运筹系列35:凸优化接口cvxpy

1. 凸优化问题

1.1 QP问题

目标函数二阶,约束一阶,称为Quadratic programming

1.2. QCQP

目标二阶,约束二阶,Quadratical Constraint Quadratic Programming。

1.3. SOCP

second order cone program,本质上还是一个QP问题(约束条件进行平方)。

1.4 DCP

一个问题能够由目标函数和一系列约束构造。如果问题遵从DCP规则,这个问题将是凸的,能够被cvxpy解决。DCP规则要求目标函数有以下两种形式:

Minimize(convex)

Maximize(concave)

在DCP规则下的有效约束为:

affine == affine

convex <= concave

concave >= convex

你能调用object.is_dcp()来检查一个问题、约束、目标函数是否满足DCP规则。

2. Cvxpy介绍

CVXPY是一种可以内置于Python中的模型编程语言,解决凸优化问题。它可以自动转化问题为标准形式,调用解法器,解包结果集。下面是个简单的例子:

from cvxpy import *

x = Variable()

y = Variable()

constraints = [x + y == 1,

x - y >= 1]

obj = Minimize(square(x - y))

prob = Problem(obj, constraints)

prob.solve()

print ("status:", prob.status)

print ("optimal value", prob.value)

print ("optimal var", x.value, y.value)

3. 其他求解器

在cvxpy默认的求解器不行时,我们要使用其他求解器,例如:

# Solving a problem with different solvers.

x = cvx.Variable(2)

obj = cvx.Minimize(x[0] + cvx.norm(x, 1))

constraints = [x >= 2]

prob = cvx.Problem(obj, constraints)

# Solve with ECOS.

prob.solve(solver=cvx.ECOS)

print("optimal value with ECOS:", prob.value)

# Solve with ECOS_BB.

prob.solve(solver=cvx.ECOS_BB)

print("optimal value with ECOS_BB:", prob.value)

# Solve with CVXOPT.

prob.solve(solver=cvx.CVXOPT)

print("optimal value with CVXOPT:", prob.value)

# Solve with SCS.

prob.solve(solver=cvx.SCS)

print("optimal value with SCS:", prob.value)

# Solve with GLPK.

prob.solve(solver=cvx.GLPK)

print("optimal value with GLPK:", prob.value)

# Solve with GLPK_MI.

prob.solve(solver=cvx.GLPK_MI)

print("optimal value with GLPK_MI:", prob.value)

# Solve with GUROBI.

prob.solve(solver=cvx.GUROBI)

print("optimal value with GUROBI:", prob.value)

# Solve with MOSEK.

prob.solve(solver=cvx.MOSEK)

print("optimal value with MOSEK:", prob.value)

# Solve with Elemental.

prob.solve(solver=cvx.ELEMENTAL)

print("optimal value with Elemental:", prob.value)

# Solve with CBC.

prob.solve(solver=cvx.CBC)

print("optimal value with CBC:", prob.value)

optimal value with ECOS: 5.99999999551

optimal value with ECOS_BB: 5.99999999551

optimal value with CVXOPT: 6.00000000512

optimal value with SCS: 6.00046055789

optimal value with GLPK: 6.0

optimal value with GLPK_MI: 6.0

optimal value with GUROBI: 6.0

optimal value with MOSEK: 6.0

optimal value with Elemental: 6.0000044085242727

optimal value with CBC: 6.0

//Use the installed_solvers utility function to get a list of the solvers your installation of CVXPY //supports.

print installed_solvers()

['CBC', 'CVXOPT', 'MOSEK', 'GLPK', 'GLPK_MI', 'ECOS_BB', 'ECOS', 'SCS'

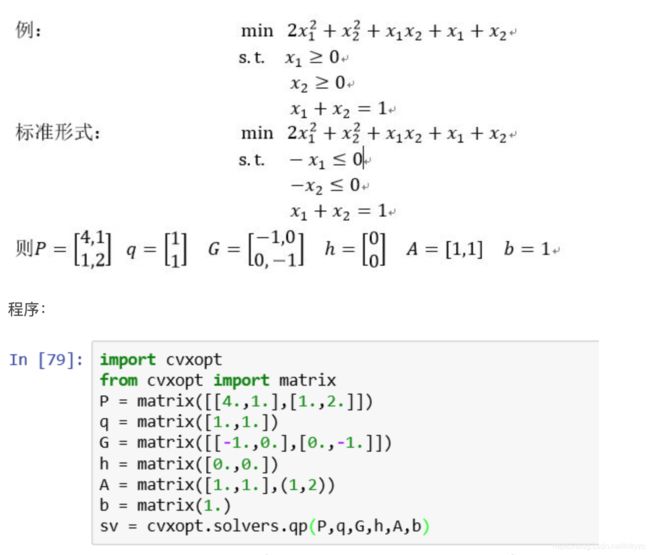

直接用cvxopt求解的例子如下:

4. DPP

DPP是Disciplined Parametrized Programming (DPP)的缩写,即保持同样形状的问题。DPP中有一种新的数据格式叫parameter,要求固定变量variable后,对于parameters是一阶的(parameter-affine)。在这种情况下,用ECOS、SCS、MOSEK时可以加速。

下面是个例子:

import cvxpy as cp

m, n = 3, 2

x = cp.Variable((n, 1))

F = cp.Parameter((m, n))

G = cp.Parameter((m, n))

g = cp.Parameter((m, 1))

gamma = cp.Parameter(nonneg=True)

objective = cp.norm((F + G) @ x - g) + gamma * cp.norm(x)

print(objective.is_dcp(dpp=True))

开启dpp=Ture后,就可以给parameter输入不同的参数,反复求解问题了,下图是resolving的时间。