https://www.kaggle.com/c/house-prices-advanced-regression-techniques

0、模型准备

#Essentials

import pandas as pd

import numpy as np

#Plots

import seaborn as sns

import matplotlib.pyplot as plt

sns.set()

#Models

from sklearn import linear_model

from sklearn import svm

from sklearn import ensemble

import xgboost

import lightgbm

import os

os.environ["KMP_DUPLICATE_LIB_OK"]="TRUE"

from mlxtend.regressor import StackingCVRegressor

#Misc

from sklearn import model_selection

from sklearn import metrics

from sklearn import preprocessing

from sklearn import neighbors

from scipy.special import boxcox1p

from scipy.stats import boxcox_normmax

#ignore warnings

import warnings

warnings.filterwarnings("ignore")

# path='C:\\Users\\sunsharp\\Desktop\\kaggle\\house-pricing\\'

path=r'/Users/ranmo/Desktop/kaggle/house-pricing/'

#===========

# 函数定义

#===========

#1、训练模型

def model_eval(model,X_train,y_train):

l_rmes=[]

kf=model_selection.KFold(10,random_state=10)

for train,test in kf.split(X_train):

X_train1 = X_train.iloc[train]

y_train1 = y_train.iloc[train]

X_test1 = X_train.iloc[test]

y_test1 = y_train.iloc[test]

y_pred1=model.fit(X_train1,y_train1).predict(X_test1)

e=np.sqrt(metrics.mean_squared_error(y_pred1,y_test1)) #还要再转化为root值

l_rmes.append(e)

print(l_rmes)

print(np.mean(l_rmes))

print()

print()

return np.mean(l_rmes)

#2、模型预测

def model_predict(model,X_test,outpath):

y_test_pred=model.predict(X_test)

SalePrice_pred=np.floor(np.exp(y_test_pred))

df_reg=pd.DataFrame({'Id':X_test.index,'SalePrice':SalePrice_pred}).set_index('Id')

df_reg.to_csv('%stest_pred.csv'%outpath)

#看一下特征情况

df=pd.read_csv('%strain.csv'%path)

df=df.set_index('Id')

df['SalePrice']=np.log(df['SalePrice']) #直接在原数据进行处理了,方便之后的分析

df.columns

#看一下有无负值

df.describe().min() #无负值数据

#看一下非数值类的数据,需要进行独热编码

df.dtypes[df.dtypes==object]

df1=pd.get_dummies(df)

df.shape

df1.shape #由原始的81个特征扩展为289个特征

#检查缺失项,独热编码会把缺失项全编码为0,因此是不用考虑的

# 可以通过这样的方式来直接判断

# df[df.dtypes[df.dtypes!=object].index].info()

# 不好直接判断,也可以通过这样来判断

for i in df1.columns:

if df1[i].value_counts().sum()!=len(df1):

print(i)

#查看一下缺失项的具体详情:

# LotFrontage:Linear feet of street connected to property 物业到街道的距离

# MasVnrArea:Masonry veneer area in square feet 砌面贴面面积

# GarageYrBlt:Year garage was built 车库建成的日期

#处理缺失值

df1['LotFrontage']=df1['LotFrontage'].fillna(df['LotFrontage'].mean())

df1['MasVnrArea']=df1['MasVnrArea'].fillna(0)

df1['GarageYrBlt']=df1['GarageYrBlt'].fillna(df['GarageYrBlt'].mean())

#数据处理完,用xgboost跑一下基本模型

X_train=df1.sample(frac=1,random_state=10).drop('SalePrice',axis=1)

y_train=df1.sample(frac=1,random_state=10).SalePrice

#=============

#xgboost 跑一下基本模型

#=============

reg=xgboost.XGBRegressor(objective='reg:squarederror')

model_eval(reg,X_train,y_train)

image.png

#=============

#用基本模型跑一下训练集

#=============

df_test=pd.read_csv('%stest.csv'%path).set_index('Id')

#独热编码,这个必须联合train里的数据进行编码了,不然维度是不够的

temp=pd.concat([df,df_test],axis=0)

temp=temp[df.columns] #columns被打乱,重新排一下

temp=pd.get_dummies(temp)

df1_test=temp.loc[df_test.index.to_list()]

#缺失值处理

for i in df1_test.columns:

if df1_test[i].value_counts().sum()!=len(df1_test):

print(i)

#缺失值有点多,有比较多0值的都处理为0

df1_test['LotFrontage']=df1_test['LotFrontage'].fillna(df['LotFrontage'].mean())

df1_test['MasVnrArea']=df1_test['MasVnrArea'].fillna(0)

df1_test['BsmtFinSF1']=df1_test['BsmtFinSF1'].fillna(0)

df1_test['BsmtFinSF2']=df1_test['BsmtFinSF2'].fillna(0)

df1_test['BsmtUnfSF']=df1_test['BsmtUnfSF'].fillna(0)

df1_test['TotalBsmtSF']=df1_test['TotalBsmtSF'].fillna(0)

df1_test['BsmtFullBath']=df1_test['BsmtFullBath'].fillna(0)

df1_test['BsmtHalfBath']=df1_test['BsmtHalfBath'].fillna(0)

df1_test['GarageYrBlt']=df1_test['GarageYrBlt'].fillna(df['GarageYrBlt'].mean())

df1_test['GarageCars']=df1_test['GarageCars'].fillna(0)

df1_test['GarageArea']=df1_test['GarageArea'].fillna(0)

#用训练好的模型预测

X_test=df1_test.drop('SalePrice',axis=1)

if X_test.shape[1]==X_train.shape[1]:

print('ok')

# #模型预测

# outpath='%s//reg//1211//'%path

# reg.fit(X_train,y_train)

# model_predict(reg,X_test,outpath)

- 实际成绩13.971

一、EDA

1.1 目标值的偏态检测

#重新进行EDA探索

#销售价格分布

plt.figure(figsize=(8,7))

sns.distplot(df.SalePrice)

plt.grid(True)

print('偏度:%f'%df.SalePrice.skew()) #标准正太分布为0

print('峰度:%f'%df.SalePrice.kurt()) #标准正太分布为1

# 对原始数据去了对数之后,正好分布趋于正态分布

image.png

(因为已经做过对数处理了)

