud')

# 统计正常案例的交易金额

ax2.hist(df["distance_from_last_transaction"][df["fraud"] == 0], bins = bins)

ax2.set_title('Not Fraud')

# 画坐标系

plt.xlabel('distance')

plt.ylabel('Number of Transactions')

plt.yscale('log')

plt.show() # 展示图像

同城诈骗,可能距离小不容易引起怀疑

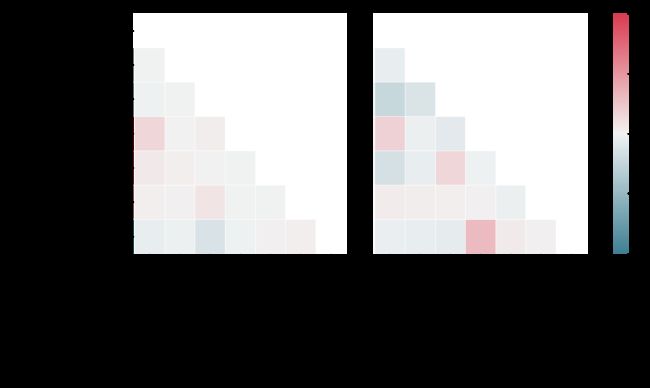

观察各个特征之间的联系

import seaborn as sns

# 创建图像

grid_kws = {"width_ratios": (.9, .9, .05), "wspace": 0.2}

f, (ax1, ax2, cbar_ax) = plt.subplots(1, 3, gridspec_kw=grid_kws, figsize = (18, 9))

# 定义调色板

cmap = sns.diverging_palette(220, 8, as_cmap=True)

# 计算正常案例中的特征联系

correlation_NonFraud = df[df["fraud"] == 0].loc[:, df.columns != 'fraud'].corr()

# 计算欺诈案例中的特征联系

correlation_Fraud = df[df["fraud"] == 1].loc[:, df.columns != 'fraud'].corr()

# 计算上三角mask矩阵

mask = np.zeros_like(correlation_NonFraud)

indices = np.triu_indices_from(correlation_NonFraud)

mask[indices] = True

# 画正常案例的特征联系热力图

ax1 =sns.heatmap(correlation_NonFraud, ax = ax1, vmin = -1, vmax = 1, cmap = cmap, square = False, \

linewidths = 0.5, mask = mask, cbar = False)

ax1.set_xticklabels(ax1.get_xticklabels(), size = 16);

ax1.set_yticklabels(ax1.get_yticklabels(), size = 16);

ax1.set_title('Normal', size = 20)

# 画欺诈案例的特征联系热力图

ax2 = sns.heatmap(correlation_Fraud, vmin = -1, vmax = 1, cmap = cmap, ax = ax2, square = False, \

linewidths = 0.5, mask = mask, yticklabels = False, \

cbar_ax = cbar_ax, cbar_kws={'orientation': 'vertical', 'ticks': [-1, -0.5, 0, 0.5, 1]})

ax2.set_xticklabels(ax2.get_xticklabels(), size = 16);

ax2.set_title('Fraud', size = 20);

cbar_ax.set_yticklabels(cbar_ax.get_yticklabels(), size = 14);

plt.show() # 展示图像

df.corr()

| distance_from_home | distance_from_last_transaction | ratio_to_median_purchase_price | repeat_retailer | used_chip | used_pin_number | online_order | fraud | |

|---|---|---|---|---|---|---|---|---|

| distance_from_home | 1.000000 | 0.000193 | -0.001374 | 0.143124 | -0.000697 | -0.001622 | -0.001301 | 0.187571 |

| distance_from_last_transaction | 0.000193 | 1.000000 | 0.001013 | -0.000928 | 0.002055 | -0.000899 | 0.000141 | 0.091917 |

| ratio_to_median_purchase_price | -0.001374 | 0.001013 | 1.000000 | 0.001374 | 0.000587 | 0.000942 | -0.000330 | 0.462305 |

| repeat_retailer | 0.143124 | -0.000928 | 0.001374 | 1.000000 | -0.001345 | -0.000417 | -0.000532 | -0.001357 |

| used_chip | -0.000697 | 0.002055 | 0.000587 | -0.001345 | 1.000000 | -0.001393 | -0.000219 | -0.060975 |

| used_pin_number | -0.001622 | -0.000899 | 0.000942 | -0.000417 | -0.001393 | 1.000000 | -0.000291 | -0.100293 |

| online_order | -0.001301 | 0.000141 | -0.000330 | -0.000532 | -0.000219 | -0.000291 | 1.000000 | 0.191973 |

| fraud | 0.187571 | 0.091917 | 0.462305 | -0.001357 | -0.060975 | -0.100293 | 0.191973 | 1.000000 |

