house price predict

波士顿房价这个项目是我自己在kaggle上做的第二个项目了,第一次自己做只达到前50%,之后看了kaggle上一位大神的思路,对自己的项目进行了改善,例如结合多个基本模型进行预测,果然误差率降低了很多,排名达到前20%,果然跟着大神走不会错。这里只做一个个人的学习总结,之后也会不断再完善。

先说下我的思路:

1. 导入数据

2. 数据处理:

——outliers 关于outliers的处理,应该仔细阅读数据描述,里面有很多关于竞赛的要求。

——目标变量 观察目标变量的分布情况,对于连续型变量

——Feature Engineering ——填补缺失值

——转化变量

——LabelEncoding 变量

——降维

——特征变量偏斜度

3. 建模

——基本模型

——打分

——叠加基本模型

——预测

4. 导出并提交

接下来看具体怎么做:

1. 导入数据并查看数据

train=pd.read_csv('houseprice/train.csv')

test=pd.read_csv('houseprice/test.csv')train.head(5)test.head(5)

2. 数据处理

outliers:

当我阅读kaggle的overview时,发现在description中的Acknowledgment中有个The Ames Housing dataset 的详细介绍,仔细阅读发现在文档中有outliers的线索,所以下一步就是按照文档中要求的,处理outliers。

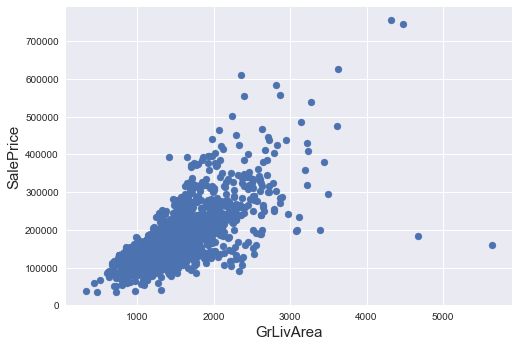

先plot一遍GrLivArea与SalePrice之间的图像,观察有哪些点属于outliers:

fig,ax=plt.subplots()

ax.scatter(x=train['GrLivArea'],y=train['SalePrice'])

plt.xlabel('GrLivArea',fontsize=15)

plt.ylabel('SalePrice',fontsize=15)

plt.show()

通过阅读The Ames Housing dataset 知道应该去除GrLivArea<4000的四个outliers,但我觉得有些大房子确实挺贵,所以像SalePrice>700000的outliers我还是保留下来了。

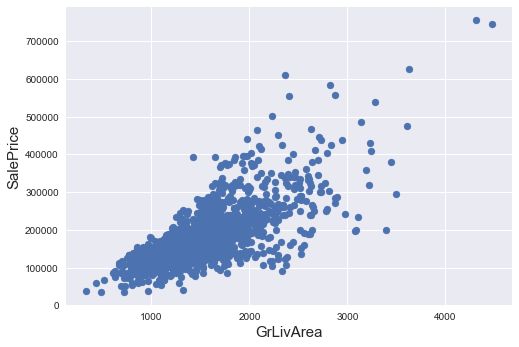

train=train.drop(train[(train['GrLivArea']>4000)&(train['SalePrice']<300000)].index)再plot一遍:

fig,ax=plt.subplots()

ax.scatter(x=train['GrLivArea'],y=train['SalePrice'])

plt.xlabel('GrLivArea',fontsize=15)

plt.ylabel('SalePrice',fontsize=15)

plt.show()

OK,outliers处理完毕。接下来处理目标变量。

目标变量:

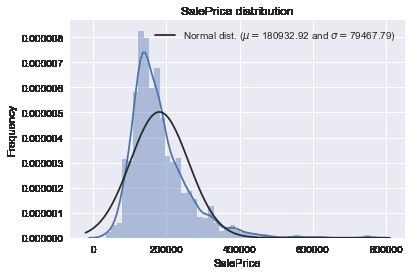

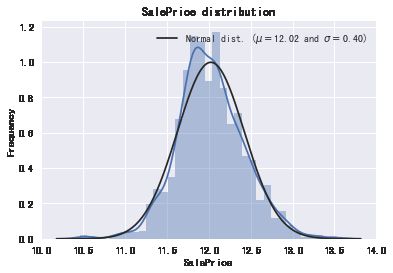

先plot出房价的分布发现房价呈右偏态分布:

sns.distplot(train['SalePrice'],fit=norm)