1.2 相关性检测

#数据相关性

corrmat=df.corr()

plt.figure(figsize=(15,15))

sns.heatmap(corrmat,linewidths=0.5)

image.png

#选取相关性最高的10个特征

corrmat_new=df[corrmat.nlargest(10,'SalePrice')['SalePrice'].index].corr()

plt.figure(figsize=(10,10))

sns.heatmap(corrmat_new,linewidths=0.5,annot=True)

image.png

(实际上针对高度线性相关的数据可能应该做处理,我这里没有做处理,在最后提出的优化方案那里会说一下。。)

sns.set()

sns.pairplot(df[['SalePrice', 'OverallQual', 'GrLivArea', 'GarageCars', 'TotalBsmtSF', 'FullBath', 'YearBuilt']])

#这里是只保留了部分特征,去掉了GarageArea、1stFloor、TotRmsAbvGrd

image.png

- 从上面的对图可以看出是存在离群点(异常点的),所以有必要把离群点筛选出来

1.3 离群点检测

#检测异常点,这个只是单纯靠样本分布的间隔来检测

def detect_outliers(x,k=5,plot=False,y=df.SalePrice,n=40):

x_new=x.dropna() #必须把空值去了

lof=neighbors.LocalOutlierFactor(n_neighbors=n)

lof.fit_predict(np.array(x_new).reshape(-1,1))

lof_scr = lof.negative_outlier_factor_

out_idx=x_new.index[pd.Series(lof_scr).sort_values()[:k].index] #因为去了空值之后index不对应了,所以要转化

if plot:

plt.figure(figsize=(10,8))

plt.scatter(x_new,y[x_new.index],c=np.exp(lof_scr), cmap='RdBu') #用指数是为了放大差距

return out_idx

- 附局部密度离群点检测:https://blog.csdn.net/wangyibo0201/article/details/51705966

# 以GrLivArea为例进行检测

#sns.set()

outs=detect_outliers(df.GrLivArea,plot=True)

#实际上 lof 离群检测中n的设置会影响结果,看一下n的合适取值

for i in range(10,70,5):

outs=detect_outliers(df.GrLivArea,n=i)

print('n=%d: %s'%(i, list(outs)))

image.png

#对所有数据维度进行lof 离群点检测,并判断其离群的次数

from collections import Counter

all_outliers=[]

numeric_features = df.drop('SalePrice',axis=1).dtypes[df.drop('SalePrice',axis=1).dtypes != 'object'].index

for i in numeric_features:

outs=detect_outliers(df[i]) #存在nan值情况

all_outliers.extend(outs)

print(Counter(all_outliers).most_common())

image.png

#一共检测出140个离群点,理论上出现次数越多的点,为离群点的概率就越大,这里用模型精度来检验

l_rems_list=[]

print('outlier_number=0:')

l_rems_list.append(model_eval(reg,X_train,y_train))

i=5

while i<=140:

outliers_list=Counter(all_outliers).most_common()[:i]

outliers_listid=pd.DataFrame(outliers_list,columns=['Id','times']).Id

#开始模型精度测试

print('outlier_number=%d:'%(i))

l_rems=model_eval(reg,X_train.drop(index=outliers_listid),y_train.drop(index=outliers_listid))

l_rems_list.append(l_rems)

i+=5

plt.figure(figsize=(10,6))

plt.plot(range(0,141,5),l_rems_list,)

plt.xlabel('outliers_number')

image.png

#粗筛异常点

from collections import Counter

numeric_features = df.drop('SalePrice',axis=1).dtypes[df.drop('SalePrice',axis=1).dtypes != 'object'].index

outliers_number=[]

l_rems_list1=[] #用剔除异常后的数据训练模型并自行测试

l_rems_list2=[] #用剔除异常后的数据训练模型并测试全部数据

print('k=0,outlier_number=0:')

l_rems=model_eval(reg,X_train,y_train)

l_rems_list1.append(l_rems)

l_rems_list2.append(l_rems)

for k in range(4,10,1):

all_outliers=[]

for i in numeric_features:

outs=detect_outliers(df[i],k=k)

all_outliers.extend(outs)

outliers_number.append(len(Counter(all_outliers).most_common()))

#将其全部剔除后进行模型测试

outliers_listid=pd.DataFrame(Counter(all_outliers).most_common(),columns=['Id','times']).Id

#开始模型精度测试

print('k=%d,outlier_number=%d:'%(k,len(Counter(all_outliers).most_common())))

l_rems1=model_eval(reg,X_train.drop(index=outliers_listid),y_train.drop(index=outliers_listid))

l_rems_list1.append(l_rems1)

l_rems2=np.sqrt(metrics.mean_squared_error(reg.fit(X_train.drop(index=outliers_listid),y_train.drop(index=outliers_listid)).predict(X_train),y_train))

l_rems_list2.append(l_rems2)

# plt

plt.figure(figsize=(10,6))

plt.plot([0,4,5,6,7,8,9],l_rems_list1)

plt.plot([0,4,5,6,7,8,9],l_rems_list2)

plt.xlabel('k_number')

image.png

#精筛异常点,k=4时,共有114个异常点

for i in numeric_features:

outs=detect_outliers(df[i],k=4) #存在nan值情况

all_outliers.extend(outs)

print(Counter(all_outliers).most_common())

l_rems_list1=[] #用剔除异常后的数据训练模型并自行测试

l_rems_list2=[] #用剔除异常后的数据训练模型并测试全部数据

print('outlier_number=0:')

l_rems=model_eval(reg,X_train,y_train)

l_rems_list1.append(l_rems)

l_rems_list2.append(l_rems)

i=5

while i<=114:

outliers_list=Counter(all_outliers).most_common()[:i]

outliers_listid=pd.DataFrame(outliers_list,columns=['Id','times']).Id

#开始模型精度测试

print('outlier_number=%d:'%(i))

l_rems1=model_eval(reg,X_train.drop(index=outliers_listid),y_train.drop(index=outliers_listid))

l_rems_list1.append(l_rems1)

l_rems2=np.sqrt(metrics.mean_squared_error(reg.fit(X_train.drop(index=outliers_listid),y_train.drop(index=outliers_listid)).predict(X_train),y_train))

l_rems_list2.append(l_rems2)

i+=5

# plt

plt.figure(figsize=(10,6))

plt.plot(range(0,114,5),l_rems_list1)

plt.plot(range(0,114,5),l_rems_list2)

plt.xlabel('outlier_number')

image.png

# 剔除20个异常点

# from collections import Counter

# all_outliers=[]

# numeric_features = df.drop('SalePrice',axis=1).dtypes[df.drop('SalePrice',axis=1).dtypes != 'object'].index

# for i in numeric_features:

# outs=detect_outliers(df[i]) #存在nan值情况

# all_outliers.extend(outs)

# print(Counter(all_outliers).most_common())

i=20

outliers_list=Counter(all_outliers).most_common()[:i]

outliers_listid=pd.DataFrame(outliers_list,columns=['Id','times']).Id

df_new=df.drop(index=outliers_listid)