从上图可以看出

- 在银行卡诈骗事件中,变量distance_from_home、ratio_to_median_purchase_price、repeat_retailer与属于诈骗有较强的

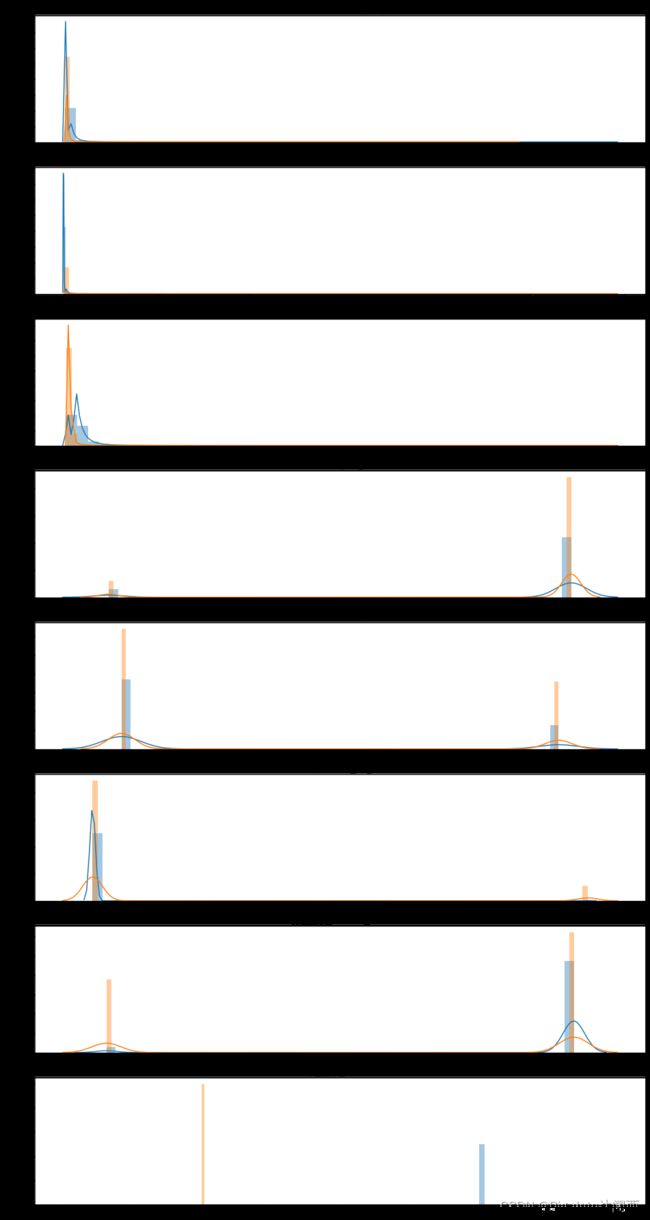

观察各个特征分布

import matplotlib.pyplot as plt

import matplotlib.gridspec as gridspec

import seaborn as sns

# 特征名

feature_num = len(df.columns)

v_feat = list(df.columns)

# 构建图像

plt.figure(figsize=(16,feature_num*4))

gs = gridspec.GridSpec(feature_num, 1)

for i, cn in enumerate(df[v_feat]):

ax = plt.subplot(gs[i])

sns.distplot(df[cn][df["fraud"] == 1], bins=50)

sns.distplot(df[cn][df["fraud"] == 0], bins=100)

ax.set_xlabel('')

ax.set_title('特征直方图: ' + str(cn))

plt.rcParams['font.sans-serif']=['SimHei']

plt.show() # 展示图像

特征工程

数据标准化

# 统一导入工具包

import numpy as np

import pandas as pd

import os

from sklearn.preprocessing import StandardScaler

from sklearn.compose import ColumnTransformer

from sklearn.model_selection import train_test_split, GridSearchCV

from sklearn.ensemble import RandomForestClassifier

from sklearn.metrics import roc_auc_score, classification_report, roc_curve, auc, plot_confusion_matrix, precision_score, recall_score, f1_score

