数学建模——线性规划类

一.线性规划

1.算法

【1】通用代码

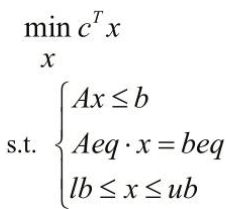

[x,y]=linprog(c,A,b,Aeq,beq,lb,ub)

例如:

max需要加负号变成min、>=需要加负号变成<=

matlab

(1)基于求解器

% LP1_1_1.m

f=[-2;-3;5];

a=[-2,5,-1;1,3,1];b=[-10;12];

aeq=[1,1,1];beq=7;

[x,y]=linprog(f,a,b,aeq,beq,zeros(3,1));

x,y=-y %最大值

x =

6.4286

0.5714

0

y =

14.5714

% 说明:在x1 x2 x3 = 6.4286 0.5714 0 的情况下,maxz = 14.5714(2)基于问题

con中根据符号分类

% LP1_1_2.m

clc,clear

prob=optimproblem('ObjectiveSense','max')

x=optimvar('x',3,'LowerBound',0);

prob.Objective=2*x(1)+3*x(2)-5*x(3);

prob.Constraints.con1=x(1)+x(2)+x(3)==7;

prob.Constraints.con2=2*x(1)-5*x(2)+x(3)>=10;

prob.Constraints.con3=x(1)+3*x(2)+x(3)<=12;

[sol,fval,flag,out]=solve(prob),sol,x;

x=sol.x,y=fvalpython

# 线性规划模型.py

from scipy.optimize import linprog

import numpy as np

c=np.array([-2,-3,5])

a=[[-2,5,-1],[1,3,1]]

b=[[-10],[12]]

aeq=[[1,1,1]]

beq=[7]

lb=[0,0,0]

ub=[None]*len(c)

bound=tuple(zip(lb,ub))

res=linprog(c,a,b,aeq,beq,bound,method='simplex',options={"disp":True})

print("最优解:",res.x)

print("目标函数最小值:",res.fun)

print("目标函数最大值:",-res.fun)

print(res)

最优解: [6.42857143 0.57142857 0. ]

目标函数最小值: -14.571428571428571

目标函数最大值: 14.571428571428571

con: array([0.])

fun: -14.571428571428571

message: 'Optimization terminated successfully.'

nit: 3

slack: array([0. , 3.85714286])

status: 0

success: True

x: array([6.42857143, 0.57142857, 0. ])【2】可以转化为线性规划

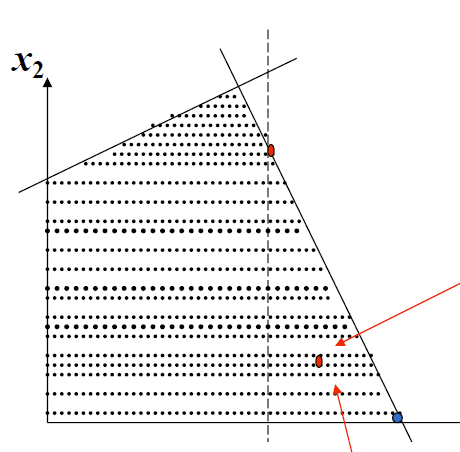

(1)绝对值

% LP_abs.m

clc,clear

c=[1,2,3,4]';

a=[1,-1,-1,1;1,-1,1,-3;1,-1,-2,3];

b=[-2,-1,-1/2]';

prob=optimproblem;

u=optimvar('u',4,'LowerBound',0);

v=optimvar('v',4,'LowerBound',0);

prob.Objective=sum(c'*(u+v));

prob.Constraints.con=a*(u-v)<=b;

[sol,fval,flag,out]=solve(prob)

x=sol.u-sol.v,minz=fval

x =

-2

0

0

0

minz =

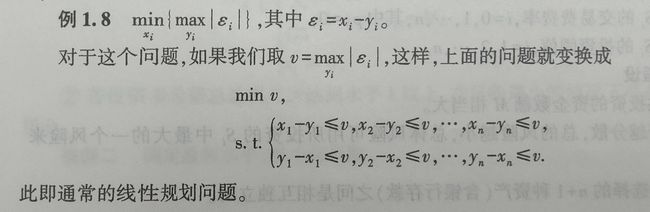

2.0000(2)min(max(q*x))

(见风投案例模型二)