X_train=df_new.sample(frac=1,random_state=10).drop('SalePrice',axis=1)

y_train=df_new.sample(frac=1,random_state=10).SalePrice

print(df_new.shape)

print(df.shape)

image.png

- 实际成绩由0.13971变为0.13634

二、特征工程

# 合并train和test,但同时要防止leak

df_new=df.drop(index=outliers_listid) #因为上面一步在测算模型的时候进行了填充,所以得重新更新下

df_feature=pd.concat([df_new,df_test],axis=0)

df_feature=df_feature[df_new.columns] #columns被打乱,重新排一下

df_feature

2.1 将不属于数值型的特征转化为字符串

df_feature.dtypes[df_feature.dtypes!=object] #依次对照,检查其是否不应该为数值型

image.png

df_feature['MSSubClass'] = df_feature['MSSubClass'].apply(str)

df_feature['YrSold'] = df_feature['YrSold'].astype(str)

df_feature['MoSold'] = df_feature['MoSold'].astype(str)

2.2 缺失值填充

#2.2 缺失值填充

df_feature.isnull().any()[df_feature.isnull().any()] #查看样本说明确定那些是允许缺失的特征(该样本没有这项特征)

special_features=['Alley','BsmtQual','BsmtCond','BsmtExposure','BsmtFinType1','BsmtFinType2','FireplaceQu',

'GarageType','GarageFinish','GarageQual','GarageCond','PoolQC','Fence','MiscFeature']

features_missing=list(df_feature.isnull().any()[df_feature.isnull().any()].index)

for i in special_features:

features_missing.remove(i)

print(len(features_missing))

features_missing

image.png

#顺便看一下train数据中缺失项

features_missing_train=list(df_new.isnull().any()[df_new.isnull().any()].index)

for i in special_features:

try:

features_missing_train.remove(i)

except:

continue

print(len(features_missing_train))

features_missing_train

image.png

# 缺失值填充的函数定义

#中间会涉及到数据泄露,因为没有严格剥离

def feature_missing(df,feature,feature_refer=None,method='mode'):

#数值型的method=[0,'mean','median']

#非数值型的method=['mode']

if feature_refer==None:

if method=='mode':

return df[feature].fillna(df[feature].value_counts().index[0]) #返回众数

if method==0:

return df[feature].fillna(0) #返回0

if method=='mean':

return df[feature].describe()['mean']

if method=='median':

return df[feature].describe()['50%']

else:

df[feature_refer]=feature_missing(df,feature=feature_refer) #参考列不能有空值,按众数填充

if method=='mean':

return df.groupby(feature_refer)[feature].transform(lambda x:x.fillna(x.mean()))

if method=='mode':

return df.groupby(feature_refer)[feature].transform(lambda x:x.fillna(x.mode()[0]))

if method=='median':

return df.groupby(feature_refer)[feature].transform(lambda x:x.fillna(x.median()))

def feature_corr(df,feature,k=10):

corrmat=df.corr()

corrmat_feature=df[corrmat.nlargest(k,feature)[feature].index].corr()

plt.figure(figsize=(10,10))

sns.heatmap(corrmat_feature,linewidths=0.5,annot=True)

def fillmethod_eval(model,df,feature,method_list,feature_refer_list=None): #feature_refer和method_list都必须是list形式

#数值型的method=[0,'mean','median']

#非数值型的method=['mode']

if feature_refer_list==None:

for i in method_list:

df_eval=df

#第一步填充,第二步测评

df_eval[feature]=feature_missing(df,feature,method=i)

df_eval=pd.get_dummies(df_eval)

print('method:%s'%(i))

model_eval(model,df_eval.sample(frac=1,random_state=10).drop('SalePrice',axis=1),df_eval.sample(frac=1,random_state=10).SalePrice)

else:

for j in feature_refer_list:

for i in method_list:

try: #因为数值型没有mode,非数值型没有mean和median

df_eval=df

#第一步填充,第二步测评

df_eval[feature]=feature_missing(df,feature,feature_refer=j,method=i)

df_eval=pd.get_dummies(df_eval)

print('refre:%s ,method:%s'%(j,i))

model_eval(model,df_eval.sample(frac=1,random_state=10).drop('SalePrice',axis=1),df_eval.sample(frac=1,random_state=10).SalePrice)

except:

continue

image.png

- 所以其实我是基于模型测试结果来进行填充,主要是三种办法:1、如果有相关性很高的,则用相关性很高的变量来填充;2、用自己的均值、中位数等等来填充;三、用其他变量的分组的均值、中无数等来填充

# train缺失特征填充

#MasVnrType和MasVnrArea

df_feature['MasVnrType']=df_feature['MasVnrType'].fillna('None')

df_feature['MasVnrArea']=df_feature['MasVnrArea'].fillna(0)

#LotFrontage

# feature_corr(df_feature,'LotFrontage') #没有很强相关性的

print('no refer:')

fillmethod_eval(reg,df_feature[:1440],'LotFrontage',method_list=[0,'mean','median'])

print('refer:')

fillmethod_eval(reg,df_feature[:1440],'LotFrontage',method_list=['mode','mean','median'],

feature_refer_list=['MSZoning','LotArea','Street','Alley','Neighborhood','Condition1'])

#结论:refre:street ,method:mean

#LotFrontage

df_feature[:1440].groupby('Street')['LotFrontage'].agg(lambda x: np.mean(pd.Series.mode(x))) #数值型groupby的众数读取

for i in df_feature.index:

if str(df_feature.loc[i,'LotFrontage'])=='nan': #配合列的名称则必须用loc

if df_feature.loc[i,'Street']=='Grvl':

df_feature.loc[i,'LotFrontage']=90.25

else:

df_feature.loc[i,'LotFrontage']=60.00

#Electrical

print('no refer:')

fillmethod_eval(reg,df_feature[:1440],'Electrical',method_list=['mode'])

print('refer:')

fillmethod_eval(reg,df_feature[:1440],'Electrical',method_list=['mode'],

feature_refer_list=['Heating','HeatingQC','CentralAir'])

