记录一次基于kaggle比赛的细节,时序分割,特征构造,缺失值处理

记录一次基于kaggle比赛的细节,时序分割,特征构造,缺失值处理。

- 前言

- 数据处理

- 缺失值的处理

- 模型构造训练部分

前言

这次参加了kaggle上的一个信用卡诈骗预测项目,比赛之中有些细节希望可以记录下来分享,同时以防时间长忘记。

比赛地址:https://www.kaggle.com/c/ieee-fraud-detection

数据处理

简要说明一下这次比赛给的数据特征:

1.四百个匿名特征

2.部分特征有大规模缺失值

3.训练和预测数据中缺失值分布有较大差异

4.疑似时间增量的特征(以证实)

5.给出了两类匿名数据,一种是关于卡账户的信息,一类是卡的交易信息。

// An highlighted block

#读取数据

train_id=pd.read_csv('data1/train_identity.csv')

test_id=pd.read_csv('data1/test_identity.csv')

train_data=pd.read_csv('data1/train_transaction.csv')

test_data=pd.read_csv('data1/test_transaction.csv')

#将两类数据拼接起来,同时清除内存

train = train_data.merge(train_id, how='left', on='TransactionID')

test = test_data.merge(test_id, how='left',on='TransactionID')

del train_id; gc.collect()

del test_id; gc.collect()

del train_data; gc.collect()

del test_data; gc.collect()

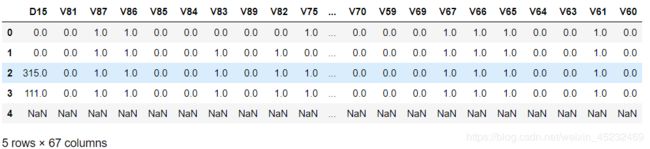

train.describe()

train.isnull().sum()

train与test缺失值比较:

training_missing = train.isna().sum(axis=0) / train.shape[0]

test_missing = test.isna().sum(axis=0) / test.shape[0]

change = (training_missing / test_missing).sort_values(ascending=False)

change = change[change<1e6] # remove the divide by zero errors

train_more=change[change>4].reset_index()

train_more.columns=['train_more_id','rate']

test_more=change[change<0.4].reset_index()

test_more.columns=['test_more_id','rate']

train_more_id=train_more['train_more_id'].values

train[train_more_id].head()

得到的是训练集中比测试集中缺少多得多的特征:

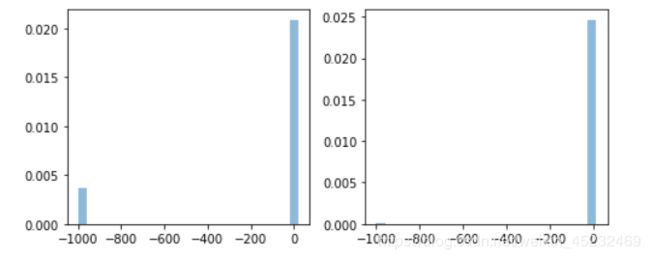

在这些特征中拿出V80进行对比,这里对缺失值进行了-999填充,可以明显看到[“TransactionDT”]>2.5e7之后train的缺失数量比Test高了许多。

fig, axs = plt.subplots(ncols=2)

train_vals = train["V80"].fillna(-999)

test_vals = test[test["TransactionDT"]>2.5e7]["V80"].fillna(-999) # values following the shift

axs[0].hist(train_vals, alpha=0.5, normed=True, bins=25)

axs[1].hist(test_vals, alpha=0.5, normed=True, bins=25)

fig.set_size_inches(7,3)

plt.tight_layout()

接下来我们对数据进行简单的分析:

-

首先在数据中可以观测到诈骗用户有大多数用的是’P_emaildomain’,考虑单独列出作为一个特征,同时对各种邮箱进行分类;

-

前面提到TransactionDT ,疑似时间增量。对其在训练和预测集的最大值与最小值相减,同时除 去‘606024’得到364,而训练集是182,预测集是182;