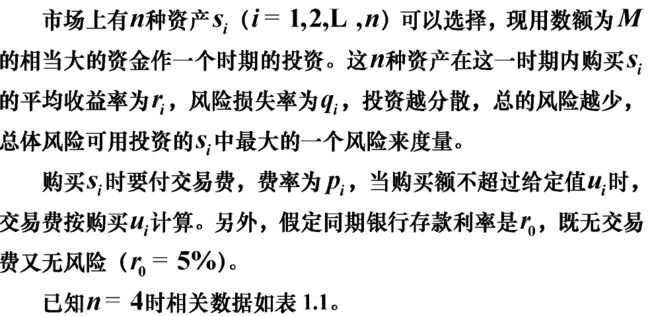

2.风投案例

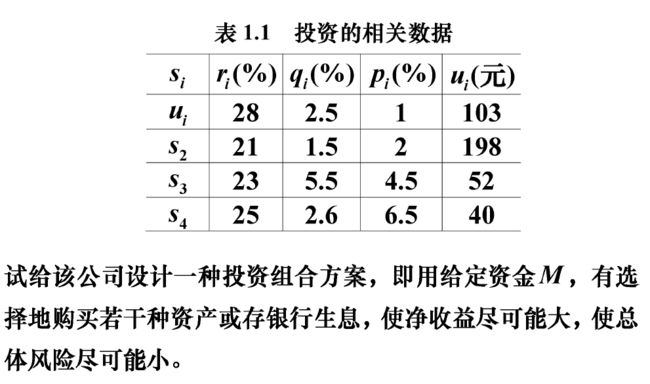

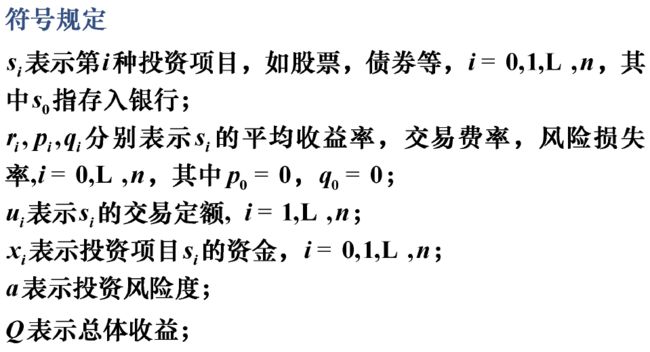

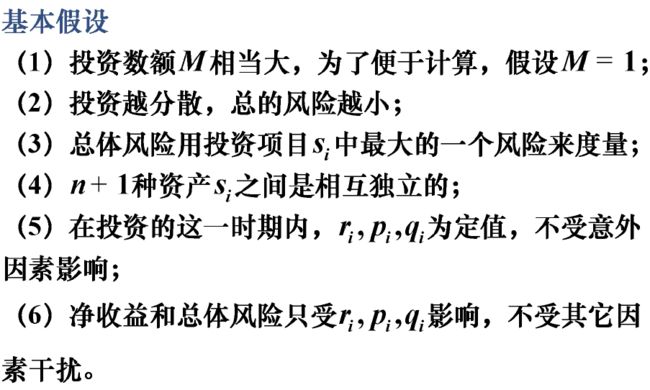

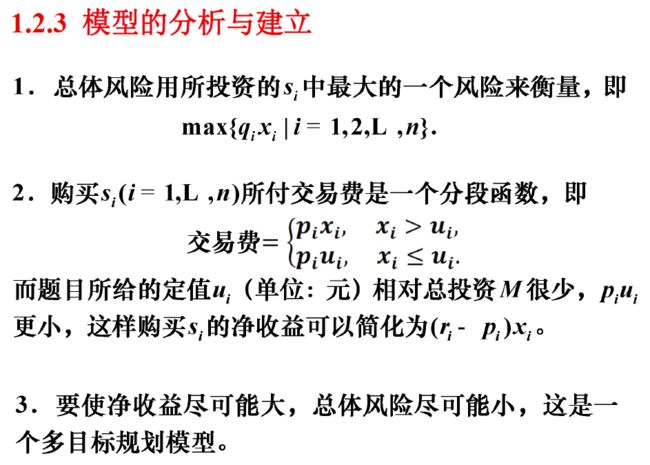

【0】题目描述

【1】模型一

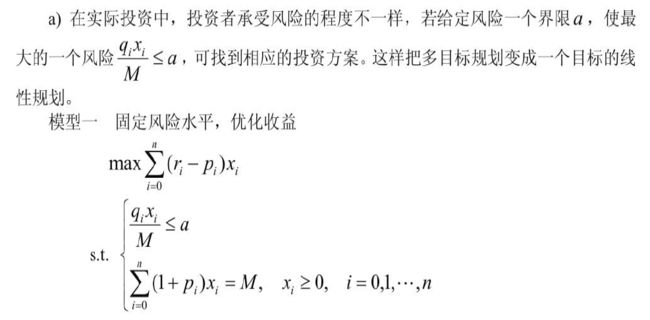

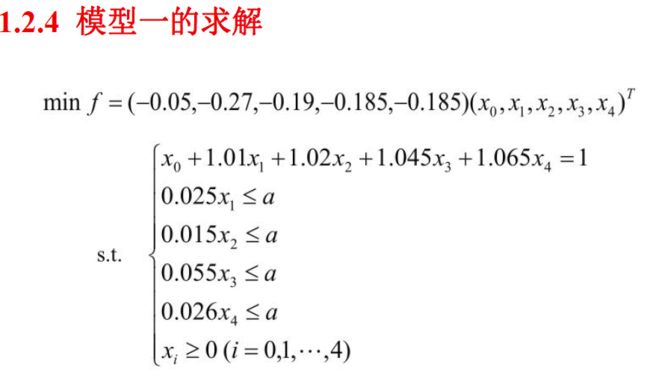

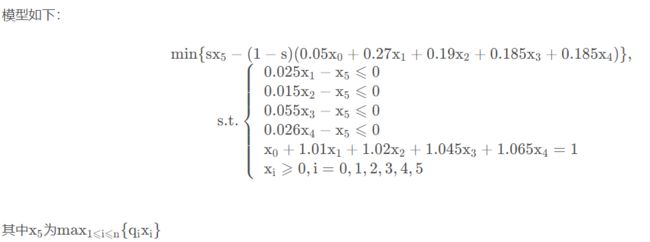

模型一:设定风险度的最大接受值,在不太冒险的情况下选择最大收益。

(1)matlab

% LP_fengtou_1.m

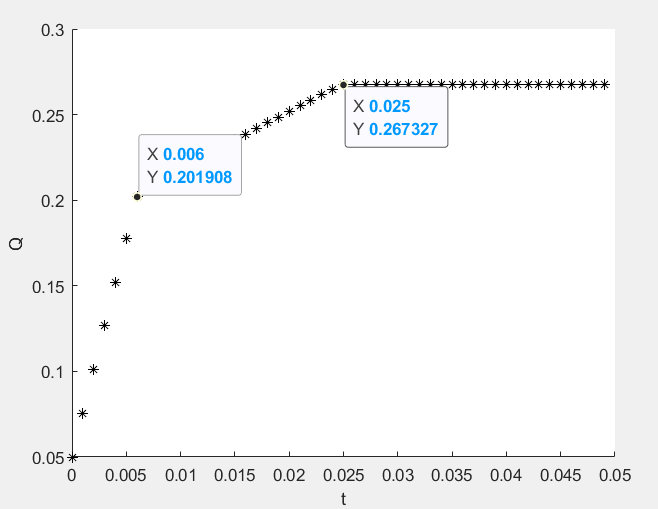

clc,clear

t=0;hold on

while t<0.05

c=[-0.05,-0.27,-0.19,-0.185,-0.185];

A=[zeros(4,1),diag([0.025,0.015,0.055,0.026])];

b=t*ones(4,1);

Aeq=[1,1.01,1.02,1.045,1.065];beq=1;

lb=zeros(5,1);

[x,Q]=linprog(c,A,b,Aeq,beq,lb);

Q=-Q;

plot(t,Q,'*k');

t=t+0.001;

end

xlabel('t'),ylabel('Q')

选择曲线的转折点作为最优投资组合。

输出转折点见模型一python代码:

鼠标在图上确定大致坐标,在循环中加入条件输出。

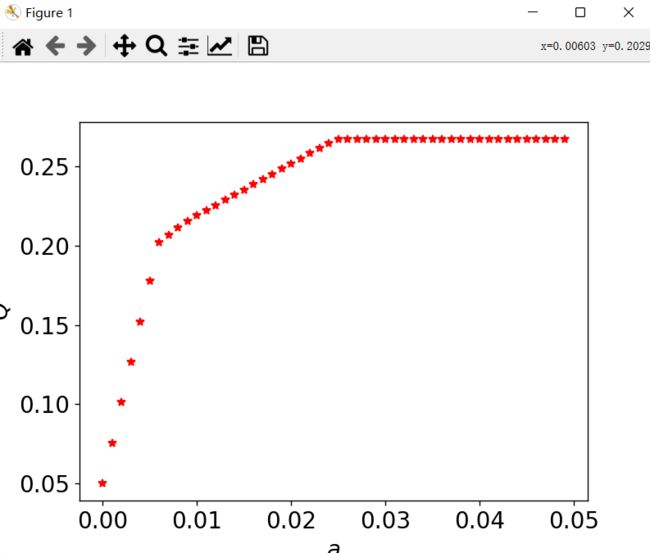

(2)python

# 风投案例.py

from scipy.optimize import linprog

import numpy as np

from numpy import ones,diag,c_,zeros

import matplotlib.pyplot as plt

plt.rc('font',size=16)

c=np.array([-0.05,-0.27,-0.19,-0.185,-0.185])

A=c_[zeros(4),diag([0.025,0.015,0.055,0.026])]

Aeq=[[1,1.01,1.02,1.045,1.065]]

beq=[1]

a=0

aa=[]

ss=[]

while a<0.05:

b=ones(4)*a

res = linprog(c, A, b, Aeq, beq)

x=res.x

Q=-res.fun

aa.append(a)

ss.append(Q)

#输出转折点

if a==0.006:

print("x=", x)

print("Q=", Q)

a=a+0.001

plt.plot(aa,ss,'r*')

plt.xlabel('$a$')

plt.ylabel('$Q$',rotation=90)

plt.savefig('模型一.png',dpi=500)

plt.show()

x= [0. 0.24 0.4 0.10909091 0.22122066]

Q= 0.20190763977806234(万元)

