量化投资 — 配对交易策略 (Pair Trading)

配对交易策略 Pair Trading

0. 引库

import pandas as pd

import numpy as np

import tushare as ts

import seaborn

from matplotlib import pyplot as plt

plt.style.use('seaborn')

%matplotlib inline

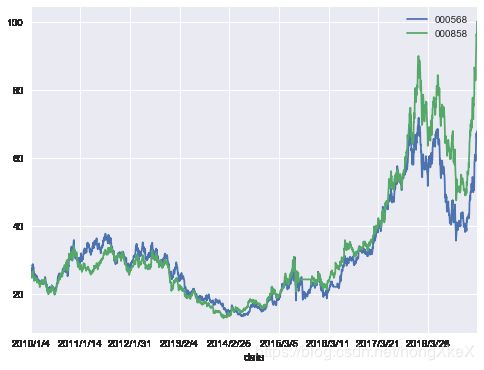

data = pd.read_csv('pair-trade-data.csv')

data.set_index('date',inplace = True)

data.head()

| 000568 | 000858 | |

|---|---|---|

| date | ||

| 2010/1/4 | 27.488118 | 26.117536 |

| 2010/1/5 | 27.335123 | 26.391583 |

| 2010/1/6 | 26.941707 | 25.694008 |

| 2010/1/7 | 26.388011 | 24.913389 |

| 2010/1/8 | 26.825140 | 24.863562 |

data.plot(figsize=(8, 6));

2. 策略开发思路

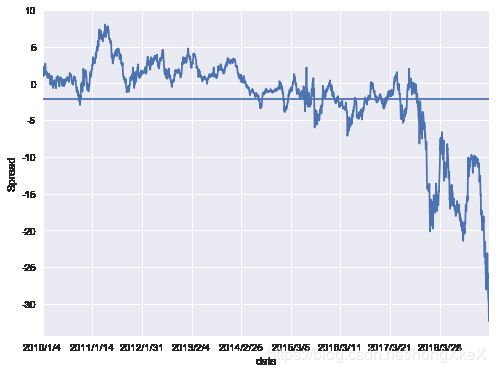

# 价差是回归的(不科学想法)

data['priceDelta'] = data['000568'] - data['000858']

data.head()

| 000568 | 000858 | priceDelta | |

|---|---|---|---|

| date | |||

| 2010/1/4 | 27.488118 | 26.117536 | 1.370582 |

| 2010/1/5 | 27.335123 | 26.391583 | 0.943540 |

| 2010/1/6 | 26.941707 | 25.694008 | 1.247699 |

| 2010/1/7 | 26.388011 | 24.913389 | 1.474622 |

| 2010/1/8 | 26.825140 | 24.863562 | 1.961578 |

# 图示价差及其均值

data['priceDelta'].plot(figsize=(8, 6));

plt.ylabel('Spread')

plt.axhline(data['priceDelta'].mean());

# 对价差进行标准化

data['zscore'] = (data['priceDelta'] - np.mean(data['priceDelta']))/np.std(data['priceDelta'])

data.head()

| 000568 | 000858 | priceDelta | zscore | |

|---|---|---|---|---|

| date | ||||

| 2010/1/4 | 27.488118 | 26.117536 | 1.370582 | 0.569895 |

| 2010/1/5 | 27.335123 | 26.391583 | 0.943540 | 0.500520 |

| 2010/1/6 | 26.941707 | 25.694008 | 1.247699 | 0.549932 |

| 2010/1/7 | 26.388011 | 24.913389 | 1.474622 | 0.586796 |

| 2010/1/8 | 26.825140 | 24.863562 | 1.961578 | 0.665903 |

len(data[data['zscore'] > 1.5])

