import pandas as pd

import pandas_datareader

import datetime

import matplotlib.pylab as plt

import seaborn as sns

from matplotlib.pylab import style

from statsmodels.tsa.arima_model import ARIMA

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

style.use('ggplot')

plt.rcParams['font.sans-serif'] = ['SimHei']

plt.rcParams['axes.unicode_minus'] = False

stockFilePath = './data/T10yr.csv'

stock = pd.read_csv(stockFilePath, index_col=0, parse_dates=[0])

print(stock.head())

print(stock.tail())

Open High Low Close Volume Adj Close

Date

2000-01-03 6.498 6.603 6.498 6.548 0 6.548

2000-01-04 6.530 6.548 6.485 6.485 0 6.485

2000-01-05 6.521 6.599 6.508 6.599 0 6.599

2000-01-06 6.558 6.585 6.540 6.549 0 6.549

2000-01-07 6.545 6.595 6.504 6.504 0 6.504

Open High Low Close Volume Adj Close

Date

2016-07-25 1.584 1.584 1.554 1.571 0 1.571

2016-07-26 1.559 1.587 1.549 1.563 0 1.563

2016-07-27 1.570 1.570 1.511 1.515 0 1.515

2016-07-28 1.525 1.535 1.493 1.511 0 1.511

2016-07-29 1.525 1.530 1.458 1.458 0 1.458

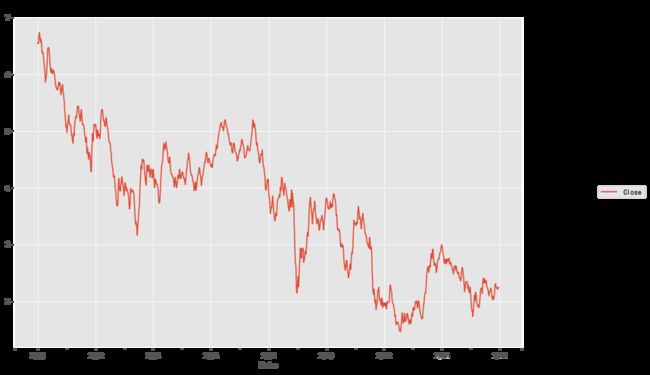

stock_week = stock['Close'].resample('W-MON').mean()

stock_train = stock_week['2000':'2015']

stock_train.plot(figsize=(12,8))

plt.legend(bbox_to_anchor=(1.25, 0.5))

plt.title('Stock close')

sns.despine()

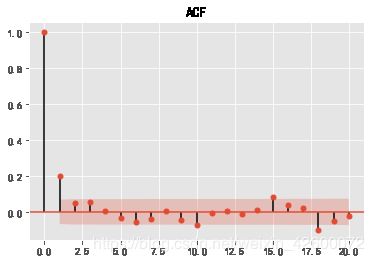

首先做差分,满足最基本的平稳性

stock_diff = stock_train.diff()

stock_diff = stock_diff.dropna()

plt.figure(figsize=(12,8))

plt.plot(stock_diff)

plt.title('一阶差分')

plt.show()

acf = plot_acf(stock_diff, lags=20)

plt.title('ACF')

acf.show()

C:\ProgramData\Anaconda3\lib\site-packages\matplotlib\figure.py:445: UserWarning: Matplotlib is currently using module://ipykernel.pylab.backend_inline, which is a non-GUI backend, so cannot show the figure.

% get_backend())

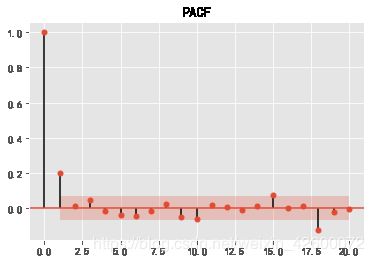

pacf = plot_pacf(stock_diff, lags=20)

plt.title('PACF')

pacf.show()

C:\ProgramData\Anaconda3\lib\site-packages\matplotlib\figure.py:445: UserWarning: Matplotlib is currently using module://ipykernel.pylab.backend_inline, which is a non-GUI backend, so cannot show the figure.

% get_backend())

model = ARIMA(stock_train, order=(1,1,1),freq='W-MON')

result = model.fit()

print(result.summary())

ARIMA Model Results

==============================================================================

Dep. Variable: D.Close No. Observations: 834

Model: ARIMA(1, 1, 1) Log Likelihood 720.846

Method: css-mle S.D. of innovations 0.102

Date: Fri, 29 Mar 2019 AIC -1433.692

Time: 15:41:45 BIC -1414.787

Sample: 01-10-2000 HQIC -1426.444

- 12-28-2015

=================================================================================

coef std err z P>|z| [0.025 0.975]

---------------------------------------------------------------------------------

const -0.0052 0.005 -1.145 0.252 -0.014 0.004

ar.L1.D.Close 0.2841 0.203 1.397 0.163 -0.115 0.683

ma.L1.D.Close -0.0869 0.213 -0.408 0.683 -0.504 0.330

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 3.5199 +0.0000j 3.5199 0.0000

MA.1 11.5087 +0.0000j 11.5087 0.0000

-----------------------------------------------------------------------------

pred = result.predict('20140609', '20160609',dynamic=True, typ='levels')

print(pred)