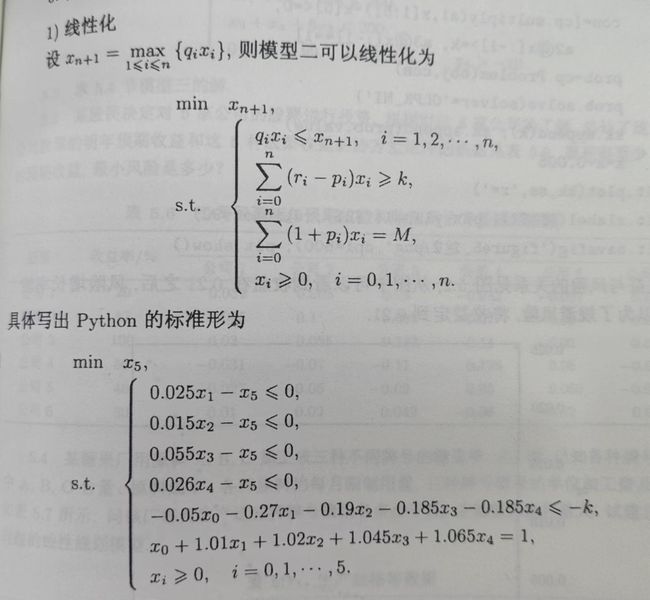

【2】模型二

模型二的目标函数:使各项目中风险最大的一项风险最小。

import numpy as np

import matplotlib.pyplot as plt

import cvxpy as cp

plt.rc('font',size=16)

x=cp.Variable(6,pos=True)

obj=cp.Minimize(x[5])

a1=np.array([0.025,0.015,0.055,0.026])

a2=np.array([0.05,0.27,0.19,0.185,0.185])

a3=np.array([1,1.01,1.02,1.045,1.065])

k=0.05

kk=[]

ss=[]

while k<0.27:

con=[cp.multiply(a1,x[1:5])-x[5]<=0,

0.05*x[0]+0.27*x[1]+0.19*x[2]+0.185*x[3]+0.185*x[4]>=k,

x[0]+1.01*x[1]+1.02*x[2]+1.045*x[3]+1.065*x[4]==1]

prob=cp.Problem(obj,con)

prob.solve(solver='CVXOPT')

#输出转折点

if abs(k-0.21)<0.0005:

print("x=",x.value)

print("风险=",prob.value)

kk.append(k)

ss.append(prob.value)

k=k+0.005

plt.plot(kk,ss,'r*')

plt.xlabel('$k$')

plt.ylabel('$R$',rotation=90)

plt.savefig('模型二.png',dpi=500)

plt.show()

x= [2.09147087e-08 3.08874349e-01 5.14790372e-01 1.40396702e-01

1.52452147e-02 7.72185738e-03]

风险= 0.00772185738406626

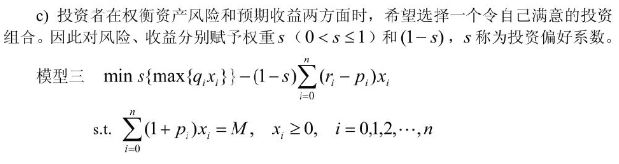

【3】模型三

模型三:风险与收益的加权线性组合。

(1)matlab

clc,clear

M=10000;prob=optimproblem;

x=optimvar('x',6,1,'LowerBound',0);

r=[0.05,0.28,0.21,0.23,0.25];

p=[0,0.01,0.02,0.045,0.065];

q=[0,0.025,0.015,0.055,0.026]';

%w=0:0.1:1;

w=[0.766,0.767,0.810,0.811,0.824,0.825,0.962,0.963,1.0];

V=[];%风险

Q=[];%收益

X=[];%最优解

prob.Constraints.con1=(1+p)*x(1:end-1)==M;

prob.Constraints.con2=q(2:end).*x(2:end-1)<=x(end);

for i=1:length(w)

prob.Objective=w(i)*x(end)-(1-w(i))*(r-p)*x(1:end-1);

[sol,fval,flag,out]=solve(prob);

xx=sol.x;

V=[V,max(q.*xx(1:end-1))];

Q=[Q,(r-p)*xx(1:end-1)];

X=[X;xx'];

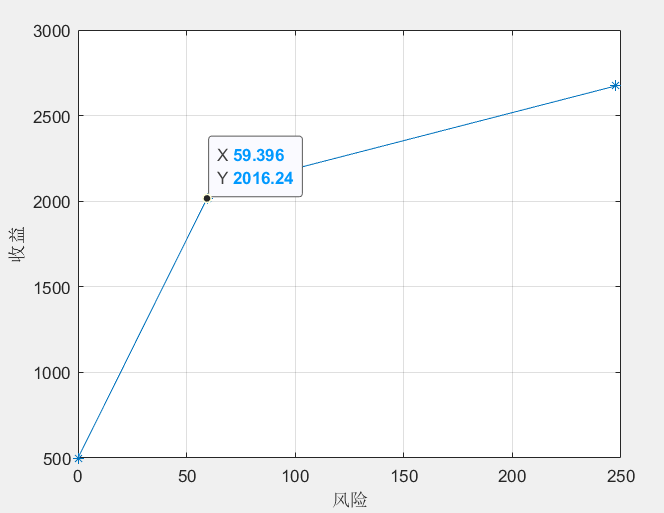

plot(V,Q,'*-');grid on

xlabel('风险');ylabel('收益')

X

end

V,Q,format

w=(权重)

[0.766, 0.767, 0.810, 0.811, 0.824, 0.825, 0.962, 0.963, 1.0];

V =(风险)

247.5248 92.2509 92.2509 78.4929 78.4929 59.3960 59.3960 0 0

Q =(收益)

1.0e+03 *

2.6733 2.1648 2.1648 2.1060 2.1060 2.0162 2.0162 0.5000 0.5000

X =

1.0e+04 *

0 0.9901 0 0 0 0.0248

0 0.3690 0.6150 0 0 0.0092

0 0.3690 0.6150 0 0 0.0092

0 0.3140 0.5233 0.1427 0 0.0078

0 0.3140 0.5233 0.1427 0 0.0078

0 0.2376 0.3960 0.1080 0.2284 0.0059(转折点处的X值)

0 0.2376 0.3960 0.1080 0.2284 0.0059

1.0000 0 0 0 0 0

1.0000 0 0 0 0 0

(2)python

from scipy.optimize import linprog

import matplotlib.pyplot as plt

plt.rc('font',size=16)

A=[[0,0.025,0,0,0,-1],[0,0,0.15,0,0,-1],[0,0,0,0.55,0,-1],[0,0,0,0,0.026,-1]]

b=[0,0,0,0]

Aeq=[[1,1.01,1.02,1.045,1.065,0]]

beq=[1]

bound=((0,None),(0,None),(0,None),(0,None),(0,None),(0,None))

s=0;ss=[];aa=[]

while s<=1:

c=[-(1-s)*0.05,-(1-s)*0.27,-(1-s)*0.19,-(1-s)*0.185,-(1-s)*0.185,s]

res=linprog(c,A,b,Aeq,beq)

ss.append(s);aa.append(-res.fun)

s=s+0.01

plt.plot(ss,aa,'r.')

plt.show()import matplotlib.pyplot as plt

import cvxpy as cp

import numpy as np

plt.rc('font',size=16)

x=cp.Variable(6)

a1=np.array([0.025,0.015,0.055,0.026])

a2=np.array([0.05,0.27,0.19,0.185,0.185])

a3=np.array([1,1.01,1.02,1.045,1.065])

con=[cp.multiply(a1,x[1:5])-x[5]<=0,a3@x[:-1]==1,x>=0]

s=0;ss=[];aa=[]

while s<=1:

obj=cp.Minimize(s*x[-1]-(1-s)*a2@x[:-1])

prob=cp.Problem(obj,con)

prob.solve(solver='GLPK_MI')

ss.append(s);aa.append(-prob.value)

s=s+0.01

plt.plot(ss,aa,'r.')