17

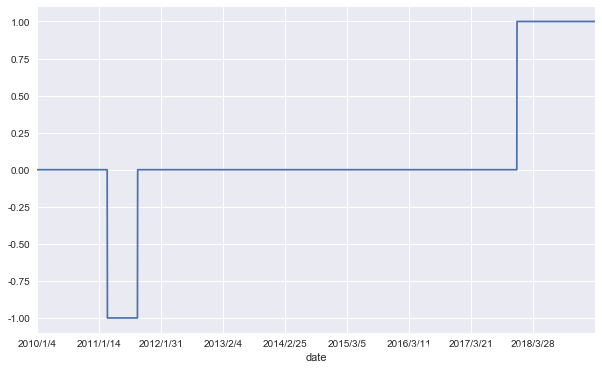

# 'position_1'是000568开平仓信号

data['position_1'] = np.where(data['zscore'] > 1.5, -1, np.nan)

data['position_1'] = np.where(data['zscore'] < -1.5, 1, data['position_1'])

data['position_1'] = np.where(abs(data['zscore']) < 0.5, 0, data['position_1'])

data.head()

| 000568 | 000858 | priceDelta | zscore | position_1 | |

|---|---|---|---|---|---|

| date | |||||

| 2010/1/4 | 27.488118 | 26.117536 | 1.370582 | 0.569895 | NaN |

| 2010/1/5 | 27.335123 | 26.391583 | 0.943540 | 0.500520 | NaN |

| 2010/1/6 | 26.941707 | 25.694008 | 1.247699 | 0.549932 | NaN |

| 2010/1/7 | 26.388011 | 24.913389 | 1.474622 | 0.586796 | NaN |

| 2010/1/8 | 26.825140 | 24.863562 | 1.961578 | 0.665903 | NaN |

产生交易信号

data['position_1'] = data['position_1'].ffill().fillna(0)

data['position_1'].plot(ylim=[-1.1, 1.1], figsize=(10, 6));

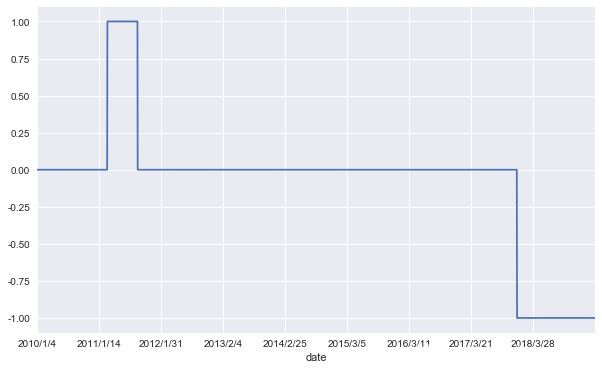

# 'position_2'是000858开平仓信号(与000568符号相反)

data['position_2'] = -np.sign(data['position_1'])

data['position_2'].plot(ylim=[-1.1, 1.1], figsize=(10, 6));

3. 计算策略年化收益并可视化

data['returns_1'] = (np.log(data['000568'] / data['000568'].shift(1))).fillna(0)

data['returns_2'] = (np.log(data['000858'] / data['000858'].shift(1))).fillna(0)

data.head(10)

| 000568 | 000858 | priceDelta | zscore | position_1 | position_2 | returns_1 | returns_2 | |

|---|---|---|---|---|---|---|---|---|

| date | ||||||||

| 2010/1/4 | 27.488118 | 26.117536 | 1.370582 | 0.569895 | 0.0 | -0.0 | 0.000000 | 0.000000 |

| 2010/1/5 | 27.335123 | 26.391583 | 0.943540 | 0.500520 | 0.0 | -0.0 | -0.005581 | 0.010438 |

| 2010/1/6 | 26.941707 | 25.694008 | 1.247699 | 0.549932 | 0.0 | -0.0 | -0.014497 | -0.026787 |

| 2010/1/7 | 26.388011 | 24.913389 | 1.474622 | 0.586796 | 0.0 | -0.0 | -0.020766 | -0.030852 |

| 2010/1/8 | 26.825140 | 24.863562 | 1.961578 | 0.665903 | 0.0 | -0.0 | 0.016430 | -0.002002 |

| 2010/1/11 | 25.936311 | 24.631037 | 1.305274 | 0.559285 | 0.0 | -0.0 | -0.033696 | -0.009396 |