-

很明显整个数据是干净的时序切割,即没有重复的时间出现,那么我们如果用datetime来处理TransactionDT 只有hour、weekend有助于模型训练,其他特征比如MONTH在训练可能帮你得到很好分数。但在预测时缺影响了模型的精度。;

-

这情况训练模型要用到TimeSeriesSplit分割训练以及测试,这应该是这场比赛的关键点;

-

前面提到过训练和预测集在TransactionDT 大于>2.5e7之后有着明显缺失值的分布不均,处理好这部分的也是拿到好名次的关键;

-

观测到hour与isFraud 的分布,呈现出1点到6点明显高于其他时间点的特点,构造’night’特征(考虑到基于一年的数据,对于季节和节假日的特征提取并没有帮助);

-

同时对于一个用户来说特征缺少的个数对于isFraud 的影响也有关(越匿名越安全?),添加’isna‘特征;

-

数据分布及其不平衡,已经尝试过欠采样和重采样以及smote重采样,效果比较一般。特别是欠采样果然是不负众望比我想象的精度还要低,最后不过选择的还是1:5的欠采样(毕竟跑的快,哈哈)加分类惩罚权重, 添加权重的原因是在欠采样之后将更多的0归类于1。

代码isna = train.isna().sum(axis=1) isna_test = test.isna().sum(axis=1) train['isna']=train.isna().sum(axis=1) test['isna']=test.isna().sum(axis=1) import datetime START_DATE = '2017-12-01' startdate = datetime.datetime.strptime(START_DATE, '%Y-%m-%d') train['TransactionDT'] = train['TransactionDT'].apply(lambda x: (startdate + datetime.timedelta(seconds = x))) test['TransactionDT'] = test['TransactionDT'].apply(lambda x: (startdate + datetime.timedelta(seconds = x))) train['hour'] = train['TransactionDT'].dt.hour test['hour'] = test['TransactionDT'].dt.hour train['month'] = train['TransactionDT'].dt.month test['month'] = test['TransactionDT'].dt.month #print(train['TransactionDT']) x=test['hour']<7 x1=test['hour']>19 x.astype(int) x1.astype(int) x2=np.add(x,x1) x2.astype(int) test['night']=x2.astype(int) x=train['hour']<7 x1=train['hour']>19 x.astype(int) x1.astype(int) x2=np.add(x,x1) x2.astype(int) train['night']=x2.astype(int) index _pro=train['P_emaildomain']=='protonmail.com' index_pro_data=train['P_emaildomain'][index_pro] train['isprotonmail']=index_pro_data del index_pro del index_pro_data index_pro=test['P_emaildomain']=='protonmail.com' index_pro_data=test['P_emaildomain'][index_pro] test['isprotonmail']=index_pro_data del index_pro del index_pro_data train.loc[ (train.isprotonmail.isnull()), 'isprotonmail' ] = 0 train['isprotonmail'].describe(include="all") test.loc[ (test.isprotonmail.isnull()), 'isprotonmail' ] = 0 test['isprotonmail'].describe(include="all") emails = {'gmail': 'google', 'att.net': 'att', 'twc.com': 'spectrum', 'scranton.edu': 'other', 'optonline.net': 'other', 'hotmail.co.uk': 'microsoft', 'comcast.net': 'other', 'yahoo.com.mx': 'yahoo', 'yahoo.fr': 'yahoo', 'yahoo.es': 'yahoo', 'charter.net': 'spectrum', 'live.com': 'microsoft', 'aim.com': 'aol', 'hotmail.de': 'microsoft', 'centurylink.net': 'centurylink', 'gmail.com': 'google', 'me.com': 'apple', 'earthlink.net': 'other', 'gmx.de': 'other', 'web.de': 'other', 'cfl.rr.com': 'other', 'hotmail.com': 'microsoft', 'protonmail.com': 'other', 'hotmail.fr': 'microsoft', 'windstream.net': 'other', 'outlook.es': 'microsoft', 'yahoo.co.jp': 'yahoo', 'yahoo.de': 'yahoo', 'servicios-ta.com': 'other', 'netzero.net': 'other', 'suddenlink.net': 'other', 'roadrunner.com': 'other', 'sc.rr.com': 'other', 'live.fr': 'microsoft', 'verizon.net': 'yahoo', 'msn.com': 'microsoft', 'q.com': 'centurylink', 'prodigy.net.mx': 'att', 'frontier.com': 'yahoo', 'anonymous.com': 'other', 'rocketmail.com': 'yahoo', 'sbcglobal.net': 'att', 'frontiernet.net': 'yahoo', 'ymail.com': 'yahoo', 'outlook.com': 'microsoft', 'mail.com': 'other', 'bellsouth.net': 'other', 'embarqmail.com': 'centurylink', 'cableone.net': 'other', 'hotmail.es': 'microsoft', 'mac.com': 'apple', 'yahoo.co.uk': 'yahoo', 'netzero.com': 'other', 'yahoo.com': 'yahoo', 'live.com.mx': 'microsoft', 'ptd.net': 'other', 'cox.net': 'other', 'aol.com': 'aol', 'juno.com': 'other', 'icloud.com': 'apple'} us_emails = ['gmail', 'net', 'edu'] for c in ['P_emaildomain', 'R_emaildomain']: train[c + '_bin'] = train[c].map(emails) test[c + '_bin'] = test[c].map(emails) train[c + '_suffix'] = train[c].map(lambda x: str(x).split('.')[-1]) test[c + '_suffix'] = test[c].map(lambda x: str(x).split('.')[-1]) train[c + '_suffix'] = train[c + '_suffix'].map(lambda x: x if str(x) not in us_emails else 'us') test[c + '_suffix'] = test[c + '_suffix'].map(lambda x: x if str(x) not in us_emails else 'us') from sklearn.preprocessing import Imputer imp = Imputer(missing_values='NaN', strategy='most_frequent', axis=0)