plt.show()

二.整数规划

0.分类

1.通用代码

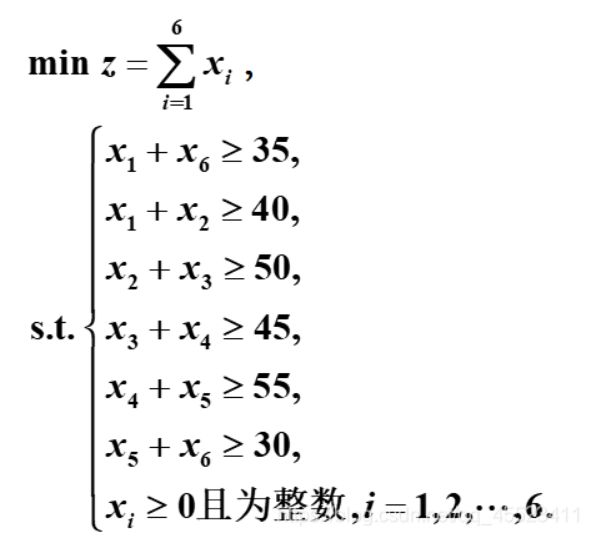

% int_LP_1.m

clc,clear,prob=optimproblem;

x=optimvar('x',6,'Type','integer','LowerBound',0);

prob.Objective=sum(x);

% 创建一个由空优化约束组成的 6×1 数组,使用 constr 初始化用于创建约束表达式的循环

coon=optimconstr(6);

a=[35,40,50,45,55,30];

con(1)=x(1)+x(6)>=35;

for i=1:5

con(i+1)=x(i)+x(i+1)>=a(i+1);

end

prob.Constraints.con=con;

[sol,fval,flag]=solve(prob)

x=sol.x

x =

35

5

45

0

55

0intlinprog函数

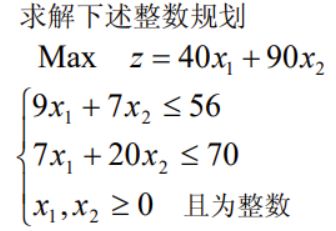

x = intlinprog(f,intcon,A,b,Aeq,beq,lb,ub):函数相比linprog多了一个参数intcon,用于标定整数变量的位置:x1、x2为整数,即intcon = [1 2]

% int_LP_intlinprog.m

c = [-40;-90];

A = [9,7;7,20];

b = [56;70];

[x,fval] = intlinprog(c,[1 2],A,b,[],[],zeros(2,1));

x,maxz=-fval

x =

4.0000

2.0000

maxz =

3402.分支定界法(剪枝)

尝试一维单调

% int_branchbunch.m

clear global;

clear;

clc;

global result; % 存储所有整数解

global lowerBound; % 下界

global upperBound; % 上界

global count; % 用以判断是否为第一次分支

count = 1;

f = [-40, -90];

A = [8, 7;7, 20;];

b = [56; 70];

Aeq = [];

beq = [];

lbnd = [0; 0];

ubnd = [inf; inf];

% f = [-3 2 -5];

% A = [1 2 -1;1 4 1;1 1 0;0 4 1];

% b = [2;4;3;6];

% Aeq = [];

% beq = [];

% lbnd=[0 0 0];

% ubnd=[1 1 1];

BinTree = createBinTreeNode({f, A, b, Aeq, beq, lbnd, ubnd});

if ~isempty(result)

[fval,flag]=min(result(:,end)); % result中每一行对应一个整数解及对应的函数值

Result=result(flag,:);

disp('该整数规划问题的最优解为:');

disp(Result(1,1:end-1));

disp('该整数规划问题的最优值为:');

disp(Result(1,end));

else

disp('该整数规划问题无可行解');

end

function BinTree = createBinTreeNode(binTreeNode)

global result;

global lowerBound;

global upperBound;

global count;

if isempty(binTreeNode)

return;

else

BinTree{1} = binTreeNode;

BinTree{2} = [];

BinTree{3} = [];

[x, fval, exitflag] = linprog(binTreeNode{1}, binTreeNode{2}, binTreeNode{3}, ...

binTreeNode{4}, binTreeNode{5}, binTreeNode{6}, binTreeNode{7});

if count == 1

% upperBound = 0; % 初始下界为空

lowerBound = fval;

count = 2;

end

if ~IsInRange(fval)

return;

end

if exitflag == 1

flag = [];

% 寻找非整数解分量

for i = 1 : length(x)

if round(x(i)) ~= x(i)

flag = i;

break;

end

end

% 分支

if ~isempty(flag)

lowerBound = max([lowerBound; fval]);

OutputLowerAndUpperBounds();

lbnd = binTreeNode{6};

ubnd = binTreeNode{7};

lbnd(flag, 1) = ceil(x(flag, 1)); % 朝正无穷四舍五入

ubnd(flag, 1) = floor(x(flag, 1));

% 进行比较,优先选择目标函数较大的进行分支

[~, fval1] = linprog(binTreeNode{1}, binTreeNode{2}, binTreeNode{3}, ...

binTreeNode{4}, binTreeNode{5}, binTreeNode{6}, ubnd);

[~, fval2] = linprog(binTreeNode{1}, binTreeNode{2}, binTreeNode{3}, ...

binTreeNode{4}, binTreeNode{5}, lbnd, binTreeNode{7});

if fval1 < fval2

% 创建左子树

BinTree{2} = createBinTreeNode({binTreeNode{1}, binTreeNode{2}, binTreeNode{3}, ...

binTreeNode{4}, binTreeNode{5}, binTreeNode{6}, ubnd});

% 创建右子树

BinTree{3} = createBinTreeNode({binTreeNode{1}, binTreeNode{2}, binTreeNode{3}, ...

binTreeNode{4}, binTreeNode{5}, lbnd, binTreeNode{7}});

else

% 创建右子树

BinTree{3} = createBinTreeNode({binTreeNode{1}, binTreeNode{2}, binTreeNode{3}, ...

binTreeNode{4}, binTreeNode{5}, lbnd, binTreeNode{7}});

% 创建左子树

BinTree{2} = createBinTreeNode({binTreeNode{1}, binTreeNode{2}, binTreeNode{3}, ...

binTreeNode{4}, binTreeNode{5}, binTreeNode{6}, ubnd});

end

else

upperBound = min([upperBound; fval]);

OutputLowerAndUpperBounds();

result = [result; [x', fval]];

return;

end

else

% 剪枝

return;

end

end

end

function y = IsInRange(fval)

global lowerBound;

global upperBound;

if isempty(upperBound) & fval >= lowerBound

y = 1;

else if (fval >= lowerBound & fval <= upperBound)

y = 1;

else

y = 0;

end

end

end

function y = OutputLowerAndUpperBounds()

global lowerBound;

global upperBound;

disp("此时下界、上界分别为");

disp(lowerBound);

if isempty(upperBound)

disp(' 无上界')

else

disp(upperBound);

end

end

该整数规划问题的最优解为:

4 2

该整数规划问题的最优值为:

-3403.割平面法

割去小数部分,尝试二维单调

function [intx,intf] = DividePlane(A,c,b,baseVector)

%功能:用割平面法求解整数规划

%调用格式:[intx,intf]=DividePlane(A,c,b,baseVector)

