时间序列中的异常检测&孤立森林&异常可视化-lstm-arivm

指标值的突然上升或下降是一种异常行为,这两种情况都需要注意。如果我们在建模之前就有异常行为的信息,那么异常检测可以通过监督学习算法来解决,但在没有反馈的情况下,最初很难识别这些点。因此,我们可以使用孤立森林(Isolation Forest)、支持向量机和LSTM等算法将其建模为一个无监督问题。下面使用孤立森林识别异常点。

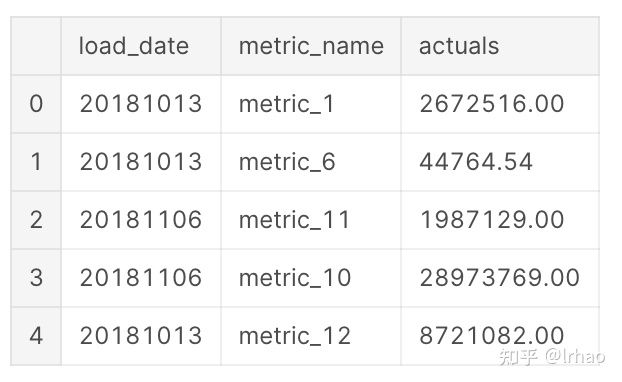

这里的数据是一个用例(如收益、流量等),每天有12个指标。我们必须首先确定在用例级别上是否存在异常。然后,为了获得更好的可操作性,我们深入到单个指标,并识别其中的异常情况。

现在在数据框中做一个透视,来创建一个数据框,在一个日期级别上包含所有指标。

metrics_df=pd.pivot_table(df,values='actuals',index='load_date',columns='metric_name')

metrics_df.head()

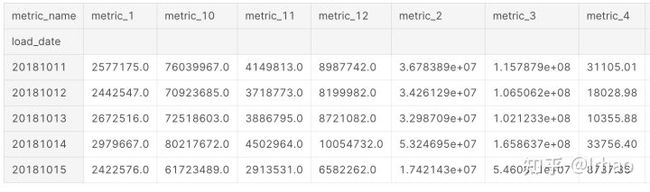

将数据框展平,并填充nan值为0

metrics_df.reset_index(inplace=True)

metrics_df.fillna(0,inplace=True)

metrics_df.head()

定义孤立森林并指定参数:

隔离森林试图分离数据中的每个点。在2D的情况下,它随机创建一条线,并试图选出一个点。在这种情况下,一个异常点只需几步就可以分离出来,而距离较近的正常点则需要相当多的步骤才能分离出来。

这里举例几个重要的参数。Contamination在这里是一个重要的参数,但是没有为它指定任何值,因为它是无监督的,我们没有关于异常值百分比的信息。

这里还可以通过在2D绘图中使用离群值验证其结果时的试错来指定它,或者如果数据是有监督的,则使用该信息来指定它,代表数据中离群点的百分比。

这里使用sklearn中自带的孤立森林,因为它是一个只有几个月数据的小数据集,而最近h2o的孤立森林也可用,它在高容量数据集上更可扩展,值得探索。

这个算法的更多细节可以参考这篇论文:https://cs.nju.edu.cn/zhouzh/zhouzh.files/publication/icdm08b.pdf

h2o孤立森林更多细节可以参考这个github链接:https://github.com/h2oai/h2o-tutorials/tree/master/tutorials/isolation-forest

metrics_df.columns

Index(['load_date', 'metric_1', 'metric_10', 'metric_11', 'metric_12',

'metric_2', 'metric_3', 'metric_4', 'metric_5', 'metric_6', 'metric_7',

'metric_8', 'metric_9'],

dtype='object', name='metric_name')

#specify the 12 metrics column names to be modelled

to_model_columns=metrics_df.columns[1:13]

from sklearn.ensemble import IsolationForest

clf=IsolationForest(n_estimators=100, max_samples='auto', \

max_features=1.0, bootstrap=False, n_jobs=-1, random_state=42, verbose=0)

clf.fit(metrics_df[to_model_columns])

IsolationForest(behaviour='old', bootstrap=False, contamination='legacy',

max_features=1.0, max_samples='auto', n_estimators=100, n_jobs=-1,

random_state=42, verbose=0)

pred = clf.predict(metrics_df[to_model_columns])

metrics_df['anomaly']=pred

outliers=metrics_df.loc[metrics_df['anomaly']==-1]

outlier_index=list(outliers.index)

#print(outlier_index)

#Find the number of anomalies and normal points here points classified -1 are anomalous

print(metrics_df['anomaly'].value_counts())

1 109

-1 12

Name: anomaly, dtype: int64

/opt/conda/lib/python3.6/site-packages/sklearn/ensemble/iforest.py:417: DeprecationWarning: threshold_ attribute is deprecated in 0.20 and will be removed in 0.22.

" be removed in 0.22.", DeprecationWarning)

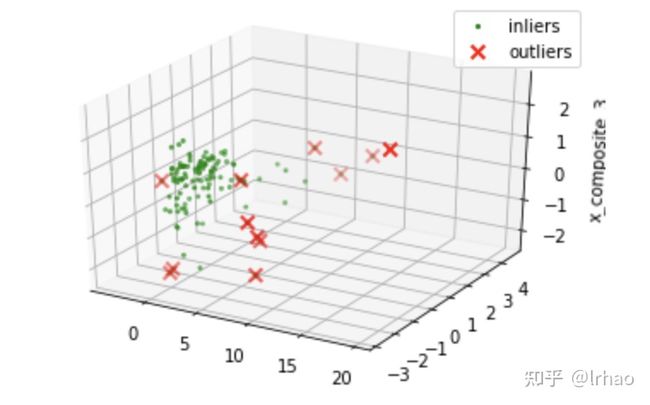

现在我们有了12个指标根据孤立森林的情况对异常情况进行了分类。我们将尝试将结果可视化,并检查分类是否有意义。

将指标归一化并拟合到PCA上,以减少维数,然后以3D方式将其绘制出来,突出显示异常。

import matplotlib.pyplot as plt

from sklearn.decomposition import PCA

from sklearn.preprocessing import StandardScaler

from mpl_toolkits.mplot3d import Axes3D

pca = PCA(n_components=3) # Reduce to k=3 dimensions

scaler = StandardScaler()

#normalize the metrics

X = scaler.fit_transform(metrics_df[to_model_columns])

X_reduce = pca.fit_transform(X)

fig = plt.figure()

ax = fig.add_subplot(111, projection='3d')

ax.set_zlabel("x_composite_3")

# Plot the compressed data points

ax.scatter(X_reduce[:, 0], X_reduce[:, 1], zs=X_reduce[:, 2], s=4, lw=1, label="inliers",c="green")

# Plot x's for the ground truth outliers

ax.scatter(X_reduce[outlier_index,0],X_reduce[outlier_index,1], X_reduce[outlier_index,2],

lw=2, s=60, marker="x", c="red", label="outliers")

ax.legend()

plt.show()

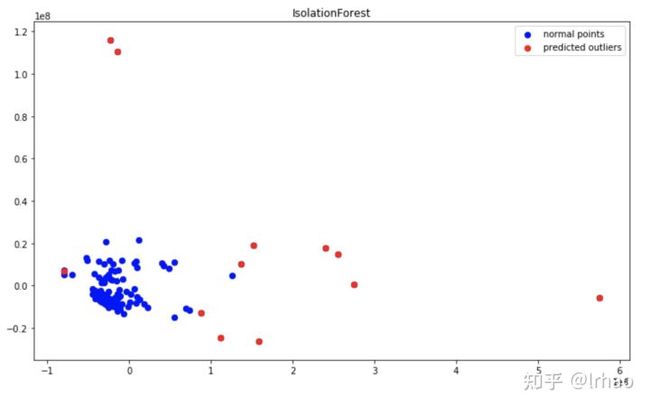

我们可以看到3D点,异常点大多是集群正常点,但一个2D点将帮助我们更好地判断。接下来,我们试着把同样的绘制成缩小到二维的主成分分析。

from sklearn.decomposition import PCA

pca = PCA(2)

pca.fit(metrics_df[to_model_columns])

res=pd.DataFrame(pca.transform(metrics_df[to_model_columns]))

Z = np.array(res)

figsize=(12, 7)

plt.figure(figsize=figsize)

plt.title("IsolationForest")

plt.contourf( Z, cmap=plt.cm.Blues_r)

b1 = plt.scatter(res[0], res[1], c='blue',

s=40,label="normal points")

b1 = plt.scatter(res.iloc[outlier_index,0],res.iloc[outlier_index,1], c='red',

s=40, edgecolor="red",label="predicted outliers")

plt.legend(loc="upper right")

plt.show()

因此,2D绘图为我们提供了一幅清晰的画面,表明算法正确地分类了用例中的异常点。

异常用红色边缘突出显示,正常点用绿色点表示。

在这里,Contamination参数起着很大的作用。我们的想法是捕获系统中所有的异常点。因此,最好是识别几个可能是正常的异常点(假阳性),但不要错过捕捉异常点(真阴性)。(所以我指定了12%作为Contamination,这取决于具体用例)

#Installing specific version of plotly to avoid Invalid property for color error in recent version which needs change in layout

!pip install plotly==2.7.0

现在我们已经发现了用例级别的异常行为。但是,要对异常采取行动,重要的是识别并提供信息,单独说明哪些指标标准是异常的。

当业务用户可以直观地看到(突然的下降/峰值)算法识别的异常时,就可以对其采取行动。所以在这个过程中,创造一个好的视觉效果也同样重要。

这个函数在时间序列上创建实际绘图,并在其上突出显示异常点。还有一个表,它提供了实际数据、更改和基于异常的条件格式化。

from plotly.offline import download_plotlyjs, init_notebook_mode, plot, iplot

import plotly.plotly as py

import matplotlib.pyplot as plt

from matplotlib import pyplot

import plotly.graph_objs as go

init_notebook_mode(connected=True)

def plot_anomaly(df,metric_name):

df.load_date = pd.to_datetime(df['load_date'].astype(str), format="%Y%m%d")

dates = df.load_date

#identify the anomaly points and create a array of its values for plot

bool_array = (abs(df['anomaly']) > 0)

actuals = df["actuals"][-len(bool_array):]

anomaly_points = bool_array * actuals

anomaly_points[anomaly_points == 0] = np.nan

#A dictionary for conditional format table based on anomaly

color_map = {0: "'rgba(228, 222, 249, 0.65)'", 1: "yellow", 2: "red"}

#Table which includes Date,Actuals,Change occured from previous point

table = go.Table(

domain=dict(x=[0, 1],

y=[0, 0.3]),

columnwidth=[1, 2],

# columnorder=[0, 1, 2,],

header=dict(height=20,

values=[['Date'], ['Actual Values '], ['% Change '],

],

font=dict(color=['rgb(45, 45, 45)'] * 5, size=14),

fill=dict(color='#d562be')),

cells=dict(values=[df.round(3)[k].tolist() for k in ['load_date', 'actuals', 'percentage_change']],

line=dict(color='#506784'),

align=['center'] * 5,

font=dict(color=['rgb(40, 40, 40)'] * 5, size=12),

# format = [None] + [",.4f"] + [',.4f'],

# suffix=[None] * 4,

suffix=[None] + [''] + [''] + ['%'] + [''],

height=27,

fill=dict(color=[test_df['anomaly_class'].map(color_map)],#map based on anomaly level from dictionary

)

))

#Plot the actuals points

Actuals = go.Scatter(name='Actuals',

x=dates,

y=df['actuals'],

xaxis='x1', yaxis='y1',

mode='line',

marker=dict(size=12,

line=dict(width=1),

color="blue"))

#Highlight the anomaly points

anomalies_map = go.Scatter(name="Anomaly",

showlegend=True,

x=dates,

y=anomaly_points,

mode='markers',

xaxis='x1',

yaxis='y1',

marker=dict(color="red",

size=11,

line=dict(

color="red",

width=2)))

axis = dict(

showline=True,

zeroline=False,

showgrid=True,

mirror=True,

ticklen=4,

gridcolor='#ffffff',

tickfont=dict(size=10))

layout = dict(

width=1000,

height=865,

autosize=False,

title=metric_name,

margin=dict(t=75),

showlegend=True,

xaxis1=dict(axis, **dict(domain=[0, 1], anchor='y1', showticklabels=True)),

yaxis1=dict(axis, **dict(domain=[2 * 0.21 + 0.20, 1], anchor='x1', hoverformat='.2f')))

fig = go.Figure(data=[table, anomalies_map, Actuals], layout=layout)

iplot(fig)

pyplot.show()

#return res

一个helper函数来查找百分比变化,根据严重程度对异常进行分类。

预测函数根据决策函数的结果,对数据进行异常分类。如果企业需要发现下一个可能产生影响的异常,可以使用这个来识别这些点。

前12个分位数为识别异常(高严重性),根据决策函数识别12-24个分位数点,将其分类为低严重性异常。

def classify_anomalies(df,metric_name):

df['metric_name']=metric_name

df = df.sort_values(by='load_date', ascending=False)

#Shift actuals by one timestamp to find the percentage chage between current and previous data point

df['shift'] = df['actuals'].shift(-1)

df['percentage_change'] = ((df['actuals'] - df['shift']) / df['actuals']) * 100

#Categorise anomalies as 0-no anomaly, 1- low anomaly , 2 - high anomaly

df['anomaly'].loc[df['anomaly'] == 1] = 0

df['anomaly'].loc[df['anomaly'] == -1] = 2

df['anomaly_class'] = df['anomaly']

max_anomaly_score = df['score'].loc[df['anomaly_class'] == 2].max()

medium_percentile = df['score'].quantile(0.24)

df['anomaly_class'].loc[(df['score'] > max_anomaly_score) & (df['score'] <= medium_percentile)] = 1

return df

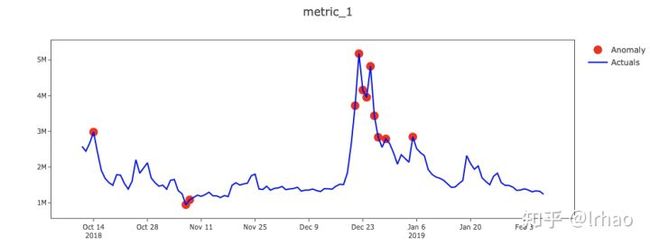

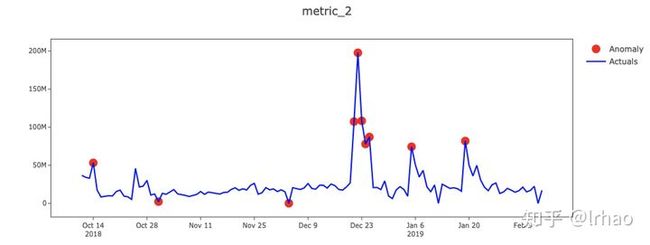

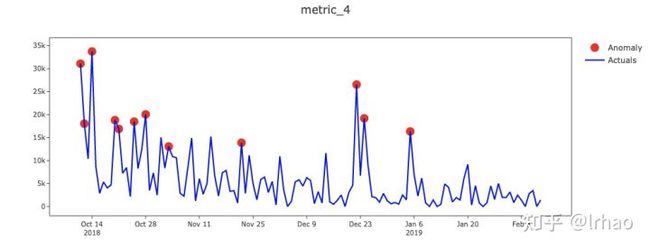

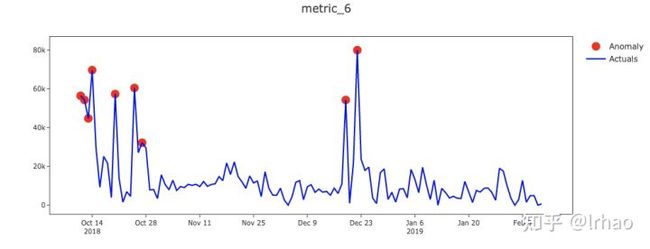

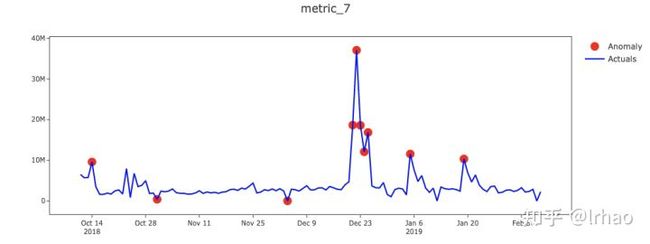

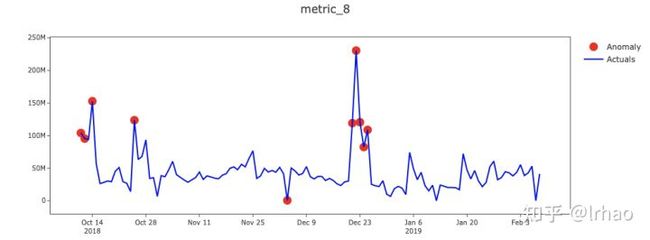

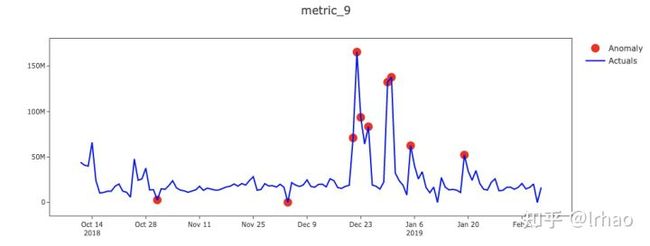

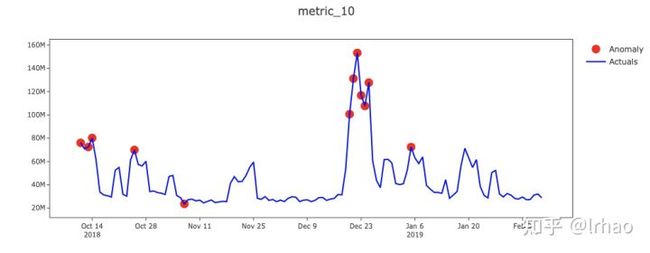

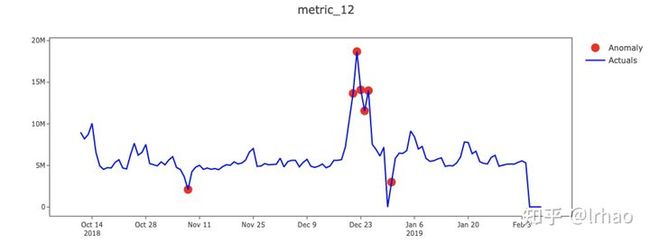

识别单个指标的异常并绘制结果。

X轴-日期,Y轴-实际值和异常点。

指标的实际值显示在蓝线中,异常点以红点突出显示。在表中,背景红色表示高异常,黄色表示低异常。

import warnings

warnings.filterwarnings('ignore')

for i in range(1,len(metrics_df.columns)-1):

clf.fit(metrics_df.iloc[:,i:i+1])

pred = clf.predict(metrics_df.iloc[:,i:i+1])

test_df=pd.DataFrame()

test_df['load_date']=metrics_df['load_date']

#Find decision function to find the score and classify anomalies

test_df['score']=clf.decision_function(metrics_df.iloc[:,i:i+1])

test_df['actuals']=metrics_df.iloc[:,i:i+1]

test_df['anomaly']=pred

#Get the indexes of outliers in order to compare the metrics with use case anomalies if required

outliers=test_df.loc[test_df['anomaly']==-1]

outlier_index=list(outliers.index)

test_df=classify_anomalies(test_df,metrics_df.columns[i])

plot_anomaly(test_df,metrics_df.columns[i])

从图中,我们能够捕捉到指标的突然峰值和低谷,并将它们投射出来。

此外,条件格式的表(可以运行代码获取,这里太占用篇幅没有展现)还可以让我们了解一些情况,比如数据不存在(值为零),这可能是数据处理过程中pipeline破裂的潜在结果,需要修复,并突出显示高级别和低级别异常。

如何使用呢?

- 如果当前时间戳对于用例来说是异常的,那么深入到指标,找出时间戳中有高度异常的指标集,以便在其上执行PCA。

- 此外,业务用户的反馈可以更新回数据中,这将有助于将其转换为监督/半监督学习问题,并比较其结果。

- 这里的一种增强是将不断发生的反常行为结合起来。如,大促销日(游戏绑定:可能会导致数天内的指标飙升)可以显示为单一行为。

本文我们将用更多的算法模型,如SARIMA、Auto Arima、LSTM用于检测时间序列预测中的异常点。

时间序列是任何与时间相关的数据(日、小时、月等)。例如:商店每天的收入是一天级别的时间序列数据。需求估计、销售预测等许多用例是典型的时间序列预测问题。

时间序列预测通过使用当前数据进行估计,帮助我们为未来的需要做好准备。一旦我们有了预测,我们就可以使用这些数据来检测异常,并将其与实际数据进行比较。

本文将一一实现这些算法模型,看看他们的优缺点。

# This Python 3 environment comes with many helpful analytics libraries installed

# It is defined by the kaggle/python docker image: https://github.com/kaggle/docker-python

# For example, here's several helpful packages to load in

import numpy as np # linear algebra

import pandas as pd # data processing, CSV file I/O (e.g. pd.read_csv)

# Input data files are available in the "../input/" directory.

# For example, running this (by clicking run or pressing Shift+Enter) will list the files in the input directory

import os

print(os.listdir("../input"))

import warnings

warnings.filterwarnings('ignore')

# Any results you write to the current directory are saved as output.- 可视化包

#Installing specific version of plotly to avoid Invalid property for color error in recent version which needs change in layout

!pip install plotly==2.7.0

from plotly.offline import download_plotlyjs, init_notebook_mode, plot, iplot

import plotly.plotly as py

import matplotlib.pyplot as plt

from matplotlib import pyplot

import plotly.graph_objs as go

init_notebook_mode(connected=True)- 这里的时间序列数据是从1月11日到12月11日的每日数值。

import pandas as pd

time_series_df=pd.read_csv('../input/time-series-data/time_series_data.csv')

time_series_df.head()

- 将其按时间顺序排列,因为我们要预测下一个点。将load_date列转换为datetime格式,并根据日期对数据进行排序。

time_series_df.load_date = pd.to_datetime(time_series_df.load_date, format='%Y%m%d')

time_series_df = time_series_df.sort_values(by="load_date")

time_series_df = time_series_df.reset_index(drop=True)

time_series_df.head()

- 数值结果应用对数变换来稳定数据中的方差,或者在将其输入模型之前使其平稳。

actual_vals = time_series_df.actuals.values

actual_log = np.log10(actual_vals)- 将数据划分为训练集和测试集(包含70个点)

SARIMA & Auto Arima

首先尝试应用SARIMA算法进行预测。SARIMA代表Seasonal Auto Regressive Integrated Moving Average。它有一个季节性参数,由于销售数据的每周季节性(即周期性是一周),我们将其初始化为7。其他参数是p,d,q,这些参数是基于ACF和PACF图识别出来的,或者我们最好使用误差最小的参数进行预测。

SARIMA更多细节可以参考这里:https://people.duke.edu/~rnau/arimrule.htm

这里我将差分因子(d)指定为1。它帮助我们消除数据中的趋势和周期。

import math

import statsmodels.api as sm

import statsmodels.tsa.api as smt

from sklearn.metrics import mean_squared_error

from matplotlib import pyplot

import matplotlib.pyplot as plt

import plotly.plotly as py

import plotly.tools as tls

train, test = actual_vals[0:-70], actual_vals[-70:]

train_log, test_log = np.log10(train), np.log10(test)

my_order = (1, 1, 1)

my_seasonal_order = (0, 1, 1, 7)每次我们预测下一个数据点,我们通过训练数据循环预测下一个数据,并在预测后添加下一个数据点,以进一步预测。这就像一个移动窗口每日水平数据(例如:前90点用于预测任何给定时间的下一个点),然后将预测数据转换回10倍变换,并绘制结果。

history = [x for x in train_log]

predictions = list()

predict_log=list()

for t in range(len(test_log)):

model = sm.tsa.SARIMAX(history, order=my_order, seasonal_order=my_seasonal_order,enforce_stationarity=False,enforce_invertibility=False)

model_fit = model.fit(disp=0)

output = model_fit.forecast()

predict_log.append(output[0])

yhat = 10**output[0]

predictions.append(yhat)

obs = test_log[t]

history.append(obs)

# print('predicted=%f, expected=%f' % (output[0], obs))

#error = math.sqrt(mean_squared_error(test_log, predict_log))

#print('Test rmse: %.3f' % error)

# plot

figsize=(12, 7)

plt.figure(figsize=figsize)

pyplot.plot(test,label='Actuals')

pyplot.plot(predictions, color='red',label='Predicted')

pyplot.legend(loc='upper right')

pyplot.show()

这是一个很好的时间序列预测。趋势、季节性是时间序列数据中的两个重要因素,如果您的算法能够捕获数据的趋势(向上/向下),如果您的数据是季节性的(每天、每周、每个季度、每年的模式),那么您的算法就适合就是一个不错的选择。

在这里,我们可以观察SARIMA算法从峰值捕获趋势,并很好地预测了正常日子的实际情况。

我们在这里指定的参数似乎可以很好地用于度量,但验证、调优参数并绘图将是一项艰难的任务。解决这个问题的一个方法是Auto Arima,它在我们指定的范围内返回算法的最佳参数集。

- 安装pyramid-arima

!pip install pyramid-arima让我们使用auto_arima找到p和q参数,并指定d为1的一阶差分和季节性为7的每周季节性。

from pyramid.arima import auto_arima

stepwise_model = auto_arima(train_log, start_p=1, start_q=1,

max_p=3, max_q=3, m=7,

start_P=0, seasonal=True,

d=1, D=1, trace=True,

error_action='ignore',

suppress_warnings=True,

stepwise=True)

print(stepwise_model)auo-arim模型可以用同样的方法进行逐步预测

import math

import statsmodels.api as sm

import statsmodels.tsa.api as smt

from sklearn.metrics import mean_squared_error

train, test = actual_vals[0:-70], actual_vals[-70:]

train_log, test_log = np.log10(train), np.log10(test)

# split data into train and test-sets

history = [x for x in train_log]

predictions = list()

predict_log=list()

for t in range(len(test_log)):

#model = sm.tsa.SARIMAX(history, order=my_order, seasonal_order=my_seasonal_order,enforce_stationarity=False,enforce_invertibility=False)

stepwise_model.fit(history)

output = stepwise_model.predict(n_periods=1)

predict_log.append(output[0])

yhat = 10**output[0]

predictions.append(yhat)

obs = test_log[t]

history.append(obs)

#print('predicted=%f, expected=%f' % (output[0], obs))

#error = math.sqrt(mean_squared_error(test_log, predict_log))

#print('Test rmse: %.3f' % error)

# plot

figsize=(12, 7)

plt.figure(figsize=figsize)

pyplot.plot(test,label='Actuals')

pyplot.plot(predictions, color='red',label='Predicted')

pyplot.legend(loc='upper right')

pyplot.show()

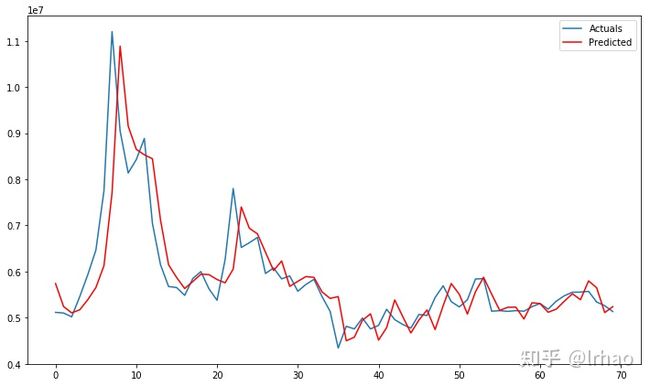

在这种情况下,auto arima和我们最初的SARIMA在预测方面也做得很好,因为它们不会去过拟合数据集。

下一步让创建一个可用数据框与实际数据和预测的结果可视化

predicted_df=pd.DataFrame()

predicted_df['load_date']=time_series_df['load_date'][-70:]

predicted_df['actuals']=test

predicted_df['predicted']=predictions

predicted_df.reset_index(inplace=True)

del predicted_df['index']

predicted_df.head()

我们有预测和实际的结果,以检测异常点这一信息。

注意:只有当数据是正态分布/高斯分布时,这才有效。

检测异常的步骤:

- 计算误差项(实际-预测)。

- 计算滑动窗口均值和标准差(这里窗口为一周)。

- 将误差为1.5、1.75、2个标准差的数据划分为低、中、高异常值。(根据该特性,5%的数据点将被识别为异常)

这里使用lambda函数对基于误差和标准偏差的异常进行分类,而不是为其提供单独的循环和函数。

import numpy as np

def detect_classify_anomalies(df,window):

df.replace([np.inf, -np.inf], np.NaN, inplace=True)

df.fillna(0,inplace=True)

df['error']=df['actuals']-df['predicted']

df['percentage_change'] = ((df['actuals'] - df['predicted']) / df['actuals']) * 100

df['meanval'] = df['error'].rolling(window=window).mean()

df['deviation'] = df['error'].rolling(window=window).std()

df['-3s'] = df['meanval'] - (2 * df['deviation'])

df['3s'] = df['meanval'] + (2 * df['deviation'])

df['-2s'] = df['meanval'] - (1.75 * df['deviation'])

df['2s'] = df['meanval'] + (1.75 * df['deviation'])

df['-1s'] = df['meanval'] - (1.5 * df['deviation'])

df['1s'] = df['meanval'] + (1.5 * df['deviation'])

cut_list = df[['error', '-3s', '-2s', '-1s', 'meanval', '1s', '2s', '3s']]

cut_values = cut_list.values

cut_sort = np.sort(cut_values)

df['impact'] = [(lambda x: np.where(cut_sort == df['error'][x])[1][0])(x) for x in

range(len(df['error']))]

severity = {0: 3, 1: 2, 2: 1, 3: 0, 4: 0, 5: 1, 6: 2, 7: 3}

region = {0: "NEGATIVE", 1: "NEGATIVE", 2: "NEGATIVE", 3: "NEGATIVE", 4: "POSITIVE", 5: "POSITIVE", 6: "POSITIVE",

7: "POSITIVE"}

df['color'] = df['impact'].map(severity)

df['region'] = df['impact'].map(region)

df['anomaly_points'] = np.where(df['color'] == 3, df['error'], np.nan)

df = df.sort_values(by='load_date', ascending=False)

df.load_date = pd.to_datetime(df['load_date'].astype(str), format="%Y-%m-%d")

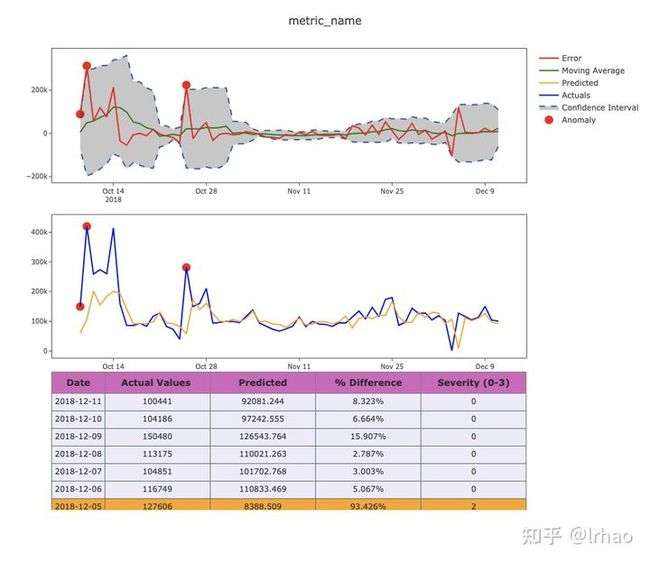

return df下面是一个可视化结果的函数。同样,清晰全面的可视化的重要性可以帮助业务用户对异常情况提供反馈,并使结果具有可操作性。

第一个图具有指定上下限边界的误差项。

异常突出显示的实际图形将很容易为用户解释/验证,因此第二幅图突出了异常的实际值和预测值。

- 蓝线-实际值

- 橙色线-预测值

- 红色-误差值

- 绿色-移动平均

- 虚线-正常行为的上下限

def plot_anomaly(df,metric_name):

#error = pd.DataFrame(Order_results.error.values)

#df = df.sort_values(by='load_date', ascending=False)

#df.load_date = pd.to_datetime(df['load_date'].astype(str), format="%Y%m%d")

dates = df.load_date

#meanval = error.rolling(window=window).mean()

#deviation = error.rolling(window=window).std()

#res = error

#upper_bond=meanval + (2 * deviation)

#lower_bond=meanval - (2 * deviation)

#anomalies = pd.DataFrame(index=res.index, columns=res.columns)

#anomalies[res < lower_bond] = res[res < lower_bond]

#anomalies[res > upper_bond] = res[res > upper_bond]

bool_array = (abs(df['anomaly_points']) > 0)

#And a subplot of the Actual Values.

actuals = df["actuals"][-len(bool_array):]

anomaly_points = bool_array * actuals

anomaly_points[anomaly_points == 0] = np.nan

#Order_results['meanval']=meanval

#Order_results['deviation']=deviation

color_map= {0: "'rgba(228, 222, 249, 0.65)'", 1: "yellow", 2: "orange", 3: "red"}

table = go.Table(

domain=dict(x=[0, 1],

y=[0, 0.3]),

columnwidth=[1, 2 ],

#columnorder=[0, 1, 2,],

header = dict(height = 20,

values = [['Date'],['Actual Values '],

['Predicted'], ['% Difference'],['Severity (0-3)']],

font = dict(color=['rgb(45, 45, 45)'] * 5, size=14),

fill = dict(color='#d562be')),

cells = dict(values = [df.round(3)[k].tolist() for k in ['load_date', 'actuals', 'predicted',

'percentage_change','color']],

line = dict(color='#506784'),

align = ['center'] * 5,

font = dict(color=['rgb(40, 40, 40)'] * 5, size=12),

#format = [None] + [",.4f"] + [',.4f'],

#suffix=[None] * 4,

suffix=[None] + [''] + [''] + ['%'] + [''],

height = 27,

#fill = dict(color=['rgb(235, 193, 238)', 'rgba(228, 222, 249, 0.65)']))

fill=dict(color= # ['rgb(245,245,245)',#unique color for the first column

[df['color'].map(color_map)],

)

))

#df['ano'] = np.where(df['color']==3, df['error'], np.nan)

anomalies = go.Scatter(name="Anomaly",

x=dates,

xaxis='x1',

yaxis='y1',

y=df['anomaly_points'],

mode='markers',

marker = dict(color ='red',

size = 11,line = dict(

color = "red",

width = 2)))

upper_bound = go.Scatter(hoverinfo="skip",

x=dates,

showlegend =False,

xaxis='x1',

yaxis='y1',

y=df['3s'],

marker=dict(color="#444"),

line=dict(

color=('rgb(23, 96, 167)'),

width=2,

dash='dash'),

fillcolor='rgba(68, 68, 68, 0.3)',

fill='tonexty')

lower_bound = go.Scatter(name='Confidence Interval',

x=dates,

xaxis='x1',

yaxis='y1',

y=df['-3s'],

marker=dict(color="#444"),

line=dict(

color=('rgb(23, 96, 167)'),

width=2,

dash='dash'),

fillcolor='rgba(68, 68, 68, 0.3)',

fill='tonexty')

Actuals = go.Scatter(name= 'Actuals',

x= dates,

y= df['actuals'],

xaxis='x2', yaxis='y2',

mode='line',

marker=dict(size=12,

line=dict(width=1),

color="blue"))

Predicted = go.Scatter(name= 'Predicted',

x= dates,

y= df['predicted'],

xaxis='x2', yaxis='y2',

mode='line',

marker=dict(size=12,

line=dict(width=1),

color="orange"))

# create plot for error...

Error = go.Scatter(name="Error",

x=dates, y=df['error'],

xaxis='x1',

yaxis='y1',

mode='line',

marker=dict(size=12,

line=dict(width=1),

color="red"),

text="Error")

anomalies_map = go.Scatter(name = "anomaly actual",

showlegend=False,

x=dates,

y=anomaly_points,

mode='markers',

xaxis='x2',

yaxis='y2',

marker = dict(color ="red",

size = 11,

line = dict(

color = "red",

width = 2)))

Mvingavrg = go.Scatter(name="Moving Average",

x=dates,

y=df['meanval'],

mode='line',

xaxis='x1',

yaxis='y1',

marker=dict(size=12,

line=dict(width=1),

color="green"),

text="Moving average")

axis=dict(

showline=True,

zeroline=False,

showgrid=True,

mirror=True,

ticklen=4,

gridcolor='#ffffff',

tickfont=dict(size=10))

layout = dict(

width=1000,

height=865,

autosize=False,

title= metric_name,

margin = dict(t=75),

showlegend=True,

xaxis1=dict(axis, **dict(domain=[0, 1], anchor='y1', showticklabels=True)),

xaxis2=dict(axis, **dict(domain=[0, 1], anchor='y2', showticklabels=True)),

yaxis1=dict(axis, **dict(domain=[2 * 0.21 + 0.20 + 0.09, 1], anchor='x1', hoverformat='.2f')),

yaxis2=dict(axis, **dict(domain=[0.21 + 0.12, 2 * 0.31 + 0.02], anchor='x2', hoverformat='.2f')))

fig = go.Figure(data = [table,anomalies,anomalies_map,

upper_bound,lower_bound,Actuals,Predicted,

Mvingavrg,Error], layout = layout)

iplot(fig)

pyplot.show()

classify_df=detect_classify_anomalies(predicted_df,7)

classify_df.reset_index(inplace=True)

del classify_df['index']

classify_df.head()

调用plot函数并将结果可视化。

plot_anomaly(classify_df.iloc[:-6,:],"metric_name")- 通过使用滑动窗口均值和标准偏差,我们可以避免在大销售日等情况下出现连续的虚假异常。

- 第一个峰值或下降是突出显示后,阈值得到调整。

- 表格还提供了实际数据、预测值、变化量和条件格式的基础上的异常级别。

LSTM

接下来,我们也尝试使用LSTM这种递归神经网络进行预测。

LSTM时间序列预测的更多细节参考这里:https://machinelearningmastery.com/time-series-prediction-lstm-recurrent-neural-networks-python-keras/

from pandas import DataFrame

from pandas import Series

from pandas import concat

from pandas import read_csv

from pandas import datetime

from sklearn.metrics import mean_squared_error

from sklearn.preprocessing import MinMaxScaler

from keras.models import Sequential

from keras.layers import Dense

from keras.layers import LSTM

from math import sqrt下面是LSTM的差分、缩放和逆函数以及训练、预测的helper函数。

# frame a sequence as a supervised learning problem

def timeseries_to_supervised(data, lag=1):

df = DataFrame(data)

columns = [df.shift(i) for i in range(1, lag+1)]

columns.append(df)

df = concat(columns, axis=1)

df.fillna(0, inplace=True)

return df

# create a differenced series

def difference(dataset, interval=1):

diff = list()

for i in range(interval, len(dataset)):

value = dataset[i] - dataset[i - interval]

diff.append(value)

return Series(diff)

# invert differenced value

def inverse_difference(history, yhat, interval=1):

return yhat + history[-interval]

# scale train and test data to [-1, 1]

def scale(train, test):

# fit scaler

scaler = MinMaxScaler(feature_range=(-1, 1))

scaler = scaler.fit(train)

# transform train

train = train.reshape(train.shape[0], train.shape[1])

train_scaled = scaler.transform(train)

# transform test

test = test.reshape(test.shape[0], test.shape[1])

test_scaled = scaler.transform(test)

return scaler, train_scaled, test_scaled

# inverse scaling for a forecasted value

def invert_scale(scaler, X, value):

new_row = [x for x in X] + [value]

array = np.array(new_row)

array = array.reshape(1, len(array))

inverted = scaler.inverse_transform(array)

return inverted[0, -1]

# fit an LSTM network to training data

def fit_lstm(train, batch_size, nb_epoch, neurons):

X, y = train[:, 0:-1], train[:, -1]

X = X.reshape(X.shape[0], 1, X.shape[1])

model = Sequential()

model.add(LSTM(neurons, batch_input_shape=(batch_size, X.shape[1], X.shape[2]), stateful=True))

model.add(Dense(1))

model.compile(loss='mean_squared_error', optimizer='adam')

for i in range(nb_epoch):

model.fit(X, y, epochs=1, batch_size=batch_size, verbose=0, shuffle=False)

model.reset_states()

return model

# make a one-step forecast

def forecast_lstm(model, batch_size, X):

X = X.reshape(1, 1, len(X))

yhat = model.predict(X, batch_size=batch_size)

return yhat[0,0]

#### LSTM

supervised = timeseries_to_supervised(actual_log, 1)

supervised_values = supervised.values

# split data into train and test-sets

train_lstm, test_lstm = supervised_values[0:-70], supervised_values[-70:]

# transform the scale of the data

scaler, train_scaled_lstm, test_scaled_lstm = scale(train_lstm, test_lstm)

对训练数据进行LSTM神经网络训练。

# fit the model batch,Epoch,Neurons

lstm_model = fit_lstm(train_scaled_lstm, 1, 850 , 3)

# forecast the entire training dataset to build up state for forecasting

train_reshaped = train_scaled_lstm[:, 0].reshape(len(train_scaled_lstm), 1, 1)

#lstm_model.predict(train_reshaped, batch_size=1)利用LSTM对预测数据进行分析并绘制结果

from matplotlib import pyplot

import matplotlib.pyplot as plt

import plotly.plotly as py

import plotly.tools as tls

# walk-forward validation on the test data

predictions = list()

for i in range(len(test_scaled_lstm)):

#make one-step forecast

X, y = test_scaled_lstm[i, 0:-1], test_scaled_lstm[i, -1]

yhat = forecast_lstm(lstm_model, 1, X)

# invert scaling

yhat = invert_scale(scaler, X, yhat)

# invert differencing

#yhat = inverse_difference(raw_values, yhat, len(test_scaled)+1-i)

# store forecast

predictions.append(10**yhat)

expected = actual_log[len(train_lstm) + i ]

# line plot of observed vs predicted

figsize=(12, 7)

plt.figure(figsize=figsize)

pyplot.plot(actual_vals[-70:],label='Actuals')

pyplot.plot(predictions, color = "red",label='Predicted')

pyplot.legend(loc='upper right')

pyplot.show()

LSTM也可以很好地用于这个指标预测。LSTM神经网络的重要参数是激活函数、神经元数量、批处理规模和epochs,这些参数需要进行调整以获得更好的结果

现在让我们在一个不同的指标数据中尝试一下,数据为同一时间段。

tf_df=pd.read_csv('../input/forecast-metric2/time_series_metric2.csv')

tf_df.head()

在此基础上,利用auto arima算法得到最佳参数并逐步进行预测,绘制实际和预测的结果。

actual_vals = tf_df.actuals.values

train, test = actual_vals[0:-70], actual_vals[-70:]

train_log, test_log = np.log10(train), np.log10(test)

from pyramid.arima import auto_arima

stepwise_model = auto_arima(train_log, start_p=1, start_q=1,

max_p=3, max_q=3, m=7,

start_P=0, seasonal=True,

d=1, D=1, trace=True,

error_action='ignore',

suppress_warnings=True,

stepwise=True)

history = [x for x in train_log]

predictions = list()

predict_log=list()

for t in range(len(test_log)):

#model = sm.tsa.SARIMAX(history, order=my_order, seasonal_order=my_seasonal_order,enforce_stationarity=False,enforce_invertibility=False)

stepwise_model.fit(history,enforce_stationarity=False,enforce_invertibility=False)

output = stepwise_model.predict(n_periods=1)

predict_log.append(output[0])

yhat = 10**output[0]

predictions.append(yhat)

obs = test_log[t]

history.append(obs)

#print('predicted=%f, expected=%f' % (output[0], obs))

#error = math.sqrt(mean_squared_error(test_log, predict_log))

#print('Test rmse: %.3f' % error)

# plot

figsize=(12, 7)

plt.figure(figsize=figsize)

pyplot.plot(test,label='Actuals')

pyplot.plot(predictions, color='red',label='Predicted')

pyplot.legend(loc='upper right')

pyplot.show()

感受总结

- 在这里,算法试图追踪实际数据。虽然这可能是一个很好的预测,其中错误是低的,但实际中的异常行为不能用它来识别。

- 这是一个利用预测技术进行异常检测的问题。我们试图捕捉数据中的趋势/季节性,同时优化错误以获得实际数据的精确脚本(这使得我们很难发现异常)。

- 每个指标都需要通过参数进行微调来验证,以便在使用预测检测异常时检测到异常。

- 对于数据分布不同的指标标准,还需要采用不同的方法来识别异常。

- 上篇文章中孤立森林检测了一次由多个指标组成的用例的异常,我们深入研究了其中单个指标的异常,孤立森林这样的算法将异常行为从数据中分离出来,可以用于推广到多个指标。