| 2010/1/12 | 26.409867 | 25.336916 | 1.072951 | 0.521543 | 0.0 | -0.0 | 0.018094 | 0.028255 |

| 2010/1/13 | 26.577433 | 25.137609 | 1.439824 | 0.581143 | 0.0 | -0.0 | 0.006325 | -0.007897 |

| 2010/1/14 | 28.420660 | 26.109231 | 2.311428 | 0.722738 | 0.0 | -0.0 | 0.067054 | 0.037924 |

| 2010/1/15 | 28.253094 | 26.208885 | 2.044209 | 0.679327 | 0.0 | -0.0 | -0.005913 | 0.003810 |

data['strategy'] = 0.5*(data['position_1'].shift(1) * data['returns_1']) + 0.5*(data['position_2'].shift(1) * data['returns_2'])

# 计算累积收益率

data[['returns_1','returns_2','strategy']].dropna().cumsum().apply(np.exp).tail(1)

| returns_1 | returns_2 | strategy | |

|---|---|---|---|

| date | |||

| 2019/4/8 | 2.470158 | 3.837651 | 0.986754 |

# 可视化累积收益率

data[['returns_1','returns_2','strategy']].dropna().cumsum().apply(np.exp).plot(figsize=(10, 6));

Pair trading 策略 - 小范围时间(2013.6-2014.12)

data2 = pd.read_csv('pair-trade-data2.csv')

data2.set_index('date',inplace = True)

data2.head()

| 000568 | 000858 | |

|---|---|---|

| date | ||

| 2013/6/3 | 20.719056 | 20.343053 |

| 2013/6/4 | 20.357220 | 20.060867 |

| 2013/6/5 | 20.514540 | 20.274644 |

| 2013/6/6 | 20.113374 | 20.172031 |

| 2013/6/7 | 19.704342 | 19.667508 |

data2.plot(figsize=(8, 6));

# 价差是回归的(不科学想法)

data2['priceDelta'] = data['000568'] - data['000858']

data2.head()

| 000568 | 000858 | priceDelta | |

|---|---|---|---|

| date | |||

| 2013/6/3 | 20.719056 | 20.343053 | 0.376004 |

| 2013/6/4 | 20.357220 | 20.060867 | 0.296353 |

| 2013/6/5 | 20.514540 | 20.274644 | 0.239896 |

| 2013/6/6 | 20.113374 | 20.172031 | -0.058657 |

| 2013/6/7 | 19.704342 | 19.667508 | 0.036833 |

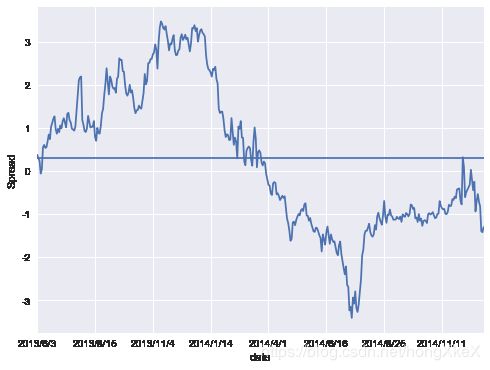

# 图示价差及其均值

data2['priceDelta'].plot(figsize=(8, 6));

plt.ylabel('Spread')

plt.axhline(data2['priceDelta'].mean());

# 对价差进行标准化

data2['zscore'] = (data2['priceDelta'] - np.mean(data2['priceDelta']))/np.std(data2['priceDelta'])

data2.head()

| 000568 | 000858 | priceDelta | zscore | |

|---|---|---|---|---|

| date | ||||

| 2013/6/3 | 20.719056 | 20.343053 | 0.376004 | 0.048513 |

| 2013/6/4 | 20.357220 | 20.060867 | 0.296353 | 0.000596 |

| 2013/6/5 | 20.514540 | 20.274644 | 0.239896 | -0.033369 |

| 2013/6/6 | 20.113374 | 20.172031 | -0.058657 | -0.212979 |

| 2013/6/7 | 19.704342 | 19.667508 | 0.036833 | -0.155532 |

len(data2[data2['zscore'] > 1.5])