(mu,sigma)=norm.fit(train['SalePrice'])

print('\n mu={:.2f} and sigma={:.2f}\n'.format(mu,sigma))

plt.legend(['Normal dist. ($\mu=${:.2f} and $\sigma=${:.2f})'.format(mu,sigma)],loc='best')

plt.ylabel('Frequency')

plt.title('SalePrice distribution')![]()

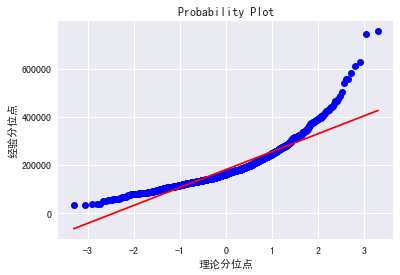

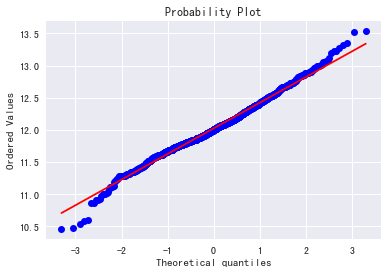

用分位数图看的更明显点:

fig=plt.figure()

res=stats.probplot(train['SalePrice'],plot=plt)

plt.rcParams['font.sans-serif'] = ['SimHei']

plt.rcParams['axes.unicode_minus'] = False

plt.ylabel('经验分位点')

plt.xlabel('理论分位点')

plt.show()

接下来我们在用log处理下salePrice,使它尽可能靠近正态分布。

train['SalePrice']=np.log1p(train['SalePrice'])sns.distplot(train['SalePrice'],fit=norm)

(mu,sigma)=norm.fit(train['SalePrice'])

print('\n mu={:.2f} and sigma={:.2f}\n'.format(mu,sigma))

plt.legend(['Normal dist. ($\mu=${:.2f} and $\sigma=${:.2f})'.format(mu,sigma)],loc='best')

plt.ylabel('Frequency')

plt.title('SalePrice distribution')

fig=plt.figure()

res=stats.probplot(train['SalePrice'],plot=plt)

plt.show()![]()

关联下两个表格接下来要开始特征工程了。

特征工程:

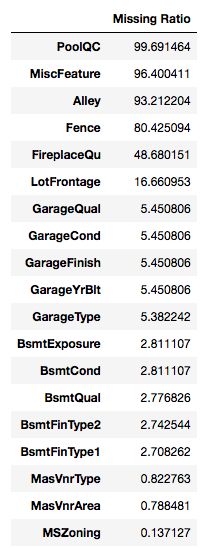

all_data_na=(all_data.isnull().sum()/len(all_data))*100

all_data_na=all_data_na.drop(all_data_na[all_data_na==0].index).sort_values(ascending=False)

missing_data=pd.DataFrame({'Missing Ratio':all_data_na})

missing_data

根据不同的变量进行不同的填充null值:

for col in ('GarageType', 'GarageFinish', 'GarageQual', 'GarageCond','PoolQC','MiscFeature','Alley','Fence',

'FireplaceQu','BsmtExposure','BsmtCond','BsmtQual','BsmtFinType2','BsmtFinType1','MasVnrType'):

all_data[col] = all_data[col].fillna('None')#按照地区分组,用每个地区的中位数填充null值

all_data['LotFrontage']=all_data.groupby('Neighborhood')['LotFrontage'].transform(lambda x: x.fillna(x.median()))for col in ('GarageYrBlt', 'GarageArea', 'GarageCars','BsmtFinSF1', 'BsmtFinSF2', 'BsmtUnfSF',