#结论:refre:CentralAir ,method:mode

#Electrical

df_feature[:1440].groupby('CentralAir')['Electrical'].describe() #非数值型groupby的众数读取

df_feature['Electrical'].fillna('SBrkr')

#GarageYrBlt

feature_corr(df_feature,'GarageYrBlt') #有强相关性的

df_feature[['GarageYrBlt','YearBuilt']] #查看,基本上GarageYrBlt=YearBuilt

for i in df_feature.index:

if str(df_feature.loc[i,'GarageYrBlt'])=='nan': #配合列的名称则必须用loc

df_feature.loc[i,'GarageYrBlt']=df_feature.loc[i,'YearBuilt']

#结论:GarageYrBlt=YearBuilt

image.png

df_feature['MSZoning']=feature_missing(df_feature,feature='MSZoning',feature_refer='MSSubClass',method='mode')

df_feature['Utilities']=feature_missing(df_feature,feature='Utilities',method='mode')

for i in df_feature.index:

if str(df_feature.loc[i,'Exterior1st'])=='nan': #配合列的名称则必须用loc

df_feature.loc[i,'Exterior1st']=df_feature.loc[i,'Exterior2nd']

for i in df_feature.index:

if str(df_feature.loc[i,'Exterior2nd'])=='nan': #配合列的名称则必须用loc

df_feature.loc[i,'Exterior2nd']=df_feature.loc[i,'Exterior1st']

# df_feature['Exterior1st'].value_counts().sum()

# df_feature['Exterior2nd'].value_counts().sum()

# 检查出来还剩一项空值,用众数填充

df_feature['Exterior1st']=feature_missing(df_feature,feature='Exterior1st',method='mode')

df_feature['Exterior2nd']=feature_missing(df_feature,feature='Exterior2nd',method='mode')

# df_feature.BsmtFinSF1[df_feature.BsmtFinSF1.isnull()]

# df_feature.BsmtFinSF2[df_feature.BsmtFinSF2.isnull()]

# df_feature[['BsmtQual','BsmtCond','BsmtFinSF1','BsmtFinSF2']].loc[2121]

#检查出来其实是0值

df_feature['BsmtFinSF1']=df_feature['BsmtFinSF1'].fillna(0)

df_feature['BsmtFinSF2']=df_feature['BsmtFinSF2'].fillna(0)

df_feature['BsmtUnfSF']=df_feature['BsmtUnfSF'].fillna(0)

df_feature['TotalBsmtSF']=df_feature['TotalBsmtSF'].fillna(0)

df_feature['BsmtFullBath']=df_feature['TotalBsmtSF'].fillna(0)

df_feature['BsmtHalfBath']=df_feature['TotalBsmtSF'].fillna(0)

df_feature['KitchenQual']=feature_missing(df_feature,feature='KitchenQual',method='mode')

df_feature['Functional']=feature_missing(df_feature,feature='Functional',method='mode')

#feature_corr(df_feature,'GarageCars') #GarageCars和GarageArea强相关,但正好两个都是空值,但偏偏又有车库。。。

# df_feature.GarageArea[df_feature.GarageArea.isnull()]

# df_feature.GarageCars[df_feature.GarageCars.isnull()]

# df_feature.GarageType[df_feature.GarageCars.isnull()]

df_feature['GarageCars']=feature_missing(df_feature,feature='GarageCars',method='mode')

df_feature['GarageArea']=feature_missing(df_feature,feature='GarageArea',method='mode')

df_feature['SaleType']=feature_missing(df_feature,feature='SaleType',method='mode')

- 实际成绩由0.13634降为0.13596,说明缺失值填充对模型精度提高很有限,而且在填充过程中你并不能确定哪一种方法是最好的。

2.3 数据偏度矫正

#数值型数据列偏度矫正

df_feature3=df_feature

highskew_index=df_feature3[numeric_features].skew()[df_feature3[numeric_features].skew() >0.15].index

#将偏度大于0.15的进行矫正,实际上根据测试,选哪个阈值进行矫正,影响都不大

for i in highskew_index:

df_feature3[i] = boxcox1p(df_feature3[i], boxcox_normmax(df_feature3[i] + 1))

2.4 特征删除

#特征删除

df_feature3.Utilities.value_counts()

df_feature3.Street.value_counts()

df_feature3.PoolQC.value_counts()

df_feature3.Fence.value_counts()

df_feature3.FireplaceQu.value_counts()

df_feature3.MiscFeature.value_counts()

#上面几个特征缺失率都太高了

df_feature5=df_feature3.drop(['Utilities', 'Street', 'PoolQC','MiscFeature', 'Alley', 'Fence'], axis=1)

2.5 融合生成新特征(其实应该最后来做这个步骤)

#融合生成新特征

#根据直觉进行的融合

df_feature6=df_feature5.copy() #为什么一定要copy???不用copy,对df_feature6的更改会影响df_feature5.。。疑问??

df_feature6['HasWoodDeck'] = (df_feature6['WoodDeckSF'] == 0) * 1

df_feature6['HasOpenPorch'] = (df_feature6['OpenPorchSF'] == 0) * 1

df_feature6['HasEnclosedPorch'] = (df_feature6['EnclosedPorch'] == 0) * 1

df_feature6['Has3SsnPorch'] = (df_feature6['3SsnPorch'] == 0) * 1

df_feature6['HasScreenPorch'] = (df_feature6['ScreenPorch'] == 0) * 1

df_feature6['YearsSinceRemodel'] = df_feature6['YrSold'].astype(int) - df_feature6['YearRemodAdd'].astype(int)

df_feature6['Total_Home_Quality'] = df_feature6['OverallQual'] + df_feature6['OverallCond']

df_feature6['TotalSF'] = df_feature6['TotalBsmtSF'] + df_feature6['1stFlrSF'] + df_feature6['2ndFlrSF']

df_feature6['YrBltAndRemod'] = df_feature6['YearBuilt'] + df_feature6['YearRemodAdd']

df_feature6['Total_sqr_footage'] = (df_feature6['BsmtFinSF1'] + df_feature6['BsmtFinSF2'] +

df_feature6['1stFlrSF'] + df_feature6['2ndFlrSF'])

