熟悉 NumPy 常用函数

# 来源:NumPy Biginner's Guide 2e ch3

读写文件

import numpy as np

# eye 用于创建单位矩阵

i2 = np.eye(2)

print i2

'''

[[ 1. 0.]

[ 0. 1.]]

'''

# 将数组以纯文本保存到 eye.txt 中

np.savetxt("eye.txt", i2)

'''

eye.txt:

1.000000000000000000e+00 0.000000000000000000e+00

0.000000000000000000e+00 1.000000000000000000e+00

'''

# 还可以读进来

print np.loadtxt('eye.txt')

[[ 1. 0.]

[ 0. 1.]]

读取 CSV

'''

data.csv:

AAPL,28-01-2011, ,344.17,344.4,333.53,336.1,21144800

分别为:

名称,日期,空,开盘,最高,最低,收盘,成交量

'''

# delimiter 是分隔符,设置为 ','

# usecols 设置需要取的列,这里只选择了收盘和成交量

# unpack 设置为 True,返回的数组是以列为主

# 可以分别将收盘和成交量赋给 c 和 v

c, v = np.loadtxt('data.csv', delimiter=',', usecols=(6,7), unpack=True)

均值

import numpy as np

c, v = np.loadtxt('data.csv', delimiter=',', usecols=(6,7), unpack=True)

# 计算成交量加权均价

# average 用于计算均值

# weights 参数指定权重

vwap = np.average(c, weights=v)

print "VWAP =", vwap

# VWAP = 350.589549353

# mean 函数也能用于计算均值

print "mean =", np.mean(c)

# mean = 351.037666667

# 计算时间时间加权均价

t = np.arange(len(c))

print "twap =", np.average(c, weights=t)

# twap = 352.428321839

最大最小值

import numpy as np

# 这次读入了最高价和最低价

h, l = np.loadtxt('data.csv', delimiter=',', usecols=(4,5), unpack=True)

# 计算历史最高价和最低价

print "highest =", np.max(h)

# highest = 364.9

print "lowest =", np.min(l)

# lowest = 333.53

# ptp 函数用于计算极差

print "Spread high price", np.ptp(h)

# Spread high price 24.86

print "Spread low price", np.ptp(l)

# Spread low price 26.97

简单统计

import numpy as np

# 读入收盘价

c = np.loadtxt('data.csv', delimiter=',', usecols=(6,), unpack=True)

# 计算中位数

print "median =", np.median(c)

# median = 352.055

# 手动计算中位数

# 首先排个序

sorted_close = np.msort(c)

print "sorted =", sorted_close

# 然后取中间元素

N = len(c)

print "middle =", sorted[(N - 1)/2]

# middle = 351.99

# 由于我们的数组长度是偶数

# 中位数应该是中间两个数的均值

# print "average middle =", (sorted[N /2] + sorted[(N - 1) / 2]) / 2

# average middle = 352.055

# 方差

print "variance =", np.var(c)

# variance = 50.1265178889

# 手动计算方差

print "variance from definition =", np.mean((c - c.mean())**2)

# variance from definition = 50.1265178889

股票收益

import numpy as np

# 简单收益

# 当天收盘价减去前一天收盘价,再除以前一天收盘价

# returns = np.diff( arr ) / arr[ : -1]

# 我们计算一下标准差(方差的平方根)

print "Standard deviation =", np.std(returns)

# Standard deviation = 0.0129221344368

# 对数收益

# 当天收盘价的对数前前一天收盘价的对数

logreturns = np.diff( np.log(c) )

# 计算收益为正的下标

# where 将布尔索引变成位置索引

posretindices = np.where(returns > 0)

print "Indices with positive returns", posretindices

# Indices with positive returns (array([ 0, 1, 4, 5, 6, 7, 9, 10, 11, 12, 16, 17, 18, 19, 21, 22, 23, 25, 28]),)

# 年化波动

annual_volatility = np.std(logreturns)/np.mean(logreturns)

annual_volatility = annual_volatility / np.sqrt(1./252.)

print annual_volatility

# 月化波动

print "Monthly volatility", annual_volatility * np.sqrt(1./12.)