'TotalBsmtSF', 'BsmtFullBath', 'BsmtHalfBath','MasVnrArea',):

all_data[col] = all_data[col].fillna(0)对于这个特征,其具体值除了一个“NoSeWa”和2个NA之外,所有记录都是“AllPub”,因为认为它对SalePrice影响不大,所以删掉。

all_data = all_data.drop(['Utilities'], axis=1)对于一下这些变量采取众数填充:

all_data['Electrical'] = all_data['Electrical'].fillna(all_data['Electrical'].mode()[0])

all_data['KitchenQual'] = all_data['KitchenQual'].fillna(all_data['KitchenQual'].mode()[0])

all_data['Exterior1st'] = all_data['Exterior1st'].fillna(all_data['Exterior1st'].mode()[0])

all_data['Exterior2nd'] = all_data['Exterior2nd'].fillna(all_data['Exterior2nd'].mode()[0])

all_data['SaleType'] = all_data['SaleType'].fillna(all_data['SaleType'].mode()[0])

all_data['MSZoning'] = all_data['MSZoning'].fillna(all_data['MSZoning'].mode()[0])all_data["Functional"] = all_data["Functional"].fillna("Typ")最后再检查一遍是否还有缺失值:

从特征中提取特征:

先观察是否有要转化类型的特征,例如以下我把一些用数字表示的评估质量等级,以及年份月份都转化成了字符串类型:

all_data['MSSubClass'] = all_data['MSSubClass'].astype(str)

all_data['OverallCond'] = all_data['OverallCond'].astype(str)

all_data['OverallQual'] = all_data['OverallQual'].astype(str)

all_data['YrSold'] = all_data['YrSold'].astype(str)

all_data['MoSold'] = all_data['MoSold'].astype(str)

all_data['GarageYrBlt'] = all_data['GarageYrBlt'].astype(str)

all_data['YearBuilt'] = all_data['YearBuilt'].astype(str)

all_data['YearRemodAdd'] = all_data['YearRemodAdd'].astype(str)然后选取一些可能对房价有影响的字符串类型特征变量,对他们进行labelencoder编码:

from sklearn.preprocessing import LabelEncoder

col=('FireplaceQu', 'BsmtQual', 'BsmtCond', 'GarageQual', 'GarageCond',

'ExterQual', 'ExterCond','HeatingQC', 'PoolQC', 'KitchenQual', 'BsmtFinType1',

'BsmtFinType2', 'Functional', 'Fence', 'BsmtExposure', 'GarageFinish', 'LandSlope',

'LotShape', 'PavedDrive', 'Street', 'Alley', 'CentralAir', 'MSSubClass',

'OverallCond', 'YrSold', 'MoSold','YearBuilt','YearRemodAdd')

for c in col:

lb=LabelEncoder()

lb.fit(all_data[c])

all_data[c]=lb.transform(all_data[c])对一些变量进行类似变量进行降维:

all_data['TotalSF'] = all_data['TotalBsmtSF'] + all_data['1stFlrSF'] + all_data['2ndFlrSF']好了,特征变量都清洗完毕,接下来看下特征变量的分布特征:

这里我用偏斜度来查看特征变量的分布情况(偏斜度绝对值越大,说明变量越偏离正态分布,与房价的线性关系越稀疏。)

numeric_feats = all_data.dtypes[all_data.dtypes != "object"].index

skewed_feats=all_data[numeric_feats].apply(lambda x: skew (x.dropna())).sort_values(ascending=False)

print("\n所有数值型变量的偏斜度:\n")

skewness = pd.DataFrame({'Skew' :skewed_feats})

skewness.head(10)

对于偏斜度绝对值较大(>0.75)的变量进行box-cox转换,从而减小最小二乘系数估计带来的误差;使不符合正态分布的变量更符合正态分布,降低伪拟合的概率:

skewness=skewness[abs(skewness)>0.75]

print("有 {} 个变量需要进行box-cox转换".format(skewness.shape[0]))![]()

from scipy.special import boxcox1p

skewed_feat=skewness.index

lam=0.15

for feat in skewed_feat:

all_data[feat]=boxcox1p(all_data[feat],lam)然后应用到full_data:

all_data = pd.get_dummies(all_data)all_data.head()

特征变量处理完毕,对full_data进行拆分:

train = all_data[:1458]

test = all_data[1459:]开始建模:

为了模型最后的误差尽量小,我用了多种模型来预测,最后参考了kaggle上一个大神自己封装的模型叠加函数,将我使用的模型综合叠加,得出最后的误差率。

from sklearn.linear_model import ElasticNet, Lasso

from sklearn.ensemble import RandomForestRegressor, GradientBoostingRegressor

from sklearn.kernel_ridge import KernelRidge

from sklearn.pipeline import make_pipeline

from sklearn.preprocessing import RobustScaler

from sklearn.base import BaseEstimator, TransformerMixin, RegressorMixin, clone

from sklearn.model_selection import KFold, cross_val_score

from sklearn.metrics import mean_squared_error#采用kfold拆分法进行交叉检验,建立打分系统,命名为rmsle_cv

n_folds = 5

def rmsle_cv(model):

kf = KFold(n_folds, shuffle=True, random_state=42)

kf = kf.get_n_splits(train.values)

rmse= np.sqrt(-cross_val_score(model, train.values, y_train, scoring="neg_mean_squared_error", cv = kf))

return(rmse)#rf=make_pipeline(RobustScaler(),RandomForestRegressor(n_estimators=1000,max_features='sqrt',random_state=3))

#score=rmsle_cv(rf)

#print("\nRandomForestRegressor score: {:.4f} ({:.4f})\n".format(score.mean(), score.std()))

#在前期数据处理时有些outliers的变量,所以这里使用RobustScaler对结果进行处理

lasso = make_pipeline(RobustScaler(), Lasso(alpha =0.0005, random_state=1))

score = rmsle_cv(lasso)

print("\nLasso score: {:.4f} ({:.4f})\n".format(score.mean(), score.std()))

ENet = make_pipeline(RobustScaler(), ElasticNet(alpha=0.0005, l1_ratio=.7, random_state=3))

score = rmsle_cv(ENet)

print("ElasticNet score: {:.4f} ({:.4f})\n".format(score.mean(), score.std()))![]()

KRR = KernelRidge(alpha=0.6, kernel='polynomial', degree=2, coef0=2.5)

score = rmsle_cv(KRR)

print("Kernel Ridge score: {:.4f} ({:.4f})\n".format(score.mean(), score.std()))![]()

GBoost = GradientBoostingRegressor(n_estimators=1000, learning_rate=0.05,

max_depth=4, max_features='sqrt',

min_samples_leaf=15, min_samples_split=10,

loss='huber', random_state =5)

score = rmsle_cv(GBoost)

print("Gradient Boosting score: {:.4f} ({:.4f})\n".format(score.mean(), score.std()))![]()

Gboost的参数配置根据自己的电脑性能来,我一开始将n_estimators设置为3000,差点卡死。

#叠加基础模型class

class AveragingModels(BaseEstimator, RegressorMixin, TransformerMixin):

def __init__(self, models):

self.models = models

# we define clones of the original models to fit the data in

def fit(self, X, y):

self.models_ = [clone(x) for x in self.models]

# Train cloned base models

for model in self.models_:

model.fit(X, y)

return self

#Now we do the predictions for cloned models and average them

def predict(self, X):

predictions = np.column_stack([

model.predict(X) for model in self.models_

])

return np.mean(predictions, axis=1) AverangingModels是我在kaggle一个大神那里看到的,已经封装完成,可以直接把代码考来使用。最后会发现确实结合了多种基础模型的score值会提升空间确实很大。大神链接我已给出。

averaged_models = AveragingModels(models = (ENet, GBoost, KRR, lasso))

score = rmsle_cv(averaged_models)

print(" Averaged base models score: {:.4f} ({:.4f})\n".format(score.mean(), score.std()))![]()

def rmsle(y, y_pred):

return np.sqrt(mean_squared_error(y, y_pred))averaged_models.fit(train.values, y_train)

averaged_train_pred = averaged_models.predict(train.values)

averaged_pred = np.expm1(averaged_models.predict(test.values))

print(rmsle(y_train, averaged_train_pred))sub = pd.DataFrame()

sub['Id'] = test_ID

sub['SalePrice'] = averaged_pred

sub.to_csv('houseprice/submission.csv',index=False)

sub.head()