@线性回归模型

原文地址:http://www.seyvoue.com/posts/91fff0b1/

声明:版权所有,转载请联系作者并注明出

overview: linear regression with one variable or multiple variables, gradient descent, normal equation, feature scaling, contour plot.

Example

| Input x | Output y |

|---|---|

| 0 | 2 |

| 1 | 4 |

| 2 | 6 |

| 3 | 8 |

从表中的数据,可以用 hθ(x)=2+2x ,拟合表中的数据。

于是当给定一个新的输入,如 x=4 ,可以预测出输出 y=2+2∗4=10

一元线性回归

建模

Hypothesis:

Cost Function:

Gradient Descent:

其中,公式 (1-3) 即,

repeatuntilconvergence:{

}

另外, α 为 learning rate.

应用

该实例来源于 coursera machine learning programming exercise1.

- DataSet

数据集的部分内容如下,完整数据集在这里。

| Population of a city (x) | Profit of a food truck in that city (y) |

|---|---|

| 6.1101 | 17.592 |

| 5.5277 | 9.1302 |

| 8.5186 | 13.662 |

| … | … |

- 目的:

如果你需要在别的城市开一家分店,经过调查,你发现利润与城市的人口有关,现需要根据已掌握的数据,去预测在 A 市开分店的收益会如何?(即告诉你 A 市的人口,利用拟合出的模型,去预测可能的利润)

完整代码

完整代码可在这里下载。

下面只列出其中的主程序:

%% Linear regression with one variable

% x refers to the population size in 10,000s

% y refers to the profit in $10,000s

%

%% Initialization

clear ; close all; clc

%% ==================== Part 1: Basic Function ====================

% Complete warmUpExercise.m

fprintf('Running warmUpExercise ... \n');

fprintf('5x5 Identity Matrix: \n');

warmUpExercise()

fprintf('Program paused. Press enter to continue.\n');

pause;

%% ======================= Part 2: Plotting =======================

fprintf('Plotting Data ...\n')

data = load('ex1data1.txt');

X = data(:, 1); y = data(:, 2);

m = length(y); % number of training examples

% Plot Data

% Note: You have to complete the code in plotData.m

plotData(X, y);

fprintf('Program paused. Press enter to continue.\n');

pause;

%% =================== Part 3: Cost and Gradient descent ===================

X = [ones(m, 1), data(:,1)]; % Add a column of ones to x

theta = zeros(2, 1); % initialize fitting parameters

% Some gradient descent settings

iterations = 1500;

alpha = 0.01;

fprintf('\nTesting the cost function ...\n')

% compute and display initial cost

J = computeCost(X, y, theta);

fprintf('With theta = [0 ; 0]\nCost computed = %f\n', J);

fprintf('Expected cost value (approx) 32.07\n');

% further testing of the cost function

J = computeCost(X, y, [-1 ; 2]);

fprintf('\nWith theta = [-1 ; 2]\nCost computed = %f\n', J);

fprintf('Expected cost value (approx) 54.24\n');

fprintf('Program paused. Press enter to continue.\n');

pause;

fprintf('\nRunning Gradient Descent ...\n')

% run gradient descent

theta = gradientDescent(X, y, theta, alpha, iterations);

% print theta to screen

fprintf('Theta found by gradient descent:\n');

fprintf('%f\n', theta);

fprintf('Expected theta values (approx)\n');

fprintf(' -3.6303\n 1.1664\n\n');

% Plot the linear fit

hold on; % keep previous plot visible

plot(X(:,2), X*theta, '-')

legend('Training data', 'Linear regression')

hold off % don't overlay any more plots on this figure

% Predict values for population sizes of 35,000 and 70,000

predict1 = [1, 3.5] *theta;

fprintf('For population = 35,000, we predict a profit of %f\n',...

predict1*10000);

predict2 = [1, 7] * theta;

fprintf('For population = 70,000, we predict a profit of %f\n',...

predict2*10000);

fprintf('Program paused. Press enter to continue.\n');

pause;

%% ============= Part 4: Visualizing J(theta_0, theta_1) =============

fprintf('Visualizing J(theta_0, theta_1) ...\n')

% Grid over which we will calculate J

theta0_vals = linspace(-10, 10, 100);

theta1_vals = linspace(-1, 4, 100);

% initialize J_vals to a matrix of 0's

J_vals = zeros(length(theta0_vals), length(theta1_vals));