40

len(data2[data2['zscore'] < -1.5])

16

# 'position_1'是000568开平仓信号

data2['position_1'] = np.where(data2['zscore'] > 1.5, -1, np.nan)

data2['position_1'] = np.where(data2['zscore'] < -1.5, 1, data2['position_1'])

data2['position_1'] = np.where(abs(data2['zscore']) < 0.5, 0, data2['position_1'])

data2.head()

| 000568 | 000858 | priceDelta | zscore | position_1 | |

|---|---|---|---|---|---|

| date | |||||

| 2013/6/3 | 20.719056 | 20.343053 | 0.376004 | 0.048513 | 0.0 |

| 2013/6/4 | 20.357220 | 20.060867 | 0.296353 | 0.000596 | 0.0 |

| 2013/6/5 | 20.514540 | 20.274644 | 0.239896 | -0.033369 | 0.0 |

| 2013/6/6 | 20.113374 | 20.172031 | -0.058657 | -0.212979 | 0.0 |

| 2013/6/7 | 19.704342 | 19.667508 | 0.036833 | -0.155532 | 0.0 |

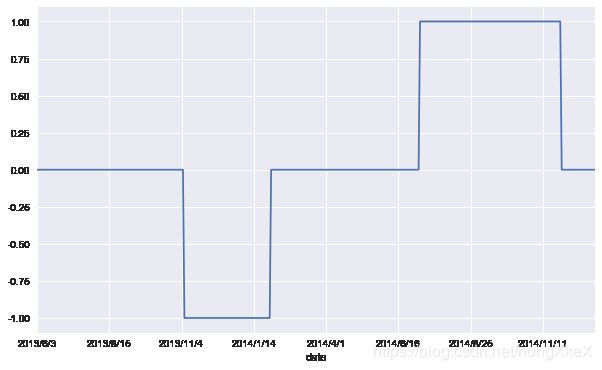

data2['position_1'] = data2['position_1'].ffill().fillna(0)

data2['position_1'].plot(ylim=[-1.1, 1.1], figsize=(10, 6));

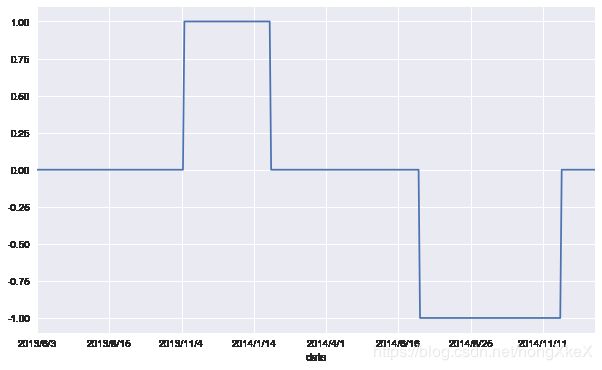

# 'position_2'是000858开平仓信号(与000568符号相反)

data2['position_2'] = -np.sign(data2['position_1'])

data2['position_2'].plot(ylim=[-1.1, 1.1], figsize=(10, 6));

data2['returns_1'] = (np.log(data2['000568'] / data2['000568'].shift(1))).fillna(0)

data2['returns_2'] = (np.log(data2['000858'] / data2['000858'].shift(1))).fillna(0)

data2.head(10)

| 000568 | 000858 | priceDelta | zscore | position_1 | position_2 | returns_1 | returns_2 | |

|---|---|---|---|---|---|---|---|---|

| date | ||||||||

| 2013/6/3 | 20.719056 | 20.343053 | 0.376004 | 0.048513 | 0.0 | -0.0 | 0.000000 | 0.000000 |

| 2013/6/4 | 20.357220 | 20.060867 | 0.296353 | 0.000596 | 0.0 | -0.0 | -0.017618 | -0.013968 |

| 2013/6/5 | 20.514540 | 20.274644 | 0.239896 | -0.033369 | 0.0 | -0.0 | 0.007698 | 0.010600 |