df_feature6['Total_Bathrooms'] = (df_feature6['FullBath'] + (0.5 * df_feature6['HalfBath']) +

df_feature6['BsmtFullBath'] + (0.5 * df_feature6['BsmtHalfBath']))

df_feature6['Total_porch_sf'] = (df_feature6['OpenPorchSF'] + df_feature6['3SsnPorch'] +

df_feature6['EnclosedPorch'] + df_feature6['ScreenPorch'] +

df_feature6['WoodDeckSF'])

df_feature6['YrBltAndRemod']=df_feature6['YearBuilt']+df_feature6['YearRemodAdd']

df_feature6['TotalSF']=df_feature6['TotalBsmtSF'] + df_feature6['1stFlrSF'] + df_feature6['2ndFlrSF']

df_feature6['Total_sqr_footage'] = (df_feature6['BsmtFinSF1'] + df_feature6['BsmtFinSF2'] +

df_feature6['1stFlrSF'] + df_feature6['2ndFlrSF'])

df_feature6['Total_Bathrooms'] = (df_feature6['FullBath'] + (0.5 * df_feature6['HalfBath']) +

df_feature6['BsmtFullBath'] + (0.5 * df_feature6['BsmtHalfBath']))

df_feature6['Total_porch_sf'] = (df_feature6['OpenPorchSF'] + df_feature6['3SsnPorch'] +

df_feature6['EnclosedPorch'] + df_feature6['ScreenPorch'] +

df_feature6['WoodDeckSF'])

2.6 简化特征(应该在特征融合之间)

#简化特征,对于某些分布单调(比如100个数据中有99个的数值是0.9,另1个是0.1)的数字型数据列,进行01取值处理。

#要确保其他字段没有包含这部分信息,比如有一个字段专门表示有无pool的,那就不用额外生成

df_feature7=df_feature6.copy()

df_feature7['haspool'] = df_feature7['PoolArea'].apply(lambda x: 1 if x > 0 else 0)

df_feature7['has2ndfloor'] = df_feature7['2ndFlrSF'].apply(lambda x: 1 if x > 0 else 0)

df_feature7['hasgarage'] = df_feature7['GarageArea'].apply(lambda x: 1 if x > 0 else 0)

df_feature7['hasbsmt'] = df_feature7['TotalBsmtSF'].apply(lambda x: 1 if x > 0 else 0)

df_feature7['hasfireplace'] = df_feature7['Fireplaces'].apply(lambda x: 1 if x > 0 else 0)

2.7 删除单一特征

#get_dummies并删除单一特征(比如某个值出现了99%以上)的特征

print("before get_dummies:",df_feature7.shape)

df_feature_final = pd.get_dummies(df_feature7)

print("after get_dummies:",df_feature_final.shape)

X_train=df_feature_final.iloc[:1440].sample(frac=1,random_state=10).drop('SalePrice',axis=1)

y_train=pd.DataFrame(df_feature_final.iloc[:1440].sample(frac=1,random_state=10).SalePrice) #不然会变成series

X_test=df_feature_final.iloc[1440:].drop('SalePrice',axis=1)

##删除单一特征,但模型结果无差异,毕竟xgboost本身就具备筛掉不重要的特征的功能,所以这里不进行单一特征删除

# for thre in np.arange(99.8,100,0.02):

# overfit = []

# for i in X_train.columns:

# counts = X_train[i].value_counts()

# zeros = counts.iloc[0]

# if zeros / len(X_train) * 100 > thre: #99.94是可以调整的,80,90,95,99...

# overfit.append(i)

# print('thre',thre)

# print(overfit)

# model_eval(reg,X_train.drop(overfit,axis=1),y_train)

print('X_train', X_train.shape, 'y_train', y_train.shape, 'X_test', X_test.shape)

print('feature engineering finished!')

image.png

- 删除单一特征和简化特征都是一样的目的,只不过删除单一特征是在get_dummies之后再删除了一次,删除的是独热编码特征。

2.8 结论

X_train.to_csv('%sX_train.csv'%path)

y_train.to_csv('%sy_train.csv'%path)

X_test.to_csv('%sX_test.csv'%path)

- 特征工程里面最有效的步骤是异常值筛选,然后把原始的0.139的成绩提升为0.133~0.135之间

三、训练模型

X_train=pd.read_csv('%sX_train.csv'%path,index_col='Id')

y_train=pd.read_csv('%sy_train.csv'%path,index_col='Id')

X_test=pd.read_csv('%sX_test.csv'%path,index_col='Id')

# 函数定义:

def find_cv(model,X_train,y_train,param_test):

model_cv=model_selection.GridSearchCV(model,param_test,cv=10,n_jobs=-1,scoring='neg_mean_squared_error')

model_cv.fit(X_train,y_train)

print("model_cv.cv_results_['mean_test_score']:=%s"%np.sqrt(-model_cv.cv_results_['mean_test_score'])) #结果是开根号值

print()

print(np.sqrt(-model_cv.best_score_))

print(model_cv.best_params_)

3.1 lasso

# lasso win

model=linear_model.Lasso(0.00037,random_state=10)

model_eval(model,X_train,y_train)

#模型预测

outpath='%s//reg//1220//lasso//'%path

model_predict(model.fit(X_train,y_train),X_test,outpath)

#实际成绩 0.11658

3.2 ridge

# ridge

model=linear_model.Ridge(9,random_state=10)

model_eval(model,X_train,y_train)

#模型预测

outpath='%s//reg//1220//ridge//'%path

y_test_pred=model.fit(X_train,y_train).predict(X_test)

SalePrice_pred=np.exp(y_test_pred)

df_reg=pd.DataFrame({'Id':X_test.index,'SalePrice':SalePrice_pred2.reshape(1,-1)[0]}).set_index('Id') #ridge模型自己怪。。生成的结果不是标准格式

df_reg.to_csv('%stest_pred.csv'%outpath)

#实际成绩 0.11668

3.3 ela

model=linear_model.ElasticNet(0.00039,0.95,random_state=10)

model_eval(model,X_train,y_train)

#模型预测

outpath='%s//reg//1220//ela//'%path

model_predict(model.fit(X_train,y_train),X_test,outpath)

#实际成绩 0.11775

3.4 svr

model=svm.SVR(gamma=1e-08,C=125000)

model_eval(model,X_train,y_train)