% Fill out J_vals

for i = 1:length(theta0_vals)

for j = 1:length(theta1_vals)

t = [theta0_vals(i); theta1_vals(j)];

J_vals(i,j) = computeCost(X, y, t);

end

end

% Because of the way meshgrids work in the surf command, we need to

% transpose J_vals before calling surf, or else the axes will be flipped

J_vals = J_vals';

% Surface plot

figure;

surf(theta0_vals, theta1_vals, J_vals)

xlabel('\theta_0'); ylabel('\theta_1');

% Contour plot

figure;

% Plot J_vals as 15 contours spaced logarithmically between 0.01 and 100

contour(theta0_vals, theta1_vals, J_vals, logspace(-2, 3, 20))

xlabel('\theta_0'); ylabel('\theta_1');

hold on;

plot(theta(1), theta(2), 'rx', 'MarkerSize', 10, 'LineWidth', 2);代码分步讲解

- step1: 绘制散点图,观察训练集的数据分布。

data = load('ex1data1.txt');

X = data(:, 1); y = data(:, 2);

m = length(y); % number of training examples

figure; % open a new figure window

plot(x,y,'rx','MarkerSize',10);

xlabel('Population of City in 10,000s');

ylabel('Profit in $10,000s');

- step2: Computing cost function J(θ)

X = [ones(m, 1), data(:,1)]; % Add a column of ones to x

theta = zeros(2, 1); % initialize fitting parameters

% Some gradient descent settings

iterations = 1500;

alpha = 0.01;

fprintf('\nTesting the cost function ...\n')

% compute and display initial cost

J = computeCost(X, y, theta);

fprintf('With theta = [0 ; 0]\nCost computed = %f\n', J);

fprintf('Expected cost value (approx) 32.07\n');

% further testing of the cost function

J = computeCost(X, y, [-1 ; 2]);

fprintf('\nWith theta = [-1 ; 2]\nCost computed = %f\n', J);

fprintf('Expected cost value (approx) 54.24\n');上面代码中的 computeCost(X, y, theta) 函数的代码如下:

function J = computeCost(X, y, theta)

%COMPUTECOST Compute cost for linear regression

% J = COMPUTECOST(X, y, theta) computes the cost of using theta as the

% parameter for linear regression to fit the data points in X and y

m = length(y); % number of training examples

J = 0;

h = X * theta;

for i=1:m,

J = J + (h(i)-y(i))^2;

end;

J = J/(2*m);

end- step3: 用 gradient descent 找到 J(θ) 的最优解 (θ0,θ1)

本例中即找出合适的 (θ0,θ1) ,使得 J(θ) 最小(或者说在允许的差值范围内)

fprintf('\nRunning Gradient Descent ...\n')

% run gradient descent

theta = gradientDescent(X, y, theta, alpha, iterations);

% print theta to screen

fprintf('Theta found by gradient descent:\n');

fprintf('%f\n', theta);上面代码中 gradientDescent(X, y, theta, alpha, iterations) 函数的代码如下:

function [theta, J_history] = gradientDescent(X, y, theta, alpha, num_iters)

%GRADIENTDESCENT Performs gradient descent to learn theta

% theta = GRADIENTDESCENT(X, y, theta, alpha, num_iters) updates theta by

% taking num_iters gradient steps with learning rate alpha

% Initialize some useful values

m = length(y); % number of training examples

J_history = zeros(num_iters, 1);

for iter = 1:num_iters,

theta = theta - X' * alpha / m * (X *theta - y);

% Save the cost J in every iteration

J_history(iter) = computeCost(X, y, theta);

end

end- step4: 绘制拟合出的线性回归模型 hθ(x)

% Plot the linear fit

hold on; % keep previous plot visible

plot(X(:,2), X*theta, '-')

legend('Training data', 'Linear regression')

hold off % don't overlay any more plots on this figure

- step5: 预测

预测分店开在人口为 35,000 and 70,000 城市的利润

predict1 = [1, 3.5] *theta;

fprintf('For population = 35,000, we predict a profit of %f\n',...

predict1*10000);

predict2 = [1, 7] * theta;

fprintf('For population = 70,000, we predict a profit of %f\n',...