from imblearn.over_sampling import SMOTE

from imblearn.under_sampling import RandomUnderSampler

from imblearn.pipeline import Pipeline

from joblib import dump, load

import matplotlib.pyplot as plt

import matplotlib.gridspec as gridspec

import seaborn as sns

# 观察特征返回每列的标准偏差

df.var()

distance_from_home 4275.954684

distance_from_last_transaction 667.865469

ratio_to_median_purchase_price 7.837698

repeat_retailer 0.104430

used_chip 0.227620

used_pin_number 0.090486

online_order 0.227334

fraud 0.079764

dtype: float64

- 前两个方差太大,我们需要对其进行标准化 因为模型会对方差较大的特征值误认为它对与分类有着较大的权重,因此把数据大小劲量均衡

### 单独使用StandardScaler()进行标准化

from sklearn.preprocessing import StandardScaler

old_dfh = df['distance_from_home'].values.reshape(-1, 1)

# print(old_amount)

print('distance_from_home标准化之前的方差', old_dfh.std())

norm_dfh = StandardScaler().fit_transform(df['distance_from_home'].values.reshape(-1, 1))

print('distance_from_home标准化之后的方差', norm_dfh.std())

### 单独使用StandardScaler()进行标准化

from sklearn.preprocessing import StandardScaler

old_dflt = df['distance_from_last_transaction'].values.reshape(-1, 1)

# print(old_amount)

print('distance_from_last_transaction标准化之前的方差', old_dflt.std())

norm_dflt = StandardScaler().fit_transform(df['distance_from_last_transaction'].values.reshape(-1, 1))

print('distance_from_last_transaction标准化之后的方差', norm_dflt.std())

distance_from_home标准化之前的方差 65.39075170364431

distance_from_home标准化之后的方差 1.0000000000000004

distance_from_last_transaction标准化之前的方差 25.843080339696936

distance_from_last_transaction标准化之后的方差 1.0

# 封装到ColumnTransformer中,方便后续调用标准化操作

column_trans = Pipeline([('scaler', StandardScaler())])

preprocessing = ColumnTransformer(

transformers=[

('column_trans', column_trans, ['distance_from_home','distance_from_last_transaction'])

], remainder='passthrough'

)

过采样与欠采样数据处理

-

SMOTE算法过采样的思想是合成新的少数类样本,合成的策略是对每个少数类样本a,从它的最近邻中随机选一个样本b,然后在a、b之间的连线上随机选一点作为新合成的少数类样本。

-

如果采用欠采样的方法,通常是对数目较多的那一类样本进行随机挑选样本,使得两类样本数目相等。这种做法会抛弃了大部分数据。

划分数据集

x = df.drop('fraud',axis=1)

x

y = df['fraud']

y

X_train, X_test, y_train, y_test = train_test_split(x, y, test_size=0.2, random_state=42)

#查看维度

print('x_train.shape:',X_train.shape)

print('y_train.shape:',y_train.shape)

print('x_test.shape:',X_test.shape)

print('y_test.shape:',y_test.shape)

x_train.shape: (800000, 7)

y_train.shape: (800000,)

x_test.shape: (200000, 7)

y_test.shape: (200000,)

SMOTE过采样

### 单独使用SMOTE的结果

# 利用SMOTE进行过采样

print('过采样前,1的样本的个数为:',len(y_train[y_train==1]))

print('过采样前,0的样本的个数为:',len(y_train[y_train==0]))

over_sampler=SMOTE(random_state=0)

X_os_train,y_os_train=over_sampler.fit_resample(X_train,y_train)

print('过采样后,1的样本的个数为:',len(y_os_train[y_os_train==1]))

print('过采样后,0的样本的个数为:',len(y_os_train[y_os_train==0]))

过采样前,1的样本的个数为: 69960

过采样前,0的样本的个数为: 730040

过采样后,1的样本的个数为: 730040

过采样后,0的样本的个数为: 730040

随机欠采样

### 单独使用随机欠采样的结果

print('欠采样前,1的样本的个数为:',len(y_train[y_train==1]))

print('欠采样前,0的样本的个数为:',len(y_train[y_train==0]))

under_sampler=RandomUnderSampler(random_state=0)