#模型预测

outpath='%s//reg//1220//svr//'%path

model_predict(model.fit(X_train,y_train),X_test,outpath)

#实际成绩 0.12521

- svr C值过大,怀疑是因为数据没有进行归一化导致的。。。

3.5 GDBT

model=ensemble.GradientBoostingRegressor(

max_depth=3,

min_weight_fraction_leaf=0.004,

min_impurity_split=0,

subsample=0.82,

max_features=0.45,

n_estimators=480,

learning_rate=0.064,

random_state=10

)

# model_eval(model,X_train,y_train)

#模型预测

outpath='%s//reg//1220//gdbt//'%path

model_predict(model.fit(X_train,y_train),X_test,outpath)

#实际成绩 0.13023

3.6 lgbm

model=lightgbm.LGBMRegressor(random_state=10,

max_depth=8,

num_leaves=11,

min_child_samples=20,

min_child_weight=0,

min_split_gain=0,

subsample=0.8,

colsample_bytree=0.24,

subsample_freq=1,

reg_alpha=0.0009,

reg_lambda=0.00088,

learning_rate=0.006,

n_estimators=2550

)

model_eval(model,X_train,y_train)

#模型预测

outpath='%s//reg//1220//lgbm//'%path

model_predict(model.fit(X_train,y_train),X_test,outpath)

#实际成绩 0.12411

3.7 xgbt

model=xgboost.XGBRegressor(random_state=10,

max_depth=6,

min_child_weight=6,

min_split_gain=6,

subsample=0.77,

colsample_bytree=0.62,

reg_alpha=1e-5,

reg_lambda=1,

n_estimators=150,

learning_rate=0.1,

)

model_eval(model,X_train,y_train)

#模型预测

outpath='%s//reg//1220//xgbt//'%path

model_predict(model.fit(X_train,y_train),X_test,outpath)

#实际成绩 0.12839

四、stacking

lasso=linear_model.Lasso(0.00037,random_state=10)

ridge=linear_model.Ridge(9,random_state=10)

ela=linear_model.ElasticNet(0.00039,0.95,random_state=10)

svr=svm.SVR(gamma=1e-08,C=125000)

gdbt=ensemble.GradientBoostingRegressor(

max_depth=3,

min_weight_fraction_leaf=0.004,

min_impurity_split=0,

subsample=0.82,

max_features=0.45,

n_estimators=480,

learning_rate=0.064,

random_state=10

)

lgbm=lightgbm.LGBMRegressor(random_state=10,

max_depth=8,

num_leaves=11,

min_child_samples=20,

min_child_weight=0,

min_split_gain=0,

subsample=0.8,

colsample_bytree=0.24,

subsample_freq=1,

reg_alpha=0.0009,

reg_lambda=0.00088,

learning_rate=0.006,

n_estimators=2550

)

xgbt=xgboost.XGBRegressor(random_state=10,

max_depth=6,

min_child_weight=6,

min_split_gain=6,

subsample=0.77,

colsample_bytree=0.62,

reg_alpha=1e-5,

reg_lambda=1,

n_estimators=150,

learning_rate=0.1,

)

4.1 第二层模型采用原始特征

reg_stack=StackingCVRegressor(regressors=lasso,meta_regressor=lasso,random_state=10,use_features_in_secondary=True)

param_test = {

'regressors':[(lasso,ridge,ela,svr,gdbt,lgbm)],

'meta_regressor':[lasso,ridge,ela,svr,gdbt,lgbm,xgbt]

}

find_cv(reg_stack,X_train,y_train,param_test)

model=StackingCVRegressor(regressors=(lasso,ridge,ela,svr,gdbt,lgbm),

meta_regressor=ridge,random_state=10,use_features_in_secondary=True)

model_eval(model,X_train,y_train)

#模型预测

outpath='%s//reg//1220//stack//ridge'%path

model_predict(model.fit(X_train,y_train),X_test,outpath)

#实际成绩 0.11689

4.2 第二层模型不采用原始特征

第二层不采用原始特征,则meta_regressor自然也不用采用之前网格寻优得到的模型

#单模型stacking,第二层不用特征量,但是混合模型是默认模型,如果可以的话,还可以对第二层网格进行寻优

reg_stack=StackingCVRegressor(regressors=lasso,meta_regressor=lasso,random_state=10,use_features_in_secondary=False)

param_test = {

'regressors':[(lasso,ridge,ela,svr,gdbt,lgbm)],

'meta_regressor':[linear_model.Lasso(random_state=10),

linear_model.Ridge(random_state=10),

linear_model.ElasticNet(random_state=10),

svm.SVR(),

ensemble.GradientBoostingRegressor(random_state=10),

lightgbm.LGBMRegressor(random_state=10),

xgboost.XGBRegressor(random_state=10)]

}

find_cv(reg_stack,X_train,y_train,param_test)

model=StackingCVRegressor(regressors=(lasso,ridge,ela,svr,gdbt,lgbm),

meta_regressor=ridge,random_state=10,use_features_in_secondary=True)

model_eval(model,X_train,y_train)

#模型预测

outpath='%s//reg//1220//stack//ridge'%path

model_predict(model.fit(X_train,y_train),X_test,outpath)

#实际成绩 0.11689

五、blending

lasso=linear_model.Lasso(0.00037,random_state=10)

ridge=linear_model.Ridge(9,random_state=10)

ela=linear_model.ElasticNet(0.00039,0.95,random_state=10)

svr=svm.SVR(gamma=1e-08,C=125000)

gdbt=ensemble.GradientBoostingRegressor(

max_depth=3,

min_weight_fraction_leaf=0.004,

min_impurity_split=0,

subsample=0.82,

max_features=0.45,

n_estimators=480,

learning_rate=0.064,

random_state=10

)

lgbm=lightgbm.LGBMRegressor(random_state=10,

max_depth=8,

num_leaves=11,

min_child_samples=20,

min_child_weight=0,

min_split_gain=0,

subsample=0.8,

colsample_bytree=0.24,

subsample_freq=1,

reg_alpha=0.0009,

reg_lambda=0.00088,

learning_rate=0.006,

n_estimators=2550

)

xgbt=xgboost.XGBRegressor(random_state=10,

max_depth=6,

min_child_weight=6,

min_split_gain=6,

subsample=0.77,

colsample_bytree=0.62,

reg_alpha=1e-5,

reg_lambda=1,

n_estimators=150,

learning_rate=0.1,

)

stack=StackingCVRegressor(regressors=(lasso,ridge,ela,svr,gdbt,lgbm),

meta_regressor=ridge,random_state=10)

def linear_blend_models_predict(models,X_train,y_train,X_test,coefs):

tmp=[np.array(model.fit(X_train,y_train).predict(X_test)).reshape(1,-1)[0] for model in models] #ridge输出格式问题

tmp =[c*d for c,d in zip(coefs,tmp)]

pres=np.array(tmp).swapaxes(0,1) #numpy中的reshape不能用于交换维度,一开始的种种问题,皆由此来

pres=np.sum(pres,axis=1)

return pres

def blend_model_eval(models,X_train,y_train,coefs,):

l_rmes=[]

kf=model_selection.KFold(10,random_state=10)

for train,test in kf.split(X_train):