predict2*10000);- (optional)step6: 绘制 J(θ) 。观察其在不同 (θ0,θ1) 下的值

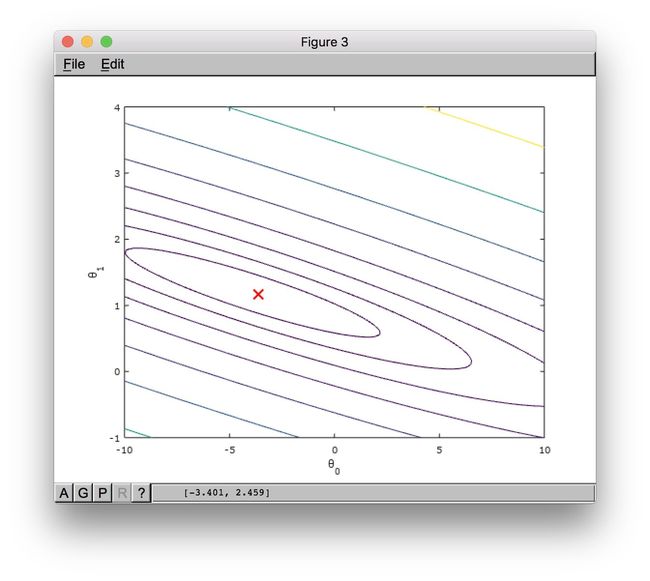

fprintf('Visualizing J(theta_0, theta_1) ...\n')

% Grid over which we will calculate J

theta0_vals = linspace(-10, 10, 100);

theta1_vals = linspace(-1, 4, 100);

% initialize J_vals to a matrix of 0's

J_vals = zeros(length(theta0_vals), length(theta1_vals));

% Fill out J_vals

for i = 1:length(theta0_vals)

for j = 1:length(theta1_vals)

t = [theta0_vals(i); theta1_vals(j)];

J_vals(i,j) = computeCost(X, y, t);

end

end

% Because of the way meshgrids work in the surf command, we need to

% transpose J_vals before calling surf, or else the axes will be flipped

J_vals = J_vals';

% Surface plot

figure;

surf(theta0_vals, theta1_vals, J_vals)

xlabel('\theta_0'); ylabel('\theta_1');

% Contour plot

figure;

% Plot J_vals as 15 contours spaced logarithmically between 0.01 and 100

contour(theta0_vals, theta1_vals, J_vals, logspace(-2, 3, 20))

xlabel('\theta_0'); ylabel('\theta_1');

hold on;

plot(theta(1), theta(2), 'rx', 'MarkerSize', 10, 'LineWidth', 2);

多元线性回归

建模

非向量形式写法

Hypothesis:

h_{\theta}(x)=\theta_0+\theta_1x+\theta_2x+\cdots+\theta_nx_n

\tag{2-1}\label{2-1}Cost Function:

J(\theta)=\frac{1}{2m}\sum_{i=1}^{m}(h_\theta(x^{(i)})-y^{(i)})^2

\tag{2-2}\label{2-2}Gradient Descent:

\theta_j:=\theta_j-\alpha\frac{\partial}{\partial\theta_j}J(\theta)

\quad for \, j=1..n

\tag{2-3}\label{2-3}

公式 (2-3) 即:

repeatuntilconvergence:{

}

⇔

repeatuntilconvergence:{

}

向量形式写法

- 公式 (2-1) 的向量形式:

\tag{2-1'}\label{2-1-1}

推导过程如下:

先看看当训练集只有一条记录时,向量形式如何表达,

当训练集有 m 条记录时,即可得到公式 (2-1') ,

令

- 公式 (2-2) 的向量形式:

\tag{2-2'}\label{2-2-1}

- 公式 (2-3) 的向量形式:

\tag{2-3'}\label{2-3-1}

推导过程如下:

⇒

另外, α 为 learning rate.

应用

该实例来源于 coursera machine learning programming exercise1.

