lecture 9:分类变量回归

先学习这个这个资料

分类变量回归——Probit和Logit(附代码)

以下两个网页上均有heckman的代码,以日本教师的优先考虑。

https://pypi.org/project/py4etrics/官方安装地址

https://github.com/Py4Etrics

https://github.com/vnery5/Econometria

https://lost-stats.github.io/Model_Estimation/GLS/heckman_correction_model.html

https://rlhick.people.wm.edu/stories/econ_407_notes_heckman.html

https://econ.pages.code.wm.edu/407/notes/docs/mle_heckman.html

Heckman 两阶段模型:

Heckman两阶段模型解决的是样本选择偏差(sample selection bias)的问题。样本选择偏差指的是我们在回归方程中估计出的参数是基于那些被选择进样本了的数据点(或者说是能够观测得到的数据点)而得出的。如果说一个数据点(观测值)是不是被选择进样本是一个外生的、纯随机的事件,那么我们据此得出的参数并不会有偏差(bias)——这个估计结果就不会有问题。

可是,一个数据点是不是能被选择进样本、或者说是不是能够被观测到,这个过程在很多时候并不是随机、外生的。比如说,就拿Wooldridge 教材中的一个经典例子来讲:研究者试图估计出受教育程度以及工作经验对于女职工工资的影响。在一个753名女性的大样本中,428名女性是有工作的,所以这项研究只能在这428名有工作(有收入)的样本中展开。那么问题来了:因为我们无法观测到那325个没有工作的样本中受教育程度以及经验对于收入的影响,并且一个人选择工作或不工作并非是随机的——人们会根据潜在的收入水平、自身条件、家庭情况、年龄等等因素综合来决定是否参加工作,于是,我们仅从那428个有工作的人身上找出的统计学结果将是有偏差的,因为样本的选择并非随机及外生的。

Heckman两阶段模型的功能就是试图纠正这种偏差导致的估计偏误。第一阶段的模型,是一个包括全样本(753人)的Probit模型,用来估计一个人参加工作与否的概率。这里的因变量是二元的,表示是否参加工作;自变量是一些会影响个人决定工作与否的外生变量,比如其他收入来源、年龄、有几个未成年子女,等等。这些自变量类似工具变量——他们会影响个人是否参加工作的决策,但不太可能影响参加工作后的收入水平。然后根据这个Probit模型,我们为每一个样本计算出逆米尔斯比率(Inverse Mills Ratio)。这个比率的作用是为每一个样本计算出一个用于修正样本选择偏差的值。

然后第二步,只需要在原来的回归方程——即对于428个有工作的样本,基于她们受教育程度和经验的回归中加入一个额外的自变量——逆米尔斯比率即可,然后估计出回归参数。

最后,观察在第二阶段方程中,逆米尔斯比率这个自变量的显著性。如果该变量不显著,则说明最一开始的回归方程并不具有样本选择偏差,研究者可以根据原来的系数来做出统计推断;但如果尼米尔比率这个参数是显著的,则说明样本选择偏差是存在的,研究者应当根据第二阶段方程里的回归系数来做出统计推断。

Heckman两阶段模型适用于解决由样本选择偏差(sample selection bias)造成的内生性问题。在经济学领域,样本选择偏差的典型例子是研究女性的受教育情况对女性工资的影响。按照这个思路,一般会去问卷收集或在哪个网站下载部分女性的受教育情况,工资,及其他特征数据,例如年龄,毕业院校等级等个人特征,然后做回归。不过这样做有一个问题,就是登记的女性,都是在工作的,但是许多受教育程度较高的女性不工作,选择做家庭主妇,这部分样本就没有算在内,样本失去随机性。这就导致模型只是用到了在工作的女性,这样得出的结论是有偏差的。在管理学领域,一个典型的问题是企业的某个特征,或者董事/CEO的某个特征,对企业R&D投入的影响。也是同样的问题,企业的R&D投入是企业自愿披露的内容,有的企业不披露,这时你做回归时就不能包括这部分样本,也会造成样本选择偏差,结果有偏。

对于这种情况,Heckman提出了一个方法,赫克曼矫正法(Heckman Correction,又称两阶段方法)。赫克曼矫正法分两个步骤进行:第一步骤,研究者根据管理学理论设计出一个计算企业披露R&D投入概率的模型,而该模型的统计估计结果可以用来预测每个个体的概率;第二步骤,研究者将这些被预测个体概率合并为一个额外的解释变量,与其他控制变量等变量一起来矫正自选择问题。这个比率叫逆米尔斯比率,inverse Mills ration, imr,也就是说,在第一步计算出imr,在第二步把imr当作一个控制变量。

以企业R&D投入问题为例,假设全样本是1000家公司,其中800家公司披露了其R&D投入。

第一阶段的模型,是一个包括全样本(1000家)的Probit模型,用来估计一家公司是否会披露其R&D投入的概率。这里的因变量是二元的,表示是否披露R&D投入;自变量是一些会影响是否披露R&D的外生变量,比如其他收入营业收入,杠杆率,公司规模,所属行业等等。然后根据这个Probit模型,为每一个样本计算出imr,imr作用是为每一个样本计算出一个用于修正样本选择偏差的值。

第二阶段,在原来的回归方程,也就是原来只有800家公司的样本的方程假如imr作为控制变量,其他都不变,然后估计出回归参数。这时不管imr显著不显著都不重要,imr显著说明样本选择偏差的确影响了你最初模型的估计,这正表明了使用Heckman两步法纠正样本选择偏差的必要性。imr不显著说明原模型不存在严重的样本选择偏差,这时Heckman第二步得到的结果应该与原模型得到的结果差不多。(关于imr的显著性是否说明样本选择偏差存在目前还有争议,不过imr不是关注的变量)。第二步关注的对象是核心解释变量是否显著。只要核心解释变量显著,就说明结果稳健。

在stata上的实现,还是刚才的例子。假设问题是研究董事会的连锁懂事比例对企业R&D投入的影响,各变量如下:

因变量:企业R&D投入额度(rd)

自变量:董事会连锁懂事比例 (interlockratio)

控制变量:公司规模(firmsize),杠杆率(leverage), 公司成长性(growth),公司年龄(age),行业R&D投入(industryrd),行业集中度(cr4),行业净资产收益率(industryroa)等。其中前三个控制变量还会影响企业R&D投入的概率。

总样本数1000家,其中800家披露了R&D投入,不考虑其他变量的缺失值。

Heckman两步法

第一步,命名一个新的因变量,企业是否披露R&D投入,ifrd

xi: probit ifrd firmsize leverage growth i.year i.ind r//Heckman两阶段的第一阶段回归,这里的r可加可不加,看需不需要控制异方差问题。

estimate store First

predict y_hat, xb

gen pdf = normalden(y_hat)

gen cdf = normal(y_hat)

gen imr = pdf/cdf//生成imr

第二步回归,把imr当作控制变量加入原模型,用原来的数据。

reg rd interlockratio leverage growth industryrd cr4 industryroa imr i.year i.ind , r if ifrd==1