处理日期

import numpy as np

from datetime import datetime

# 将日期映射为星期

# Monday 0

# Tuesday 1

# Wednesday 2

# Thursday 3

# Friday 4

# Saturday 5

# Sunday 6

def datestr2num(s):

return datetime.strptime(s, "%d-%m-%Y").date().weekday()

# 读取星期和收盘价,converters 将日期映射成星期

dates, close = np.loadtxt('data.csv', delimiter=',', usecols=(1,6), converters={1: datestr2num}, unpack=True)

print "Dates =", dates

# Dates = [ 4. 0. 1. 2. 3. 4. 0. 1. 2. 3. 4. 0. 1. 2. 3. 4. 1. 2. 4. 0. 1. 2. 3. 4. 0. 1. 2. 3. 4.]

# 计算一周中每一天的均值

averages = np.zeros(5)

for i in range(5):

indices = np.where(dates == i)

prices = np.take(close, indices)

avg = np.mean(prices)

print "Day", i, "prices", prices, "Average", avg

averages[i] = avg

'''

Day 0 prices [[ 339.32 351.88 359.18 353.21 355.36]] Average 351.79

Day 1 prices [[ 345.03 355.2 359.9 338.61 349.31 355.76]] Average 350.635

Day 2 prices [[ 344.32 358.16 363.13 342.62 352.12 352.47]] Average 352.136666667

Day 3 prices [[ 343.44 354.54 358.3 342.88 359.56 346.67]] Average 350.898333333

Day 4 prices [[ 336.1 346.5 356.85 350.56 348.16 360. 351.99]] Average 350.022857143

'''

# 计算星期几最高,星期几最低

top = np.max(averages)

print "Highest average", top

# Highest average 352.136666667

print "Top day of the week", np.argmax(averages)

# Top day of the week 2

bottom = np.min(averages)

print "Lowest average", bottom

# Lowest average 350.022857143

print "Bottom day of the week", np.argmin(averages

# Bottom day of the week 4

真实波动幅度均值(ATR)

# 真实波动幅度(TR)定义为以下三个度量的最大值

# 1. 当天最高价减当天最低价

# 2. 当天最高价减前一天的收盘价的绝对值

# 3. 前一天收盘价减当天最低价的绝对值

import numpy as np

import sys

# 读入最高价、最低价、收盘价

h, l, c = np.loadtxt('data.csv', delimiter=',', usecols=(4, 5, 6), unpack=True)

# 读入数据数量

N = int(sys.argv[1])

# 获取最近 N 天的最高价和最低价

h = h[-N:]

l = l[-N:]

print "len(h)", len(h), "len(l)", len(l)

print "Close", c

# 由于需要前一天的收盘价,所以往天移动一天

previousclose = c[-N -1: -1]

print "len(previousclose)", len(previousclose)

print "Previous close", previousclose

# maximum 逐元素获得最大值

truerange = np.maximum(h - l, h - previousclose, previousclose - l)

print "True range", truerange

# 计算 ATR

atr = np.zeros(N)

# 第一个 ATR 通过均值来计算

atr[0] = np.mean(truerange)

# 计算之后每一个 ATR

# atr[i] = ((N - 1) * atr[i - 1] + tr[i]) / N

for i in range(1, N):

atr[i] = (N - 1) * atr[i - 1] + truerange[i]

atr[i] /= N

print "ATR", atr

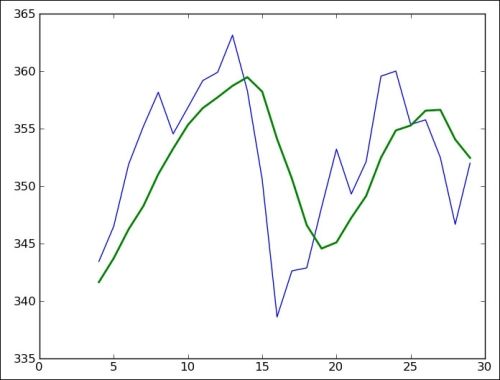

简单滑动均值

# 每一天的简单滑动均值

# 就是当天与前 (N - 1) 天的均值

# 其中 N 是窗口大小

import numpy as np

import sys

from matplotlib.pyplot import plot

from matplotlib.pyplot import show

N = int(sys.argv[1])