| 2013/6/6 | 20.113374 | 20.172031 | -0.058657 | -0.212979 | 0.0 | -0.0 | -0.019749 | -0.005074 |

| 2013/6/7 | 19.704342 | 19.667508 | 0.036833 | -0.155532 | 0.0 | -0.0 | -0.020546 | -0.025329 |

| 2013/6/13 | 19.562754 | 19.012515 | 0.550239 | 0.153334 | 0.0 | -0.0 | -0.007212 | -0.033871 |

| 2013/6/14 | 19.617816 | 19.012515 | 0.605301 | 0.186459 | 0.0 | -0.0 | 0.002811 | 0.000000 |

| 2013/6/17 | 19.255979 | 18.720423 | 0.535556 | 0.144501 | 0.0 | -0.0 | -0.018616 | -0.015482 |

| 2013/6/18 | 19.405434 | 18.853192 | 0.552241 | 0.154539 | 0.0 | -0.0 | 0.007731 | 0.007067 |

| 2013/6/19 | 19.956054 | 19.269202 | 0.686852 | 0.235521 | 0.0 | -0.0 | 0.027979 | 0.021826 |

data2['strategy'] = 0.5*(data2['position_1'].shift(1) * data2['returns_1']) + 0.5*(data2['position_2'].shift(1) * data2['returns_2'])

# 计算累积收益率

data2[['returns_1','returns_2','strategy']].dropna().cumsum().apply(np.exp).tail(1)

| returns_1 | returns_2 | strategy | |

|---|---|---|---|

| date | |||

| 2014/12/31 | 0.892955 | 0.97347 | 1.12623 |

# 可视化累积收益率

data2[['returns_1','returns_2','strategy']].dropna().cumsum().apply(np.exp).plot(figsize=(10, 6));

# 计算年化收益率

data2[['returns_1','returns_2','strategy']].dropna().mean() * 252

returns_1 -0.073915

returns_2 -0.017554

strategy 0.077608

dtype: float64

# 计算年化风险

data2[['returns_1','returns_2','strategy']].dropna().std() * 252 ** 0.5

returns_1 0.300306

returns_2 0.280425

strategy 0.057016

dtype: float64

# 策略累积收益率

data2['cumret'] = data2['strategy'].dropna().cumsum().apply(np.exp)

# 策略累积最大值

data2['cummax'] = data2['cumret'].cummax()

# 算回撤序列

drawdown = (data2['cummax'] - data2['cumret'])

# 算最大回撤

drawdown.max()

0.03645280148896235

Pair trading 策略 - 考虑时间序列平稳性

import pandas as pd

import numpy as np

import tushare as ts

import seaborn

from matplotlib import pyplot as plt

plt.style.use('seaborn')

%matplotlib inline

1. 数据准备

data3 = pd.read_csv('pair-trade-data2.csv')

data3.set_index('date',inplace = True)

data3.head()

| 000568 | 000858 | |

|---|---|---|

| date | ||

| 2013/6/3 | 20.719056 | 20.343053 |

| 2013/6/4 | 20.357220 | 20.060867 |

| 2013/6/5 | 20.514540 | 20.274644 |

| 2013/6/6 | 20.113374 | 20.172031 |

| 2013/6/7 | 19.704342 | 19.667508 |

data3.plot(figsize=(8,6));

2. 策略开发思路

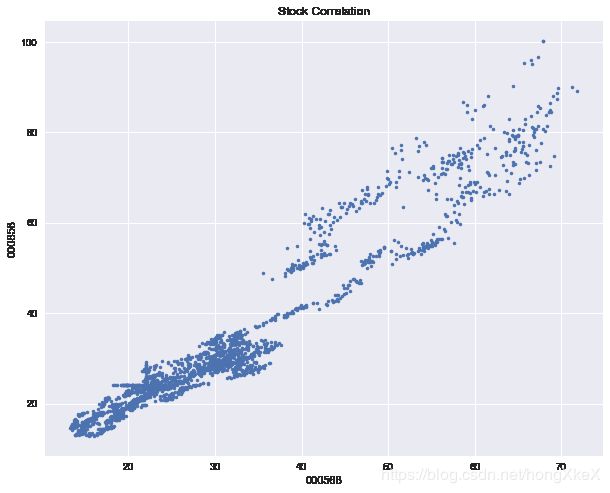

data3.corr() # 协方差矩阵

| 000568 | 000858 | |

|---|---|---|

| 000568 | 1.000000 | 0.552409 |

| 000858 | 0.552409 | 1.000000 |

# 可视化看相关关系

plt.figure(figsize =(10,8))

