1.Pandas教程-金融分析教程(1)

注意: 教程内容来自 https://nbviewer.jupyter.org/github/twiecki/financial-analysis-python-tutorial/tree/master/ 这不是完整的系统的pandas教程,此外源教程测试demo老旧,新版本pandas可能无法兼容源程序,本教程是在原教程基础上进行的修正. 使用Spyder IDE进行测试

# -*- coding: utf-8 -*-

"""

Created on Sun Mar 29 17:58:13 2020

@author: CHERN

"""

import datetime

import pandas as pd

from pandas import Series, DataFrame

print(pd.__version__)

import matplotlib.pyplot as plt

import matplotlib as mpl

mpl.rc('figure', figsize=(8, 7))

print(mpl.__version__)

测试程序使用的pandas版本为1.0.1,matplotlib版本为3.1.3

1. 创建和加载数据

1.1 根据python内置list/dict生成

# -*- coding: utf-8 -*-

"""

Created on Sun Mar 29 17:58:13 2020

@author: CHERN

"""

import datetime

import pandas as pd

from pandas import Series, DataFrame

# print(pd.__version__)

import matplotlib.pyplot as plt

import matplotlib as mpl

mpl.rc('figure', figsize=(8, 7))

# print(mpl.__version__)

# 通过python构造一维序列

labels = ['a', 'b', 'c', 'd', 'e']

s = Series([1, 2, 3, 4, 5], index=labels)

print(s)

print(r"'b' in s?")

print('b' in s)

print(s['b'])

print("Series.to_dict() can convert Series to dict")

mapping = s.to_dict()

print(mapping)

print("Series(dict) can convert dict to Series")

print(Series(mapping))

[外链图片转存失败,源站可能有防盗链机制,建议将图片保存下来直接上传(img-eKV3iS94-1586606244035)(assets/2020-03-29-18-12-01.png)]

用法总结

Series对象的构造函数可以传递dict字典类型变量,也可以使用python中list列表.Series.to_dict()方法能够把Series对象转化为python内置dict对象- 通过

'b' in s可以判断键'b'是否存在于Series对象的index中,返回值为True/Falses['b']能够获取Series中数据

1.2 从网络中获取

# -*- coding: utf-8 -*-

"""

Created on Sun Mar 29 17:58:13 2020

@author: CHERN

"""

import datetime

import pandas as pd

from pandas import Series, DataFrame

# print(pd.__version__)

import numpy as np

from pandas_datareader import data, wb # 需要安装 pip install pandas_datareader

import matplotlib.pyplot as plt

import matplotlib

import matplotlib as mpl

mpl.rc('figure', figsize=(8, 7))

# print(mpl.__version__)

# 定义获取数据的时间段

start = datetime.datetime(2010, 1, 1)

end = datetime.datetime(2016,5,20)

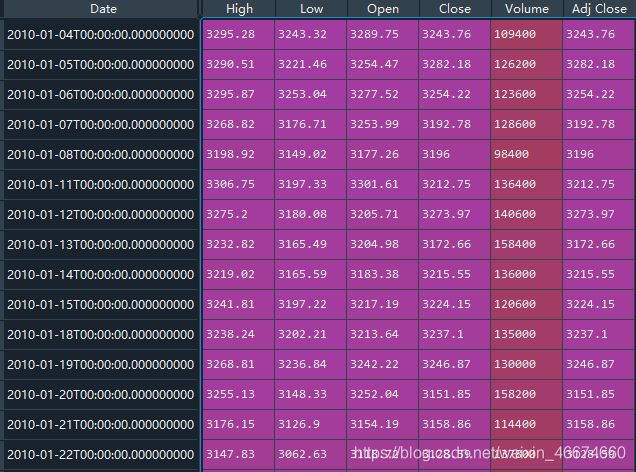

sh = data.DataReader("000001.SS", 'yahoo', start, end)

print(sh.head(3)) # 输出数据前三行

# 将从Yahoo上获取的pandas.Dataframe数据保存到.csv文件中

sh.to_csv('sh.csv')

注意:

- 版本有更新,之前

pd.io.data.get_data_yahoo()方法已经被弃用,当前使用DataReader方法进行实验操作.- 国内访问数据可能会比较慢,需要开启VPN. 为简单起见(代码直接复用,而不需要其他文件),下面得案例将按照从网上获取数据进行

用法小结:

from pandas_datareader import data之后,data.DataReader()方法能够从网络获取金融数据(股票历史数据)DataFrame对象如果行数太多,可以使用.head()方法输出其前5行,.head(n)输出前n行