X_us_train,y_us_train=under_sampler.fit_resample(X_train,y_train)

print('欠采样后,1的样本的个数为:',len(y_us_train[y_us_train==1]))

print('欠采样后,0的样本的个数为:',len(y_us_train[y_us_train==0]))

欠采样前,1的样本的个数为: 69960

欠采样前,0的样本的个数为: 730040

欠采样后,1的样本的个数为: 69960

欠采样后,0的样本的个数为: 69960

流水线建构模型

数据在进行模型拟合之前,需要先将数据进行输入标准化等操作转换为新数据,对于新数据,模型的预测和评估都需要进行多次转换。使用Pipeline(流水线)技术可以将数据处理和模型拟合结合在一起,减少代码量。

Pipeline 的中间过程由sklearn相适配的转换器(transformer)构成,最后一步是一个estimator(模型)。中间的节点都可以执行fit和transform方法,这样预处理都可以封装进去;最后节点只需要实现fit方法

from sklearn.linear_model import SGDClassifier # 随机梯度

from sklearn.neighbors import KNeighborsClassifier # K近邻

from sklearn.tree import DecisionTreeClassifier # 决策树

from sklearn.ensemble import RandomForestClassifier # 随机森林

from sklearn.model_selection import cross_val_score # 交叉验证计算accuracy

from sklearn.model_selection import GridSearchCV # 网格搜索,获取最优参数

from sklearn.model_selection import StratifiedKFold # 交叉验证

from collections import Counter

from xgboost import XGBClassifier

# 评估指标

from sklearn.metrics import confusion_matrix, precision_score, recall_score, f1_score, roc_auc_score, accuracy_score, classification_report

from sklearn.ensemble import BaggingClassifier # 集成学习

过采样流水线模型训练分数

classifiers = {

"KNN":KNeighborsClassifier(), # K近邻

'DT':DecisionTreeClassifier(), # 决策树

'RFC':RandomForestClassifier(), # 随机森林

'Bagging':BaggingClassifier(), # 集成学习bagging

'SGD':SGDClassifier(), #随机梯度

'XGB':XGBClassifier() #XGBoost算法

}

def accuracy_scores(x_train, y_train):

for key, classifier in classifiers.items(): # 遍历每一个分类器,分别训练、计算得分

over_pipe = Pipeline([

('preprocessing', preprocessing),

('sampler', SMOTE() ), # 数据高度不平衡,因此使用SMOTE对少数类进行过采样

('classifier',classifier)

])

over_pipe.fit(x_train, y_train)

training_score = cross_val_score(over_pipe, x_train, y_train, cv=5) # 5折交叉验证

print("Classifier Name : ", classifier.__class__.__name__," Training Score :", round(training_score.mean(), 4)*100,'%')

print("过采样的各个分类模型的训练分数:")

accuracy_scores(X_train,y_train)

过采样的各个分类模型的训练分数:

Classifier Name : KNeighborsClassifier Training Score : 99.8 %

Classifier Name : DecisionTreeClassifier Training Score : 100.0 %

Classifier Name : RandomForestClassifier Training Score : 100.0 %

Classifier Name : BaggingClassifier Training Score : 100.0 %

Classifier Name : SGDClassifier Training Score : 92.77 %

Classifier Name : XGBClassifier Training Score : 100.0 %

欠采样流水线模型训练分数

def under_accuracy_scores(x_train, y_train):

for key, classifier in classifiers.items(): # 遍历每一个分类器,分别训练、计算得分

# 欠采样

under_pipe = Pipeline([

('preprocessing', preprocessing),

('sampler', RandomUnderSampler() ), # The data is highly imbalanced, hence undersample majority class with RandomUnderSampler

('classifier', classifier)

])

under_pipe.fit(x_train, y_train)

training_score = cross_val_score(under_pipe, x_train, y_train, cv=5) # 5折交叉验证

print("Classifier Name : ", classifier.__class__.__name__," Training Score :", round(training_score.mean(), 4)*100,'%')

print("欠采样的各个分类模型的训练分数:")

under_accuracy_scores(X_train,y_train)

欠采样的各个分类模型的训练分数:

Classifier Name : KNeighborsClassifier Training Score : 99.26 %

Classifier Name : DecisionTreeClassifier Training Score : 99.99 %

Classifier Name : RandomForestClassifier Training Score : 99.99 %

Classifier Name : BaggingClassifier Training Score : 99.99 %

Classifier Name : SGDClassifier Training Score : 92.46 %

Classifier Name : XGBClassifier Training Score : 99.99 %

综上过采样和欠采样的模型训练分数:

-

过采样的模型比欠采样的模型训练分数高

-

在过采样模型中 ,决策树模型、随机森林模型、Bagging模型、XGBoost模型的训练分数达到了100%,我们选择这四个模型作为分类模型,

-

后面对这四个模型进行最优参数搜索、融合模型

网格搜索,得到每个模型的最优参数模型

- cross_val_score :

一般用于获取每折的交叉验证的得分,然后根据这个得分为模型选择合适的超参数,通常需要编写循环手动完成交叉验证过程;

- GridSearchCV :

除了自行完成叉验证外,还返回了最优的超参数及对应的最优模型

所以相对于cross_val_score来说,GridSearchCV在使用上更为方便;但是对于细节理解上,手动实现循环调用cross_val_score会更好些。

#1、决策树模型最优参数寻找

def DT_gs(x_train, y_train):

DT_param = {

'classifier__criterion':['gini', 'entropy'], # 衡量标准

'classifier__max_depth':list(range(2, 5, 1)), # 树的深度

'classifier__min_samples_leaf':list(range(2, 7, 1)) # 最小叶子节点数

}

DT_pipe =Pipeline([

('preprocessing', preprocessing),

('sampler', SMOTE() ), # 数据高度不平衡,因此使用SMOTE对少数类进行过采样

('classifier',DecisionTreeClassifier())

])

dt_gs = GridSearchCV(estimator=DT_pipe,param_grid=DT_param, n_jobs=-1,verbose=50, cv=4, scoring='roc_auc')

dt_gs.fit(x_train, y_train)

dt_best_estimators = dt_gs.best_estimator_ # 最优参数

return dt_best_estimators

# 2、随机森林最优参数选择

def RFC_gs(x_train, y_train):

grid_search_models = {

'classifier__n_estimators': [25,50,75,100,200] # 仅作示例,可以选择其他参数

}

RFC_over_pipe = Pipeline([

('preprocessing', preprocessing),

('sampler', SMOTE() ), # 数据高度不平衡,因此使用SMOTE对少数类进行过采样

('classifier',RandomForestClassifier())

])

pipe = GridSearchCV(RFC_over_pipe, grid_search_models, verbose=50, cv=5, scoring='roc_auc')

pipe.fit(x_train, y_train)

bst = pipe.best_estimator_ # 最优参数

return bst

# 3、Bagging模型最优参数选择

def bag_gs(x_train, y_train):

BAG_param = {

'classifier__n_estimators':[10, 15, 20] #集成的基估计器的个数

}

bag_over_pipe = Pipeline([

('preprocessing', preprocessing),

('sampler', SMOTE() ), # 数据高度不平衡,因此使用SMOTE对少数类进行过采样

('classifier',BaggingClassifier())

])

bag_over_pipe = GridSearchCV(bag_over_pipe, BAG_param, verbose=50, cv=5, scoring='roc_auc')

bag_over_pipe.fit(x_train, y_train)

bag_bst = bag_over_pipe.best_estimator_ # 最优参数

return bag_bst

# 3、XGBoost模型最优参数选择

def xgb_gs(x_train, y_train):

XGB_param = {

'classifier__max_depth':[3,4,5,6]

}

xgb_over_pipe = Pipeline([

('preprocessing', preprocessing),

('sampler', SMOTE() ), # 数据高度不平衡,因此使用SMOTE对少数类进行过采样

('classifier',XGBClassifier())

])

xgb_over_pipe = GridSearchCV(xgb_over_pipe, XGB_param, verbose=50, cv=5, scoring='roc_auc')

xgb_over_pipe.fit(x_train, y_train)

xgb_bst = xgb_over_pipe.best_estimator_ # 最优参数

return xgb_bst

# 得到最优参数模型

DT_best_estimator = DT_gs(X_train, y_train)

RFC_best_estimator = RFC_gs(X_train, y_train)

BAG_best_estimator = bag_gs(X_train, y_train)

