python版期货量化交易(AlgoPlus)案例(多进程处理子任务)

python版期货量化交易(AlgoPlus)案例(多进程处理子任务)

python因为简单、易上手,所以深受大家的喜爱,并且随着人工智能的不断发展与进步,python也一跃成为了最受欢迎的编程语言之一,俗话说:人生苦短,我用python。伴随着量化交易的崛起,上期所下面的子公司根据CTP接口封装出了python版本的api接口:Algoplus

文章目录

- python版期货量化交易(AlgoPlus)案例(多进程处理子任务)

- 前言

- 一、AlgoPlus是什么?

- 二、使用步骤

-

- 1.引入库

- 2.账号配置

- 3.合成分钟线

- 4.Join函数

- 5.结果展示

- 总结

前言

为了 策略的安全性,有必要自己搭建一套交易系统

提示:以下是本篇文章正文内容,下面案例可供参考

一、AlgoPlus是什么?

安装: pip install AlgoPlus

关于AlgoPlus的介绍请查看www.algoplus.com官网,这里不得不得不吐槽有一下,AlgoPlus官网有一段时间打不开。

二、使用步骤

1.引入库

代码如下(示例):

# from CTP.MdApi import *

from AlgoPlus.CTP.FutureAccount import get_simnow_account, FutureAccount

from AlgoPlus.CTP.FutureAccount import SIMNOW_SERVER, MD_LOCATION, TD_LOCATION

from multiprocessing import Process, Queue

from CTP.MdApi import run_bar_engine, run_tick_engine

from CTP.TradeApi import run_trade_engine

2.账号配置

代码如下(示例):

# 账户配置

future_account = FutureAccount(

broker_id='9999', # 期货公司BrokerID

# server_dict={'TDServer': "180.168.146.187:10130", 'MDServer': '180.168.146.187:10131'}, # TEST

server_dict={'TDServer': "218.202.237.33:10102", 'MDServer': '218.202.237.33:10112'}, # 移动

# TDServer为交易服务器,MDServer为行情服务器。服务器地址格式为"ip:port。"

reserve_server_dict={},

investor_id="****************", # 账户

password="****************", # 密码

app_id='simnow_client_test', # 认证使用AppID

auth_code='0000000000000000', # 认证使用授权码

instrument_id_list=instrument_id_list, # 订阅合约列表

md_page_dir=MD_LOCATION, # MdApi流文件存储地址,默认MD_LOCATION

td_page_dir=TD_LOCATION # TraderApi流文件存储地址,默认TD_LOCATION

)

SimNow提供了7x24小时的模拟服务器

3.合成分钟线

代码如下(algoplus提供官方示例):

# ///深度行情通知

def OnRtnDepthMarketData(self, pDepthMarketData):

last_update_time = self.bar_dict[pDepthMarketData['InstrumentID']]["UpdateTime"]

is_new_1minute = (pDepthMarketData['UpdateTime'][:-2] != last_update_time[:-2]) and pDepthMarketData['UpdateTime'] != b'21:00:00' # 1分钟K线条件

# is_new_5minute = is_new_1minute and int(pDepthMarketData['UpdateTime'][-4]) % 5 == 0 # 5分钟K线条件

# is_new_10minute = is_new_1minute and pDepthMarketData['UpdateTime'][-4] == b"0" # 10分钟K线条件

# is_new_10minute = is_new_1minute and int(pDepthMarketData['UpdateTime'][-5:-3]) % 15 == 0 # 15分钟K线条件

# is_new_30minute = is_new_1minute and int(pDepthMarketData['UpdateTime'][-5:-3]) % 30 == 0 # 30分钟K线条件

# is_new_hour = is_new_1minute and int(pDepthMarketData['UpdateTime'][-5:-3]) % 60 == 0 # 60分钟K线条件

# # 新K线开始

if is_new_1minute and self.bar_dict[pDepthMarketData['InstrumentID']]["UpdateTime"] != b"99:99:99":

for md_queue in self.md_queue_list:

md_queue.put(self.bar_dict[pDepthMarketData['InstrumentID']])

# 将Tick池化为Bar

tick_to_bar(self.bar_dict[pDepthMarketData['InstrumentID']], pDepthMarketData, is_new_1minute)

注意:我在向队列里添加数据时使用了深拷贝,官方给的示例有时无法得到正确的一分钟k线数据,因为当你在交易进程中还未拿到k线数据之前,已经被修改了。

4.Join函数

在Join函数中可以写策略逻辑:开仓、平仓等。

def Join(self):

lastPrice = 0 # 上根k线的收盘价

while True:

if self.status == 0:

if not self.md_queue.empty():

makeData = self.md_queue.get(True)

# 撤单

if self.local_position_dict:

if self.local_position_dict[self.tickData['InstrumentID']]['Volume'] != 0:

self.req_remove(self.tickData)

print(f"====={makeData}")

# 亏损超8个点止损,回撤6个点止损

for instrument_id, position in self.local_position_dict.items():

if self.symbol_close[instrument_id] == 1:

if instrument_id not in self.md_dict.keys():

break

if position['Volume'] != 0 and position['Direction'] == b'0':

self.sell_close(b'', instrument_id, makeData['LastPrice'] - 6, 1)

print(f"卖平仓:{lastPrice},{makeData['LastPrice']}")

else:

self.buy_close(b'', instrument_id, makeData['LastPrice'] + 6, 1)

print(f"买平仓:{lastPrice},{makeData['LastPrice']}")

if lastPrice != 0:

sleep(1) # 时间是59s的时候休眠1s,0s时开仓

if makeData['LastPrice'] >= lastPrice:

self.buy_open(b'', b'p2209', makeData['LastPrice'] + 6, 1)

print(f"买开仓:{lastPrice},{makeData['LastPrice']}")

else:

self.sell_open(b'', b'p2209', makeData['LastPrice'] - 6, 1)

print(f"卖开仓:{lastPrice},{makeData['LastPrice']}")

lastPrice = makeData['LastPrice']

# 初始化为最新价

self.HighPrice = makeData['LastPrice']

self.LowPrice = makeData['LastPrice']

else:

sleep(1)

# 止盈止损

self.check_position()

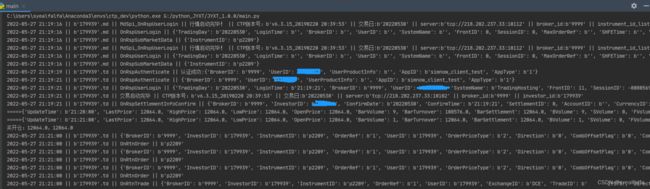

5.结果展示

源代码链接: https://pan.baidu.com/s/10HnZf89cEAbXtlbrJRlVEA .

提取码:yooq

如果您熟悉c++11,请看CTP开发案例:

CTP接口开发链接: https://blog.csdn.net/syealfalfa/article/details/124994132 .

总结

请关注www.algoplus.com官网的最新消息