%其中, A:约束矩阵;

% c:目标函数系数向量;

% b:约束右端向量;

% baseVector:初始基向量;

% intx:目标函数取最值时的自变量值;

% intf:目标函数的最值;

sz = size(A);

nVia = sz(2);%获取有多少决策变量

n = sz(1);%获取有多少约束条件

xx = 1:nVia;

if length(baseVector) ~= n

disp('基变量的个数要与约束矩阵的行数相等!');

mx = NaN;

mf = NaN;

return;

end

M = 0;

sigma = -[transpose(c) zeros(1,(nVia-length(c)))];

xb = b;

%首先用单纯形法求出最优解

while 1

[maxs,ind] = max(sigma);

%--------------------用单纯形法求最优解--------------------------------------

if maxs <= 0 %当检验数均小于0时,求得最优解。

vr = find(c~=0 ,1,'last');

for l=1:vr

ele = find(baseVector == l,1);

if(isempty(ele))

mx(l) = 0;

else

mx(l)=xb(ele);

end

end

if max(abs(round(mx) - mx))<1.0e-7 %判断最优解是否为整数解,如果是整数解。

intx = mx;

intf = mx*c;

return;

else %如果最优解不是整数解时,构建切割方程

sz = size(A);

sr = sz(1);

sc = sz(2);

[max_x, index_x] = max(abs(round(mx) - mx));

[isB, num] = find(index_x == baseVector);

fi = xb(num) - floor(xb(num));

for i=1:(index_x-1)

Atmp(1,i) = A(num,i) - floor(A(num,i));

end

for i=(index_x+1):sc

Atmp(1,i) = A(num,i) - floor(A(num,i));

end

Atmp(1,index_x) = 0; %构建对偶单纯形法的初始表格

A = [A zeros(sr,1);-Atmp(1,:) 1];

xb = [xb;-fi];

baseVector = [baseVector sc+1];

sigma = [sigma 0];

%-------------------对偶单纯形法的迭代过程----------------------

while 1

%----------------------------------------------------------

if xb >= 0 %判断如果右端向量均大于0,求得最优解

if max(abs(round(xb) - xb))<1.0e-7

%如果用对偶单纯形法求得了整数解,则返回最优整数解

vr = find(c~=0 ,1,'last');

for l=1:vr

ele = find(baseVector == l,1);

if(isempty(ele))

mx_1(l) = 0;

else

mx_1(l)=xb(ele);

end

end

intx = mx_1;

intf = mx_1*c;

return;

else %如果对偶单纯形法求得的最优解不是整数解,继续添加切割方程

sz = size(A);

sr = sz(1);

sc = sz(2);

[max_x, index_x] = max(abs(round(mx_1) - mx_1));

[isB, num] = find(index_x == baseVector);

fi = xb(num) - floor(xb(num));

for i=1:(index_x-1)

Atmp(1,i) = A(num,i) - floor(A(num,i));

end

for i=(index_x+1):sc

Atmp(1,i) = A(num,i) - floor(A(num,i));

end

Atmp(1,index_x) = 0; %下一次对偶单纯形迭代的初始表格

A = [A zeros(sr,1);-Atmp(1,:) 1];

xb = [xb;-fi];

baseVector = [baseVector sc+1];

sigma = [sigma 0];

continue;

end

else %如果右端向量不全大于0,则进行对偶单纯形法的换基变量过程

minb_1 = inf;

chagB_1 = inf;

sA = size(A);

[br,idb] = min(xb);

for j=1:sA(2)

if A(idb,j)<0

bm = sigma(j)/A(idb,j);

if bm0

bz = xb(j)/A(j,ind);

if bz

% int_LP_divideplane.m

c = [-1;-1]; % 不要加松弛变量

A = [-1 1 1 0;3 1 0 1]; % 加上松弛变量

b = [1;4];

[x,fval] = DividePlane(A,c,b,[3 4]); % 松弛变量 3 4

x,maxz=fval

x =

1.0000 1.0000

maxz =

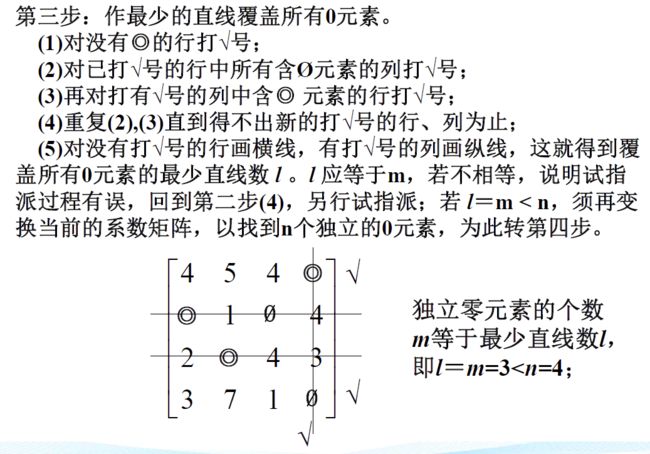

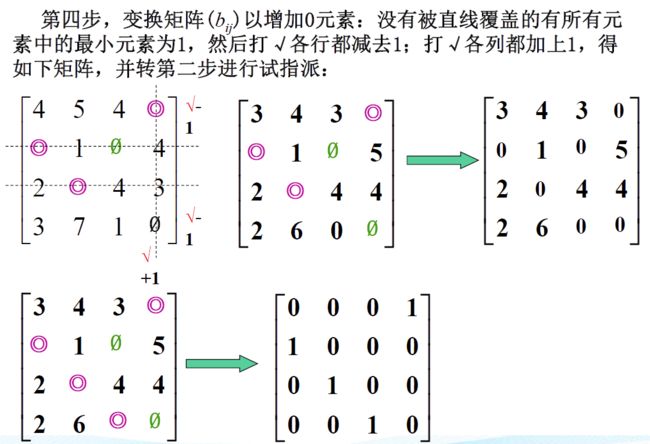

-24.匈牙利算法

【1】

【2】

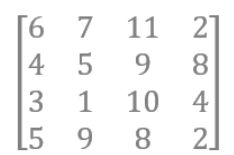

% int_XiongYaLi.m

c = [6 7 11 2;4 5 9 8;3 1 10 4;5 9 8 2];

a = zeros(8,16);

for i = 1:4

a(i,(i-1)*4+1:4*i) = 1;

a(4+i,i:4:16) = 1;

end

b = ones(8,1);

[x,y] = linprog(c,[],[],a,b,zeros(16,1),ones(16,1));

X = reshape(x,4,4)

opt = y

% X =

%

% 0 0 0 1

% 1 0 0 0

% 0 1 0 0

% 0 0 1 0

%

%

% opt =

%

% 15

A=[6 7 11 2;

4 5 9 8;

3 1 10 4;

5 9 8 2];

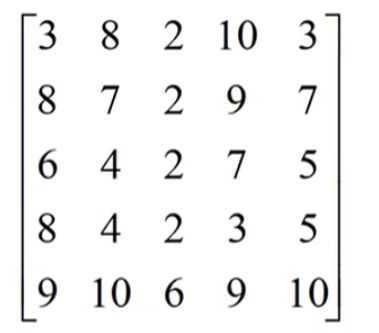

% A = [3 8 2 10 3;8 7 2 9 7;6 4 2 7 5;8 4 2 3 5;9 10 6 9 10];

B=Hungary(A);

[~,b]=linear_assignment(A,B)