注意:这里Date为对象

sh的索引

1.3 从文件(.csv/.xlsx etc.)文件中读取数据

# -*- coding: utf-8 -*-

"""

Created on Sun Mar 29 17:58:13 2020

@author: CHERN

"""

import datetime

import pandas as pd

from pandas import Series, DataFrame

# print(pd.__version__)

import numpy as np

from pandas_datareader import data, wb # 需要安装 pip install pandas_datareader

import matplotlib.pyplot as plt

import matplotlib

import matplotlib as mpl

mpl.rc('figure', figsize=(8, 7))

# print(mpl.__version__)

# 定义获取数据的时间段

df = pd.read_csv('sh.csv', index_col='Date', parse_dates=True)

print(df)

2. Series and DataFrame: (基础操作)

2.1 索引切片创建新列

# -*- coding: utf-8 -*-

"""

Created on Sun Mar 29 17:58:13 2020

@author: CHERN

"""

import datetime

import pandas as pd

from pandas import Series, DataFrame

# print(pd.__version__)

import numpy as np

from pandas_datareader import data, wb # 需要安装 pip install pandas_datareader

import matplotlib.pyplot as plt

import matplotlib

import matplotlib as mpl

mpl.rc('figure', figsize=(8, 7))

# print(mpl.__version__)

# 定义获取数据的时间段

df = pd.read_csv('sh.csv', index_col='Date', parse_dates=True)

# print(df)

# type(ts) = pandas.core.series.Series

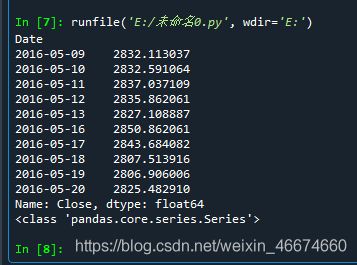

ts = df['Close'][-10:]

print(ts)

print(type(ts))

在IPython中继续执行:

date = ts.index[5]

date

输出:

Timestamp('2016-05-16 00:00:00')

输入:

ts[date]

输出:

2850.862060546875

输入:

ts[5]

输出:

2850.862060546875

输入:

df[['Open', 'Close']].head()

输出:

Open Close

Date

2010-01-04 3289.750000 3243.760010

2010-01-05 3254.468018 3282.178955

2010-01-06 3277.517090 3254.215088

2010-01-07 3253.990967 3192.775879

2010-01-08 3177.259033 3195.997070

输入:

df['diff'] = df.Open - df.Close

df.head()

输出:

High Low ... Adj Close diff

Date ...

2010-01-04 3295.279053 3243.319092 ... 3243.760010 45.989990

2010-01-05 3290.511963 3221.461914 ... 3282.178955 -27.710938

2010-01-06 3295.867920 3253.043945 ... 3254.215088 23.302002

2010-01-07 3268.819092 3176.707031 ... 3192.775879 61.215088

2010-01-08 3198.919922 3149.017090 ... 3195.997070 -18.738037

[5 rows x 7 columns]

输入:

del df['diff']

df.head()

输出:

High Low ... Volume Adj Close

Date ...

2010-01-04 3295.279053 3243.319092 ... 109400 3243.760010

2010-01-05 3290.511963 3221.461914 ... 126200 3282.178955

2010-01-06 3295.867920 3253.043945 ... 123600 3254.215088

2010-01-07 3268.819092 3176.707031 ... 128600 3192.775879

2010-01-08 3198.919922 3149.017090 ... 98400 3195.997070

[5 rows x 6 columns]

用法小结:

- 指令

del df['diff']可以删除数据df中'diff'列

3. 常规的金融计算

3.1 移动平均

close_px = df['Adj Close']

mavg = pd.rolling_mean(close_px, 40)

mavg[-10:]

输出:

File "", line 2, in

mavg = pd.rolling_mean(close_px, 40)

File "C:\Python\lib\site-packages\pandas\__init__.py", line 262, in __getattr__

raise AttributeError(f"module 'pandas' has no attribute '{name}'")

AttributeError: module 'pandas' has no attribute 'rolling_mean'

pandas版本更新,启用

rolling_mean()方法

close_px = df['Adj Close']

mavg = close_px.rolling(40).mean()

mavg

输出:

Date

2010-01-04 NaN

2010-01-05 NaN

2010-01-06 NaN

2010-01-07 NaN

2010-01-08 NaN

2016-05-16 2970.439978

2016-05-17 2967.653333

2016-05-18 2962.371130

2016-05-19 2957.559705

2016-05-20 2952.947778

Name: Adj Close, Length: 1550, dtype: float64

3.2 收益

输入:

rets = close_px / close_px.shift(1) - 1

# rets = close_px.pct_change()

rets.head()