plt.title('Stock Correlation')

plt.plot(data['000568'], data['000858'], '.');

plt.xlabel('000568')

plt.ylabel('000858')

data.dropna(inplace = True)

# 对两股票价格做线性回归(白噪声项符合正态分布)

[slope, intercept] = np.polyfit(data3.iloc[:,0], data3.iloc[:,1], 1).round(2)

slope,intercept

(0.51, 7.82)

data3['spread'] = data3.iloc[:,1] - (data3.iloc[:,0]*slope + intercept)

data3.head()

| 000568 | 000858 | spread | |

|---|---|---|---|

| date | |||

| 2013/6/3 | 20.719056 | 20.343053 | 1.956334 |

| 2013/6/4 | 20.357220 | 20.060867 | 1.858684 |

| 2013/6/5 | 20.514540 | 20.274644 | 1.992228 |

| 2013/6/6 | 20.113374 | 20.172031 | 2.094210 |

| 2013/6/7 | 19.704342 | 19.667508 | 1.798294 |

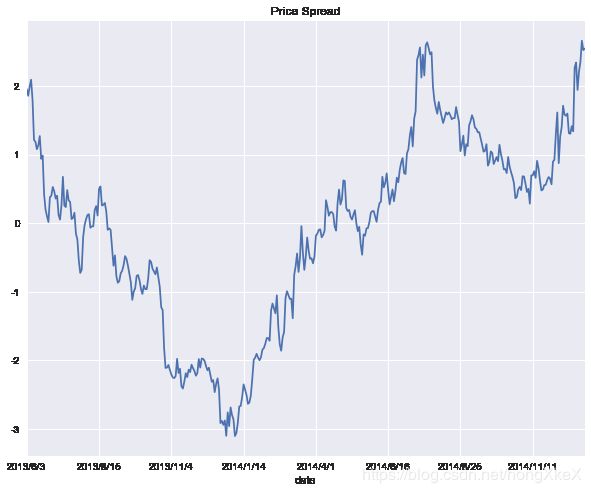

data3['spread'].plot(figsize = (10,8),title = 'Price Spread');

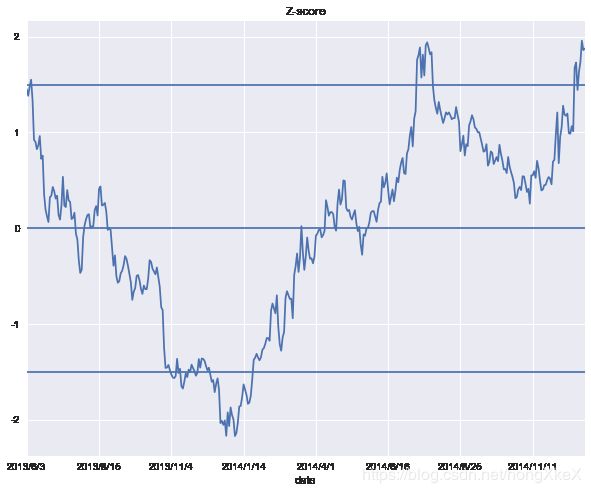

data3['zscore'] = (data3['spread'] - data3['spread'].mean())/data3['spread'].std()

data3.head()

| 000568 | 000858 | spread | zscore | |

|---|---|---|---|---|

| date | ||||

| 2013/6/3 | 20.719056 | 20.343053 | 1.956334 | 1.452385 |

| 2013/6/4 | 20.357220 | 20.060867 | 1.858684 | 1.382488 |

| 2013/6/5 | 20.514540 | 20.274644 | 1.992228 | 1.478078 |

| 2013/6/6 | 20.113374 | 20.172031 | 2.094210 | 1.551075 |

| 2013/6/7 | 19.704342 | 19.667508 | 1.798294 | 1.339261 |

data3['zscore'].plot(figsize = (10,8),title = 'Z-score')

plt.axhline(1.5)

plt.axhline(0)

plt.axhline(-1.5)

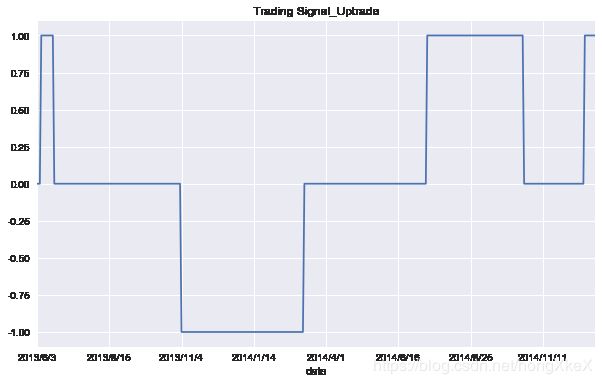

产生交易信号

data3['position_1'] = np.where(data3['zscore'] > 1.5, 1, np.nan)

data3['position_1'] = np.where(data3['zscore'] < -1.5, -1, data3['position_1'])

data3['position_1'] = np.where(abs(data3['zscore']) < 0.5, 0, data3['position_1'])

data3['position_1'] = data3['position_1'].ffill().fillna(0)

data3['position_1'].plot(ylim=[-1.1, 1.1], figsize=(10, 6),title = 'Trading Signal_Uptrade');

data3['position_2'] = -np.sign(data3['position_1'])

data3['position_2'].plot(ylim=[-1.1, 1.1], figsize=(10, 6),title = 'Trading Signal_Downtrade');

3. 计算策略年化收益并可视化

data3['returns_1'] = np.log(data3['000568'] / data3['000568'].shift(1))

data3['returns_2'] = np.log(data3['000858'] / data3['000858'].shift(1))

data3['strategy'] = 0.5*(data3['position_1'].shift(1) * data3['returns_1']) + 0.5*(data3['position_2'].shift(1) * data3['returns_2'])

# 计算累积收益率

data3[['returns_1','returns_2','strategy']].dropna().cumsum().apply(np.exp).tail(1)

| returns_1 | returns_2 | strategy | |

|---|---|---|---|

| date | |||

| 2014/12/31 | 0.892955 | 0.97347 | 1.174494 |

data3[['returns_1','returns_2','strategy']].dropna().cumsum().apply(np.exp).plot(figsize=(10, 8),title = 'Strategy_Backtesting');

# 计算年化收益率

data3[['returns_1','returns_2','strategy']].dropna().mean() * 252

returns_1 -0.073915

returns_2 -0.017554

strategy 0.105002

dtype: float64

# 计算年化风险

data3[['returns_1','returns_2','strategy']].dropna().std() * 252 ** 0.5

returns_1 0.300306

returns_2 0.280425

strategy 0.068639

dtype: float64

# 策略累积收益率

data3['cumret'] = data3['strategy'].dropna().cumsum().apply(np.exp)

# 策略累积最大值

data3['cummax'] = data3['cumret'].cummax()

# 算回撤序列

drawdown = (data3['cummax'] - data3['cumret'])

# 算最大回撤

drawdown.max()

0.038159777097367176

策略的思考

- 对多只ETF进行配对交易,是很多实盘量化基金的交易策略;

策略的风险和问题:

-

Spread不回归的风险,当市场结构发生重大改变时,用过去历史回归出来的Spread会发生不回归的重大风险;

-

中国市场做空受到限制,策略中有部分做空的收益是无法获得的;

-

回归系数需要Rebalancing;

-

策略没有考虑交易成本和其他成本;