需要注意的是,在第一步,确定哪些变量会影响企业披露其R&D数据时,这些变量不一定是原模型的因变量,可以是可以不是,是不是要说明理由。

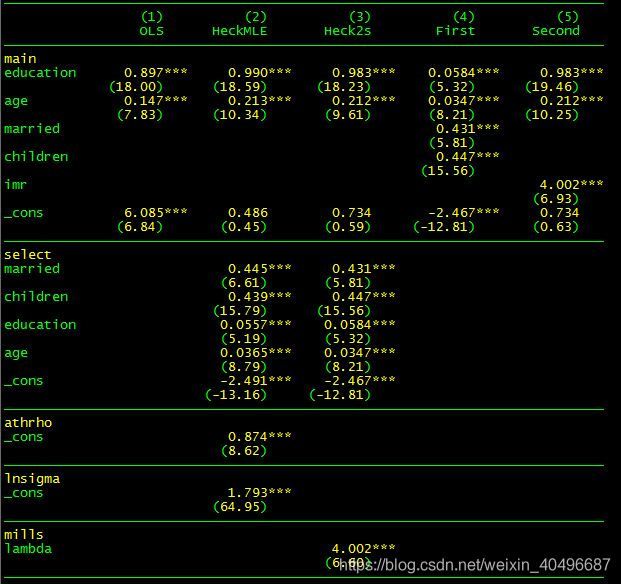

例二:

数据地址:点击下载

*数据来源: https://gitee.com/arlionn/data

use womenwk.dta, clear

*描述性统计数据

sum age educ married children wage

*简单的ols模型,存在选择性偏误

reg wage educ age

est store OLS

*第一种方法 heckman maximum likelihood

heckman wage educ age, select(married children educ age) //默认最大似然估计

est store HeckMLE

*第二种方法 heckman two-step all-in-one 不可以进行cluster调整

heckman wage educ age, select(married children educ age) twostep

est store Heck2s

*第二种方法 heckman two-step step-by-step 可以进行cluster调整

probit work married children educ age

est store First

predict y_hat, xb

gen pdf = normalden(y_hat) //概率密度函数

gen cdf = normal(y_hat) //累积分布函数

gen imr = pdf/cdf //计算逆米尔斯比率

reg wage educ age imr if work == 1 //女性工作子样本

est store Second

vif //方差膨胀因子

*对比结果

local m "OLS HeckMLE Heck2s First Second"

esttab `m', mtitle(`m') nogap compress pr2 ar2

python实现:

import numpy as np

import pandas as pd

# true parameters

rho_t = np.array([0.8])

rho_x_w_t = np.array([0.8])

gamma_t = np.array([.5,1.0])

beta_t = np.array([-2.0,0.5])

sigma_e_t = np.array([1.0])

N =5000

# generate toy data consistent with heckman:

# generate potentially correlated x,w data

mean_x_w = np.array([0,0])

cov_x_w = np.array([[1,rho_x_w_t[0]],[rho_x_w_t[0], 1]])

w, x = np.random.multivariate_normal(mean_x_w, cov_x_w, N).T

# add constant to first position and convert to DataFrame

w_ = pd.DataFrame(np.c_[np.ones(N),w],columns=['Constant (Selection)','Slope (Selection)'])

x_ = pd.DataFrame(np.c_[np.ones(N),x], columns=['Constant','Slope'])

# generate errors

mean_u_eps = np.array([0,0])

cov_u_eps = np.array([[1,rho_t[0]],[rho_t[0],sigma_e_t]])

u, epsilon = np.random.multivariate_normal(mean_u_eps, cov_u_eps, N).T

# generate latent zstar

zstar = w_.dot(gamma_t) + u

# generate observed z (indicator=1 if zstar is positive)

z = zstar > 0

# generate latent ystar

ystar = x_.dot(beta_t) + epsilon

y=ystar.copy()

# generate observed y [if z=0, set y to NaN]

y[~z] = np.nan

stata_data = pd.DataFrame(np.c_[y,z,x,w], columns=['y','z','x','w'])

stata_data.to_stata('/tmp/heckman_data.dta')

print(stata_data.head())

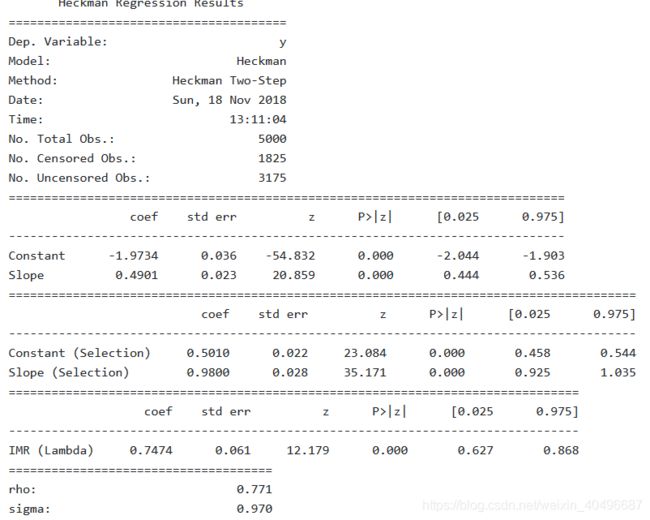

import heckman as heckman

res = heckman.Heckman(y, x_, w_).fit(method='twostep')

print(res.summary())

来源:网络地址

来源:网络地址

"""

Heckman correction for sample selection bias (the Heckit procedure).

Original Code Created August 19, 2014 by B.I.

Last modified February 26, 2017 by B.I.

NO warranty is provided for this software.

"""

import numpy as np

import statsmodels.api as sm

import statsmodels.base.model as base

from statsmodels.iolib import summary

from statsmodels.tools.numdiff import approx_fprime

from scipy.stats import norm

import warnings

import pandas as pd

class Heckman(base.LikelihoodModel):

"""

Class for Heckman correction for sample selection bias model.

Parameters

----------

endog : 1darray

Data for the dependent variable. Should be set to np.nan for

censored observations.

exog : 2darray

Data for the regression (response) equation. If a constant

term is desired, the user should directly add the constant

column to the data before using it as an argument here.

exog_select : 2darray

Data for the selection equation. If a constant

term is desired, the user should directly add the constant

column to the data before using it as an argument here.

**kwargs:

missing=, which can be 'none', 'drop', or 'raise'

Notes

-----

The selection equation should contain at least one variable that

is not in the regression (response) equation, i.e. the selection

equation should contain at least one instrument. However, this

module should still work if the user chooses not to do this.