XGB_best_estimator = xgb_gs(X_train,y_train)

print('4个模型最优参数:')

print('DT_best_estimator:',DT_best_estimator)

print('RFC_best_estimator:',RFC_best_estimator)

print('BAG_best_estimator:',BAG_best_estimator)

print('XGB_best_estimator:',XGB_best_estimator)

4个模型最优参数:

DT_best_estimator: Pipeline(steps=[('preprocessing',

ColumnTransformer(remainder='passthrough',

transformers=[('column_trans',

Pipeline(steps=[('scaler',

StandardScaler())]),

['distance_from_home',

'distance_from_last_transaction'])])),

('sampler', SMOTE()),

('classifier',

DecisionTreeClassifier(max_depth=4, min_samples_leaf=4))])

RFC_best_estimator: Pipeline(steps=[('preprocessing',

ColumnTransformer(remainder='passthrough',

transformers=[('column_trans',

Pipeline(steps=[('scaler',

StandardScaler())]),

['distance_from_home',

'distance_from_last_transaction'])])),

('sampler', SMOTE()),

('classifier', RandomForestClassifier(n_estimators=75))])

BAG_best_estimator: Pipeline(steps=[('preprocessing',

ColumnTransformer(remainder='passthrough',

transformers=[('column_trans',

Pipeline(steps=[('scaler',

StandardScaler())]),

['distance_from_home',

'distance_from_last_transaction'])])),

('sampler', SMOTE()), ('classifier', BaggingClassifier())])

XGB_best_estimator: Pipeline(steps=[('preprocessing',

ColumnTransformer(remainder='passthrough',

transformers=[('column_trans',

Pipeline(steps=[('scaler',

StandardScaler())]),

['distance_from_home',

'distance_from_last_transaction'])])),

('sampler', SMOTE()),

('classifier',

XGBClassifier(base_score=0.5, booster='gbtree', callbacks=None,

colsample_bylevel=1, colsample_bynode=1,

colsa...

gamma=0, gpu_id=-1, grow_policy='depthwise',

importance_type=None, interaction_constraints='',

learning_rate=0.300000012, max_bin=256,

max_cat_to_onehot=4, max_delta_step=0,

max_depth=3, max_leaves=0, min_child_weight=1,

missing=nan, monotone_constraints='()',

n_estimators=100, n_jobs=0, num_parallel_tree=1,

predictor='auto', random_state=0, reg_alpha=0,

reg_lambda=1, ...))])

保存最优参数的四个模型

import joblib as jl

#保存决策树模型:

jl.dump(DT_best_estimator,'./模型保存/dt.pkl')

#保存随机森林模型:

jl.dump(RFC_best_estimator,'./模型保存/rfc.pkl')

#保存bagging模型:

jl.dump(BAG_best_estimator,'./模型保存/bag.pkl')

#保存xgboost模型:

jl.dump(XGB_best_estimator,'./模型保存/xgb.pkl')

四个模型模型评估

评估指标数据

用 precision_recall_fscore_support 可以同时计算真实值和预测值之间的精确率、召回率、F 值、支持度。支持度为在真实值每一类出现的事件次数。

from sklearn.metrics import precision_recall_fscore_support

from sklearn.metrics import accuracy_score

def caculate(models, x_test, y_test):

# 计算各种参数的值

accuracy_results = []

F1_score_results = []

Recall_results = []

Precision_results = []

AUC_ROC_results = []

for model in models:

y_pred = model.predict(x_test)

accuracy = accuracy_score(y_test, y_pred) # 计算准确度

precision, recall, f1_score, _ = precision_recall_fscore_support(y_test, y_pred) # 计算:精确度,召回率,f1_score

AUC_ROC = roc_auc_score(y_test, y_pred) # 计算AUC

# 保存计算值

accuracy_results.append(round(accuracy,4))

F1_score_results.append(round(f1_score.mean(),4))

Recall_results.append(round(recall.mean(),4))

AUC_ROC_results.append(AUC_ROC)

Precision_results.append(round(precision.mean(),4))

return accuracy_results, F1_score_results, Recall_results, AUC_ROC_results, Precision_results

# 将所有最优超参数的模型放在一起

best_models = [ DT_best_estimator, RFC_best_estimator, BAG_best_estimator, XGB_best_estimator]

# 调用函数计算各项指标值

accuracy_results, F1_score_results, Recall_results, AUC_ROC_results, Precision_results = caculate(best_models, X_test, y_test)