已知:

- DataSet

数据集的部分内容如下,完整数据集在这里

| Size of the house (x1) | Number of bedrooms (x2) | Price of the house |

|---|---|---|

| 2104 | 3 | 399900 |

| 1600 | 3 | 329900 |

| 2400 | 3 | 369900 |

| 1416 | 2 | 232000 |

| … | … | … |

- 目的:

若房价与房子的面积,房间的数量有关,作为房东的你,想要预测手上已有房源的市场价。

完整代码

完整代码可在这里下载。

下面只列出其中的主程序:

%% Linear regression with multiple variables

%% Initialization

%% ================ Part 1: Feature Normalization ================

%% Clear and Close Figures

clear ; close all; clc

fprintf('Loading data ...\n');

%% Load Data

data = load('ex1data2.txt');

X = data(:, 1:2);

y = data(:, 3);

m = length(y);

% Print out some data points

fprintf('First 10 examples from the dataset: \n');

fprintf(' x = [%.0f %.0f], y = %.0f \n', [X(1:10,:) y(1:10,:)]');

fprintf('Program paused. Press enter to continue.\n');

pause;

% Scale features and set them to zero mean

fprintf('Normalizing Features ...\n');

[X mu sigma] = featureNormalize(X);

% Add intercept term to X

X = [ones(m, 1) X];

%% ================ Part 2: Gradient Descent ================

% ====================== YOUR CODE HERE ======================

% Instructions: We have provided you with the following starter

% code that runs gradient descent with a particular

% learning rate (alpha).

%

% Your task is to first make sure that your functions -

% computeCost and gradientDescent already work with

% this starter code and support multiple variables.

%

% After that, try running gradient descent with

% different values of alpha and see which one gives

% you the best result.

%

% Finally, you should complete the code at the end

% to predict the price of a 1650 sq-ft, 3 br house.

%

% Hint: By using the 'hold on' command, you can plot multiple

% graphs on the same figure.

%

% Hint: At prediction, make sure you do the same feature normalization.

%

fprintf('Running gradient descent ...\n');

% Choose some alpha value

alpha = 0.01;

num_iters = 400;

% Init Theta and Run Gradient Descent

theta = zeros(3, 1);

[theta, J_history] = gradientDescentMulti(X, y, theta, alpha, num_iters);

% Plot the convergence graph

figure;

plot(1:numel(J_history), J_history, '-b', 'LineWidth', 2);

xlabel('Number of iterations');

ylabel('Cost J');

% Display gradient descent's result

fprintf('Theta computed from gradient descent: \n');

fprintf(' %f \n', theta);

fprintf('\n');

% Estimate the price of a 1650 sq-ft, 3 br house

% ====================== YOUR CODE HERE ======================

% Recall that the first column of X is all-ones. Thus, it does

% not need to be normalized.

price = featureNormalize([1 1650 3]) * theta; % You should change this

% ============================================================

fprintf(['Predicted price of a 1650 sq-ft, 3 br house ' ...

'(using gradient descent):\n $%f\n'], price);

fprintf('Program paused. Press enter to continue.\n');

pause;

%% ================ Part 3: Normal Equations ================

fprintf('Solving with normal equations...\n');

% ====================== YOUR CODE HERE ======================

% Instructions: The following code computes the closed form

% solution for linear regression using the normal

% equations. You should complete the code in

% normalEqn.m

%

% After doing so, you should complete this code

% to predict the price of a 1650 sq-ft, 3 br house.

%

%% Load Data

data = csvread('ex1data2.txt');

X = data(:, 1:2);

y = data(:, 3);

m = length(y);

% Add intercept term to X

X = [ones(m, 1) X];

% Calculate the parameters from the normal equation

theta = normalEqn(X, y);

% Display normal equation's result

fprintf('Theta computed from the normal equations: \n');

fprintf(' %f \n', theta);

fprintf('\n');

% Estimate the price of a 1650 sq-ft, 3 br house

% ====================== YOUR CODE HERE ======================

price = [1 1650 3] * theta; % You should change this

% ============================================================

fprintf(['Predicted price of a 1650 sq-ft, 3 br house ' ...

'(using normal equations):\n $%f\n'], price);代码分步讲解

- step1: 特征的归一化处理 feature normalization

data = load('ex1data2.txt');

X = data(:, 1:2);

y = data(:, 3);

m = length(y);

% Scale features and set them to zero mean

fprintf('Normalizing Features ...\n');

[X mu sigma] = featureNormalize(X);

% Add intercept term to X

X = [ones(m, 1) X];代码中的 featureNormalize(X) 函数如下:

function [X_norm, mu, sigma] = featureNormalize(X)

%FEATURENORMALIZE Normalizes the features in X

% FEATURENORMALIZE(X) returns a normalized version of X where

% the mean value of each feature is 0 and the standard deviation

% is 1. This is often a good preprocessing step to do when

% working with learning algorithms.

% You need to set these values correctly

X_norm = X;

mu = zeros(1, size(X, 2));

sigma = zeros(1, size(X, 2));

% Instructions: First, for each feature dimension, compute the mean

% of the feature and subtract it from the dataset,

% storing the mean value in mu. Next, compute the

% standard deviation of each feature and divide

% each feature by it's standard deviation, storing

% the standard deviation in sigma.

%

% Note that X is a matrix where each column is a

% feature and each row is an example. You need

% to perform the normalization separately for

% each feature.

%

% Hint: You might find the 'mean' and 'std' functions useful.

%

mu = mean(X);

sigma = std(X);

for i = 1:size(X,1),

X_norm(i,:) = (X_norm(i,:)-mu) ./ sigma;

end;

end- step2: 用 gradient descent 找到 J(Θ) 的最优解 Θ

fprintf('Running gradient descent ...\n');

% Choose some alpha value

alpha = 0.01;

num_iters = 400;

% Init Theta and Run Gradient Descent

theta = zeros(3, 1);

[theta, J_history] = gradientDescentMulti(X, y, theta, alpha, num_iters);

% Display gradient descent's result

fprintf('Theta computed from gradient descent: \n');

fprintf(' %f \n', theta);

fprintf('\n');代码中的gradientDescentMulti(X, y, theta, alpha, num_iters)函数代码如下:

function [theta, J_history] = gradientDescentMulti(X, y, theta, alpha, num_iters)

%GRADIENTDESCENTMULTI Performs gradient descent to learn theta

% theta = GRADIENTDESCENTMULTI(x, y, theta, alpha, num_iters) updates theta by

% taking num_iters gradient steps with learning rate alpha

% Initialize some useful values

m = length(y); % number of training examples

J_history = zeros(num_iters, 1);

for iter = 1:num_iters,

theta = theta - X' * alpha / m * (X *theta - y);

% Save the cost J in every iteration

J_history(iter) = computeCostMulti(X, y, theta);

end

end代码中的computeCostMulti(X, y, theta)函数代码如下:

function J = computeCostMulti(X, y, theta)

%COMPUTECOSTMULTI Compute cost for linear regression with multiple variables

% J = COMPUTECOSTMULTI(X, y, theta) computes the cost of using theta as the

% parameter for linear regression to fit the data points in X and y

% Initialize some useful values

m = length(y); % number of training examples

% You need to return the following variables correctly

J = 0;

h = X * theta;

for i=1:m,

J = J + (h(i)-y(i))^2;

end;

J = J/(2*m);

end- step3: 绘制 J(Θ) 关于迭代次数的曲线图,以帮助选择合适的 learning rate α

% Plot the convergence graph

figure;

plot(1:numel(J_history), J_history, '-b', 'LineWidth', 2);

xlabel('Number of iterations');

ylabel('Cost J');

- step4: 预测

预测 size=1650(feet2),bedrooms=3 的房价。

% Estimate the price of a 1650 sq-ft, 3 br house

price = featureNormalize([1 1650 3]) * theta; %其中的 theta 在之前几步已经算出- (Optional)也可以使用 Normal Equation 代替 gradient descent 去寻找最优解

fprintf('Solving with normal equations...\n');

%% Load Data

data = csvread('ex1data2.txt');

X = data(:, 1:2);

y = data(:, 3);

m = length(y);

% Add intercept term to X

X = [ones(m, 1) X];

% Calculate the parameters from the normal equation

theta = normalEqn(X, y);

% Display normal equation's result

fprintf('Theta computed from the normal equations: \n');

fprintf(' %f \n', theta);

fprintf('\n');代码中的normalEqn(X, y)函数代码如下:

function [theta] = normalEqn(X, y)

%NORMALEQN Computes the closed-form solution to linear regression

% NORMALEQN(X,y) computes the closed-form solution to linear

% regression using the normal equations.

theta = zeros(size(X, 2), 1);

theta = pinv(X' * X) * X' * y;

endNote:

使用 normal equation,相比于 gradient descent 来说代码量更小。

| Gradient Descent | Normal Equation |

|---|---|

| need to choose learning rate ‘ α ’ | No need to choose learning rate ‘ α ’ |

| needs many iterations | No need to iterate |

| 时间复杂度 O(kn2) | 时间复杂度 O(n3) |

| works well when n is large(n = nums of features) | slow if n is very large |