"""

def __init__(self, endog, exog, exog_select, **kwargs):

# check that Z has same index as X (and consequently Y through super().__init__)

if pd.__name__ in type(endog).__module__ and pd.__name__ in type(exog).__module__:

if not all(endog.index==exog_select.index):

raise ValueError("Z indices need to be the same as X and Y indices")

# shape checks

if (len(endog) == len(exog)) and (len(endog) == len(exog_select)):

pass

else:

raise ValueError("Y, X, and Z data shapes do not conform with each other.")

try:

if (endog.ndim == 1) and (exog.ndim <= 2) and (exog_select.ndim <= 2):

pass

else:

raise ValueError("Y, X, and Z data shapes do not conform with each other.")

except AttributeError:

if (np.asarray(endog).ndim == 1) and (np.asarray(exog).ndim <= 2) and (np.asarray(exog_select).ndim <= 2):

pass

else:

raise ValueError("Y, X, and Z data shapes do not conform with each other.")

# give missing (treated) values in endog variable finite values so that super().__init__

# does not strip them out -- they will be put back after the call to super().__init__

treated = np.asarray(~np.isnan(endog))

try:

endog_nomissing = endog.copy()

endog_nomissing[~treated] = -99999

except (TypeError, AttributeError):

endog_nomissing = [endog[i] if treated[i] else -99999 for i in range(len(treated))]

# create 1-D array that will be np.nan for every row of exog_select that has any missing

# values and a finite value otherwise for the call to super().__init__ so that it can

# strip out rows where exog_select has missing data if missing option is set

if np.asarray(exog_select).ndim==2:

exog_select_1dnan_placeholder = \

[np.nan if any(np.isnan(row)) else 1 for row in np.asarray(exog_select)]

else: # assume ==1

exog_select_1dnan_placeholder = [np.nan if np.isnan(row) else 1 for row in np.asarray(exog_select)]

if pd.__name__ in type(endog).__module__:

exog_select_1dnan_placeholder = pd.Series(exog_select_1dnan_placeholder, index=endog.index)

else:

exog_select_1dnan_placeholder = np.array(exog_select_1dnan_placeholder)

# create array of sequential row positions so that rows of exog_select that have missing

# data can be identified after call to super().__init__

obsno = np.array(list(range(len(endog))))

# call super().__init__

super(Heckman, self).__init__(

endog_nomissing, exog=exog,

exog_select_1dnan_placeholder=exog_select_1dnan_placeholder, obsno=obsno,

treated=treated,

**kwargs)

# put np.nan back into endog for treated rows

self.endog = self.data.endog = \

np.asarray(

[self.endog[i] if self.treated[i] else np.nan for i in range(len(self.treated))]

)

# strip out rows stripped out by call to super().__init__ in Z variable

self.exog_select = np.asarray([np.asarray(exog_select)[obs] for obs in self.obsno])

# store variable names of exog_select

try:

self.exog_select_names = exog_select.columns.tolist()

except AttributeError:

self.exog_select_names = None

# delete attributes created by the call to super().__init__ that are no longer needed

del self.exog_select_1dnan_placeholder

del self.obsno

# store observation counts

self.nobs_total = len(endog)

self.nobs_uncensored = self.nobs = np.sum(self.treated)

self.nobs_censored = self.nobs_total - self.nobs_uncensored

def initialize(self):

self.wendog = self.endog

self.wexog = self.exog

def whiten(self, data):

"""

Model whitener for Heckman correction model does nothing.

"""

return data

def get_datamats(self):

Y = np.asarray(self.endog)

Y = Y[self.treated]

X = np.asarray(self.exog)

X = X[self.treated,:]

if X.ndim==1:

X = np.atleast_2d(X).T

Z = np.asarray(self.exog_select)

if Z.ndim==1:

Z = np.atleast_2d(Z).T

return Y, X, Z

def fit(self, method='twostep', start_params_mle=None, method_mle=None, maxiter_mle=None, **kwargs_mle):

"""

Fit the Heckman selection model.

Parameters

----------

method : str

Can only be "2step", which uses Heckman's two-step method.

start_params_mle: 1darray

If using MLE, starting parameters.

method_mle: str

If using MLE, the MLE estimation method.

maxiter_mle: scalar

If using MLE, the maximum number of iterations for MLE estimation.

**kwargs_mle:

Other arguments to pass to optimizer for MLE estimation.

Returns

-------

A HeckmanResults class instance.

See Also

---------

HeckmanResults

"""

## Show warning to user if estimation is by two-step but MLE arguments were also provided

if method=='twostep':

if start_params_mle is not None or method_mle is not None or maxiter_mle is not None or \

len(kwargs_mle.keys())>0:

warnings.warn('The user chose to estimate the Heckman model by Two-Step,' + \

' but MLE arguments were provided. Extraneous MLE arguments will be ignored.')

## fit

if method=='twostep':

results = self._fit_twostep()

elif method=='mle':

results = self._fit_mle(

start_params_mle=start_params_mle, method_mle=method_mle, maxiter_mle=maxiter_mle,

**kwargs_mle)

else:

raise ValueError("Invalid choice for estimation method.")

## return fitted Heckman model

return results

def _fit_twostep(self):

########################################################################

# PRIVATE METHOD

# Fits using Heckman two-step from Heckman (1979).

########################################################################

## prep data

Y, X, Z = self.get_datamats()

## Step 1

step1model = sm.Probit(self.treated, Z)

step1res = step1model.fit(disp=False)

step1_fitted = np.atleast_2d(step1res.fittedvalues).T

step1_varcov = step1res.cov_params()

inverse_mills = norm.pdf(step1_fitted)/norm.cdf(step1_fitted)

## Step 2

W = np.hstack((X, inverse_mills[self.treated] ) )

step2model = sm.OLS(Y, W)

step2res = step2model.fit()

params = step2res.params[:-1]

betaHat_inverse_mills = step2res.params[-1]

## Compute standard errors

# Compute estimated error variance of censored regression

delta = np.multiply(inverse_mills, inverse_mills + step1_fitted)[self.treated]

sigma2Hat = step2res.resid.dot(step2res.resid) / self.nobs_uncensored + \

(betaHat_inverse_mills**2 * sum(delta)) / self.nobs_uncensored

sigma2Hat = sigma2Hat[0]

sigmaHat = np.sqrt(sigma2Hat)

rhoHat = betaHat_inverse_mills / sigmaHat

# compute standard errors of beta estimates of censored regression

delta_1d = delta.T[0]

Q = rhoHat**2 * ((W.T*delta_1d).dot(Z[self.treated])).dot(step1_varcov).dot((Z[self.treated].T*delta_1d).dot(W))

WT_W_inv = np.linalg.inv(W.T.dot(W))