缺失值的处理

test[['dist1','dist2','C1','C2','C4','C5','C6','C7','C8','C9','C10','C11','C12','C13','C14']]=imp.fit_transform(test[['dist1','dist2','C1','C2','C4','C5','C6','C7','C8','C9','C10','C11','C12','C13','C14']])

train[['dist1','dist2','C1','C2','C4','C5','C6','C7','C8','C9','C10','C11','C12','C13','C14']]=imp.fit_transform(train[['dist1','dist2','C1','C2','C4','C5','C6','C7','C8','C9','C10','C11','C12','C13','C14']])

test[test.TransactionDT>2.5e7][train_more_id]=imp.fit_transform(test[test.TransactionDT>2.5e7][train_more_id])

train[train_more_id]=imp.fit_transform(train[train_more_id])

这部分处理了一些缺失较少的数据,接来下有些缺失较多但却很重要的特征采用随机森林的方法填充,这里只上一段代码

from sklearn.ensemble import RandomForestRegressor

def set_missing_card2(df):

# 把已有的数值型特征取出来丢进Random Forest Regressor中

give_df = df[['card2', 'TransactionID', 'card1', 'TransactionAmt', 'C1', 'C2', 'C4', 'C5', 'C6', 'C7', 'C8', 'C9', 'C10', 'C11', 'C12', 'C13']]

# 乘客分成已知年龄和未知年龄两部分

# ,'card3','card5','addr1''addr2'

known_card2 = give_df[give_df.card2.notnull()].as_matrix()

unknown_card2 = give_df[give_df.card2.isnull()].as_matrix()

# y即目标年龄

y = known_card2[:, 0]

# X即特征属性值

X = known_card2[:, 1:]

# fit到RandomForestRegressor之中

rfr = RandomForestRegressor(random_state=0, n_estimators=10, n_jobs=-1)

rfr.fit(X, y)

# 用得到的模型进行未知年龄结果预测

predictedcard2= rfr.predict(unknown_card2[:, 1::])# 一个或是2个冒号都一样的

# 用得到的预测结果填补原缺失数据

df.loc[(df.card2.isnull()), 'card2']= predictedcard2

return df, rfr

# train_data.head()

train, rfr = set_missing_card2(train)

test, rfr = set_missing_card2(test)

接下来处理其他缺失的特征值和字典符特征编码。

for c1, c2 in train.dtypes.reset_index().values:

if c2=='O':

train[c1] = train[c1].map(lambda x: labels[str(x).lower()])

test[c1] = test[c1].map(lambda x: labels[str(x).lower()])

train.fillna(-999, inplace=True)

test.fillna(-999, inplace=True)

for f in test.columns: #train中有需要预测的项,懒得remove了直接用test

if train[f].dtype=='object' or test[f].dtype=='object':

print(f)

lbl = preprocessing.LabelEncoder()

lbl.fit(list(train[f].values) + list(test[f].values))

train[f] = lbl.transform(list(train[f].values))

test[f] = lbl.transform(list(test[f].values))

这里原来有个想法就是把数据按月分开再进行欠/重采样,在按4个月训练2个月测试来做,后来时间不够了直接上TimeSeriesSplit划分更方便。

columns_list=list(train)

####按月拆分数据集

train_12=train[train.month==12]

train_1=train[train.month==1]

train_2=train[train.month==2]

train_3=train[train.month==3]

train_4=train[train.month==4]

train_5=train[train.month==5]

train_6=train[train.month==6]

from imblearn.under_sampling import RandomUnderSampler

ran=RandomUnderSampler(return_indices=True) ##intialize to return indices of dropped rows

train_12,y_train12,dropped12 = ran.fit_sample(train_12,train_12['isFraud'])

train_1,y_train1,dropped1 = ran.fit_sample(train_1,train_1['isFraud'])

train_2,y_train2,dropped2 = ran.fit_sample(train_2,train_2['isFraud'])

train_3,y_train3,dropped3 = ran.fit_sample(train_3,train_3['isFraud'])

train_4,y_train4,dropped4 = ran.fit_sample(train_4,train_4['isFraud'])

train_5,y_train5,dropped5 = ran.fit_sample(train_5,train_5['isFraud'])

train_6,y_train6,dropped6 = ran.fit_sample(train_6,train_6['isFraud'])

del train

del y_train12

del y_train1

del y_train2

del y_train3

del y_train4

del y_train5

del y_train6

'''#随机过采样

from imblearn.over_sampling import RandomOverSampler

ros = RandomOverSampler(random_state=0)

train_data, y_train = ros.fit_sample(train, y_train)

del train; gc.collect()'''

'''#smote过采样

from imblearn.over_sampling import SMOTE

smote = SMOTE(frac=0.1, random_state=1)

train_data, y_train = smote.fit_sample(train, y_train)'''

'''from imblearn.under_sampling import RandomUnderSampler

ran=RandomUnderSampler(return_indices=True) ##intialize to return indices of dropped rows

train_data,y_train,dropped = ran.fit_sample(train,y_train)

del train; gc.collect()'''

模型构造训练部分

这次没用SVM打比赛,用的是神器XGBOOST ,过两天出个手推XGBOOST以及调参的贴,这里就不详细展开说了。直接上文档上的代码:

def fast_auc(y_true, y_prob):

y_true = np.asarray(y_true)

y_true = y_true[np.argsort(y_prob)]

nfalse = 0

auc = 0

n = len(y_true)

for i in range(n):

y_i = y_true[i]

nfalse += (1 - y_i)

auc += y_i * nfalse

auc /= (nfalse * (n - nfalse))

return auc

def eval_auc(y_true, y_pred):

return 'auc', fast_auc(y_true, y_pred), True

def group_mean_log_mae(y_true, y_pred, types, floor=1e-9):

maes = (y_true-y_pred).abs().groupby(types).mean()

return np.log(maes.map(lambda x: max(x, floor))).mean()

def train_model_classification(X, X_test, y, params, folds, model_type='lgb', eval_metric='auc', columns=None, plot_feature_importance=False, model=None,

verbose=10000, early_stopping_rounds=200, n_estimators=50000, splits=None, n_folds=3, averaging='usual', n_jobs=-1):

"""

A function to train a variety of classification models.

Returns dictionary with oof predictions, test predictions, scores and, if necessary, feature importances.

:params: X - training data, can be pd.DataFrame or np.ndarray (after normalizing)

:params: X_test - test data, can be pd.DataFrame or np.ndarray (after normalizing)

:params: y - target

:params: folds - folds to split data

:params: model_type - type of model to use

:params: eval_metric - metric to use

:params: columns - columns to use. If None - use all columns

:params: plot_feature_importance - whether to plot feature importance of LGB

:params: model - sklearn model, works only for "sklearn" model type

"""

columns = X.columns if columns is None else columns

n_splits = folds.n_splits if splits is None else n_folds

X_test = X_test[columns]

# to set up scoring parameters

metrics_dict = {'auc': {'lgb_metric_name': eval_auc,

'catboost_metric_name': 'AUC',

'sklearn_scoring_function': metrics.roc_auc_score},

}

result_dict = {}

if averaging == 'usual':

# out-of-fold predictions on train data

oof = np.zeros((len(X), 1))

# averaged predictions on train data

prediction = np.zeros((len(X_test), 1))

elif averaging == 'rank':

# out-of-fold predictions on train data

oof = np.zeros((len(X), 1))

# averaged predictions on train data

prediction = np.zeros((len(X_test), 1))

# list of scores on folds

scores = []

feature_importance = pd.DataFrame()

# split and train on folds

for fold_n, (train_index, valid_index) in enumerate(folds.split(X)):

print(f'Fold {fold_n + 1} started at {time.ctime()}')

if type(X) == np.ndarray:

X_train, X_valid = X[columns][train_index], X[columns][valid_index]

y_train, y_valid = y[train_index], y[valid_index]

else:

X_train, X_valid = X[columns].iloc[train_index], X[columns].iloc[valid_index]

y_train, y_valid = y.iloc[train_index], y.iloc[valid_index]

if model_type == 'lgb':

model = lgb.LGBMClassifier(**params, n_estimators=n_estimators, n_jobs = n_jobs)

model.fit(X_train, y_train,

eval_set=[(X_train, y_train), (X_valid, y_valid)], eval_metric=metrics_dict[eval_metric]['lgb_metric_name'],

verbose=verbose, early_stopping_rounds=early_stopping_rounds)

y_pred_valid = model.predict_proba(X_valid)[:, 1]

y_pred = model.predict_proba(X_test, num_iteration=model.best_iteration_)[:, 1]

if model_type == 'xgb':

train_data = xgb.DMatrix(data=X_train, label=y_train, feature_names=X.columns)

valid_data = xgb.DMatrix(data=X_valid, label=y_valid, feature_names=X.columns)

watchlist = [(train_data, 'train'), (valid_data, 'valid_data')]

model = xgb.train(dtrain=train_data, num_boost_round=n_estimators, evals=watchlist, early_stopping_rounds=early_stopping_rounds, verbose_eval=verbose, params=params)

y_pred_valid = model.predict(xgb.DMatrix(X_valid, feature_names=X.columns), ntree_limit=model.best_ntree_limit)

y_pred = model.predict(xgb.DMatrix(X_test, feature_names=X.columns), ntree_limit=model.best_ntree_limit)

if model_type == 'sklearn':

model = model

model.fit(X_train, y_train)

y_pred_valid = model.predict(X_valid).reshape(-1,)

score = metrics_dict[eval_metric]['sklearn_scoring_function'](y_valid, y_pred_valid)

print(f'Fold {fold_n}. {eval_metric}: {score:.4f}.')

print('')

y_pred = model.predict_proba(X_test)

if model_type == 'cat':

model = CatBoostClassifier(iterations=n_estimators, eval_metric=metrics_dict[eval_metric]['catboost_metric_name'], **params,

loss_function=metrics_dict[eval_metric]['catboost_metric_name'])

model.fit(X_train, y_train, eval_set=(X_valid, y_valid), cat_features=[], use_best_model=True, verbose=False)

y_pred_valid = model.predict(X_valid)

y_pred = model.predict(X_test)

if averaging == 'usual':

oof[valid_index] = y_pred_valid.reshape(-1, 1)

scores.append(metrics_dict[eval_metric]['sklearn_scoring_function'](y_valid, y_pred_valid))

prediction += y_pred.reshape(-1, 1)

elif averaging == 'rank':

oof[valid_index] = y_pred_valid.reshape(-1, 1)

scores.append(metrics_dict[eval_metric]['sklearn_scoring_function'](y_valid, y_pred_valid))

prediction += pd.Series(y_pred).rank().values.reshape(-1, 1)

if model_type == 'lgb' and plot_feature_importance:

# feature importance

fold_importance = pd.DataFrame()

fold_importance["feature"] = columns

fold_importance["importance"] = model.feature_importances_

fold_importance["fold"] = fold_n + 1

feature_importance = pd.concat([feature_importance, fold_importance], axis=0)

prediction /= n_splits

print('CV mean score: {0:.4f}, std: {1:.4f}.'.format(np.mean(scores), np.std(scores)))

result_dict['oof'] = oof

result_dict['prediction'] = prediction

result_dict['scores'] = scores

if model_type == 'lgb':

if plot_feature_importance:

feature_importance["importance"] /= n_splits

cols = feature_importance[["feature", "importance"]].groupby("feature").mean().sort_values(

by="importance", ascending=False)[:50].index

best_features = feature_importance.loc[feature_importance.feature.isin(cols)]

plt.figure(figsize=(16, 12));

sns.barplot(x="importance", y="feature", data=best_features.sort_values(by="importance", ascending=False));

plt.title('LGB Features (avg over folds)');

result_dict['feature_importance'] = feature_importance

result_dict['top_columns'] = cols

return result_dict

模型参数

这里要用到TimeSeriesSplit划分。

from sklearn.model_selection import TimeSeriesSplit

n_fold = 7

folds = TimeSeriesSplit(n_splits=n_fold)

folds = KFold(n_splits=5)

import time

params = {'num_leaves': 256,

'min_child_samples': 79,

'objective': 'binary',

'max_depth': 13,

'learning_rate': 0.03,

"boosting_type": "gbdt",

"subsample_freq": 3,

"subsample": 0.9,

"bagging_seed": 11,

"metric": 'auc',

"verbosity": -1,

'reg_alpha': 0.3,

'reg_lambda': 0.3,

'colsample_bytree': 0.9,

# 'categorical_feature': cat_cols

}

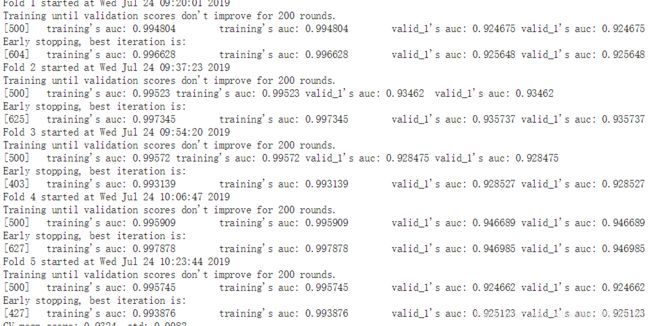

result_dict_lgb = train_model_classification(X=train, X_test=X_test, y=y_train, params=params, folds=folds, model_type='lgb', eval_metric='auc', plot_feature_importance=True,

verbose=500, early_stopping_rounds=200, n_estimators=5000, averaging='usual', n_jobs=-1)

*训练结果以及特征重要排序

最后提交的时候给我一个惊喜0.9430,有点没想通为啥分数比本地训练精度还高??某些特征在本地训练没有帮助而在预测时发挥了很好的效果?暂时就这些把,如果掉出10%我在考虑多堆叠几个模型(这种方法在实际生产中几乎没什么luan用,但是在比赛中确是大杀器,不过还是希望更多的发掘特征以及与出路来达到更好的分数把)