# 将各项值放入到DataFrame中

result_df = pd.DataFrame(columns=['Accuracy', 'F1-score', 'Recall', 'Precision', 'AUC_ROC'],

index=['DT','RFC','Bagging','XGBoost'])

result_df['Accuracy'] = accuracy_results

result_df['F1-score'] = F1_score_results

result_df['Recall'] = Recall_results

result_df['Precision'] = Precision_results

result_df['AUC_ROC'] = AUC_ROC_results

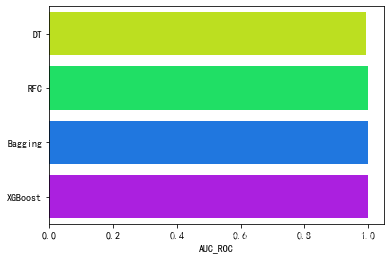

result_df

| Accuracy | F1-score | Recall | Precision | AUC_ROC | |

|---|---|---|---|---|---|

| DT | 0.9934 | 0.9799 | 0.9927 | 0.9680 | 0.992728 |

| RFC | 1.0000 | 1.0000 | 0.9999 | 1.0000 | 0.999940 |

| Bagging | 1.0000 | 0.9999 | 0.9999 | 0.9999 | 0.999929 |

| XGBoost | 1.0000 | 0.9999 | 1.0000 | 0.9999 | 0.999986 |

可视化 AUC_ROC的评分.

# 可视化 AUC的评分.

g = sns.barplot('AUC_ROC', result_df.index, data=result_df, palette='hsv', orient='h')

计算各个模型的AUC值

from sklearn.model_selection import cross_val_predict

DT_pred = DT_best_estimator.predict(X_test)

RFC_pred = RFC_best_estimator.predict(X_test)

BAG_pred = BAG_best_estimator.predict(X_test)

XGB_pred = XGB_best_estimator.predict(X_test)

print(DT_pred)

print(RFC_pred)

print(BAG_pred)

print(XGB_pred)

[0. 0. 0. ... 1. 0. 0.]

[0. 0. 0. ... 1. 0. 0.]

[0. 0. 0. ... 1. 0. 0.]

[0 0 0 ... 1 0 0]

# 计算auc的评分

print('决策树模型auc分数 :', round(roc_auc_score(y_test, DT_pred),2))

print('随机森林模型auc分数 :', round(roc_auc_score(y_test, RFC_pred),2))

print('bagging模型auc分数 :', round(roc_auc_score(y_test, BAG_pred),2))

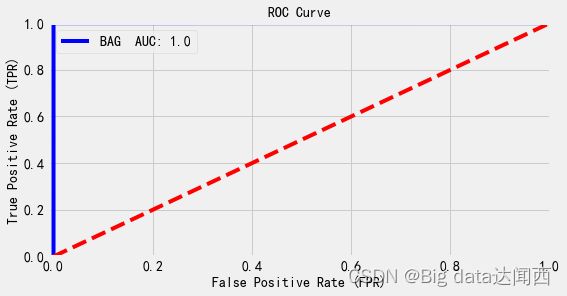

print('xgboost模型auc分数 :', round(roc_auc_score(y_test, XGB_pred),2))

决策树模型auc分数 : 0.99

随机森林模型auc分数 : 1.0

bagging模型auc分数 : 1.0

xgboost模型auc分数 : 1.0

绘制各个模型的roc曲线:

DT_fpr, DT_tpr, DT_threshold = roc_curve(y_test, DT_pred)

RFC_fpr, RFC_tpr, RFC_threshold = roc_curve(y_test, RFC_pred)

BAG_fpr, BAG_tpr, BAG_threshold = roc_curve(y_test, BAG_pred)

XGB_fpr, XGB_tpr, XGB_threshold = roc_curve(y_test, XGB_pred)

# 绘制roc曲线

def graph_roc(fpr, tpr, name, score):

plt.figure(figsize=(8,4)) # 画布大小

plt.title("ROC Curve", fontsize=14)

plt.plot(fpr, tpr, 'b',label=name+" AUC: "+ str(round(score,2)))

plt.plot([0, 1], [0, 1], color='r', linestyle='--')

plt.axis([-0.01, 1, 0, 1]) # 坐标轴

plt.xlabel("False Positive Rate (FPR)", fontsize=14)

plt.ylabel("True Positive Rate (TPR)", fontsize=14)

plt.legend()

plt.show()