% b =

% 4 1 8 2

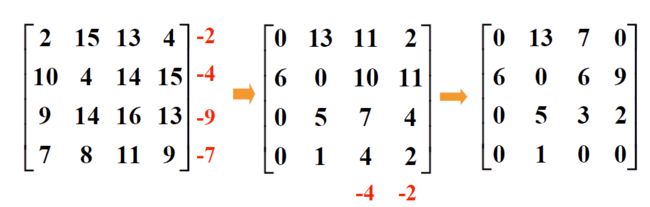

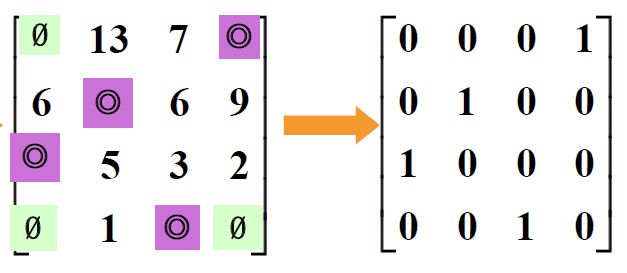

function res=Hungary(N)

%输入的矩阵应N*N的

[a,~]=size(N);

%第一步每一行减去当前行最小值

for ii = 1:a

N(ii,:)= N(ii,:)-min( N(ii,:));

end

%第二步每一列减去当前列最小值

for ii = 1:a

N(:,ii)= N(:,ii)-min( N(:,ii));

end

num=0;

while num~=a

[num,N_min,del_hang,del_lie]=line_count(N);

if num ~=a

for ii=1:a

if del_hang(ii)~=ii

N(ii,:) = N(ii,:)-N_min;

end

if del_lie(ii)==ii

N(:,ii) = N(:,ii)+N_min;

end

end

else

res=N;

end

end

function [num,M_min,del_hang,del_lie]=line_count(M)

[a,~]=size(M);

num=0;

h=0;

del_hang=zeros(a,1);

del_lie=zeros(a,1);

for ii=1:a

del=ii-h;

[~,b]=size(find(M(del,:)==0));

if b>= 2

M(del,:)=[];

h=h+1;

del_hang(ii)=ii; %得到被覆盖的行数

num=num+1;

end

end

l=0;

for ii=1:a

del=ii-l;

[b,~]=size(find(M(:,del)==0));

if b >=1

M(:,del)=[];

l=l+1;

del_lie(ii)=ii; %得到被覆盖的列数

num=num+1;

end

end

M_min=min(min(M));

end

end

function [place,res]=linear_assignment(M,N)

%N是n维矩阵,N是经过Hungary处理的

%M是未处理前的

[a,~]=size(N);

x=0;

place=zeros(1,a);

res=zeros(1,a);

judge=zeros(1,a);

while find(N==0)

for ii=1:a

judge(ii)=length(find(N(ii,:)==0));

end

judge(find(judge==0))=[];

if min(judge)==1

for ii=1:a

if length(find(N(ii,:)==0))==1 %先选出行中只有1个0

x=x+1;

place(x)=ii+(find(N(ii,:)==0)-1)*a; %得到矩阵中的位置

h=find(N(ii,:)==0);

N(ii,:)=1./zeros(1,a);

N(:,h)=1./zeros(a,1);

end

end

end

for ii=1:a

judge(ii)=length(find(N(ii,:)==0));

end

judge(find(judge==0))=[];

if min(judge)==2

x=x+1;

q=find(N==0);

place(x)=q(1);

N(mod(q(1),a),:)=1./zeros(1,a);

N(:,fix(q(1)/a)+1)=1./zeros(a,1);

end

end

[place,~]=sort(place);

for ii=1:length(place)

res(ii)=M(place(ii));

end

end 5.0-1规划

【1】intlinprog函数

0-1规划问题也可以看做区间在[0,1]的整数规划,下面利用intlinprog函数进行计算

% intlinprog_01.m

c = [-3 2 -5]';

A = [1 2 -1;1 4 1;1 1 0;0 4 1];

b = [2;4;3;6];

[x,fval] = intlinprog(c,[1 2 3],A,b,[],[],zeros(3,1),ones(3,1));

x,maxz = -fval

x =

1

0

1

maxz =

8【2】指派问题

(1)纯0-1整数规划

c=np.array([[4,8,7,15,12],

[7,9,17,14,10],

[6,9,12,8,7],

[6,7,14,6,10],

[6,9,12,10,6]])

x=cp.Variable((5,5),integer=True)

obj=cp.Minimize(cp.sum(cp.multiply(c,x)))

con=[0<=x,x<=1,

cp.sum(x,axis=0,keepdims=True)==1,

cp.sum(x,axis=1,keepdims=True)==1]

prob=cp.Problem(obj,con)

prob.solve(solver='GLPK_MI')

print("最优值为:",prob.value)

print("最优解为:\n",x.value)

最优值为: 34.0

最优解为:

[[0. 0. 1. 0. 0.]

[0. 1. 0. 0. 0.]

[1. 0. 0. 0. 0.]

[0. 0. 0. 1. 0.]

[0. 0. 0. 0. 1.]](2)广义指派

5*x(1)+4*x(2)<=24+y(1)M; %M是充分大的数

7*x(1)+3*x(2)<=45+y(2)M;

y(1)+y(2)=1;i=1,2,3为三种生产方式

x(i)为产量;c(i)为每件产品的成本;k(i)为每种方式的固定成本

min z=(k(1)*y(1)+c(1)*x(1))+(k(2)*y(2)+c(2)*x(2))+(k(3)*y(3)+c(3)*x(3));

y(i)*m<=x(i)<=y(i)*M; %m充分小,M充分大

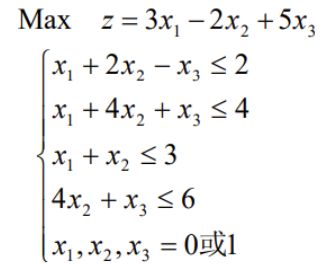

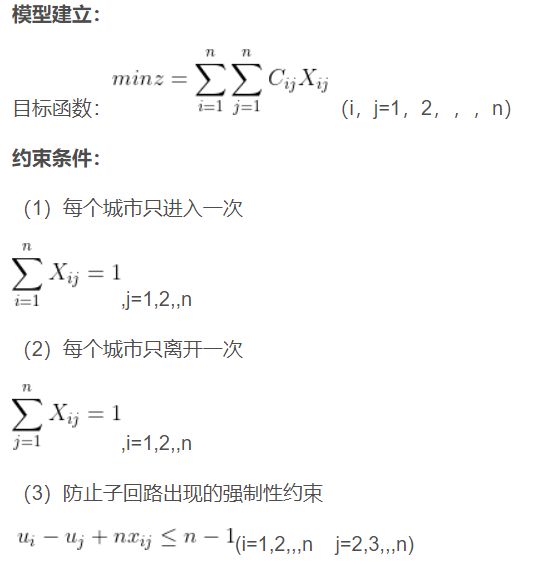

y(i)=0 or 1;【3】旅行商问题(TSP)

(司P31)比赛项目排序问题中,由于开始项目和结束项目没有连接,可引入虚拟项目15,与各项目的权重为0

三.非线性规划

- 算法

【1】二次规划

目标函数二次,约束条件线性

H为实对称矩阵

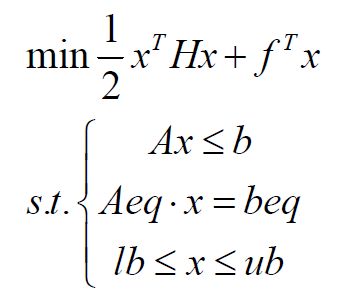

[x,fval]=quadprog(H,f,A,b,Aeq,beq,lb,ub,x0)

