【时间序列】ARIMA模型 评估标准

%load_ext autoreload

%autoreload 2

%matplotlib inline

%config InlineBackend.figure_format='retina'

from __future__ import absolute_import, division, print_function

import sys

import os

import pandas as pd

import numpy as np

# TSA from Statsmodels

import statsmodels.api as sm

import statsmodels.formula.api as smf

import statsmodels.tsa.api as smt

# Display and Plotting

import matplotlib.pylab as plt

import seaborn as sns

pd.set_option('display.float_format', lambda x: '%.5f' % x) # pandas

np.set_printoptions(precision=5, suppress=True) # numpy

pd.set_option('display.max_columns', 100)

pd.set_option('display.max_rows', 100)

# seaborn plotting style

sns.set(style='ticks', context='poster')

filename_ts = 'data/series1.csv'

ts_df = pd.read_csv(filename_ts, index_col=0, parse_dates=[0])

n_sample = ts_df.shape[0]

n_train=int(0.95*n_sample)+1

n_forecast=n_sample-n_train

#ts_df

ts_train = ts_df.iloc[:n_train]['value']

ts_test = ts_df.iloc[n_train:]['value']

def tsplot(y, lags=None, title='', figsize=(14, 8)):

fig = plt.figure(figsize=figsize)

layout = (2, 2)

ts_ax = plt.subplot2grid(layout, (0, 0))

hist_ax = plt.subplot2grid(layout, (0, 1))

acf_ax = plt.subplot2grid(layout, (1, 0))

pacf_ax = plt.subplot2grid(layout, (1, 1))

y.plot(ax=ts_ax)

ts_ax.set_title(title)

y.plot(ax=hist_ax, kind='hist', bins=25)

hist_ax.set_title('Histogram')

smt.graphics.plot_acf(y, lags=lags, ax=acf_ax)

smt.graphics.plot_pacf(y, lags=lags, ax=pacf_ax)

[ax.set_xlim(0) for ax in [acf_ax, pacf_ax]]

sns.despine()

fig.tight_layout()

return ts_ax, acf_ax, pacf_ax

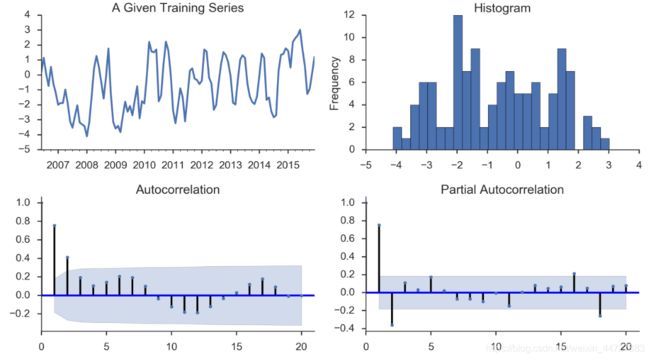

tsplot(ts_train, title='A Given Training Series', lags=20);

#Model Estimation

# Fit the model

arima200 = sm.tsa.SARIMAX(ts_train, order=(2,0,0))

model_results = arima200.fit()

import itertools

p_min = 0

d_min = 0

q_min = 0

p_max = 4

d_max = 0

q_max = 4

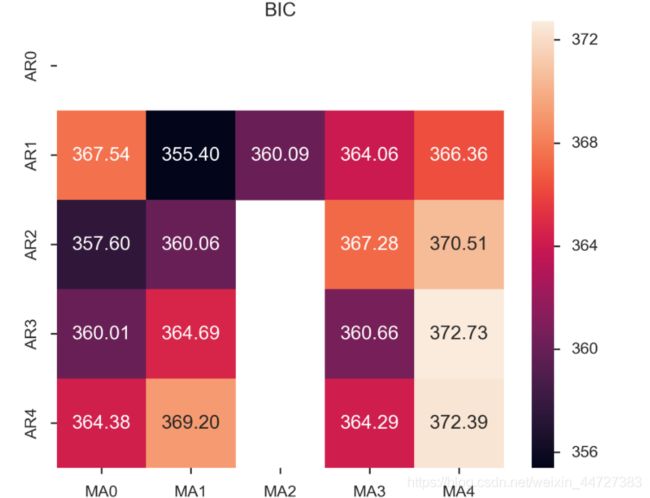

# Initialize a DataFrame to store the results

results_bic = pd.DataFrame(index=['AR{}'.format(i) for i in range(p_min,p_max+1)],

columns=['MA{}'.format(i) for i in range(q_min,q_max+1)])

for p,d,q in itertools.product(range(p_min,p_max+1),

range(d_min,d_max+1),

range(q_min,q_max+1)):

if p==0 and d==0 and q==0:

results_bic.loc['AR{}'.format(p), 'MA{}'.format(q)] = np.nan

continue

try:

model = sm.tsa.SARIMAX(ts_train, order=(p, d, q),

#enforce_stationarity=False,

#enforce_invertibility=False,

)

results = model.fit()

results_bic.loc['AR{}'.format(p), 'MA{}'.format(q)] = results.bic

except:

continue

results_bic = results_bic[results_bic.columns].astype(float)

fig, ax = plt.subplots(figsize=(10, 8))

ax = sns.heatmap(results_bic,

mask=results_bic.isnull(),

ax=ax,

annot=True,

fmt='.2f',

);

ax.set_title('BIC');

AIC(赤池信息准则)、BIC(贝叶斯信息准则)越小越好

# Alternative model selection method, limited to only searching AR and MA parameters

train_results = sm.tsa.arma_order_select_ic(ts_train, ic=['aic', 'bic'], trend='nc', max_ar=4, max_ma=4)

print('AIC', train_results.aic_min_order)

print('BIC', train_results.bic_min_order)

AIC (4, 2)

BIC (1, 1)

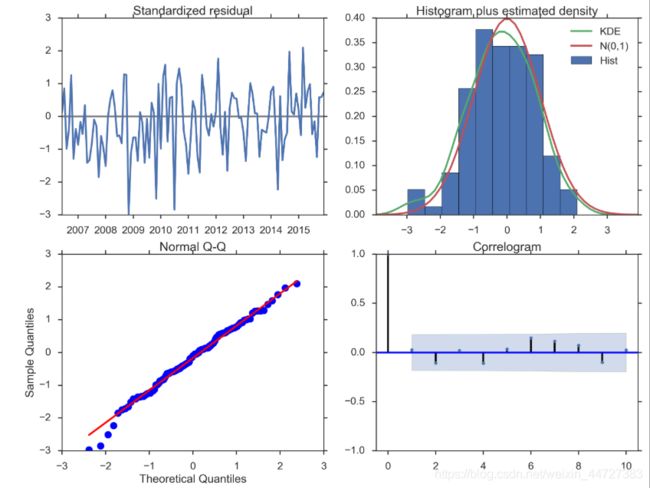

#残差分析 正态分布 QQ图线性

model_results.plot_diagnostics(figsize=(16, 12));