线性回归中的非线性变换

非线性变换

在线性回归模型中,会发现有些变量与预测变量不是线性关系,所以需要非线性变换,把非线性关系转换为线性关系。

一、单变量做变换

载入boston房价数据

from sklearn.datasets import load_boston

from random import shuffle

boston = load_boston()

#seed(0) # Creates a replicable shuffling

#new_index = range(boston.data.shape[0])

#shuffle(new_index) # shuffling the index

#X, y = boston.data[new_index], boston.target[new_index]

X, y = boston.data, boston.target

print (X.shape, y.shape, boston.feature_names)

#散点图判断变量与目标之间的关系

import pandas as pd

df = pd.DataFrame(X,columns=boston.feature_names)

df['target'] = y

scatter = df.plot(kind='scatter', x='LSTAT', y='target', c='r')

从图中可以看出,LSTA可尝试log变换

import numpy as np

from sklearn.feature_selection.univariate_selection import f_regression

a=df['LSTAT'].values

y=boston.target

a=a.reshape(-1,1)

#注意:f_regression中的X参数和Y参数都必须是narray格式,且X必须是矩阵模式。

'''print(type(a))

print(type(y))

print(np.shape(a))

print(np.shape(y))

print(a)

print(y)'''

F, pval = f_regression(a,y)

#X_indices = np.arange(X.shape[-1])

print('F score for the original feature %.1f' % F)

F, pval = f_regression(np.log(a),y)

print('F score for the transformed feature %.1f' % F)

可以看出,log变换之后,F值变大,变换比较有效

import matplotlib.pyplot as plt

c=np.log(a)

#plt.scatter(a,y,s=[30],c='b')

plt.scatter(c,y,s=[30],c='b')

如上图,关系呈现线性。

二、除了考虑单变量,还要考虑变量之间的交互作用

#加载助手类:线性回归模型,K折交叉验证

from sklearn.linear_model import LinearRegression

from sklearn.cross_validation import cross_val_score

from sklearn.cross_validation import KFold

regression = LinearRegression(normalize=True)

crossvalidation = KFold(n=X.shape[0], n_folds=10, shuffle=True, random_state=1)

#加载波士顿房价预测数据集

from sklearn.datasets import load_boston

from random import shuffle

boston = load_boston()

X, y = boston.data, boston.target

df = pd.DataFrame(X,columns=boston.feature_names)

baseline = np.mean(cross_val_score(regression, df, y, scoring='r2', cv=crossvalidation, n_jobs=1))

#创建一个列表,该列表遍历所有的交互项(n*n次),如果加入了某个交互项的模型的k折交叉验证得分高于基准线,就会把交互项和得分存在列表中

interactions = list()

for feature_A in boston.feature_names:

for feature_B in boston.feature_names:

if feature_A > feature_B:

df['interaction'] = df[feature_A] * df[feature_B]

score = np.mean(cross_val_score(regression, df, y, scoring='r2', cv=crossvalidation, n_jobs=1))

if score > baseline:

interactions.append((feature_A, feature_B, round(score,3)))

print ('Baseline R2: %.3f' % baseline)

print ('Top 10 interactions: %s' % sorted(interactions, key=lambda x:x[2], reverse=True)[:10])

结果集如下:

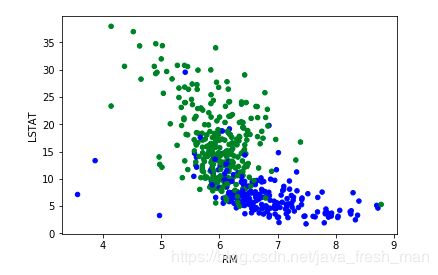

现在检测rm、lstat与房价的关系

colors = ['b' if v > np.mean(y) else 'g' for v in y]

scatter = df.plot(kind='scatter', x='RM', y='LSTAT', c=colors)

rm代表每栋房子的房间数

LSTAT代表该地区低社会地位人口占比,

综上,房间数越多、地区人口社会越高,房价越高,符合常识。

:Attribute Information (in order):

- CRIM per capita crime rate by town

- ZN proportion of residential land zoned for lots over 25,000 sq.ft.

- INDUS proportion of non-retail business acres per town

- CHAS Charles River dummy variable (= 1 if tract bounds river; 0 otherwise)

- NOX nitric oxides concentration (parts per 10 million)

- RM average number of rooms per dwelling

- AGE proportion of owner-occupied units built prior to 1940

- DIS weighted distances to five Boston employment centres

- RAD index of accessibility to radial highways

- TAX full-value property-tax rate per $10,000

- PTRATIO pupil-teacher ratio by town

- B 1000(Bk - 0.63)^2 where Bk is the proportion of blacks by town

- LSTAT % lower status of the population

- MEDV Median value of owner-occupied homes in $1000's

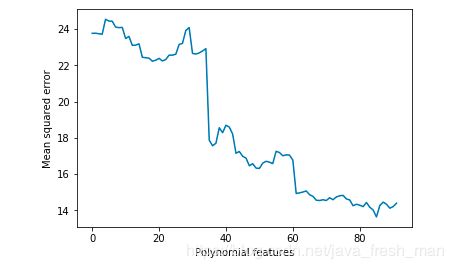

三、多项式回归:添加二次项和相互变量

# Adding polynomial features (x**2,y**2,xy)

polyX = pd.DataFrame(X,columns=boston.feature_names)

baseline = np.mean(cross_val_score(regression, polyX, y, scoring='neg_mean_squared_error', cv=crossvalidation, n_jobs=1))

improvements = [baseline]

for feature_A in boston.feature_names:

polyX[feature_A+'^2'] = polyX[feature_A]**2

improvements.append(np.mean(cross_val_score(regression, polyX, y, scoring='neg_mean_squared_error', cv=crossvalidation, n_jobs=1)))

for feature_B in boston.feature_names:

if feature_A > feature_B:

polyX[feature_A+'*'+feature_B] = polyX[feature_A] * polyX[feature_B]

improvements.append(np.mean(cross_val_score(regression, polyX, y, scoring='neg_mean_squared_error', cv=crossvalidation, n_jobs=1)))

#作图

import matplotlib.pyplot as plt

import numpy as np

plt.figure()

plt.plot(range(0,92),np.abs(improvements),'-')

plt.xlabel('Polynomial features')

plt.ylabel('Mean squared error')

plt.show()

#验证均方差

print(baseline)

print (np.shape(polyX))

crossvalidation = KFold(n=X.shape[0], n_folds=10, shuffle=True, random_state=1)

print ('Mean squared error %.3f' % abs(np.mean(cross_val_score(regression, polyX, y, scoring='neg_mean_squared_error', cv=crossvalidation, n_jobs=1))))

图中可以看出,多项式的特征越多不一定越好。

检查最终的模型,发现polyX有104个特征,一般对于一个特征至少需要有10-20个观察点,最好在30个以上。

此案例有506个观察点,特征点25左右比较合适。104个太多。从折线图看,20是个不错的点。

如果想获得完美的模型,需要逐一去尝试变量。

![]()