% DLP_1.m

H=[4,-4;-4,8];

f=[-6;3];

a=[1,1;4,1];

b=[3;9];

[x,fval]=quadprog(H,f,a,b,[],[],zeros(2,1))

x =

2.0854

0.6585

fval =

-5.5976% DLP_2.m

x0 = [1;1];

A=[1,1;4,1];

b=[3;9];

Aeq = [];

beq = [];

lb = [0;0];

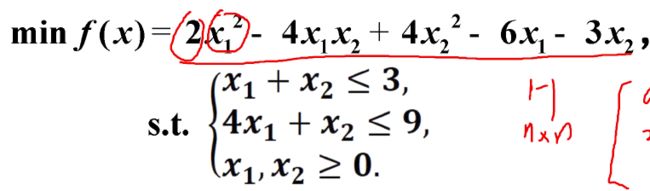

[x,fval] = fmincon(@fun,x0,A,b,Aeq,beq,lb)

function f = fun(x)

f = 2*x(1)-4*x(1)*x(2)+4*x(2)^2-6*x(1)-3*x(2)

end

x =

2.0000

1.0000

fval =

-15.0000【2】无约束非线性规划

无约束优化问题有局部最优解的充分条件:梯度=0;Hesse矩阵正定

% NLP_nocon.m

clc,clear

f = @(x) x(1)^3-x(2)^3+3*x(1)^2+3*x(2)^2-9*x(1);

g = @(x) -f(x);

[m1,n1] = fminunc(f,[0,0])%求极小值

[m2,n2] = fminsearch(g,[0,0]);%求极大值

m2,n2=-n2

m1 =

1.0000 -0.0000

n1 =

-5

m2 =

-3.0000 2.0000

n2 =

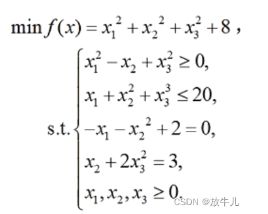

31.0000【3】有约束非线性规划

% NLP_con_1.m

%[x,fval]=fmincon('fun1',x0,A,b,Aeq,beq,lb,ub,'fun2')

[x,y]=fmincon('fun1',rand(3,1),[],[],[],[],zeros(3,1),[],'fun2')

function f = fun1(x);

f=sum(x.^2)+8;

end

function [g,h] = fun2(x)

g=[-x(1)^2+x(2)-x(3)^2

x(1)+x(2)^2+x(3)^3-20];

h=[-x(1)-x(2)^2+2

x(2)+2*x(3)^2-3];

end

x =

0.5522

1.2033

0.9478

y =

10.6511% NLP_con_2.m

clc,clear

x = optimvar('x',3,'LowerBound',0);

prob = optimproblem('Objective',sum(x.^2)+8);

con1 = [-x(1)^2+x(2)-x(3)^2 <= 0

x(1)+x(2)^2+x(3)^3 <= 20];

con2 = [-x(1)-x(2)^2+2 == 0

x(2)+2*x(3)^2 == 3];

prob.Constraints.con1 = con1;

prob.Constraints.con2 = con2;

x0.x = rand(3,1);

[s,f,flag,out] = solve(prob,x0);

s.x,f(1)只有等式约束

拉格朗日法

(2)一般形式

罚函数法

不等式约束g(x,i)<=0 等式约束h(x,j)=0

不等式 g(x,i)<=0 转化为 等式 max(0,g(x,i))=0

罚函数:T(x.M)=f(x)+M*sum(max(0,g(x,i)))+M*sum(h(x,j)^2)【4】凸规划(f''>=0)

(1)判定:Hesse处处半正定

% NLP_TU.m

clc,clear

prob=optimproblem;

x=optimvar('x',2,'LowerBound',0);

prob.Objective=sum(x.^2)-4*x(1)+4;

con=[-x(1)+x(2)-2<=0

x(1)^2-x(2)+1<=0];

prob.Constraints.con=con;

x0.x=rand(2,1)

[sol,fval,flag,out]=solve(prob,x0),sol.x(2)K-T条件

只要是最优点,一定满足K-T条件

若为凸规划,则充要条件

【5】蒙特卡洛法

% MTKL.m

clc,clear

rng(0) %rng('shuffle')

p0=0;n=10^6;tic

for i=1:n

x=randi([0,99],1,5);

[f,g]=mengte(x);

if all(g<=0)

if p02.LINGO

model:

sets:

row/1..4/:b;

col/1..5/:c1,c2,x;

link(row,col):a;

endsets

data:

c1=1,1,3,4,2;

c2=-8,-2,-3,-1,-2;

a=1 1 1 1 1

1 2 2 1 6

2 1 6 0 0

0 0 1 1 5;

b=400,800,200,200;

enddata

max=@sum(col:c1*x^2+c2*x);

@for(row(i):@sum(col(j):a(i,j)*x(j))

3.案例+灵敏度分析

(司P42)

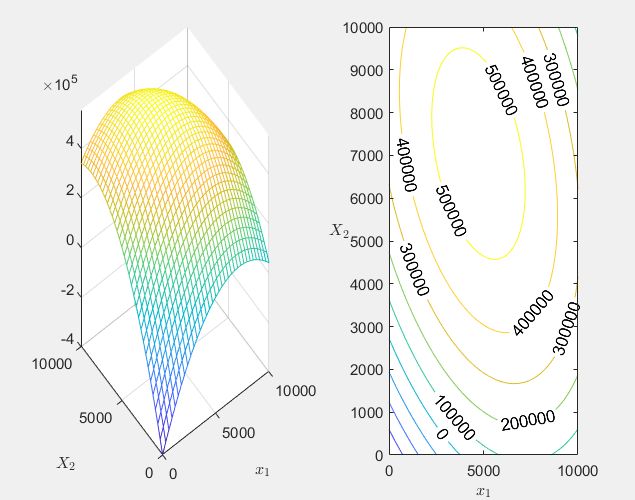

clc,clear,format long g,close all

syms x1 x2

f=(339-0.01*x1-0.003*x2)*x1+(399-0.004*x1-0.01*x2)*x2-(400000+195*x1+225*x2);

f=simplify(f);

f1=diff(f,x1);f2=diff(f,x2);

[x10,x20]=solve(f1,f2);

x10=round(double(x10));x20=round(double(x20));

f0=subs(f,{x1,x2},{x10,x20});

f0=double(f0);

subplot(121),fmesh(f,[0,10000,0,10000]),title('')

xlabel('$x_1$','Interpreter','latex')

ylabel('$X_2$','Interpreter','latex')

subplot(122),L=fcontour(f,[0,10000,0,10000]);

contour(L.XData,L.YData,L.ZData,'ShowText','on')

xlabel('$x_1$','Interpreter','latex')

ylabel('$X_2$','Interpreter','latex','Rotation',0)

p1=339-0.01*x10-0.003*x20

p2=399-0.004*x10-0.01*x20

c=400000+195*x10+225*x20 %总支出

rate=f0/c %利润

x10

x20

灵敏度分析

clc,clear,format long g,close all

syms x1 x2 a

f=(339-0.01*x1-0.003*x2)*x1+(399-0.004*x1-0.01*x2)*x2-(400000+195*x1+225*x2);

f=simplify(f);

f1=diff(f,x1);f2=diff(f,x2);

[x10,x20]=solve(f1,f2);

subplot(121),fplot(x10,[0.002,0.02]),title('') %x1关于a的曲线

xlabel('$x_1$','Interpreter','latex')

ylabel('$X_2$','Interpreter','latex','Rotation',0)

subplot(122),fplot(x20,[0.002,0.02]),title('') %x2关于a的曲线

xlabel('$x_1$','Interpreter','latex')

ylabel('$X_2$','Interpreter','latex','Rotation',0)

dx1=diff(x10,a);dx10=subs(dx1,a,0.01);dx10=double(dx10);

sx1a=dx10*0.01/4735;

dx2=diff(x20,a);dx20=subs(dx2,a,0.01);dx20=double(dx20);

sx2a=dx20*0.01/7043;

F=subs(f,{x1,x2},{x10,x20});

F=simplify(F);

figure,fplot(F,[0.002,0.02]),title('')

xlabel('$x_1$','Interpreter','latex')

ylabel('$X_2$','Interpreter','latex','Rotation',0)

Sya=-4735^2*0.01/553641;

f3=subs(f,{x1,x2,a},{4735,7043,0.011});

f3=double(f3);

f4=subs(F,a,0.011) %近似最优利润

f4=double(f4) %最优利润

delta=(f4-f3)/f4 %利润的相对误差四.多目标规划

1.多目标规划

max f1(x)=2x(1)+3x(2)

min f2(x)=x(1)+2x(2)

0.5x(1)+0.25x(2)<=8

0.2x(1)+0.2x(2)<=4

x(1)+x(2)>=10

x(1)>=0

x(2)>=0

【1】线性加权

min 0.5(-f1)+0.5(f2)

结果:

x(1)=7,x(2)=13

【2】理想点

分别求解得f1=-53,f2=10

新的目标函数 min f=[-2x(1)-3x(2)+53]^2+[x(1)+2x(2)-10]^2

结果:

x(1)=13.36,x(2)=5.28

【3】序贯

分别求解得f1=-53

加入条件-2x(1)-3x(2)=-53求f2

结果:

x(1)=7,x(2)=13

clc,clear,prob=optimproblem;

x=optimvar('x',2,'LowerBound',0);

c1=[-2,-3];c2=[1,2];

a=[0.5,0.25;0.2,0.2;1,5;-1,-1];

b=[8;4;72;-10];

prob.Constraints.con1=a*x<=b

obj1=0.5*c1*x+0.5*c2*x

prob1=prob;prob1.Objective=obj1;

[sol1,fval1]=solve(prob1),sx=sol1.x

f1=-c1*sx,f2=c2*sx

prob21=prob;prob21.Objective=c1*x;

[sol21,fval21]=solve(prob21),sx21=sol21.x

prob22=prob;prob22.Objective=c2*x;

[sol22,fval22]=solve(prob22),sx22=sol22.x

prob23=prob;

prob23.Objective=(c1*x-fval21)^2+(c2*x-fval22)^2;

[sol23,fval23]=solve(prob23),sx23=sol23.x

prob3=prob;prob3.Objective=c2*x;

prob3.Constraints.con2=c1*x==fval21;

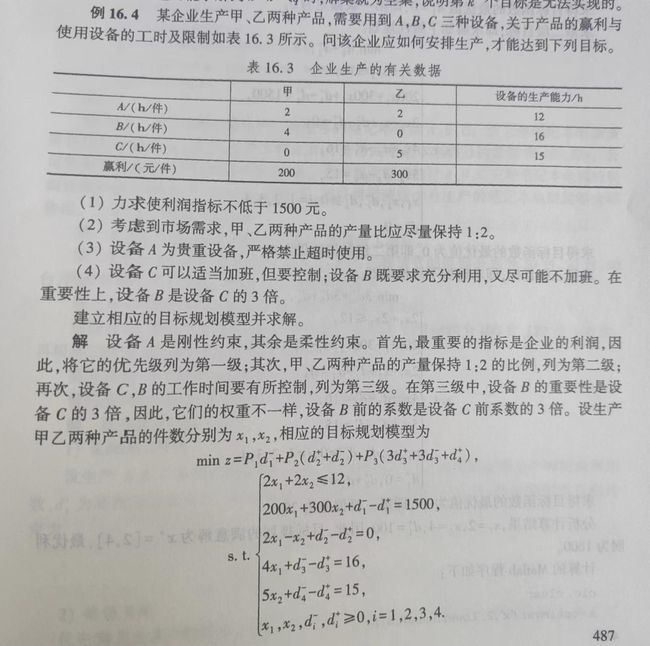

[sol3,fval3]=solve(prob3),sx3=sol3.x2.目标规划

正负偏差变量

软硬约束

“尽量”

优先权

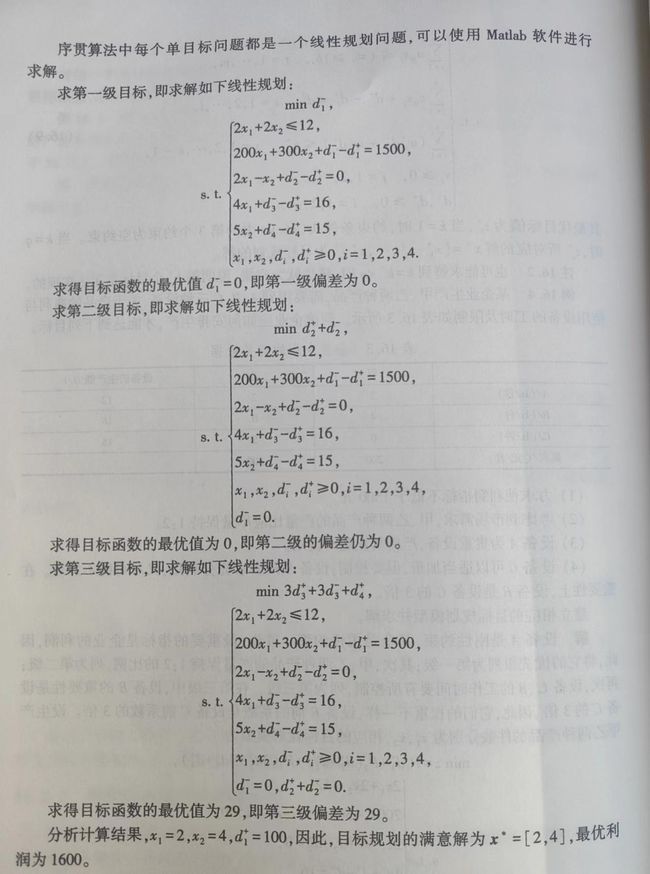

序贯算法:

根据优先级排序,将目标规划分解成一系列单目标规划,依次求解

clc,clear

x=optimvar('x',2,'LowerBound',0);

dp=optimvar('dp',4,'LowerBound',0);

dm=optimvar('dm',4,'LowerBound',0);

p=optimproblem('ObjectiveSense','min');

p.Constraints.con1=2*sum(x)<=12;

con2=[200*x(1)+300*x(2)+dm(1)-dp(1)==1500

2*x(1)-x(2)+dm(2)-dp(2)==0

4*x(1)+dm(3)-dp(3)==16

5*x(2)+dm(4)-dp(4)==15];

p.Constraints.con2=con2;

goal=100000*ones(3,1);

mobj=[dm(1);dp(2)+dm(2);3*dp(3)+3*dm(3)+dp(4)];

for i=1:3

p.Constraints.con3=[mobj<=goal];

p.Objective=mobj(i);

[sx,fval]=solve(p);

fprintf('第%d级目标计算结果如下:\n',i)

fval,xx=sx.x,sdm=sx.dm,sdp=sx.dp

goal(i)=fval;

end