输出:

Date

2010-01-04 NaN

2010-01-05 0.011844

2010-01-06 -0.008520

2010-01-07 -0.018880

2010-01-08 0.001009

Name: Adj Close, dtype: float64

4. 绘图基础

close_px.plot(label='AAPL')

mavg.plot(label='mavg')

plt.legend()

[外链图片转存失败,源站可能有防盗链机制,建议将图片保存下来直接上传(img-VS5moCnW-1586606244038)(assets/2020-03-29-20-40-41.png)]

扩展…

# -*- coding: utf-8 -*-

"""

Created on Sun Mar 29 17:58:13 2020

@author: CHERN

"""

import datetime

import pandas as pd

from pandas import Series, DataFrame

# print(pd.__version__)

import numpy as np

from pandas_datareader import data, wb # 需要安装 pip install pandas_datareader

import matplotlib.pyplot as plt

import matplotlib

import matplotlib as mpl

mpl.rc('figure', figsize=(8, 7))

# print(mpl.__version__)

# 定义获取数据的时间段

start = datetime.datetime(2010, 1, 1)

end = datetime.datetime(2016,5,20)

sh = data.DataReader(['AAPL','GE','GOOG','IBM','KO', 'MSFT', 'PEP'],'yahoo', start, end)['Adj Close']

print(sh.head(3)) # 输出数据前三行

Symbols AAPL GE GOOG ... KO MSFT PEP

Date ...

2009-12-31 26.131752 10.526512 308.832428 ... 19.278732 23.925440 44.622261

2010-01-04 26.538483 10.749147 312.204773 ... 19.292267 24.294369 44.945187

2010-01-05 26.584366 10.804806 310.829926 ... 19.058893 24.302216 45.488274

[3 rows x 7 columns]

输入:

rets = df.pct_change()

plt.scatter(rets.PEP, rets.KO)

plt.xlabel('Returns PEP')

plt.ylabel('Returns KO')

pd.scatter_matrix(rets, diagonal='kde', figsize=(10, 10));

输出:

File "C:\Python\lib\site-packages\pandas\__init__.py", line 262, in __getattr__

raise AttributeError(f"module 'pandas' has no attribute '{name}'")

AttributeError: module 'pandas' has no attribute 'scatter_matrix'

pandas的scatter_matrix用法已经发生变化了,变成了pandas.plotting.scatter_matrix

重新输入:

pd.plotting.scatter_matrix(rets, diagonal='kde', figsize=(10, 10));

[外链图片转存失败,源站可能有防盗链机制,建议将图片保存下来直接上传(img-aAdqCmPm-1586606244040)(assets/2020-03-29-21-18-44.png)]

知识小结:

- 散点图是用来判断两个变量之间的相互关系的工具,一般情况下,散点图用两组数据构成多个坐标点,通过观察坐标点的分布,判断变量间是否存在关联关系,以及相关关系的强度。此外,如果不存在相关关系,可以使用散点图总结特征点的分布模式,即矩阵图(象限图)

pd.scatter_matrix()和pd.scatter()用于绘制散点图矩阵和散点图

输入:

corr = rets.corr()

corr

输出:

Symbols AAPL GE GOOG IBM KO MSFT PEP

Symbols

AAPL 1.000000 0.387574 0.406971 0.387261 0.298461 0.393892 0.273217

GE 0.387574 1.000000 0.423675 0.532942 0.491217 0.478202 0.485198

GOOG 0.406971 0.423675 1.000000 0.402424 0.329096 0.463922 0.322701

IBM 0.387261 0.532942 0.402424 1.000000 0.449300 0.495341 0.412432

KO 0.298461 0.491217 0.329096 0.449300 1.000000 0.402174 0.643624

MSFT 0.393892 0.478202 0.463922 0.495341 0.402174 1.000000 0.414073

PEP 0.273217 0.485198 0.322701 0.412432 0.643624 0.414073 1.000000

输入:

plt.imshow(corr, cmap='hot', interpolation='none')

plt.colorbar()

plt.xticks(range(len(corr)), corr.columns)

plt.yticks(range(len(corr)), corr.columns);

用法小结:

pd.corr()方法用于计算两个序列之间的相关性

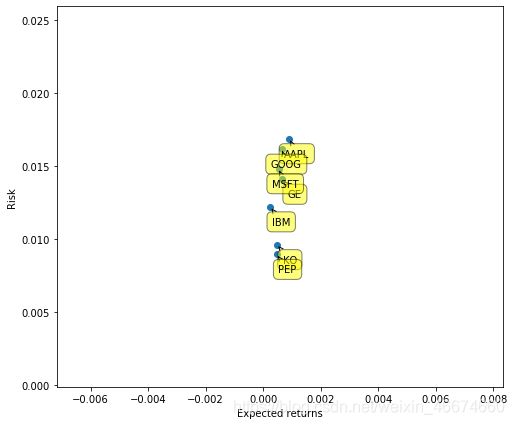

我们经常感兴趣的一件事是预期回报(通常是回报率的均值)与我们承担的风险之间(回报率的方差)的关系。这两者之间往往存在一种权衡。

这里我们使用plt.annotate在散点图上标注标签。

plt.scatter(rets.mean(), rets.std())

plt.xlabel('Expected returns')

plt.ylabel('Risk')

for label, x, y in zip(rets.columns, rets.mean(), rets.std()):

plt.annotate(

label,

xy = (x, y), xytext = (20, -20),

textcoords = 'offset points', ha = 'right', va = 'bottom',

bbox = dict(boxstyle = 'round,pad=0.5', fc = 'yellow', alpha = 0.5),

arrowprops = dict(arrowstyle = '->', connectionstyle = 'arc3,rad=0'))

5. 数据对齐与Nan处理

程序:

# -*- coding: utf-8 -*-

"""

Created on Sun Mar 29 17:58:13 2020

@author: CHERN

"""

import datetime

import pandas as pd

from pandas import Series, DataFrame

# print(pd.__version__)

import numpy as np

from pandas_datareader import data, wb # 需要安装 pip install pandas_datareader

import matplotlib.pyplot as plt

import matplotlib

import matplotlib as mpl

mpl.rc('figure', figsize=(8, 7))

# print(mpl.__version__)

series_list = []

securities = ['AAPL', 'GOOG', 'IBM', 'MSFT']

for security in securities:

s = data.DataReader(security,'yahoo',

start=datetime.datetime(2011, 10, 1),

end=datetime.datetime(2013, 1, 1))['Adj Close']

s.name = security # Rename series to match security name

series_list.append(s)

df = pd.concat(series_list, axis=1)

print(df.head())

AAPL GOOG IBM MSFT

Date

2011-09-30 47.285904 256.558350 130.822800 20.321293

2011-10-03 46.452591 246.834808 129.640747 20.027370

2011-10-04 46.192177 250.012894 130.725555 20.688694

2011-10-05 46.905209 251.407669 132.304108 21.137737

2011-10-06 46.796078 256.393982 135.924973 21.505136

输入:

df.ix[0, 'AAPL'] = np.nan

df.ix[1, ['GOOG', 'IBM']] = np.nan

df.ix[[1, 2, 3], 'MSFT'] = np.nan

df.head()

输出:

AttributeError: 'DataFrame' object has no attribute 'ix'

输入:

df.loc[df.index[0],['AAPL']] = np.nan

df.loc[df.index[1],['GOOG','IBM']]=np.nan

df.loc[df.index[1:3],'MSFT']=np.nan

输出:

AAPL GOOG IBM MSFT

Date

2011-09-30 NaN 256.558350 130.822800 20.321293

2011-10-03 46.452591 NaN NaN NaN

2011-10-04 46.192177 250.012894 130.725555 NaN

2011-10-05 46.905209 251.407669 132.304108 NaN

2011-10-06 46.796078 256.393982 135.924973 21.505136

输入:

(df.AAPL + df.GOOG).head()

输出:

Date

2011-09-30 NaN

2011-10-03 NaN

2011-10-04 296.205070

2011-10-05 298.312878

2011-10-06 303.190060

dtype: float64

输入:

df.ffill().head()

输出:

AAPL GOOG IBM MSFT

Date

2011-09-30 NaN 256.558350 130.822800 20.321293

2011-10-03 46.452591 256.558350 130.822800 20.321293

2011-10-04 46.192177 250.012894 130.725555 20.321293

2011-10-05 46.905209 251.407669 132.304108 20.321293

2011-10-06 46.796078 256.393982 135.924973 21.505136

NaN

2011-10-04 296.205070

2011-10-05 298.312878

2011-10-06 303.190060

dtype: float64

输入:

```python

df.ffill().head()

输出:

AAPL GOOG IBM MSFT

Date

2011-09-30 NaN 256.558350 130.822800 20.321293

2011-10-03 46.452591 256.558350 130.822800 20.321293

2011-10-04 46.192177 250.012894 130.725555 20.321293

2011-10-05 46.905209 251.407669 132.304108 20.321293

2011-10-06 46.796078 256.393982 135.924973 21.505136