WT_R = W.T*(1 - rhoHat**2 * delta_1d)

normalized_varcov_all = WT_W_inv.dot(WT_R.dot(W)+Q).dot(WT_W_inv)

del WT_W_inv

del WT_R

del delta_1d

normalized_varcov = normalized_varcov_all[:-1,:-1]

varcov_all = sigma2Hat * normalized_varcov_all

varcov = varcov_all[:-1,:-1]

stderr_all = np.sqrt(np.diag(varcov_all))

stderr = stderr_all[:-1]

stderr_betaHat_inverse_mills = stderr_all[-1]

## store results

results = HeckmanResults(self, params, normalized_varcov, sigma2Hat,

select_res=step1res,

params_inverse_mills=betaHat_inverse_mills, stderr_inverse_mills=stderr_betaHat_inverse_mills,

var_reg_error=sigma2Hat, corr_eqnerrors=rhoHat,

method='twostep')

return results

def _fit_mle(self, start_params_mle=None, method_mle=None, maxiter_mle=None, **kwargs_mle):

# get number of X parameters and number of Z parameters

Y, X, Z = self.get_datamats()

num_xvars = X.shape[1]

num_zvars = Z.shape[1]

del Y, X, Z

# let the Heckman two-step parameter estimates be the starting values

# of the the optimizer of the Heckman MLE estimate if not specified by user

if start_params_mle is None:

twostep_res = self._fit_twostep()

xparams = np.asarray(twostep_res.params)

zparams = np.asarray(twostep_res.select_res.params)

params_all = np.append(xparams, zparams)

params_all = np.append(params_all,

np.log(np.sqrt(twostep_res.var_reg_error)))

params_all = np.append(params_all,

(1./2.)*np.log((1+twostep_res.corr_eqnerrors)/(1-twostep_res.corr_eqnerrors)))

start_params_mle = params_all

# fit Heckman parameters by MLE

results_mle = super(Heckman, self).fit(

start_params=start_params_mle, method=method_mle, maxiter=maxiter_mle,

**kwargs_mle

)

xbeta_hat = np.asarray(results_mle.params[:num_xvars]) # reg eqn coefs

zbeta_hat = np.asarray(results_mle.params[num_xvars:num_xvars+num_zvars]) # selection eqn coefs

log_sigma_hat = results_mle.params[-2]

atanh_rho_hat = results_mle.params[-1]

sigma_hat = np.exp(log_sigma_hat)

rho_hat = np.tanh(atanh_rho_hat)

scale = results_mle.scale

xbeta_ncov_hat = results_mle.normalized_cov_params[:num_xvars,:num_xvars]

zbeta_ncov_hat = results_mle.normalized_cov_params[

num_xvars:(num_xvars+num_zvars),num_xvars:(num_xvars+num_zvars)

]

imr_hat = rho_hat*sigma_hat

# use the Delta method to compute the variance of lambda (the inverse Mills ratio)

log_sigma_var_hat = results_mle.normalized_cov_params[-2,-2] * scale

atanh_rho_var_hat = results_mle.normalized_cov_params[-1,-1] * scale

def grad_lambda(log_sigma, atanh_rho):

return np.array([atanh_rho, log_sigma])

grad_lambda_hat = np.atleast_2d(grad_lambda(sigma_hat, rho_hat))

covmat = results_mle.normalized_cov_params[-2:,-2:] * scale

imr_stderr_hat = np.sqrt(

grad_lambda_hat.dot(covmat).dot(grad_lambda_hat.T)[0,0]

)

del grad_lambda_hat

del covmat

# fill in results for this fit, and return

DUMMY_COEF_STDERR_IMR = 0.

results = HeckmanResults(self, xbeta_hat,

xbeta_ncov_hat, scale,

select_res=base.LikelihoodModelResults(None, zbeta_hat, zbeta_ncov_hat, scale),

params_inverse_mills=imr_hat, stderr_inverse_mills=imr_stderr_hat,

var_reg_error=sigma_hat**2, corr_eqnerrors=rho_hat,

method='mle')

return results

def loglike(self, params):

return self.loglikeobs(params).sum(axis=0)

def nloglike(self, params):

return -self.loglikeobs(params).sum(axis=0)

def loglikeobs(self, params_all):

"""

Log-likelihood of model.

Parameters

----------

params_all : array-like

Parameter estimates, with the parameters for the regression

equation coming first, then the parameters for the

selection equation, then log sigma, then atanh rho.

Returns

-------

loglike : float

The value of the log-likelihood function for a Heckman correction model.

"""

# set up data and parameters needed to compute log likelihood

Y, X, Z = self.get_datamats()

D = self.treated

num_xvars = X.shape[1]

num_zvars = Z.shape[1]

xbeta = np.asarray(params_all[:num_xvars]) # reg eqn coefs

zbeta = np.asarray(params_all[num_xvars:num_xvars+num_zvars]) # selection eqn coefs

log_sigma = params_all[-2]

atanh_rho = params_all[-1]

sigma = np.exp(log_sigma)

rho = np.tanh(atanh_rho)

# line the data vectors up

Z_zbeta_aligned = Z.dot(zbeta)

X_xbeta = X.dot(xbeta)

X_xbeta_aligned = np.empty(self.nobs_total)

X_xbeta_aligned[:] = np.nan

X_xbeta_aligned[D] = X_xbeta

del X_xbeta

Y_aligned = np.empty(self.nobs_total)

Y_aligned[:] = np.nan

Y_aligned[D] = Y

# create an array where each row is the log likelihood for the corresponding observation

norm_cdf_input = (Z_zbeta_aligned+(Y_aligned-X_xbeta_aligned)*rho/sigma) / np.sqrt(1-rho**2)

norm_cdf_input[~D] = 0 # dummy value

ll_obs_observed = \

np.multiply(D,

norm.logcdf(norm_cdf_input) - \

(1./2.)*((Y_aligned-X_xbeta_aligned)/sigma)**2 - \

np.log(np.sqrt(2*np.pi)*sigma))

ll_obs_observed[~D] = 0

ll_obs_notobserved = \

np.multiply(1-D,

norm.logcdf(-Z_zbeta_aligned))

ll_obs = ll_obs_observed + ll_obs_notobserved

# return log likelihood by observation vector

return ll_obs

def score(self, params):

'''

Gradient of log-likelihood evaluated at params

'''

#this is the numerical approx func taken from

# base.model.GenericLikelihoodModel

kwds = {}

kwds.setdefault('centered', True)

return approx_fprime(params, self.loglike, **kwds).ravel()

def jac(self, params, **kwds):

'''

Jacobian/Gradient of log-likelihood evaluated at params for each

observation.

'''

#this is the numerical approx func taken from

# base.model.GenericLikelihoodModel

#kwds.setdefault('epsilon', 1e-4)

kwds.setdefault('centered', True)

return approx_fprime(params, self.loglikeobs, **kwds)

def hessian(self, params):

'''

Hessian of log-likelihood evaluated at params

'''

#this is the numerical approx func taken from

# base.model.GenericLikelihoodModel

from statsmodels.tools.numdiff import approx_hess

# need options for hess (epsilon)

return approx_hess(params, self.loglike)

def predict(self, params, exog=None):

"""

Return linear predicted values from a design matrix.

Parameters

----------

exog : array-like

Design / exogenous data

params : array-like, optional after fit has been called

Parameters of a linear model

Returns

-------

An array of fitted values

Notes

-----

If the model has not yet been fit, params is not optional.

"""

if exog is None:

exog = self.exog

return np.dot(exog, params)

if self._results is None and params is None:

raise ValueError("If the model has not been fit, then you must specify the params argument.")

if self._results is not None:

return np.dot(exog, self._results.params)

else:

return np.dot(exog, params)

class HeckmanResults(base.LikelihoodModelResults):

"""

Class to represent results/fits for Heckman model.

Attributes

----------

select_res : ProbitResult object

The ProbitResult object created when estimating the selection equation.

params_inverse_mills : scalar

Parameter estimate of the coef on the inverse Mills term in the second step.

stderr_inverse_mills : scalar

Standard error of the parameter estimate of the coef on the inverse Mills

term in the second step.

var_reg_error : scalar

Estimate of the "sigma" term, i.e. the error variance estimate of the

regression (response) equation

corr_eqnerrors : scalar

Estimate of the "rho" term, i.e. the correlation estimate of the errors between the

regression (response) equation and the selection equation

method : string

The method used to produce the estimates, i.e. 'twostep', 'mle'

"""

def __init__(self, model, params, normalized_cov_params=None, scale=1.,

select_res=None,

params_inverse_mills=None, stderr_inverse_mills=None,

var_reg_error=None, corr_eqnerrors=None,

method=None):

super(HeckmanResults, self).__init__(model, params,

normalized_cov_params,

scale)

self.select_res = select_res

self.params_inverse_mills = params_inverse_mills

self.stderr_inverse_mills = stderr_inverse_mills

self.var_reg_error = var_reg_error

self.corr_eqnerrors = corr_eqnerrors

self.method = method

if not hasattr(self, 'use_t'):

self.use_t = False

if not hasattr(self.select_res, 'use_t'):

self.select_res.use_t = False

def summary(self, yname=None, xname=None, zname=None, title=None, alpha=.05):

"""Summarize the Heckman model Results

Parameters

-----------

yname : string, optional

Default is `y`

xname : list of strings, optional

Default is `x_##` for ## in p the number of regressors

in the regression (response) equation.

zname : list of strings, optional

Default is `z_##` for ## in p the number of regressors

in the selection equation.

title : string, optional

Title for the top table. If not None, then this replaces the

default title

alpha : float

significance level for the confidence intervals

Returns

-------

smry : Summary instance

this holds the summary tables and text, which can be printed or

converted to various output formats.

See Also

--------

statsmodels.iolib.summary.Summary : class to hold summary

results

"""

## Put in Z name detected from data if none supplied, unless that too could not be

## inferred from data, then put in generic names

if zname is None and self.model.exog_select_names is not None:

zname=self.model.exog_select_names

elif zname is None and self.model.exog_select_names is None:

try:

zname = ['z' + str(i) for i in range(len(self.model.exog_select[0]))]

zname[0] = 'z0_or_zconst'

except TypeError:

zname = 'z0_or_zconst'

try: # for Python 3

if isinstance(zname, str):

zname = [zname]

except NameError: # for Python 2

if isinstance(zname, basestring):

zname = [zname]

## create summary object

# instantiate the object

smry = summary.Summary()

# add top info

if self.method=='twostep':

methodstr = 'Heckman Two-Step'

elif self.method=='mle':

methodstr = 'Heckman MLE'

else:

raise ValueError("Invalid method set")

top_left = [('Dep. Variable:', None),

('Model:', None),

('Method:', [methodstr]),

('Date:', None),

('Time:', None),

('No. Total Obs.:', ["%#i" % self.model.nobs_total]),

('No. Censored Obs.:', ["%#i" % self.model.nobs_censored]),

('No. Uncensored Obs.:', ["%#i" % self.model.nobs_uncensored]),

]

if hasattr(self, 'cov_type'):

top_left.append(('Covariance Type:', [self.cov_type]))

top_right = [

]

if title is None:

title = self.model.__class__.__name__ + ' ' + "Regression Results"

smry.add_table_2cols(self, gleft=top_left, gright=top_right,

yname=yname, xname=xname, title=title)

# add the Heckman-corrected regression table

smry.add_table_params(self, yname=yname, xname=xname, alpha=alpha,

use_t=self.use_t)

# add the selection equation estimates table

smry.add_table_params(self.select_res, yname=yname, xname=zname, alpha=alpha,

use_t=self.select_res.use_t)

# add the estimate to the inverse Mills estimate (z-score)

smry.add_table_params(

base.LikelihoodModelResults(None, np.atleast_1d(self.params_inverse_mills),

normalized_cov_params=np.atleast_1d(self.stderr_inverse_mills**2), scale=1.),

yname=None, xname=['IMR (Lambda)'], alpha=alpha,

use_t=False)

# add point estimates for rho and sigma

diagn_left = [('rho:', ["%#6.3f" % self.corr_eqnerrors]),

('sigma:', ["%#6.3f" % np.sqrt(self.var_reg_error)]),

]

diagn_right = [

]

smry.add_table_2cols(self, gleft=diagn_left, gright=diagn_right,

yname=yname, xname=xname,

title="")

# add text at end

smry.add_extra_txt(['First table are the estimates for the regression (response) equation.',

'Second table are the estimates for the selection equation.',

'Third table is the estimate for the coef of the inverse Mills ratio (Heckman\'s Lambda).'])

## return

return smry

https://github.com/vnery5/Econometria/blob/main/Heckman.py

# -*- coding: utf-8 -*-

"""

Created on Sun Dec 19 14:08:43 2021

@author: Administrator

"""

##Importando os pacotes e módulos necessários

import pandas as pd

import numpy as np

import math

#Para Regressão Linear Múltipla (OLS, GLS e WLS) e Testes Estatísticos

import statsmodels.api as sm

import econtools

import econtools.metrics as mt

from scipy import stats

#Pacotes de fórmula patsy no SM

from statsmodels.formula.api import logit, probit, poisson, ols, wls

#Pacotes para tabelas

from statsmodels.iolib.summary2 import summary_col

#Pacotes para fazer a coleta dos dados armazenados no mesmo diretório e outros pacotes gerais

import os

import pathlib

import glob

from IPython.display import clear_output

import gc

import subprocess #permite a cópia para o clipboard das equações gerados com as funções equation()

## Outros Pacotes

import statsmodels.base.model as base

from statsmodels.iolib import summary

from statsmodels.tools.numdiff import approx_fprime

from scipy.stats import norm

from scipy.optimize import minimize

from scipy.special import log_ndtr

from sklearn.linear_model import LinearRegression

from sklearn.metrics import mean_squared_error, mean_absolute_error

import warnings

class Heckman(base.LikelihoodModel):

"""

Class for Heckman correction for sample selection bias model.

Parameters

----------

endog : 1darray

Data for the dependent variable. Should be set to np.nan for

censored observations.

exog : 2darray

Data for the regression (response) equation. If a constant

term is desired, the user should directly add the constant

column to the data before using it as an argument here.

exog_select : 2darray

Data for the selection equation. If a constant

term is desired, the user should directly add the constant

column to the data before using it as an argument here.

**kwargs:

missing=, which can be 'none', 'drop', or 'raise'

Notes

-----

The selection equation should contain at least one variable that

is not in the regression (response) equation, i.e. the selection

equation should contain at least one instrument. However, this

module should still work if the user chooses not to do this.

"""

def __init__(self, endog, exog, exog_select, **kwargs):

# check that Z has same index as X (and consequently Y through super().__init__)

if pd.__name__ in type(endog).__module__ and pd.__name__ in type(exog).__module__:

if not all(endog.index==exog_select.index):

raise ValueError("Z indices need to be the same as X and Y indices")

# shape checks

if (len(endog) == len(exog)) and (len(endog) == len(exog_select)):

pass

else:

raise ValueError("Y, X, and Z data shapes do not conform with each other.")

try:

if (endog.ndim == 1) and (exog.ndim <= 2) and (exog_select.ndim <= 2):

pass

else:

raise ValueError("Y, X, and Z data shapes do not conform with each other.")

except AttributeError:

if (np.asarray(endog).ndim == 1) and (np.asarray(exog).ndim <= 2) and (np.asarray(exog_select).ndim <= 2):

pass

else:

raise ValueError("Y, X, and Z data shapes do not conform with each other.")

# give missing (treated) values in endog variable finite values so that super().__init__

# does not strip them out -- they will be put back after the call to super().__init__

treated = np.asarray(~np.isnan(endog))

try:

endog_nomissing = endog.copy()

endog_nomissing[~treated] = -99999

except (TypeError, AttributeError):

endog_nomissing = [endog[i] if treated[i] else -99999 for i in range(len(treated))]

# create 1-D array that will be np.nan for every row of exog_select that has any missing

# values and a finite value otherwise for the call to super().__init__ so that it can

# strip out rows where exog_select has missing data if missing option is set

if np.asarray(exog_select).ndim==2:

exog_select_1dnan_placeholder = \

[np.nan if any(np.isnan(row)) else 1 for row in np.asarray(exog_select)]

else: # assume ==1

exog_select_1dnan_placeholder = [np.nan if np.isnan(row) else 1 for row in np.asarray(exog_select)]

if pd.__name__ in type(endog).__module__:

exog_select_1dnan_placeholder = pd.Series(exog_select_1dnan_placeholder, index=endog.index)

else:

exog_select_1dnan_placeholder = np.array(exog_select_1dnan_placeholder)

# create array of sequential row positions so that rows of exog_select that have missing

# data can be identified after call to super().__init__

obsno = np.array(list(range(len(endog))))

# call super().__init__

super(Heckman, self).__init__(

endog_nomissing, exog=exog,

exog_select_1dnan_placeholder=exog_select_1dnan_placeholder, obsno=obsno,

treated=treated,

**kwargs)

# put np.nan back into endog for treated rows

self.endog = self.data.endog = \

np.asarray(

[self.endog[i] if self.treated[i] else np.nan for i in range(len(self.treated))]

)

# strip out rows stripped out by call to super().__init__ in Z variable

self.exog_select = np.asarray([np.asarray(exog_select)[obs] for obs in self.obsno])

# store variable names of exog_select

try:

self.exog_select_names = exog_select.columns.tolist()

except AttributeError:

self.exog_select_names = None

# delete attributes created by the call to super().__init__ that are no longer needed

del self.exog_select_1dnan_placeholder

del self.obsno

# store observation counts

self.nobs_total = len(endog)

self.nobs_uncensored = self.nobs = np.sum(self.treated)

self.nobs_censored = self.nobs_total - self.nobs_uncensored

def initialize(self):

self.wendog = self.endog

self.wexog = self.exog

def whiten(self, data):

"""

Model whitener for Heckman correction model does nothing.

"""

return data

def get_datamats(self):

Y = np.asarray(self.endog)

Y = Y[self.treated]

X = np.asarray(self.exog)

X = X[self.treated,:]

if X.ndim==1:

X = np.atleast_2d(X).T

Z = np.asarray(self.exog_select)

if Z.ndim==1:

Z = np.atleast_2d(Z).T

return Y, X, Z

def fit(self, method='twostep', start_params_mle=None, method_mle=None, maxiter_mle=None, **kwargs_mle):

"""

Fit the Heckman selection model.

Parameters

----------

method : str

Can only be "2step", which uses Heckman's two-step method.

start_params_mle: 1darray

If using MLE, starting parameters.

method_mle: str

If using MLE, the MLE estimation method.

maxiter_mle: scalar

If using MLE, the maximum number of iterations for MLE estimation.

**kwargs_mle:

Other arguments to pass to optimizer for MLE estimation.

Returns

-------

A HeckmanResults class instance.

See Also

---------

HeckmanResults

"""

## Show warning to user if estimation is by two-step but MLE arguments were also provided

if method=='twostep':

if start_params_mle is not None or method_mle is not None or maxiter_mle is not None or \

len(kwargs_mle.keys())>0:

warnings.warn('The user chose to estimate the Heckman model by Two-Step,' + \

' but MLE arguments were provided. Extraneous MLE arguments will be ignored.')

## fit

if method=='twostep':

results = self._fit_twostep()

elif method=='mle':

results = self._fit_mle(

start_params_mle=start_params_mle, method_mle=method_mle, maxiter_mle=maxiter_mle,

**kwargs_mle)

else:

raise ValueError("Invalid choice for estimation method.")

## return fitted Heckman model

return results

def _fit_twostep(self):

########################################################################

# PRIVATE METHOD

# Fits using Heckman two-step from Heckman (1979).

########################################################################

## prep data

Y, X, Z = self.get_datamats()

## Step 1

step1model = sm.Probit(self.treated, Z)

step1res = step1model.fit(disp=False)

step1_fitted = np.atleast_2d(step1res.fittedvalues).T

step1_varcov = step1res.cov_params()

inverse_mills = norm.pdf(step1_fitted)/norm.cdf(step1_fitted)

## Step 2

W = np.hstack((X, inverse_mills[self.treated] ) )

step2model = sm.OLS(Y, W)

step2res = step2model.fit()

params = step2res.params[:-1]

betaHat_inverse_mills = step2res.params[-1]

## Compute standard errors

# Compute estimated error variance of censored regression

delta = np.multiply(inverse_mills, inverse_mills + step1_fitted)[self.treated]

sigma2Hat = step2res.resid.dot(step2res.resid) / self.nobs_uncensored + \

(betaHat_inverse_mills**2 * sum(delta)) / self.nobs_uncensored

sigma2Hat = sigma2Hat[0]

sigmaHat = np.sqrt(sigma2Hat)

rhoHat = betaHat_inverse_mills / sigmaHat

# compute standard errors of beta estimates of censored regression

delta_1d = delta.T[0]

Q = rhoHat**2 * ((W.T*delta_1d).dot(Z[self.treated])).dot(step1_varcov).dot((Z[self.treated].T*delta_1d).dot(W))

WT_W_inv = np.linalg.inv(W.T.dot(W))

WT_R = W.T*(1 - rhoHat**2 * delta_1d)

normalized_varcov_all = WT_W_inv.dot(WT_R.dot(W)+Q).dot(WT_W_inv)

del WT_W_inv

del WT_R

del delta_1d

normalized_varcov = normalized_varcov_all[:-1,:-1]

varcov_all = sigma2Hat * normalized_varcov_all

varcov = varcov_all[:-1,:-1]

stderr_all = np.sqrt(np.diag(varcov_all))

stderr = stderr_all[:-1]

stderr_betaHat_inverse_mills = stderr_all[-1]

## store results

results = HeckmanResults(self, params, normalized_varcov, sigma2Hat,

select_res=step1res,

params_inverse_mills=betaHat_inverse_mills, stderr_inverse_mills=stderr_betaHat_inverse_mills,

var_reg_error=sigma2Hat, corr_eqnerrors=rhoHat,

method='twostep')

return results

def _fit_mle(self, start_params_mle=None, method_mle=None, maxiter_mle=None, **kwargs_mle):

# get number of X parameters and number of Z parameters

Y, X, Z = self.get_datamats()

num_xvars = X.shape[1]

num_zvars = Z.shape[1]

# let the Heckman two-step parameter estimates be the starting values

# of the the optimizer of the Heckman MLE estimate if not specified by user

if start_params_mle is None:

twostep_res = self._fit_twostep()

xparams = np.asarray(twostep_res.params)

zparams = np.asarray(twostep_res.select_res.params)

params_all = np.append(xparams, zparams)

params_all = np.append(params_all,

np.log(np.sqrt(twostep_res.var_reg_error)))

params_all = np.append(params_all,

(1./2.)*np.log((1+twostep_res.corr_eqnerrors)/(1-twostep_res.corr_eqnerrors)))

start_params_mle = params_all

# fit Heckman parameters by MLE

results_mle = super(Heckman, self).fit(

start_params=start_params_mle, method=method_mle, maxiter=maxiter_mle,

**kwargs_mle

)

xbeta_hat = np.asarray(results_mle.params[:num_xvars]) # reg eqn coefs

zbeta_hat = np.asarray(results_mle.params[num_xvars:num_xvars+num_zvars]) # selection eqn coefs

log_sigma_hat = results_mle.params[-2]

atanh_rho_hat = results_mle.params[-1]

sigma_hat = np.exp(log_sigma_hat)

rho_hat = np.tanh(atanh_rho_hat)

scale = results_mle.scale

xbeta_ncov_hat = results_mle.normalized_cov_params[:num_xvars,:num_xvars]

zbeta_ncov_hat = results_mle.normalized_cov_params[

num_xvars:(num_xvars+num_zvars),num_xvars:(num_xvars+num_zvars)

]

imr_hat = rho_hat*sigma_hat

# use the Delta method to compute the variance of lambda (the inverse Mills ratio)

log_sigma_var_hat = results_mle.normalized_cov_params[-2,-2] * scale

atanh_rho_var_hat = results_mle.normalized_cov_params[-1,-1] * scale

def grad_lambda(log_sigma, atanh_rho):

return np.array([atanh_rho, log_sigma])

grad_lambda_hat = np.atleast_2d(grad_lambda(sigma_hat, rho_hat))

covmat = results_mle.normalized_cov_params[-2:,-2:] * scale

imr_stderr_hat = np.sqrt(

grad_lambda_hat.dot(covmat).dot(grad_lambda_hat.T)[0,0]

)

del grad_lambda_hat

del covmat

# fill in results for this fit, and return

DUMMY_COEF_STDERR_IMR = 0.

results = HeckmanResults(self, xbeta_hat,

xbeta_ncov_hat, scale,

select_res=base.LikelihoodModelResults(None, zbeta_hat, zbeta_ncov_hat, scale),

params_inverse_mills=imr_hat, stderr_inverse_mills=imr_stderr_hat,

var_reg_error=sigma_hat**2, corr_eqnerrors=rho_hat,

method='mle')

return results

def loglike(self, params):

return self.loglikeobs(params).sum(axis=0)

def nloglike(self, params):

return -self.loglikeobs(params).sum(axis=0)

def loglikeobs(self, params_all):

"""

Log-likelihood of model.

Parameters

----------

params_all : array-like

Parameter estimates, with the parameters for the regression

equation coming first, then the parameters for the

selection equation, then log sigma, then atanh rho.

Returns

-------

loglike : float

The value of the log-likelihood function for a Heckman correction model.

"""

# set up data and parameters needed to compute log likelihood

Y, X, Z = self.get_datamats()

D = self.treated

num_xvars = X.shape[1]

num_zvars = Z.shape[1]

xbeta = np.asarray(params_all[:num_xvars]) # reg eqn coefs

zbeta = np.asarray(params_all[num_xvars:num_xvars+num_zvars]) # selection eqn coefs

log_sigma = params_all[-2]

atanh_rho = params_all[-1]

sigma = np.exp(log_sigma)

rho = np.tanh(atanh_rho)

# line the data vectors up

Z_zbeta_aligned = Z.dot(zbeta)

X_xbeta = X.dot(xbeta)

X_xbeta_aligned = np.empty(self.nobs_total)

X_xbeta_aligned[:] = np.nan

X_xbeta_aligned[D] = X_xbeta

del X_xbeta

Y_aligned = np.empty(self.nobs_total)

Y_aligned[:] = np.nan

Y_aligned[D] = Y

# create an array where each row is the log likelihood for the corresponding observation

norm_cdf_input = (Z_zbeta_aligned+(Y_aligned-X_xbeta_aligned)*rho/sigma) / np.sqrt(1-rho**2)

norm_cdf_input[~D] = 0 # dummy value

ll_obs_observed = \

np.multiply(D,

norm.logcdf(norm_cdf_input) - \

(1./2.)*((Y_aligned-X_xbeta_aligned)/sigma)**2 - \

np.log(np.sqrt(2*np.pi)*sigma))

ll_obs_observed[~D] = 0

ll_obs_notobserved = \

np.multiply(1-D,

norm.logcdf(-Z_zbeta_aligned))

ll_obs = ll_obs_observed + ll_obs_notobserved

# return log likelihood by observation vector

return ll_obs

def score(self, params):

'''

Gradient of log-likelihood evaluated at params

'''

#this is the numerical approx func taken from

# base.model.GenericLikelihoodModel

kwds = {}

kwds.setdefault('centered', True)

return approx_fprime(params, self.loglike, **kwds).ravel()

def jac(self, params, **kwds):

'''

Jacobian/Gradient of log-likelihood evaluated at params for each

observation.

'''

#this is the numerical approx func taken from

# base.model.GenericLikelihoodModel

#kwds.setdefault('epsilon', 1e-4)

kwds.setdefault('centered', True)

return approx_fprime(params, self.loglikeobs, **kwds)

def hessian(self, params):

'''

Hessian of log-likelihood evaluated at params

'''

#this is the numerical approx func taken from

# base.model.GenericLikelihoodModel

from statsmodels.tools.numdiff import approx_hess

# need options for hess (epsilon)

return approx_hess(params, self.loglike)

def predict(self, params, exog=None):

"""

Return linear predicted values from a design matrix.

Parameters

----------

exog : array-like

Design / exogenous data

params : array-like, optional after fit has been called

Parameters of a linear model

Returns

-------

An array of fitted values

Notes

-----

If the model has not yet been fit, params is not optional.

"""

if exog is None:

exog = self.exog

return np.dot(exog, params)

if self._results is None and params is None:

raise ValueError("If the model has not been fit, then you must specify the params argument.")

if self._results is not None:

return np.dot(exog, self._results.params)

else:

return np.dot(exog, params)

class HeckmanResults(base.LikelihoodModelResults):

"""

Class to represent results/fits for Heckman model.

Attributes

----------

select_res : ProbitResult object

The ProbitResult object created when estimating the selection equation.

params_inverse_mills : scalar

Parameter estimate of the coef on the inverse Mills term in the second step.

stderr_inverse_mills : scalar

Standard error of the parameter estimate of the coef on the inverse Mills

term in the second step.

var_reg_error : scalar

Estimate of the "sigma" term, i.e. the error variance estimate of the

regression (response) equation

corr_eqnerrors : scalar

Estimate of the "rho" term, i.e. the correlation estimate of the errors between the

regression (response) equation and the selection equation

method : string

The method used to produce the estimates, i.e. 'twostep', 'mle'

"""

def __init__(self, model, params, normalized_cov_params=None, scale=1.,

select_res=None,

params_inverse_mills=None, stderr_inverse_mills=None,

var_reg_error=None, corr_eqnerrors=None,

method=None):

super(HeckmanResults, self).__init__(model, params,

normalized_cov_params,

scale)

self.select_res = select_res

self.params_inverse_mills = params_inverse_mills

self.stderr_inverse_mills = stderr_inverse_mills

self.var_reg_error = var_reg_error

self.corr_eqnerrors = corr_eqnerrors

self.method = method

if not hasattr(self, 'use_t'):

self.use_t = False

if not hasattr(self.select_res, 'use_t'):

self.select_res.use_t = False

def summary(self, yname=None, xname=None, zname=None, title=None, alpha=.05):

"""Summarize the Heckman model Results

Parameters

-----------

yname : string, optional

Default is `y`

xname : list of strings, optional

Default is `x_##` for ## in p the number of regressors

in the regression (response) equation.

zname : list of strings, optional

Default is `z_##` for ## in p the number of regressors

in the selection equation.

title : string, optional

Title for the top table. If not None, then this replaces the

default title

alpha : float

significance level for the confidence intervals

Returns

-------

smry : Summary instance

this holds the summary tables and text, which can be printed or

converted to various output formats.

See Also

--------

statsmodels.iolib.summary.Summary : class to hold summary

results

"""

## Put in Z name detected from data if none supplied, unless that too could not be

## inferred from data, then put in generic names

if zname is None and self.model.exog_select_names is not None:

zname=self.model.exog_select_names

elif zname is None and self.model.exog_select_names is None:

try:

zname = ['z' + str(i) for i in range(len(self.model.exog_select[0]))]

zname[0] = 'z0_or_zconst'

except TypeError:

zname = 'z0_or_zconst'

if isinstance(zname, str):

zname = [zname]

## create summary object

# instantiate the object

smry = summary.Summary()

# add top info

if self.method=='twostep':

methodstr = 'Heckman Two-Step'

elif self.method=='mle':

methodstr = 'Heckman MLE'

else:

raise ValueError("Invalid method set")

top_left = [('Dep. Variable:', None),

('Model:', None),

('Method:', [methodstr]),

('Date:', None),

('Time:', None),

('No. Total Obs.:', ["%#i" % self.model.nobs_total]),

('No. Censored Obs.:', ["%#i" % self.model.nobs_censored]),

('No. Uncensored Obs.:', ["%#i" % self.model.nobs_uncensored]),

]

if hasattr(self, 'cov_type'):

top_left.append(('Covariance Type:', [self.cov_type]))

top_right = [

]

if title is None:

title = self.model.__class__.__name__ + ' ' + "Regression Results"

smry.add_table_2cols(self, gleft=top_left, gright=top_right,

yname=yname, xname=xname, title=title)

# add the Heckman-corrected regression table

smry.add_table_params(self, yname=yname, xname=xname, alpha=alpha,

use_t=self.use_t)

# add the selection equation estimates table

smry.add_table_params(self.select_res, yname=yname, xname=zname, alpha=alpha,

use_t=self.select_res.use_t)

# add the estimate to the inverse Mills estimate (z-score)

smry.add_table_params(

base.LikelihoodModelResults(None, np.atleast_1d(self.params_inverse_mills),

normalized_cov_params=np.atleast_1d(self.stderr_inverse_mills**2), scale=1.),

yname=None, xname=['IMR (Lambda)'], alpha=alpha,

use_t=False)

# add point estimates for rho and sigma

diagn_left = [('rho:', ["%#6.3f" % self.corr_eqnerrors]),

('sigma:', ["%#6.3f" % np.sqrt(self.var_reg_error)]),

]

diagn_right = [

]

smry.add_table_2cols(self, gleft=diagn_left, gright=diagn_right,

yname=yname, xname=xname,

title="")

# add text at end

smry.add_extra_txt(['First table are the estimates for the regression (response) equation.',

'Second table are the estimates for the selection equation.',

'Third table is the estimate for the coef of the inverse Mills ratio (Heckman\'s Lambda).'])

## return

return smry

参考文献:

Heckman两阶段法介绍