X_train1 = X_train.iloc[train]

y_train1 = y_train.iloc[train]

X_test1 = X_train.iloc[test]

y_test1 = y_train.iloc[test]

y_pred1=linear_blend_models_predict(models,X_train1,y_train1,X_test1,coefs)

e=np.sqrt(metrics.mean_squared_error(y_pred1,y_test1)) #还要再转化为root值

l_rmes.append(e)

print(l_rmes)

print(np.mean(l_rmes))

print()

print()

return np.mean(l_rmes)

def blend_model_predict(models,X_train,y_train,X_test,coefs,outpath):

y_test_pred=linear_blend_models_predict(models,X_train,y_train,X_test,coefs)

SalePrice_pred=np.floor(np.exp(y_test_pred))

df_reg=pd.DataFrame({'Id':X_test.index,'SalePrice':SalePrice_pred}).set_index('Id')

df_reg.to_csv('%stest_pred.csv'%outpath)

image.png

5.1 基础模型blend

models=[lasso,ridge,ela,svr,gdbt,lgbm,xgbt,stack]

print('1')

models=[lasso,ridge,ela]

coefs=[1,1,1]/np.sum([1,1,1])

blend_model_eval(models,X_train,y_train,coefs)

outpath='%s//reg//1220//blend//1//'%path

blend_model_predict(models,X_train,y_train,X_test,coefs,outpath)

#0.11619

print('2')

models=[gdbt,lgbm,xgbt]

coefs=[1,1,1]/np.sum([1,1,1])

blend_model_eval(models,X_train,y_train,coefs)

outpath='%s//reg//1220//blend//2//'%path

blend_model_predict(models,X_train,y_train,X_test,coefs,outpath)

#0.12502

print('3')

models=[lasso,ridge,ela,stack]

coefs=[1,1,1,1]/np.sum([1,1,1,1])

blend_model_eval(models,X_train,y_train,coefs)

outpath='%s//reg//1220//blend//3//'%path

blend_model_predict(models,X_train,y_train,X_test,coefs,outpath)

#0.11605

print('4')

models=[lasso,ridge,ela,stack,lgbm,svr]

coefs=[1,1,1,1,0.8,0.8]/np.sum([1,1,1,1,0.8,0.8])

blend_model_eval(models,X_train,y_train,coefs)

outpath='%s//reg//1220//blend//4//'%path

blend_model_predict(models,X_train,y_train,X_test,coefs,outpath)

#0.11604

print('5')

models=[lasso,ridge,ela,stack,lgbm,svr,xgbt]

coefs=[1,1,1,1,0.8,0.8,0.6]/np.sum([1,1,1,1,0.8,0.8,0.6])

blend_model_eval(models,X_train,y_train,coefs)

outpath='%s//reg//1220//blend//5//'%path

blend_model_predict(models,X_train,y_train,X_test,coefs,outpath)

#0.11621

print('6')

models=[lasso,ridge,ela,stack,lgbm,svr,xgbt,gdbt]

coefs=[1,1,1,1,0.8,0.8,0.6,0.5]/np.sum([1,1,1,1,0.8,0.8,0.6,0.5])

blend_model_eval(models,X_train,y_train,coefs)

outpath='%s//reg//1220//blend//6//'%path

blend_model_predict(models,X_train,y_train,X_test,coefs,outpath)

#0.11664

print('7')

models=[lasso,ridge,ela,stack,lgbm,svr,xgbt,gdbt]

coefs=[1.5,1,1,1,0.8,0.8,0.6,0.3]/np.sum([1.5,1,1,1,0.8,0.8,0.6,0.3])

blend_model_eval(models,X_train,y_train,coefs)

outpath='%s//reg//1220//blend//7//'%path

blend_model_predict(models,X_train,y_train,X_test,coefs,outpath)

#0.11634

image.png

5.2 top kernel mix

sub1=pd.read_csv('%s//reg//1220//lasso//test_pred.csv'%path).set_index('Id')

sub2=pd.read_csv('%s//reg//1220//ridge//test_pred.csv'%path).set_index('Id')

sub3=pd.read_csv('%s//reg//1220//stack//ridge//2//test_pred.csv'%path).set_index('Id')

sub4=pd.read_csv('%s//reg//1220//blend//3//test_pred.csv'%path).set_index('Id')

sub5=pd.read_csv('%s//reg//1220//blend//4//test_pred.csv'%path).set_index('Id')

outpath='%s//reg//1220//blendtop//1//'%path

SalePrice_pred=np.floor(0.25*(sub1.SalePrice)+0.25*(sub2.SalePrice)+0.25*(sub3.SalePrice)+0.25*(sub4.SalePrice))

df_reg=pd.DataFrame({'Id':X_test.index,'SalePrice':SalePrice_pred}).set_index('Id')

df_reg.to_csv('%stest_pred.csv'%outpath)

#0.11613

outpath='%s//reg//1220//blendtop//2//'%path

SalePrice_pred=np.floor(0.2*(sub1.SalePrice)+0.2*(sub2.SalePrice)+0.2*(sub3.SalePrice)+0.2*(sub4.SalePrice)+0.2*(sub5.SalePrice))

df_reg=pd.DataFrame({'Id':X_test.index,'SalePrice':SalePrice_pred}).set_index('Id')

df_reg.to_csv('%stest_pred.csv'%outpath)

#0.11601

outpath='%s//reg//1220//blendtop//3//'%path

SalePrice_pred=np.floor(0.5*(sub4.SalePrice)+0.5*(sub5.SalePrice))

df_reg=pd.DataFrame({'Id':X_test.index,'SalePrice':SalePrice_pred}).set_index('Id')

df_reg.to_csv('%stest_pred.csv'%outpath)