#决策树

graph_roc(DT_fpr, DT_tpr, 'DT', roc_auc_score(y_test, DT_pred))

# 随机森林

graph_roc(RFC_fpr, RFC_tpr, 'RFC', roc_auc_score(y_test, RFC_pred))

#bag

graph_roc(BAG_fpr,BAG_tpr, 'BAG', roc_auc_score(y_test, BAG_pred))

#XGB

graph_roc(XGB_fpr,XGB_tpr, 'XGB', roc_auc_score(y_test, XGB_pred))

模型评估总结

,四个效果好的模型在模型评估上展现

准确率、精确率、召回率、F1值、ROC曲线、AUC 都显示很高, 说明四个模型在分类上效果显著,可信度高

加载模型、融合

import joblib

model1 = joblib.load(filename="./模型保存/dt.pkl")

model1

model2 = joblib.load('./模型保存/rfc.pkl')

model3 = joblib.load('./模型保存/bag.pkl')

model4 = joblib.load('./模型保存/xgb.pkl')

# 将4个较好的模型集成起来,当做一个模型

from sklearn.ensemble import VotingClassifier

voting_clf = VotingClassifier(estimators=[('DT', model1), ('RFC', model2), ('BAG',model3),

('XGB', model4)], n_jobs=-1,voting='soft')

voting_clf

模型训练

import pandas as pd

import numpy as np

df=pd.read_csv("数据集/card_transdata.csv",encoding='utf-8') #文件路径为绝对路径,根据自己电脑文件夹的路径修改

df

x = df.drop('fraud',axis=1)

x

y = df['fraud']

y

from sklearn.model_selection import train_test_split, GridSearchCV

X_train, X_test, y_train, y_test = train_test_split(x, y, test_size=0.2, random_state=42)

#查看维度

print('x_train.shape:',X_train.shape)

print('y_train.shape:',y_train.shape)

print('x_test.shape:',X_test.shape)

print('y_test.shape:',y_test.shape)

x_train.shape: (800000, 7)

y_train.shape: (800000,)

x_test.shape: (200000, 7)

y_test.shape: (200000,)

# 训练

voting_clf.fit(X_train, y_train)

#训练分数

from sklearn.model_selection import cross_val_score # 交叉验证计算accuracy

training_score = cross_val_score(voting_clf, X_train, y_train, cv=5) # 5折交叉验证

print("融合后模型训练分数:", round(training_score.mean(), 4)*100,'%')

融合后模型训练分数: 100.0 %

# 预测

y_final_pred = voting_clf.predict(X_test)

y_final_pred

array([0., 0., 0., ..., 1., 0., 0.])

模型评估

from sklearn.metrics import roc_auc_score, classification_report, roc_curve, auc, plot_confusion_matrix, precision_score, recall_score, f1_score

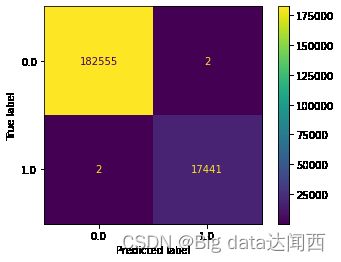

混淆矩阵

#

import matplotlib.pyplot as plt

plot_confusion_matrix(voting_clf, X_test, y_test)

plt.show() # 展示图像

计算精确率、召回率以及综合两者的F1值

y_preds = voting_clf.predict(X_test)

p = precision_score(y_test, y_preds)

r = recall_score(y_test, y_preds)

f1 = f1_score(y_test, y_preds)

print("precision(准确率): ", p)

print("recall(召回率): ", r)

print("F1: ", f1)

precision(准确率): 0.9998853408243995

recall(召回率): 0.9998853408243995

F1: 0.9998853408243995

print(classification_report(y_test, y_preds)) #评价指标

precision recall f1-score support

0.0 1.00 1.00 1.00 182557

1.0 1.00 1.00 1.00 17443

accuracy 1.00 200000

macro avg 1.00 1.00 1.00 200000

weighted avg 1.00 1.00 1.00 200000

保存融合后的模型

joblib.dump(voting_clf,'./模型保存/best_model.pkl')

最后:

创作不易,如果觉得有参考价值,请点个关注再走呗,请点个关注再走呗,请点个关注再走呗,蟹蟹