# 使用 ones 函数创建大小为 N 的数组

# 并除以 N 来创建权重

weights = np.ones(N) / N

print "Weights", weights

# 假设 N 为 5:

# Weights [ 0.2 0.2 0.2 0.2 0.2]

# 读入收盘价

c = np.loadtxt('data.csv', delimiter=',', usecols=(6,), unpack=True)

# 调用 convolve 函数来计算滑动平均

sma = np.convolve(weights, c)[N-1:-N+1]

# 绘制函数图像

# 要注意横轴从 (N - 1) 开始

t = np.arange(N - 1, len(c))

plot(t, c[N-1:], lw=1.0)

plot(t, sma, lw=2.0)

show()

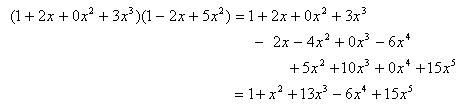

注:

np.convolve计算离散卷积,定义为:

离散卷积其实就是系数数组的多项式乘法。例如计算[1, 2, 0, 3]和[1, -2, 5]的卷积:

结果为[1, 1, 13, -6, 15]。

指数滑动均值

import numpy as np

import sys

from matplotlib.pyplot import plot

from matplotlib.pyplot import show

x = np.arange(5)

# exp 计算 e 的 x 次方

print "Exp", np.exp(x)

# Exp [ 1. 2.71828183 7.3890561 20.08553692 54.59815003]

# linspace 使用起始值、终止值和数量,返回等间隔的数组

print "Linspace", np.linspace(-1, 0, 5)

# Linspace [-1. -0.75 -0.5 -0.25 0. ]

N = int(sys.argv[1])

# 计算权重

weights = np.exp(np.linspace(-1., 0., N))

weights /= weights.sum()

print "Weights", weights

# 假设 N 为 5:

# Weights [ 0.11405072 0.14644403 0.18803785 0.24144538 0.31002201]

# 读入收盘价

c = np.loadtxt('data.csv', delimiter=',', usecols=(6,), unpack=True)

# 使用 convolve 计算指数滑动均值

ema = np.convolve(weights, c)[N-1:-N+1]

# 绘制函数图像

t = np.arange(N - 1, len(c))

plot(t, c[N-1:], lw=1.0)

plot(t, ema, lw=2.0)

show()

布林带

import numpy as np

import sys

from matplotlib.pyplot import plot

from matplotlib.pyplot import show

# 读取窗口大小

N = int(sys.argv[1])

# 这是简单滑动平均的权重

weights = np.ones(N) / N

print "Weights", weights

# 读取收盘价

c = np.loadtxt('data.csv', delimiter=',', usecols=(6,), unpack=True)

# 计算简单滑动平均

sma = np.convolve(weights, c)[N-1:-N+1]

# 手动计算滑动标准差

deviation = []

C = len(c)

for i in range(N - 1, C):

# 对于每一天

# 滑动标准差是当天与前 (N - 1) 天的标准差

# 和滑动均值类似,原书这里有误

dev = c[i - (N - 1): i + 1]

averages = np.zeros(N)

# 这里的 fill 将数组元素全部变为指定值

# 相当于 averages.flat = sma[i - (N - 1)]

# 但是比它快

averages.fill(sma[i - (N - 1)])

# 也可以直接写 dev -= sma[i - (N - 1)]

dev = dev - averages

dev = dev ** 2

dev = np.sqrt(np.mean(dev))

deviation.append(dev)

deviation = 2 * np.array(deviation)

print len(deviation), len(sma)