#0.11590

outpath='%s//reg//1220//blendtop//5//'%path

SalePrice_pred=np.floor(0.2*(sub1.SalePrice)+0.1*(sub2.SalePrice)+0.1*(sub3.SalePrice)+0.3*(sub4.SalePrice)+0.3*(sub5.SalePrice))

df_reg=pd.DataFrame({'Id':X_test.index,'SalePrice':SalePrice_pred}).set_index('Id')

df_reg.to_csv('%stest_pred.csv'%outpath)

#0.11595

- 历史最优成绩0.11590

六、最后调整

根据一些参考理论:让超低的房价更低,让超高的房价更高(通常来说,会将小者放大,大者缩小,但房价有其特殊性:有些偏远地区的房子比预测更低。但实际上并未取得更好地效果

#让超低的房价更低,让超高的房价更高(通常来说,会将小者放大,大者缩小,但房价有其特殊性:有些偏远地区的房子比预测更低,

outpath='%s//reg//1220//submission//3//'%path

submission=pd.read_csv('%s//reg//1220//blendtop//2//test_pred.csv'%path).set_index('Id')

q1 = submission['SalePrice'].quantile(0.0045)

q2 = submission['SalePrice'].quantile(0.998)

submission['SalePrice'] = submission['SalePrice'].apply(lambda x: x if x > q1 else x*0.84)

submission['SalePrice'] = submission['SalePrice'].apply(lambda x: x if x < q2 else x*1.05)

submission.to_csv('%stest_pred.csv'%outpath)

#0.11647

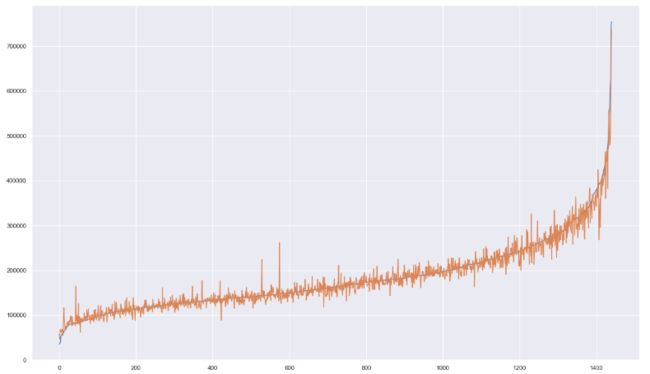

x=list(range(len(y_train)))

y1=np.exp(y_train.SalePrice).sort_values()

y2=np.exp(y_train_pred.loc[np.exp(y_train.SalePrice).sort_values().index])

sns.set()

plt.figure(figsize=(20,12))

plt.plot(x,y1)

plt.plot(x,y2)

image.png

- 所以从训练集中可以看出,预测的结果和实际结果在末尾和订单的偏差,有大也有小,有高也有低。

- 所以尝试用训练集自己的结果,来确定是应该增加还是减少,增加和减少的比率又是多少:

#对down进行操作,关键列表:q_down_list,coef_down_list,rmse_down_min_list

q_down=[0]

rmse=np.sqrt(metrics.mean_squared_error(np.log(y2),np.log(y1)))

rmse_down_min_list=[rmse]

q_down_list=[0]

coef_down_list=[]

y_temp=y2.copy()

# for i in np.arange(0,0.1,0.0005):

for i in np.arange(0,0.1,0.0005):

q_down.append(y2['SalePrice'].quantile(i))

rmse_temp=[]

for j in np.arange(0.3,3,0.01):

a = y_temp['SalePrice'].apply(lambda x: x if x >= q_down[-1] or x <= q_down[-2] else x*j)

rmse_temp.append(np.sqrt(metrics.mean_squared_error(np.log(a),np.log(y1))))

temp=rmse_temp-rmse_down_min_list[-1]

if temp.min()<0:

q_down_list.append(y2['SalePrice'].quantile(i))

rmse_down_min_list.append(np.array(rmse_temp).min())

coef_down_list.append(list(np.arange(0.3,3,0.01))[np.array(rmse_temp).argmin()])

y_temp['SalePrice'] = y_temp['SalePrice'].apply(lambda x: x if x >= q_down_list[-1] or x <= q_down_list[-2] else x*coef_down_list[-1])

#对up进行操作,,关键列表:q_up_list,coef_up_list,rmse_up_min_list

q_up=[0]

rmse=np.sqrt(metrics.mean_squared_error(np.log(y2),np.log(y1)))

rmse_up_min_list=[rmse]

q_up_list=[0]

coef_up_list=[]

y_temp=y2.copy()

# for i in np.arange(0,0.1,0.0005):

for i in np.arange(0,0.1,0.0005):

q_up.append(y2['SalePrice'].quantile(1-i))

rmse_temp=[]

for j in np.arange(0.3,3,0.01):

a = y_temp['SalePrice'].apply(lambda x: x if x <= q_up[-1] or x >= q_up[-2] else x*j)

rmse_temp.append(np.sqrt(metrics.mean_squared_error(np.log(a),np.log(y1))))

temp=rmse_temp-rmse_up_min_list[-1]

if temp.min()<0:

q_up_list.append(y2['SalePrice'].quantile(1-i))

rmse_up_min_list.append(np.array(rmse_temp).min())

coef_up_list.append(list(np.arange(0.3,3,0.01))[np.array(rmse_temp).argmin()])

y_temp['SalePrice'] = y_temp['SalePrice'].apply(lambda x: x if x <= q_up_list[-1] or x >= q_up_list[-2] else x*coef_up_list[-1])

#调整边缘房价

outpath='%s//reg//1220//submission//5//'%path

submission=pd.read_csv('%s//reg//1220//blendtop//3//test_pred.csv'%path).set_index('Id')

for i in range(len(q_down_list)-1):

submission['SalePrice']=submission['SalePrice'].apply(lambda x: x if x >= q_down_list[i+1] or x <= q_down[i] else x*coef_down_list[i])

submission.to_csv('%stest_pred.csv'%outpath)

#0.12527

- 但是调整结果很不理想。。。

七、结论

大概从stack开始就没有起到很好的优化效果,最终结果0.1159和lasso的0.11658提升有限。。思考了一下,可能有以下几个方面还可以优化: