文章目录

- 一、Pandas介绍:

- 1. Pandas介绍:

- 2.为什么要使用Pandas:

- 3. DataFrame:

- 4.DataFrame

- 4.1 DataFrame结构

- 4.2 DatatFrame的属性

- 4.3 DatatFrame的常用方法:

- 4.3 DatatFrame索引的设置

- 4.4 MultiIndex与Panel

- 4.5 series对象:

- 二、pandas的基本操作:

- 1. 读取数据:

- 1.1 索引操作

- 1.直接使用行列索引:(先列后行)

- 2.先列后行的索引方式

- 1.2 赋值操作:

- 1.3 排序操作:

- 1. df.sort_index():

- 2. df.sort_values()

- 三、DataFrame运算:

- 1. 算术运算

- 2. 逻辑运算:

- 2.1 条件判断:

- 2.2 布尔索引

- 2.3 布尔赋值

- 2.4 逻辑运算函数:

- 3.统计运算:

- 3.1describe()

- 3.2 统计函数

- 3.4 累计统计函数

- 3.5 自定义运算

- 四、panads画图:

- 1.pandas.DataFrame.plot

- 2 pandas.Series.plot

- 五、文件读取与存储:

- 1.CSV

- 1.1 读取csv文件-read_csv

- 1.2 写入csv文件-to_csv

- 1.3 读取远程的csv

- 2.HDF5

- 3.Excel文件的读取:

- 3.1 excel文件的读取:

- 4.json数据的读取:

- 4.1 read_json

- 4.2 to_json

一、Pandas介绍:

1. Pandas介绍:

- 2008年WesMcKinney开发出的库

- 专门用于数据挖掘的开源python库

- 以Numpy为基础,借力Numpy模块在计算方面性能高的优势

- 基于matplotlib,能够简便的画图

- 独特的数据结构

2.为什么要使用Pandas:

Numpy已经能够帮助我们处理数据,能够结合matplotlib解决部分数据展示等问题,那么pandas学习的目的在什么地方呢?

- 便捷的数据处理能力

- 读取文件方便

- 封装了Matplotlib、Numpy的画图和计算

3. DataFrame:

import numpy as np

stock_change = np.random.normal(0, 1, (10, 5))

stock_change

array([[-0.78146676, -0.29810035, 0.17317068, -0.78727269, -1.13741097],

[-1.64768295, 0.1966735 , -0.40381405, -1.38547391, 1.03162812],

[-0.88359711, -0.51776621, 0.31386734, -0.79209882, -0.75448839],

[ 0.39497997, 0.47411555, -1.22856179, 2.32711195, 0.16330958],

[ 1.71156574, 1.32175126, -0.27637519, -0.1037488 , 0.80180467],

[ 0.16196088, 1.23434847, 0.09890927, 0.39747989, -0.28454071],

[ 1.17218486, 1.57634118, -0.58714471, 1.40127241, 0.19774915],

[ 0.76779403, 1.44145798, -1.36100164, 0.44464079, -0.56796337],

[-1.80942914, 1.89610206, -0.37059895, -0.95929575, 0.19099914],

[ 0.53646672, -0.19264632, -1.61610463, 1.27208662, 0.61560309]])

但是这样的数据形式很难看到存储的是什么样的数据,并且也很难获取相应的数据,比如需要获取某个指定股票的数据,就很难去获取!!

问题:如何让数据更有意义的显示?

import pandas as pd

stock_data = pd.DataFrame(stock_change)

stock_data

|

0 |

1 |

2 |

3 |

4 |

| 0 |

-0.781467 |

-0.298100 |

0.173171 |

-0.787273 |

-1.137411 |

| 1 |

-1.647683 |

0.196674 |

-0.403814 |

-1.385474 |

1.031628 |

| 2 |

-0.883597 |

-0.517766 |

0.313867 |

-0.792099 |

-0.754488 |

| 3 |

0.394980 |

0.474116 |

-1.228562 |

2.327112 |

0.163310 |

| 4 |

1.711566 |

1.321751 |

-0.276375 |

-0.103749 |

0.801805 |

| 5 |

0.161961 |

1.234348 |

0.098909 |

0.397480 |

-0.284541 |

| 6 |

1.172185 |

1.576341 |

-0.587145 |

1.401272 |

0.197749 |

| 7 |

0.767794 |

1.441458 |

-1.361002 |

0.444641 |

-0.567963 |

| 8 |

-1.809429 |

1.896102 |

-0.370599 |

-0.959296 |

0.190999 |

| 9 |

0.536467 |

-0.192646 |

-1.616105 |

1.272087 |

0.615603 |

-

增加行索引;

-

增加列索引:

- 股票的日期是一个时间的序列,我们要实现从前往后的时间还要考虑每月的总天数等,不方便。使用pd.date_range():用于生成一组连续的时间序列(暂时了解)

date_range(start=None,end=None, periods=None, freq='B')

start:开始时间

end:结束时间

periods:时间天数

freq:递进单位,默认1天,'B'默认略过周末

help(pd.date_range)

Help on function date_range in module pandas.core.indexes.datetimes:

date_range(start=None, end=None, periods=None, freq=None, tz=None, normalize=False, name=None, closed=None, **kwargs)

Return a fixed frequency DatetimeIndex.

Parameters

----------

start : str or datetime-like, optional

Left bound for generating dates.

end : str or datetime-like, optional

Right bound for generating dates.

periods : integer, optional

Number of periods to generate.

freq : str or DateOffset, default 'D'

Frequency strings can have multiples, e.g. '5H'. See

:ref:`here ` for a list of

frequency aliases.

tz : str or tzinfo, optional

Time zone name for returning localized DatetimeIndex, for example

'Asia/Hong_Kong'. By default, the resulting DatetimeIndex is

timezone-naive.

normalize : bool, default False

Normalize start/end dates to midnight before generating date range.

name : str, default None

Name of the resulting DatetimeIndex.

closed : {None, 'left', 'right'}, optional

Make the interval closed with respect to the given frequency to

the 'left', 'right', or both sides (None, the default).

**kwargs

For compatibility. Has no effect on the result.

Returns

-------

rng : DatetimeIndex

See Also

--------

DatetimeIndex : An immutable container for datetimes.

timedelta_range : Return a fixed frequency TimedeltaIndex.

period_range : Return a fixed frequency PeriodIndex.

interval_range : Return a fixed frequency IntervalIndex.

Notes

-----

Of the four parameters ``start``, ``end``, ``periods``, and ``freq``,

exactly three must be specified. If ``freq`` is omitted, the resulting

``DatetimeIndex`` will have ``periods`` linearly spaced elements between

``start`` and ``end`` (closed on both sides).

To learn more about the frequency strings, please see `this link

`__.

Examples

--------

**Specifying the values**

The next four examples generate the same `DatetimeIndex`, but vary

the combination of `start`, `end` and `periods`.

Specify `start` and `end`, with the default daily frequency.

>>> pd.date_range(start='1/1/2018', end='1/08/2018')

DatetimeIndex(['2018-01-01', '2018-01-02', '2018-01-03', '2018-01-04',

'2018-01-05', '2018-01-06', '2018-01-07', '2018-01-08'],

dtype='datetime64[ns]', freq='D')

Specify `start` and `periods`, the number of periods (days).

>>> pd.date_range(start='1/1/2018', periods=8)

DatetimeIndex(['2018-01-01', '2018-01-02', '2018-01-03', '2018-01-04',

'2018-01-05', '2018-01-06', '2018-01-07', '2018-01-08'],

dtype='datetime64[ns]', freq='D')

Specify `end` and `periods`, the number of periods (days).

>>> pd.date_range(end='1/1/2018', periods=8)

DatetimeIndex(['2017-12-25', '2017-12-26', '2017-12-27', '2017-12-28',

'2017-12-29', '2017-12-30', '2017-12-31', '2018-01-01'],

dtype='datetime64[ns]', freq='D')

Specify `start`, `end`, and `periods`; the frequency is generated

automatically (linearly spaced).

>>> pd.date_range(start='2018-04-24', end='2018-04-27', periods=3)

DatetimeIndex(['2018-04-24 00:00:00', '2018-04-25 12:00:00',

'2018-04-27 00:00:00'],

dtype='datetime64[ns]', freq=None)

**Other Parameters**

Changed the `freq` (frequency) to ``'M'`` (month end frequency).

>>> pd.date_range(start='1/1/2018', periods=5, freq='M')

DatetimeIndex(['2018-01-31', '2018-02-28', '2018-03-31', '2018-04-30',

'2018-05-31'],

dtype='datetime64[ns]', freq='M')

Multiples are allowed

>>> pd.date_range(start='1/1/2018', periods=5, freq='3M')

DatetimeIndex(['2018-01-31', '2018-04-30', '2018-07-31', '2018-10-31',

'2019-01-31'],

dtype='datetime64[ns]', freq='3M')

`freq` can also be specified as an Offset object.

>>> pd.date_range(start='1/1/2018', periods=5, freq=pd.offsets.MonthEnd(3))

DatetimeIndex(['2018-01-31', '2018-04-30', '2018-07-31', '2018-10-31',

'2019-01-31'],

dtype='datetime64[ns]', freq='3M')

Specify `tz` to set the timezone.

>>> pd.date_range(start='1/1/2018', periods=5, tz='Asia/Tokyo')

DatetimeIndex(['2018-01-01 00:00:00+09:00', '2018-01-02 00:00:00+09:00',

'2018-01-03 00:00:00+09:00', '2018-01-04 00:00:00+09:00',

'2018-01-05 00:00:00+09:00'],

dtype='datetime64[ns, Asia/Tokyo]', freq='D')

`closed` controls whether to include `start` and `end` that are on the

boundary. The default includes boundary points on either end.

>>> pd.date_range(start='2017-01-01', end='2017-01-04', closed=None)

DatetimeIndex(['2017-01-01', '2017-01-02', '2017-01-03', '2017-01-04'],

dtype='datetime64[ns]', freq='D')

Use ``closed='left'`` to exclude `end` if it falls on the boundary.

>>> pd.date_range(start='2017-01-01', end='2017-01-04', closed='left')

DatetimeIndex(['2017-01-01', '2017-01-02', '2017-01-03'],

dtype='datetime64[ns]', freq='D')

Use ``closed='right'`` to exclude `start` if it falls on the boundary.

>>> pd.date_range(start='2017-01-01', end='2017-01-04', closed='right')

DatetimeIndex(['2017-01-02', '2017-01-03', '2017-01-04'],

dtype='datetime64[ns]', freq='D')

stock_index = ['股票'+str(i) for i in range(stock_change.shape[0])]

date = pd.date_range('2019-01-01', periods=stock_change.shape[1], freq='B')

data = pd.DataFrame(stock_change, index=stock_index, columns=date)

data

|

2019-01-01 |

2019-01-02 |

2019-01-03 |

2019-01-04 |

2019-01-07 |

| 股票0 |

-0.781467 |

-0.298100 |

0.173171 |

-0.787273 |

-1.137411 |

| 股票1 |

-1.647683 |

0.196674 |

-0.403814 |

-1.385474 |

1.031628 |

| 股票2 |

-0.883597 |

-0.517766 |

0.313867 |

-0.792099 |

-0.754488 |

| 股票3 |

0.394980 |

0.474116 |

-1.228562 |

2.327112 |

0.163310 |

| 股票4 |

1.711566 |

1.321751 |

-0.276375 |

-0.103749 |

0.801805 |

| 股票5 |

0.161961 |

1.234348 |

0.098909 |

0.397480 |

-0.284541 |

| 股票6 |

1.172185 |

1.576341 |

-0.587145 |

1.401272 |

0.197749 |

| 股票7 |

0.767794 |

1.441458 |

-1.361002 |

0.444641 |

-0.567963 |

| 股票8 |

-1.809429 |

1.896102 |

-0.370599 |

-0.959296 |

0.190999 |

| 股票9 |

0.536467 |

-0.192646 |

-1.616105 |

1.272087 |

0.615603 |

4.DataFrame

4.1 DataFrame结构

DataFrame对象既有行索引,又有列索引

- 行索引,表明不同行,横向索引,叫index

- 列索引,表名不同列,纵向索引,叫columns

4.2 DatatFrame的属性

data.index

Index(['股票0', '股票1', '股票2', '股票3', '股票4', '股票5', '股票6', '股票7', '股票8', '股票9'], dtype='object')

data.columns

DatetimeIndex(['2019-01-01', '2019-01-02', '2019-01-03', '2019-01-04',

'2019-01-07'],

dtype='datetime64[ns]', freq='B')

data.shape

(10, 5)

data.values

array([[-0.78146676, -0.29810035, 0.17317068, -0.78727269, -1.13741097],

[-1.64768295, 0.1966735 , -0.40381405, -1.38547391, 1.03162812],

[-0.88359711, -0.51776621, 0.31386734, -0.79209882, -0.75448839],

[ 0.39497997, 0.47411555, -1.22856179, 2.32711195, 0.16330958],

[ 1.71156574, 1.32175126, -0.27637519, -0.1037488 , 0.80180467],

[ 0.16196088, 1.23434847, 0.09890927, 0.39747989, -0.28454071],

[ 1.17218486, 1.57634118, -0.58714471, 1.40127241, 0.19774915],

[ 0.76779403, 1.44145798, -1.36100164, 0.44464079, -0.56796337],

[-1.80942914, 1.89610206, -0.37059895, -0.95929575, 0.19099914],

[ 0.53646672, -0.19264632, -1.61610463, 1.27208662, 0.61560309]])

data.T

|

股票0 |

股票1 |

股票2 |

股票3 |

股票4 |

股票5 |

股票6 |

股票7 |

股票8 |

股票9 |

| 2019-01-01 |

-0.781467 |

-1.647683 |

-0.883597 |

0.394980 |

1.711566 |

0.161961 |

1.172185 |

0.767794 |

-1.809429 |

0.536467 |

| 2019-01-02 |

-0.298100 |

0.196674 |

-0.517766 |

0.474116 |

1.321751 |

1.234348 |

1.576341 |

1.441458 |

1.896102 |

-0.192646 |

| 2019-01-03 |

0.173171 |

-0.403814 |

0.313867 |

-1.228562 |

-0.276375 |

0.098909 |

-0.587145 |

-1.361002 |

-0.370599 |

-1.616105 |

| 2019-01-04 |

-0.787273 |

-1.385474 |

-0.792099 |

2.327112 |

-0.103749 |

0.397480 |

1.401272 |

0.444641 |

-0.959296 |

1.272087 |

| 2019-01-07 |

-1.137411 |

1.031628 |

-0.754488 |

0.163310 |

0.801805 |

-0.284541 |

0.197749 |

-0.567963 |

0.190999 |

0.615603 |

4.3 DatatFrame的常用方法:

data.head(5)

|

2019-01-01 |

2019-01-02 |

2019-01-03 |

2019-01-04 |

2019-01-07 |

| 股票0 |

-0.781467 |

-0.298100 |

0.173171 |

-0.787273 |

-1.137411 |

| 股票1 |

-1.647683 |

0.196674 |

-0.403814 |

-1.385474 |

1.031628 |

| 股票2 |

-0.883597 |

-0.517766 |

0.313867 |

-0.792099 |

-0.754488 |

| 股票3 |

0.394980 |

0.474116 |

-1.228562 |

2.327112 |

0.163310 |

| 股票4 |

1.711566 |

1.321751 |

-0.276375 |

-0.103749 |

0.801805 |

data.tail(5)

|

2019-01-01 |

2019-01-02 |

2019-01-03 |

2019-01-04 |

2019-01-07 |

| 股票5 |

0.161961 |

1.234348 |

0.098909 |

0.397480 |

-0.284541 |

| 股票6 |

1.172185 |

1.576341 |

-0.587145 |

1.401272 |

0.197749 |

| 股票7 |

0.767794 |

1.441458 |

-1.361002 |

0.444641 |

-0.567963 |

| 股票8 |

-1.809429 |

1.896102 |

-0.370599 |

-0.959296 |

0.190999 |

| 股票9 |

0.536467 |

-0.192646 |

-1.616105 |

1.272087 |

0.615603 |

4.3 DatatFrame索引的设置

data.index[3] = '股票_3'

正确的方式:

stock_code = ["股票_" + str(i) for i in range(stock_change.shape[0])]

data.index = stock_code

data

|

2019-01-01 |

2019-01-02 |

2019-01-03 |

2019-01-04 |

2019-01-07 |

| 股票_0 |

-0.781467 |

-0.298100 |

0.173171 |

-0.787273 |

-1.137411 |

| 股票_1 |

-1.647683 |

0.196674 |

-0.403814 |

-1.385474 |

1.031628 |

| 股票_2 |

-0.883597 |

-0.517766 |

0.313867 |

-0.792099 |

-0.754488 |

| 股票_3 |

0.394980 |

0.474116 |

-1.228562 |

2.327112 |

0.163310 |

| 股票_4 |

1.711566 |

1.321751 |

-0.276375 |

-0.103749 |

0.801805 |

| 股票_5 |

0.161961 |

1.234348 |

0.098909 |

0.397480 |

-0.284541 |

| 股票_6 |

1.172185 |

1.576341 |

-0.587145 |

1.401272 |

0.197749 |

| 股票_7 |

0.767794 |

1.441458 |

-1.361002 |

0.444641 |

-0.567963 |

| 股票_8 |

-1.809429 |

1.896102 |

-0.370599 |

-0.959296 |

0.190999 |

| 股票_9 |

0.536467 |

-0.192646 |

-1.616105 |

1.272087 |

0.615603 |

重设索引

- reset_index(drop=False)

- 设置新的下标索引

- drop:默认为False,不删除原来索引,如果为True,删除原来的索引值

data.reset_index()

|

index |

2019-01-01 00:00:00 |

2019-01-02 00:00:00 |

2019-01-03 00:00:00 |

2019-01-04 00:00:00 |

2019-01-07 00:00:00 |

| 0 |

股票_0 |

-0.781467 |

-0.298100 |

0.173171 |

-0.787273 |

-1.137411 |

| 1 |

股票_1 |

-1.647683 |

0.196674 |

-0.403814 |

-1.385474 |

1.031628 |

| 2 |

股票_2 |

-0.883597 |

-0.517766 |

0.313867 |

-0.792099 |

-0.754488 |

| 3 |

股票_3 |

0.394980 |

0.474116 |

-1.228562 |

2.327112 |

0.163310 |

| 4 |

股票_4 |

1.711566 |

1.321751 |

-0.276375 |

-0.103749 |

0.801805 |

| 5 |

股票_5 |

0.161961 |

1.234348 |

0.098909 |

0.397480 |

-0.284541 |

| 6 |

股票_6 |

1.172185 |

1.576341 |

-0.587145 |

1.401272 |

0.197749 |

| 7 |

股票_7 |

0.767794 |

1.441458 |

-1.361002 |

0.444641 |

-0.567963 |

| 8 |

股票_8 |

-1.809429 |

1.896102 |

-0.370599 |

-0.959296 |

0.190999 |

| 9 |

股票_9 |

0.536467 |

-0.192646 |

-1.616105 |

1.272087 |

0.615603 |

- 以某列值设置为新的索引

- set_index(keys, drop=True)

- keys : 列索引名成或者列索引名称的列表

- drop : boolean, default True.当做新的索引,删除原来的列

设置新索引案例:

df = pd.DataFrame({'month': [12, 3, 6, 9],

'year': [2013, 2014, 2014, 2014],

'sale':[55, 40, 84, 31]})

df

|

month |

year |

sale |

| 0 |

12 |

2013 |

55 |

| 1 |

3 |

2014 |

40 |

| 2 |

6 |

2014 |

84 |

| 3 |

9 |

2014 |

31 |

df.set_index('month')

|

year |

sale |

| month |

|

|

| 12 |

2013 |

55 |

| 3 |

2014 |

40 |

| 6 |

2014 |

84 |

| 9 |

2014 |

31 |

df.set_index(keys = ['year', 'month'])

|

|

sale |

| year |

month |

|

| 2013 |

12 |

55 |

| 2014 |

3 |

40 |

| 6 |

84 |

| 9 |

31 |

df.set_index(keys = ['year', 'month']).index

MultiIndex([(2013, 12),

(2014, 3),

(2014, 6),

(2014, 9)],

names=['year', 'month'])

- 注:通过刚才的设置,这样DataFrame就变成了一个具有MultiIndex的DataFrame。

4.4 MultiIndex与Panel

1.MultiIndex

多级或分层索引对象。

- index属性

- names:levels的名称

- levels:每个level的元组值

df.set_index(keys = ['year', 'month']).index.names

FrozenList(['year', 'month'])

df.set_index(keys = ['year', 'month']).index.levels

FrozenList([[2013, 2014], [3, 6, 9, 12]])

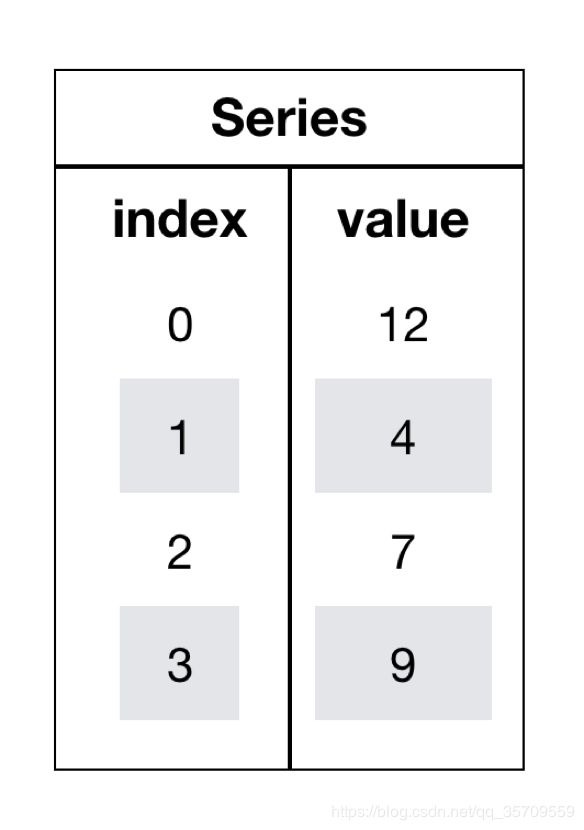

4.5 series对象:

df

|

month |

year |

sale |

| 0 |

12 |

2013 |

55 |

| 1 |

3 |

2014 |

40 |

| 2 |

6 |

2014 |

84 |

| 3 |

9 |

2014 |

31 |

type(df)

pandas.core.frame.DataFrame

ser = df['sale']

ser

0 55

1 40

2 84

3 31

Name: sale, dtype: int64

type(ser)

pandas.core.series.Series

ser.index

RangeIndex(start=0, stop=4, step=1)

ser.values

array([55, 40, 84, 31])

1.创建series:

通过已有数据创建

pd.Series(np.arange(10))

pd.Series([6.7, 5.6, 3, 10, 2], index=[1, 2, 3, 4, 5])

通过字典数据创建

pd.Series({'red':100, 'blue':200, 'green': 500, 'yellow':1000})

pd.Series([5,6,7,8,9], index=[1,2,3,4,5])

1 5

2 6

3 7

4 8

5 9

dtype: int64

二、pandas的基本操作:

为了更好的理解这些基本操作,将读取一个真实的股票数据。关于文件操作,后面在介绍,这里只先用一下API:

1. 读取数据:

import pandas as pd

data = pd.read_csv("./stock_day/stock_day.csv")

data = data.drop(["ma5","ma10","ma20","v_ma5","v_ma10","v_ma20"], axis=1)

data

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

36105.01 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

23331.04 |

0.44 |

2.05 |

0.58 |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

| 2015-03-06 |

13.17 |

14.48 |

14.28 |

13.13 |

179831.72 |

1.12 |

8.51 |

6.16 |

| 2015-03-05 |

12.88 |

13.45 |

13.16 |

12.87 |

93180.39 |

0.26 |

2.02 |

3.19 |

| 2015-03-04 |

12.80 |

12.92 |

12.90 |

12.61 |

67075.44 |

0.20 |

1.57 |

2.30 |

| 2015-03-03 |

12.52 |

13.06 |

12.70 |

12.52 |

139071.61 |

0.18 |

1.44 |

4.76 |

| 2015-03-02 |

12.25 |

12.67 |

12.52 |

12.20 |

96291.73 |

0.32 |

2.62 |

3.30 |

643 rows × 8 columns

data.columns

Index(['open', 'high', 'close', 'low', 'volume', 'price_change', 'p_change',

'turnover'],

dtype='object')

data.index

Index(['2018-02-27', '2018-02-26', '2018-02-23', '2018-02-22', '2018-02-14',

'2018-02-13', '2018-02-12', '2018-02-09', '2018-02-08', '2018-02-07',

...

'2015-03-13', '2015-03-12', '2015-03-11', '2015-03-10', '2015-03-09',

'2015-03-06', '2015-03-05', '2015-03-04', '2015-03-03', '2015-03-02'],

dtype='object', length=643)

1.1 索引操作

Numpy当中我们已经讲过使用索引选取序列和切片选择,pandas也支持类似的操作,也可以直接使用列名、行名

称,甚至组合使用。

1.直接使用行列索引:(先列后行)

data["close"]

2018-02-27 24.16

2018-02-26 23.53

2018-02-23 22.82

2018-02-22 22.28

2018-02-14 21.92

...

2015-03-06 14.28

2015-03-05 13.16

2015-03-04 12.90

2015-03-03 12.70

2015-03-02 12.52

Name: close, Length: 643, dtype: float64

data.open

2018-02-27 23.53

2018-02-26 22.80

2018-02-23 22.88

2018-02-22 22.25

2018-02-14 21.49

...

2015-03-06 13.17

2015-03-05 12.88

2015-03-04 12.80

2015-03-03 12.52

2015-03-02 12.25

Name: open, Length: 643, dtype: float64

data.open[0]

23.53

data.open[:10]

2018-02-27 23.53

2018-02-26 22.80

2018-02-23 22.88

2018-02-22 22.25

2018-02-14 21.49

2018-02-13 21.40

2018-02-12 20.70

2018-02-09 21.20

2018-02-08 21.79

2018-02-07 22.69

Name: open, dtype: float64

data[['close','open']].head()

|

close |

open |

| 2018-02-27 |

24.16 |

23.53 |

| 2018-02-26 |

23.53 |

22.80 |

| 2018-02-23 |

22.82 |

22.88 |

| 2018-02-22 |

22.28 |

22.25 |

| 2018-02-14 |

21.92 |

21.49 |

2.先列后行的索引方式

结合loc或者iloc使用索引

- iloc: 通过索引角标进行索引,通过索引角标完成索引,也支持切片

- loc: 通过索引名称完成索引,也支持切片;

- ix: 混合索引,既能够支持索引角标,也能支持索引名称 (被废弃)

data.iloc[:2]

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

1.53 |

data.iloc[:2,:3]

|

open |

high |

close |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

data.iloc[:2,3]

2018-02-27 23.53

2018-02-26 22.80

Name: low, dtype: float64

data.iloc[-2]

open 12.52

high 13.06

close 12.70

low 12.52

volume 139071.61

price_change 0.18

p_change 1.44

turnover 4.76

Name: 2015-03-03, dtype: float64

data.loc[:"2018-02-14", 'open':'close']

|

open |

high |

close |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

data.ix[:4, 'open':'close']

/home/chengfei/miniconda3/envs/jupyter/lib/python3.6/site-packages/ipykernel_launcher.py:1: FutureWarning:

.ix is deprecated. Please use

.loc for label based indexing or

.iloc for positional indexing

See the documentation here:

http://pandas.pydata.org/pandas-docs/stable/user_guide/indexing.html#ix-indexer-is-deprecated

"""Entry point for launching an IPython kernel.

/home/chengfei/miniconda3/envs/jupyter/lib/python3.6/site-packages/pandas/core/indexing.py:822: FutureWarning:

.ix is deprecated. Please use

.loc for label based indexing or

.iloc for positional indexing

See the documentation here:

http://pandas.pydata.org/pandas-docs/stable/user_guide/indexing.html#ix-indexer-is-deprecated

retval = getattr(retval, self.name)._getitem_axis(key, axis=i)

|

open |

high |

close |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

1.2 赋值操作:

对DataFrame当中的close列进行重新赋值为1

data['close'] = 1

data.close = 1

1.3 排序操作:

排序有两种形式,一种对内容进行排序,一种对索引进行排序

DataFrame:

- 使用df.sort_values(key=, ascending=)对内容进行排序

- 单个键或者多个键进行排序,默认升序

- ascending=False:降序

- ascending=True:升序

- 使用df.sort_index对索引进行排序

1. df.sort_index():

data.head()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

36105.01 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

23331.04 |

0.44 |

2.05 |

0.58 |

data.head().sort_index()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

23331.04 |

0.44 |

2.05 |

0.58 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

36105.01 |

0.36 |

1.64 |

0.90 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |

1.32 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

1.53 |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

2.39 |

data.head().sort_index(ascending=False)

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

36105.01 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

23331.04 |

0.44 |

2.05 |

0.58 |

help(data.sort_values)

Help on method sort_values in module pandas.core.frame:

sort_values(by, axis=0, ascending=True, inplace=False, kind='quicksort', na_position='last') method of pandas.core.frame.DataFrame instance

Sort by the values along either axis.

Parameters

----------

by : str or list of str

Name or list of names to sort by.

- if `axis` is 0 or `'index'` then `by` may contain index

levels and/or column labels

- if `axis` is 1 or `'columns'` then `by` may contain column

levels and/or index labels

.. versionchanged:: 0.23.0

Allow specifying index or column level names.

axis : {0 or 'index', 1 or 'columns'}, default 0

Axis to be sorted.

ascending : bool or list of bool, default True

Sort ascending vs. descending. Specify list for multiple sort

orders. If this is a list of bools, must match the length of

the by.

inplace : bool, default False

If True, perform operation in-place.

kind : {'quicksort', 'mergesort', 'heapsort'}, default 'quicksort'

Choice of sorting algorithm. See also ndarray.np.sort for more

information. `mergesort` is the only stable algorithm. For

DataFrames, this option is only applied when sorting on a single

column or label.

na_position : {'first', 'last'}, default 'last'

Puts NaNs at the beginning if `first`; `last` puts NaNs at the

end.

Returns

-------

sorted_obj : DataFrame or None

DataFrame with sorted values if inplace=False, None otherwise.

Examples

--------

>>> df = pd.DataFrame({

... 'col1': ['A', 'A', 'B', np.nan, 'D', 'C'],

... 'col2': [2, 1, 9, 8, 7, 4],

... 'col3': [0, 1, 9, 4, 2, 3],

... })

>>> df

col1 col2 col3

0 A 2 0

1 A 1 1

2 B 9 9

3 NaN 8 4

4 D 7 2

5 C 4 3

Sort by col1

>>> df.sort_values(by=['col1'])

col1 col2 col3

0 A 2 0

1 A 1 1

2 B 9 9

5 C 4 3

4 D 7 2

3 NaN 8 4

Sort by multiple columns

>>> df.sort_values(by=['col1', 'col2'])

col1 col2 col3

1 A 1 1

0 A 2 0

2 B 9 9

5 C 4 3

4 D 7 2

3 NaN 8 4

Sort Descending

>>> df.sort_values(by='col1', ascending=False)

col1 col2 col3

4 D 7 2

5 C 4 3

2 B 9 9

0 A 2 0

1 A 1 1

3 NaN 8 4

Putting NAs first

>>> df.sort_values(by='col1', ascending=False, na_position='first')

col1 col2 col3

3 NaN 8 4

4 D 7 2

5 C 4 3

2 B 9 9

0 A 2 0

1 A 1 1

2. df.sort_values()

data.head(10).sort_values(by="close",ascending=False)

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

36105.01 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

23331.04 |

0.44 |

2.05 |

0.58 |

| 2018-02-08 |

21.79 |

22.09 |

21.88 |

21.75 |

27068.16 |

0.09 |

0.41 |

0.68 |

| 2018-02-07 |

22.69 |

23.11 |

21.80 |

21.29 |

53853.25 |

-0.50 |

-2.24 |

1.35 |

| 2018-02-13 |

21.40 |

21.90 |

21.48 |

21.31 |

30802.45 |

0.28 |

1.32 |

0.77 |

| 2018-02-12 |

20.70 |

21.40 |

21.19 |

20.63 |

32445.39 |

0.82 |

4.03 |

0.81 |

| 2018-02-09 |

21.20 |

21.46 |

20.36 |

20.19 |

54304.01 |

-1.50 |

-6.86 |

1.36 |

data.head(10).sort_values(by=["close","open"],ascending=False)

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

36105.01 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

23331.04 |

0.44 |

2.05 |

0.58 |

| 2018-02-08 |

21.79 |

22.09 |

21.88 |

21.75 |

27068.16 |

0.09 |

0.41 |

0.68 |

| 2018-02-07 |

22.69 |

23.11 |

21.80 |

21.29 |

53853.25 |

-0.50 |

-2.24 |

1.35 |

| 2018-02-13 |

21.40 |

21.90 |

21.48 |

21.31 |

30802.45 |

0.28 |

1.32 |

0.77 |

| 2018-02-12 |

20.70 |

21.40 |

21.19 |

20.63 |

32445.39 |

0.82 |

4.03 |

0.81 |

| 2018-02-09 |

21.20 |

21.46 |

20.36 |

20.19 |

54304.01 |

-1.50 |

-6.86 |

1.36 |

三、DataFrame运算:

1. 算术运算

- DataFrame.add(other):数学运算加上具体的一个数字

- DataFrame.sub(other):减

- DataFrame.mul(other):乘

- DataFrame.div(other):除

- DataFrame.truediv(other): 浮动除法

- DataFrame.floordiv(other): 整数除法

- DataFrame.mod(other):模运算

- DataFrame.pow(other):幂运算

import numpy as np

import pandas as pd

df = pd.DataFrame(data=np.arange(16).reshape(4,4), index = list("ABCD"))

df

|

0 |

1 |

2 |

3 |

| A |

0 |

1 |

2 |

3 |

| B |

4 |

5 |

6 |

7 |

| C |

8 |

9 |

10 |

11 |

| D |

12 |

13 |

14 |

15 |

df + 1

|

0 |

1 |

2 |

3 |

| A |

1 |

2 |

3 |

4 |

| B |

5 |

6 |

7 |

8 |

| C |

9 |

10 |

11 |

12 |

| D |

13 |

14 |

15 |

16 |

df.add(1)

|

0 |

1 |

2 |

3 |

| A |

1 |

2 |

3 |

4 |

| B |

5 |

6 |

7 |

8 |

| C |

9 |

10 |

11 |

12 |

| D |

13 |

14 |

15 |

16 |

2. 逻辑运算:

2.1 条件判断:

df>10

|

0 |

1 |

2 |

3 |

| A |

False |

False |

False |

False |

| B |

False |

False |

False |

False |

| C |

False |

False |

False |

True |

| D |

True |

True |

True |

True |

2.2 布尔索引

df[df>10]

|

0 |

1 |

2 |

3 |

| A |

NaN |

NaN |

NaN |

NaN |

| B |

NaN |

NaN |

NaN |

NaN |

| C |

NaN |

NaN |

NaN |

11.0 |

| D |

12.0 |

13.0 |

14.0 |

15.0 |

2.3 布尔赋值

df[df>10] = 1000

df

|

0 |

1 |

2 |

3 |

| A |

0 |

1 |

2 |

3 |

| B |

4 |

5 |

6 |

7 |

| C |

8 |

9 |

10 |

1000 |

| D |

1000 |

1000 |

1000 |

1000 |

data.head()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

36105.01 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

23331.04 |

0.44 |

2.05 |

0.58 |

data = data.astype('float64')

data[(data.close > 21.5) & (data.close < 23) ].head(10)

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

36105.01 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

23331.04 |

0.44 |

2.05 |

0.58 |

| 2018-02-08 |

21.79 |

22.09 |

21.88 |

21.75 |

27068.16 |

0.09 |

0.41 |

0.68 |

| 2018-02-07 |

22.69 |

23.11 |

21.80 |

21.29 |

53853.25 |

-0.50 |

-2.24 |

1.35 |

| 2018-02-06 |

22.80 |

23.55 |

22.29 |

22.20 |

55555.00 |

-0.97 |

-4.17 |

1.39 |

| 2018-02-02 |

22.40 |

22.70 |

22.62 |

21.53 |

33242.11 |

0.20 |

0.89 |

0.83 |

| 2018-02-01 |

23.71 |

23.86 |

22.42 |

22.22 |

66414.64 |

-1.30 |

-5.48 |

1.66 |

| 2018-01-03 |

22.42 |

22.83 |

22.79 |

22.18 |

74687.10 |

0.38 |

1.70 |

1.87 |

| 2018-01-02 |

22.30 |

22.54 |

22.42 |

22.05 |

42677.76 |

0.12 |

0.54 |

1.07 |

2.4 逻辑运算函数:

- query(expr)

- expr:查询字符串

通过query使得刚才的过程更加方便简单

data.query("p_change > 2 & turnover > 15")

data.query('close>21.5 & open < 23' ).head()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

36105.01 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

23331.04 |

0.44 |

2.05 |

0.58 |

| 2018-02-08 |

21.79 |

22.09 |

21.88 |

21.75 |

27068.16 |

0.09 |

0.41 |

0.68 |

data.close.isin([23.53,21.92]).head(10)

2018-02-27 False

2018-02-26 True

2018-02-23 False

2018-02-22 False

2018-02-14 True

2018-02-13 False

2018-02-12 False

2018-02-09 False

2018-02-08 False

2018-02-07 False

Name: close, dtype: bool

3.统计运算:

3.1describe()

综合分析: 能够直接得出很多统计结果,count, mean, std, min, max 等

data.describe()

data.describe()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| count |

643.000000 |

643.000000 |

643.000000 |

643.000000 |

643.000000 |

643.000000 |

643.000000 |

643.000000 |

| mean |

21.272706 |

21.900513 |

21.336267 |

20.771835 |

99905.519114 |

0.018802 |

0.190280 |

2.936190 |

| std |

3.930973 |

4.077578 |

3.942806 |

3.791968 |

73879.119354 |

0.898476 |

4.079698 |

2.079375 |

| min |

12.250000 |

12.670000 |

12.360000 |

12.200000 |

1158.120000 |

-3.520000 |

-10.030000 |

0.040000 |

| 25% |

19.000000 |

19.500000 |

19.045000 |

18.525000 |

48533.210000 |

-0.390000 |

-1.850000 |

1.360000 |

| 50% |

21.440000 |

21.970000 |

21.450000 |

20.980000 |

83175.930000 |

0.050000 |

0.260000 |

2.500000 |

| 75% |

23.400000 |

24.065000 |

23.415000 |

22.850000 |

127580.055000 |

0.455000 |

2.305000 |

3.915000 |

| max |

34.990000 |

36.350000 |

35.210000 |

34.010000 |

501915.410000 |

3.030000 |

10.030000 |

12.560000 |

3.2 统计函数

Numpy当中已经详细介绍,在这里演示min(最小值), max(最大值), mean(平均值), median(中位数), var(方差), std(标准差)结果,

| count |

Number of non-NA observations |

说明 |

| sum |

Sum of values |

求和 |

| mean |

Mean of values |

平均值 |

| median |

Arithmetic median of values |

中位数 |

| min |

Minimum |

最小值 |

| max |

Maximum |

最大值 |

| mode |

Mode |

|

| abs |

Absolute Value |

绝对值 |

| prod |

Product of values |

累积 |

| std |

Bessel-corrected sample standard deviation |

标准差 |

| var |

Unbiased variance |

方差 |

| idxmax |

compute the index labels with the maximum |

最大值的索引标签 |

| idxmin |

compute the index labels with the minimum |

最小值的索引标签 |

data.max()

open 34.99

high 36.35

close 35.21

low 34.01

volume 501915.41

price_change 3.03

p_change 10.03

turnover 12.56

dtype: float64

data.max(axis=1).head(10)

2018-02-27 95578.03

2018-02-26 60985.11

2018-02-23 52914.01

2018-02-22 36105.01

2018-02-14 23331.04

2018-02-13 30802.45

2018-02-12 32445.39

2018-02-09 54304.01

2018-02-08 27068.16

2018-02-07 53853.25

dtype: float64

3.4 累计统计函数

| 函数 |

作用 |

| cumsum |

计算前1/2/3/…/n个数的和 |

| cummax |

计算前1/2/3/…/n个数的最大值 |

| cummin |

计算前1/2/3/…/n个数的最小值 |

| cumprod |

计算前1/2/3/…/n个数的积 |

1.累计求和:

data.head()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

36105.01 |

0.36 |

1.64 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

23331.04 |

0.44 |

2.05 |

0.58 |

data.cumsum().head()

|

open |

high |

close |

low |

volume |

price_change |

p_change |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

2.39 |

| 2018-02-26 |

46.33 |

49.66 |

47.69 |

46.33 |

156563.14 |

1.32 |

5.70 |

3.92 |

| 2018-02-23 |

69.21 |

73.03 |

70.51 |

69.04 |

209477.15 |

1.86 |

8.12 |

5.24 |

| 2018-02-22 |

91.46 |

95.79 |

92.79 |

91.06 |

245582.16 |

2.22 |

9.76 |

6.14 |

| 2018-02-14 |

112.95 |

117.78 |

114.71 |

112.54 |

268913.20 |

2.66 |

11.81 |

6.72 |

data = pd.read_csv('./stock_day.csv')

data

|

open |

high |

close |

low |

volume |

price_change |

p_change |

ma5 |

ma10 |

ma20 |

v_ma5 |

v_ma10 |

v_ma20 |

turnover |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

95578.03 |

0.63 |

2.68 |

22.942 |

22.142 |

22.875 |

53782.64 |

46738.65 |

55576.11 |

2.39 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

60985.11 |

0.69 |

3.02 |

22.406 |

21.955 |

22.942 |

40827.52 |

42736.34 |

56007.50 |

1.53 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

52914.01 |

0.54 |

2.42 |

21.938 |

21.929 |

23.022 |

35119.58 |

41871.97 |

56372.85 |

1.32 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

36105.01 |

0.36 |

1.64 |

21.446 |

21.909 |

23.137 |

35397.58 |

39904.78 |

60149.60 |

0.90 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

23331.04 |

0.44 |

2.05 |

21.366 |

21.923 |

23.253 |

33590.21 |

42935.74 |

61716.11 |

0.58 |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

| 2015-03-06 |

13.17 |

14.48 |

14.28 |

13.13 |

179831.72 |

1.12 |

8.51 |

13.112 |

13.112 |

13.112 |

115090.18 |

115090.18 |

115090.18 |

6.16 |

| 2015-03-05 |

12.88 |

13.45 |

13.16 |

12.87 |

93180.39 |

0.26 |

2.02 |

12.820 |

12.820 |

12.820 |

98904.79 |

98904.79 |

98904.79 |

3.19 |

| 2015-03-04 |

12.80 |

12.92 |

12.90 |

12.61 |

67075.44 |

0.20 |

1.57 |

12.707 |

12.707 |

12.707 |

100812.93 |

100812.93 |

100812.93 |

2.30 |

| 2015-03-03 |

12.52 |

13.06 |

12.70 |

12.52 |

139071.61 |

0.18 |

1.44 |

12.610 |

12.610 |

12.610 |

117681.67 |

117681.67 |

117681.67 |

4.76 |

| 2015-03-02 |

12.25 |

12.67 |

12.52 |

12.20 |

96291.73 |

0.32 |

2.62 |

12.520 |

12.520 |

12.520 |

96291.73 |

96291.73 |

96291.73 |

3.30 |

643 rows × 14 columns

data.price_change.sort_index().cumsum()

2015-03-02 0.32

2015-03-03 0.50

2015-03-04 0.70

2015-03-05 0.96

2015-03-06 2.08

...

2018-02-14 9.87

2018-02-22 10.23

2018-02-23 10.77

2018-02-26 11.46

2018-02-27 12.09

Name: price_change, Length: 643, dtype: float64

import matplotlib.pyplot as plt

data.price_change.sort_index().cumsum().plot()

plt.show()

3.5 自定义运算

- apply(func, axis=0)

- func:自定义函数

- axis=0:默认是列,axis=1为行进行运算

- 定义一个对列,最大值-最小值的函数

data[['open', 'close']].apply(lambda x: x.max() - x.min(), axis=0)

open 22.74

close 22.85

dtype: float64

data.apply(lambda x:x.max() - x.min(), axis=0)

open 22.740

high 23.680

close 22.850

low 21.810

volume 500757.290

price_change 6.550

p_change 20.060

ma5 21.176

ma10 19.666

ma20 17.478

v_ma5 393638.800

v_ma10 340897.650

v_ma20 245969.790

turnover 12.520

dtype: float64

四、panads画图:

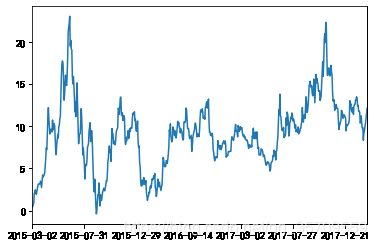

1.pandas.DataFrame.plot

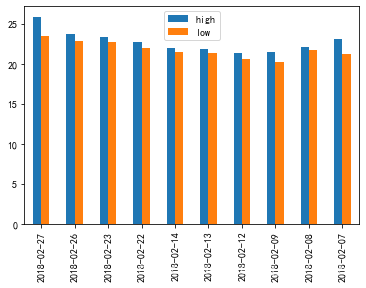

ret = data[['high', 'low']]

ret.plot()

ret[:10].plot(kind='bar')

plt.show()

data.price_change.plot(kind='hist', figsize=(20,10))

plt.show()

2 pandas.Series.plot

更多参数细节:https://pandas.pydata.org/pandas-docs/stable/generated/pandas.Series.plot.html?highlight=plot#pandas.Series.plot

import pandas as pd

import matplotlib.pyplot as plt

pd.plotting.scatter_matrix(data,figsize=(20,10))

plt.show()

pd.plotting.scatter_matrix(data.iloc[:,:10],figsize=(20,10))

plt.show()

五、文件读取与存储:

数据大部分存在于文件当中,所以pandas会支持复杂的IO操作,pandas的API支持众多的文件格式,如CSV、SQL、XLS、JSON、HDF5。

| format type |

data description |

reader |

writer |

| text |

CSV |

read_csv |

to_csv |

| text |

JSON |

read_json |

to_json |

| text |

HTML |

read_html |

to_html |

| text |

local clipboard |

read_clipboard |

to_clipboard |

| binary |

MS Excel |

read_excel |

to_excel |

| binary |

HDF5 Format |

read_hdf |

to_hdf |

| binary |

Feather Format |

read_feather |

to_feather |

| binary |

Parquet Format |

read_parquet |

to_parquet |

| binary |

Msgpack |

read_msgpack |

to_msgpack |

| binary |

Stata |

read_stata |

to_stata |

| binary |

SAS |

read_sas |

|

| binary |

Python Pickle Format |

read_pickle |

to_pickle |

| SQL |

SQL |

read_sql |

to_sql |

| SQL |

Google Big Query |

read_gbq |

to_gbq |

1.CSV

1.1 读取csv文件-read_csv

- pandas.read_csv(filepath_or_buffer, sep =’,’ , delimiter = None)

- filepath_or_buffer:文件路径

- usecols:指定读取的列名,列表形式

import pandas as pd

data = pd.read_csv("./stock_day/stock_day.csv", usecols=['open', 'high', 'close','low'])

data.head(10)

|

open |

high |

close |

low |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

| 2018-02-13 |

21.40 |

21.90 |

21.48 |

21.31 |

| 2018-02-12 |

20.70 |

21.40 |

21.19 |

20.63 |

| 2018-02-09 |

21.20 |

21.46 |

20.36 |

20.19 |

| 2018-02-08 |

21.79 |

22.09 |

21.88 |

21.75 |

| 2018-02-07 |

22.69 |

23.11 |

21.80 |

21.29 |

1.2 写入csv文件-to_csv

-

DataFrame.to_csv(path_or_buf=None, sep=’, ’, columns=None, header=True, index=True, index_label=None, mode=‘w’, encoding=None)

- path_or_buf :string or file handle, default None

- sep :character, default ‘,’

- columns :sequence, optional

- mode:‘w’:重写, ‘a’ 追加

- index:是否写进行索引

- header :boolean or list of string, default True,是否写进列索引值

-

Series.to_csv(path=None, index=True, sep=’, ‘, na_rep=’’, float_format=None, header=False, index_label=None, mode=‘w’, encoding=None, compression=None, date_format=None, decimal=’.’)

Write Series to a comma-separated values (csv) file

ret.head().to_csv("./test.csv")

ret = pd.read_csv("./test.csv")

ret

|

Unnamed: 0 |

high |

low |

| 0 |

2018-02-27 |

25.88 |

23.53 |

| 1 |

2018-02-26 |

23.78 |

22.80 |

| 2 |

2018-02-23 |

23.37 |

22.71 |

| 3 |

2018-02-22 |

22.76 |

22.02 |

| 4 |

2018-02-14 |

21.99 |

21.48 |

会发现将索引存入到文件当中,变成单独的一列数据。如果需要删除,可以指定index参数,删除原来的文件,重新保存一次。

ret.set_index("Unnamed: 0")

|

high |

low |

| Unnamed: 0 |

|

|

| 2018-02-27 |

25.88 |

23.53 |

| 2018-02-26 |

23.78 |

22.80 |

| 2018-02-23 |

23.37 |

22.71 |

| 2018-02-22 |

22.76 |

22.02 |

| 2018-02-14 |

21.99 |

21.48 |

ret.head().to_csv("./test.csv", columns=['high'], index=False)

pd.read_csv("./test.csv")

|

high |

| 0 |

25.88 |

| 1 |

23.78 |

| 2 |

23.37 |

| 3 |

22.76 |

| 4 |

21.99 |

stock_day[:10].to_csv("./test.csv", mode='a')

import pandas as pd

ret = pd.read_csv("./stock_day/stock_day.csv", usecols=['open', 'high', 'close','low'])

ret.head().to_csv("./test.csv", mode='a')

ret = pd.read_csv("./test.csv")

ret.set_index("Unnamed: 0")

ret

|

Unnamed: 0 |

open |

high |

close |

low |

| 0 |

2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

| 1 |

2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

| 2 |

2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

| 3 |

2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

| 4 |

2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

又存进了一个列名,所以当以追加方式添加数据的时候,一定要去掉列名columns,指定header=False

import pandas as pd

ret = pd.read_csv("./stock_day/stock_day.csv", usecols=['open', 'high', 'close','low'])

ret.head().to_csv("./test.csv", mode='a',header=False)

ret = pd.read_csv("./test.csv",index_col=0)

ret

|

open |

high |

close |

low |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

| 2018-02-27 |

23.53 |

25.88 |

24.16 |

23.53 |

| 2018-02-26 |

22.80 |

23.78 |

23.53 |

22.80 |

| 2018-02-23 |

22.88 |

23.37 |

22.82 |

22.71 |

| 2018-02-22 |

22.25 |

22.76 |

22.28 |

22.02 |

| 2018-02-14 |

21.49 |

21.99 |

21.92 |

21.48 |

1.3 读取远程的csv

指定names,既列名

names = [f"第{x}列" for x in range(1,12)]

pd.read_csv("url",names = names)

2.HDF5

拓展:

优先选择使用HDF5文件存储

- HDF5在存储的是支持压缩,使用的方式是blosc,这个是速度最快的也是pandas默认支持的

- 使用压缩可以提磁盘利用率,节省空间

- HDF5还是跨平台的,可以轻松迁移到hadoop 上面

2.1 read_hdf与to_hdf

HDF5文件的读取和存储需要指定一个键,值为要存储的DataFrame

- pandas.read_hdf(path_or_buf,key =None,** kwargs)

从h5文件当中读取数据

- path_or_buffer:文件路径

- key:读取的键

- mode:打开文件的模式

- return:Theselected object

- DataFrame.to_hdf(path_or_buf, key, \kwargs)

hdf_data = pd.read_hdf("./stock_data/day/day_close.h5")

ret = hdf_data.iloc[:10,:10]

ret.to_hdf("./test.h5", key="close_10")

ret = pd.read_hdf("./test.h5", key="close_10")

ret

|

000001.SZ |

000002.SZ |

000004.SZ |

000005.SZ |

000006.SZ |

000007.SZ |

000008.SZ |

000009.SZ |

000010.SZ |

000011.SZ |

| 0 |

16.30 |

17.71 |

4.58 |

2.88 |

14.60 |

2.62 |

4.96 |

4.66 |

5.37 |

6.02 |

| 1 |

17.02 |

19.20 |

4.65 |

3.02 |

15.97 |

2.65 |

4.95 |

4.70 |

5.37 |

6.27 |

| 2 |

17.02 |

17.28 |

4.56 |

3.06 |

14.37 |

2.63 |

4.82 |

4.47 |

5.37 |

5.96 |

| 3 |

16.18 |

16.97 |

4.49 |

2.95 |

13.10 |

2.73 |

4.89 |

4.33 |

5.37 |

5.77 |

| 4 |

16.95 |

17.19 |

4.55 |

2.99 |

13.18 |

2.77 |

4.97 |

4.42 |

5.37 |

5.92 |

| 5 |

17.76 |

17.30 |

4.78 |

3.10 |

13.70 |

3.01 |

5.17 |

4.63 |

5.37 |

6.22 |

| 6 |

18.10 |

16.93 |

4.98 |

3.16 |

13.48 |

3.31 |

5.69 |

4.78 |

5.37 |

6.48 |

| 7 |

17.71 |

17.93 |

4.91 |

3.25 |

13.89 |

3.25 |

5.98 |

4.88 |

5.37 |

6.57 |

| 8 |

17.40 |

17.65 |

4.95 |

3.20 |

13.89 |

3.01 |

5.58 |

4.84 |

5.37 |

6.25 |

| 9 |

18.27 |

18.58 |

4.95 |

3.23 |

13.97 |

3.05 |

5.76 |

4.94 |

5.37 |

6.56 |

3.Excel文件的读取:

框架:xlrd

文件后缀:xls、xlsx

3.1 excel文件的读取:

ex_data = pd.read_excel("./scores.xlsx")

ex_data

|

Unnamed: 0 |

一本分数线 |

Unnamed: 2 |

二本分数线 |

Unnamed: 4 |

| 0 |

NaN |

文科 |

理科 |

文科 |

理科 |

| 1 |

2018.0 |

576 |

532 |

488 |

432 |

| 2 |

2017.0 |

555 |

537 |

468 |

439 |

| 3 |

2016.0 |

583 |

548 |

532 |

494 |

| 4 |

2015.0 |

579 |

548 |

527 |

495 |

| 5 |

2014.0 |

565 |

543 |

507 |

495 |

| 6 |

2013.0 |

549 |

550 |

494 |

505 |

| 7 |

2012.0 |

495 |

477 |

446 |

433 |

| 8 |

2011.0 |

524 |

484 |

481 |

435 |

| 9 |

2010.0 |

524 |

494 |

474 |

441 |

| 10 |

2009.0 |

532 |

501 |

489 |

459 |

| 11 |

2008.0 |

515 |

502 |

472 |

455 |

| 12 |

2007.0 |

528 |

531 |

489 |

478 |

| 13 |

2006.0 |

516 |

528 |

476 |

476 |

ex_data = pd.read_excel("./scores.xlsx", header=[0,1],index_col=0)

ex_data

|

一本分数线 |

二本分数线 |

|

文科 |

理科 |

文科 |

理科 |

| 2018 |

576 |

532 |

488 |

432 |

| 2017 |

555 |

537 |

468 |

439 |

| 2016 |

583 |

548 |

532 |

494 |

| 2015 |

579 |

548 |

527 |

495 |

| 2014 |

565 |

543 |

507 |

495 |

| 2013 |

549 |

550 |

494 |

505 |

| 2012 |

495 |

477 |

446 |

433 |

| 2011 |

524 |

484 |

481 |

435 |

| 2010 |

524 |

494 |

474 |

441 |

| 2009 |

532 |

501 |

489 |

459 |

| 2008 |

515 |

502 |

472 |

455 |

| 2007 |

528 |

531 |

489 |

478 |

| 2006 |

516 |

528 |

476 |

476 |

ex_data.一本分数线

|

文科 |

理科 |

| 2018 |

576 |

532 |

| 2017 |

555 |

537 |

| 2016 |

583 |

548 |

| 2015 |

579 |

548 |

| 2014 |

565 |

543 |

| 2013 |

549 |

550 |

| 2012 |

495 |

477 |

| 2011 |

524 |

484 |

| 2010 |

524 |

494 |

| 2009 |

532 |

501 |

| 2008 |

515 |

502 |

| 2007 |

528 |

531 |

| 2006 |

516 |

528 |

ex_data.一本分数线.to_excel("./test.xls")

ex_data2 = pd.read_excel("./test.xls",index_col=0)

ex_data2

4.json数据的读取:

4.1 read_json

help(pd.read_json)

json_data = pd.read_json("./Sarcasm_Headlines_Dataset.json", orient='records',lines=True)

json_data

4.2 to_json

- DataFrame.to_json(path_or_buf=None, orient=None, lines=False)

- 将Pandas 对象存储为json格式

- path_or_buf=None:文件地址

- orient:存储的json形式,{‘split’,’records’,’index’,’columns’,’values’}

- lines:一个对象存储为一行

json_data[:10].to_json("./test.json", orient='records',lines=True)