# 上布林带是简单滑动均值加上两倍滑动标准差

# 下布林带是简单滑动均值减去两倍滑动标准差

upperBB = sma + deviation

lowerBB = sma - deviation

c_slice = c[N-1:]

between_bands = np.where((c_slice < upperBB) & (c_slice > lowerBB))

print lowerBB[between_bands]

print c[between_bands]

print upperBB[between_bands]

between_bands = len(np.ravel(between_bands))

print "Ratio between bands", float(between_bands)/len(c_slice)

# 绘制收盘价、简单滑动均值

# 上布林带和下布林带的图像

# 要注意横轴从 N - 1 开始

t = np.arange(N - 1, C)

plot(t, c_slice, lw=1.0)

plot(t, sma, lw=2.0)

plot(t, upperBB, lw=3.0)

plot(t, lowerBB, lw=4.0)

show()

使用线性模型预测收盘价

import numpy as np

import sys

N = int(sys.argv[1])

# 读入收盘价

c = np.loadtxt('data.csv', delimiter=',', usecols=(6,), unpack=True)

# 取后 N 天的收盘价,并倒序

b = c[-N:]

bbx = b[::-1]

print "bbx", bbx

# bbx [ 351.99 346.67 352.47 355.76 355.36]

# 构建 NxN 的二维数组

A = np.zeros((N, N), float)

print "Zeros N by N", A

'''

A = np.zeros((N, N), float)

print "Zeros N by N", A

Zeros N by N [[ 0. 0. 0. 0. 0.]

[ 0. 0. 0. 0. 0.]

[ 0. 0. 0. 0. 0.]

[ 0. 0. 0. 0. 0.]

[ 0. 0. 0. 0. 0.]]

'''

# A[i] 是倒数第 i 天的前 N 天的收盘价

for i in range(N):

A[i, ] = c[-N - 1 - i: - 1 - i]

print "A", A

'''

A [[ 360. 355.36 355.76 352.47 346.67]

[ 359.56 360. 355.36 355.76 352.47]

[ 352.12 359.56 360. 355.36 355.76]

[ 349.31 352.12 359.56 360. 355.36]

[ 353.21 349.31 352.12 359.56 360. ]]

'''

# 根据每一天前 N 天收盘价来预测当天收盘价

# np.linalg.lstsq 是最小二乘法的多元线性回归

# A 是输入属性的数据集,行是记录,列是属性

# b 是输出属性的数组

# x 是系数数组,x = (A^T A)^(-1) A^T b

(x, residuals, rank, s) = np.linalg.lstsq(A, b)

print x, residuals, rank, s

# [ 0.78111069 -1.44411737 1.63563225 -0.89905126 0.92009049] [] 5 [ 1.77736601e+03 1.49622969e+01 8.75528492e+00 5.15099261e+00 1.75199608e+00]

# 通过后 N 天收盘价来预测下一天的收盘价

print np.dot(b, x)

# 357.939161015

剪切和压缩数组

import numpy as np

a = np.arange(5)

print "a =", a

# a = [0 1 2 3 4]

# clip 用于剪切数组

# 小于最小值的元素会替换成最小值

# 大于最大值的元素会替换成最大值

print "Clipped", a.clip(1, 2)

# Clipped [1 1 2 2 2]

a = np.arange(4)

print a

# [0 1 2 3]

# compress 用于过滤元素

# 等价于 a[a > 2]

print "Compressed", a.compress(a > 2)

# Compressed [3]

计算阶乘

import numpy as np

b = np.arange(1, 9)

print "b =", b

# b = [1 2 3 4 5 6 7 8]

# prod 用于求出各元素乘积

print "Factorial", b.prod()

# Factorial 40320

# cumprod 求出累积连乘

# P[i] = a[0] * ... * a[i]

print "Factorials", b.cumprod()

# Factorials [ 1 2 6 24 120 720 5040 40320]